We have a two-day regime shift in the JPY. Can it continue?

The most Canadian thing ever.

We have a two-day regime shift in the JPY. Can it continue?

The most Canadian thing ever.

Flat

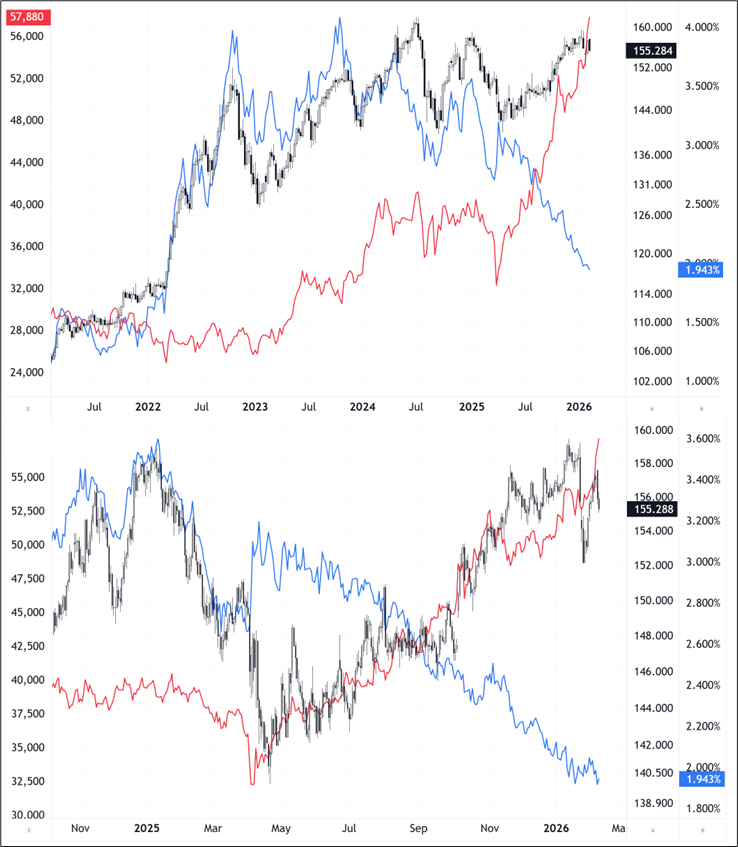

USDJPY is weird. The market is now trying to adopt a new narrative where a stronger Nikkei and stable JGBs are bullish JPY in a sort of BUY JAPAN trade. The JPY correlations have been in erratic flux in recent years as rate differentials lost their power over USDJPY starting around Liberation Day and the big Sell America theme that was supposed to start then was in fact the bottom for USDJPY. The pair bottomed the third week of April at 140 and went up in a straight line even as rate differentials compressed aggressively from 3% in 10s down to the current 1.94%.

Instead of following the collapsing rate differential, the market decided that higher JGB yields were a sign of fiscal concern on run it hot policies in Japan and so the Nikkei and USDJPY took off and said goodbye to the 10-year spread. Here’s the history in overlay format. The first is weekly back to 2021 and the second is daily back to the election of Donald Trump.

USDJPY vs. 10-year US/Japan rate differential and Nikkei

You could model USDJPY in a more sophisticated way than this, but you’re going to get the same answer: USDJPY has been following Nikkei since Liberation Day, not rate differentials. If higher JGB yields are a result of falling certainty in Japan’s ability to manage the bond market confidence game, it makes sense that we would see JGBs down and JPY down and that’s the explanation for why the blue line is going down while the black bars (USDJPY) are going up. Meanwhile, a strong Nikkei means that Japanese savers are confident and willing to send money abroad while foreign investors buying Nikkei hedged keep selling JPY.

So the question now is: Has the LDP landslide somehow restored confidence in the Japanese bond market? If you believe the answer to that question is “yes” then a buy Japan trade does make sense. But I don’t really see what has changed and therefore I don’t trust this move lower in USDJPY. Sure, Takaichi has taken a fairly sane line post-election. That is why JGBs have rallied. But down here in USDJPY, I am not sure there is more juice in owning JPY with Nikkei exploding higher.

In summary: Takaichi has stabilized markets for now and that’s why USDJPY is at 155.00. But it doesn’t mean we need to go much lower. To be long JPY, you need to believe that the correlation to Nikkei will break and it becomes an unhedged BUY JAPAN trade. That’s possible. I just think the jury’s still out.

The big short-term USDJPY support is around 154.50/70. Pressing USDJPY shorts here seems like a really bad idea to me into a flurry of major US data. Risky. We are right at the big level in AUDUSD again, too, and may have already formed a double top. 0.7120/0.7160 is the key band of resistance (2024 highs) and we have now formed a double top at 0.7093/97. I think the market is rather short USD at this point and the U.S. data may not cooperate.

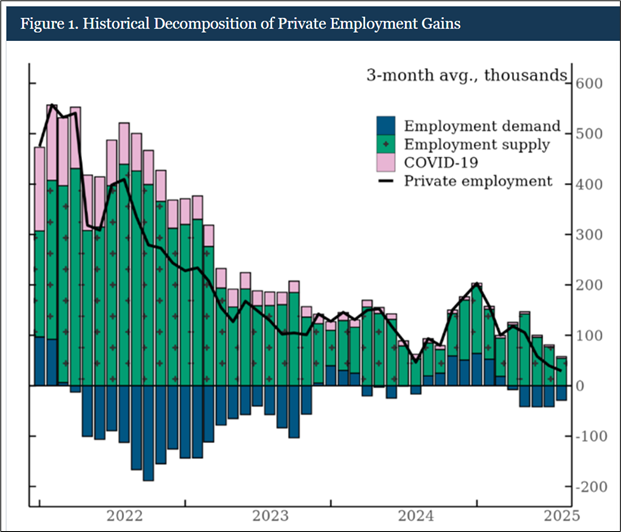

I had mentioned yesterday that I think U.S. jobs could come in weak, but upon further review, I am neutral. I had thought that large Challenger layoffs in health care and the weak December JOLTS pointed to a potential for a weak January NFP reading, but the evidence is mixed.

Payrolls is more about supply of labor than demand these days, so it’s quite confusing. For example, check out this chart, from a January 30 Fed piece on supply and demand for labor.

Putting the pieces together, I didn’t find any edge on the jobs report.

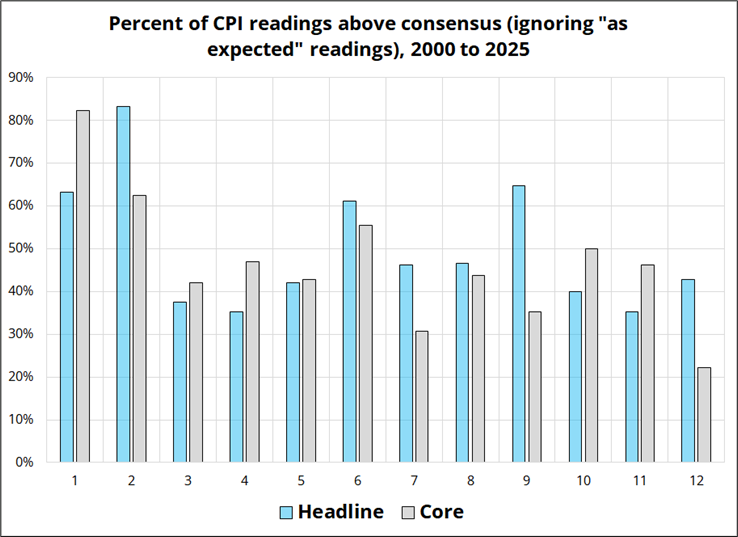

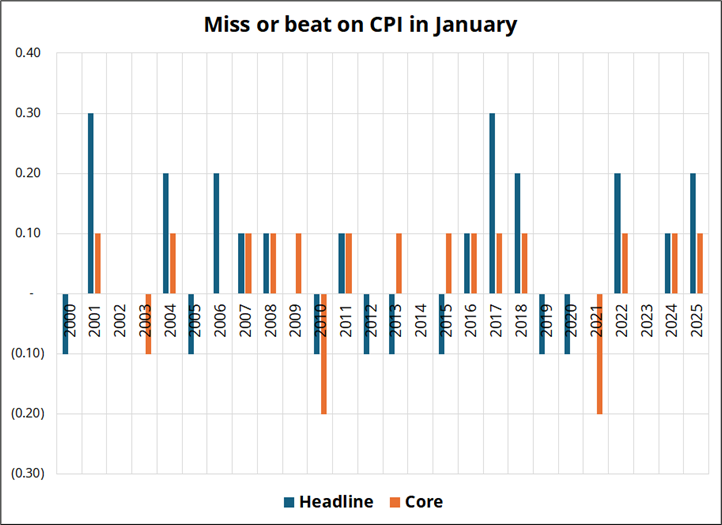

While I don’t have a view on jobs, it’s worth remembering that economists are unreasonably bad at measuring January inflation for some reason. Prices reset for many products on January 1 and therefore in times of abnormally-high inflation, you should expect January to come in stronger than other months. You would think this would easily be captured in economist models, but it’s not. Two charts:

Today’s headline Retail Sales come in weak and the control group is even weaker. Not sure it matters too much given NFP and CPI on deck, but there you go. Definitely small bullish bonds but hard to chase with bigger data points coming.

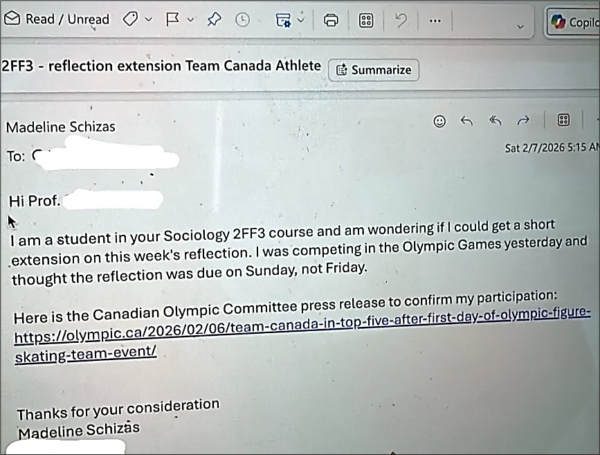

The headline below is from Bloomberg, not the Onion.

It must be difficult for journalists and headline writers at serious news outlets to report on this sort of nonsense with a straight face.

The most Canadian thing ever. :]