The BCOM footprint has been small so far

On this day in 2007

The BCOM footprint has been small so far

On this day in 2007

Flat

Nonfarm payrolls comes in pretty much on the screws, confirming that the worst of the Liberation Day policy shock + DOGE resignations + US Government Shutdown distortions are out and the US economy continues to operate in a soft landing equilibrium. I don’t see any trade to be done on this release.

Perhaps the only interesting takeaway so far, as I type this at 8:33 a.m., is that US yields made a micro probe through 4.20% and rejected that, for now. I am closely watching the 4.20% level because it has been the cap on yields since August 2025. A close above 4.20% is not great news for bond bulls.

Meanwhile, the weakest USD shorts to open the year have been reducing as we remain stuck in a regime with low narrative strength and low volatility. USDJPY is about to enter a miniature weak patch next week as the NISA flows peter out and the 12-15JAN period tends to see a bit of an air pocket as Japanese outflows stop and the JPY outperforms. Shockingly, USDJPY has had zero up days for January 12 since 2010 and just two since the year 2000. Could be fooled by randomness, but more likely it’s just that Japanese savers send a lot of money into foreign investments over the first 10 days of the year, then the price mean reverts a tad.

Speaking of non-price-sensitive flows, silver absorbed Day One of the BCOM selling very well as you can see the flow in the 1-minute chart, but it’s not that spectacular. Silver settlement is a one-minute window from 1:24 p.m. to 1:25 p.m., and here’s the chart of what happened. The exact bottom was the volume spike at that time.

There was a similar, but smaller spike in volume in gold at 1:30 (that’s gold’s settlement time). If you trade anything commodity-related, it’s helpful to understand the dynamics of the Trade at Settlement (TAS) order type because they often create big volumes and big distortions around settlement. You see it mostly in CL as there is often bananas price action between 14:29 and 14:30 in crude oil, even when there is no BCOM rebalance. TAS orders are a bit like a WMR fix in FX… Clients leave the orders and then market makers promise to fill them at the settlement price, plus a small fee. This leads to massive volumes and crazy price movements in that time window as everyone tries to balance their buys and sells and execute balances in the market at the same time.

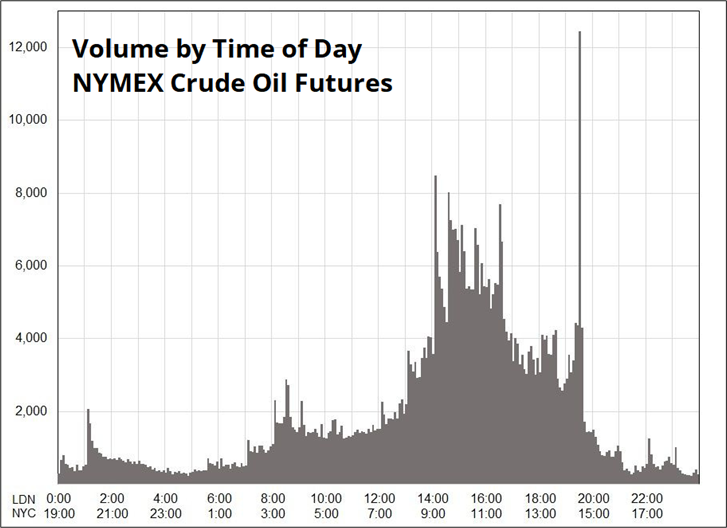

To give you a sense of how insane the CL TAS window can be, here is CL volume by time of day. TAS often accounts for around 10% of daily trading volume in NYMEX crude and we’re talking about a 1-minute settlement window. The jockeying for position begins a bit earlier than 14:29, of course, but it’s a lot of volume jammed into a small period. TAS is not generally as important in metals because there are other fixes used by producers (London fix, etc.), but obviously during BCOM rebalance the silver settlement comes into focus.

Here are all the settlement times for the CME commodities. My takeaway after one day of BCOM rebalancing is that the impact on silver is muted and it’s going to be a non-event. I am moving on from my silver adventure with no real profits or losses to speak of.

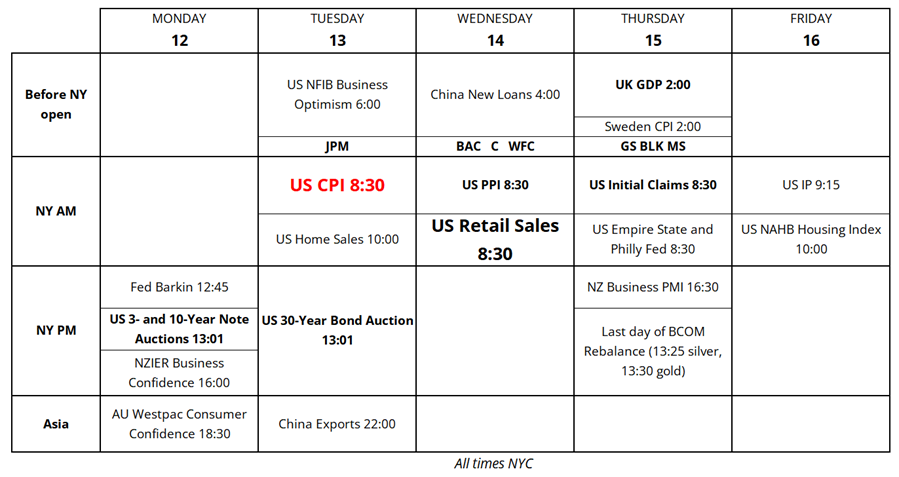

Next week’s calendar features two big reports from the US along with a smattering of other data points. Plus the start of US earnings season.

Have a digitally detoxified day.

On this day in 2007

Happy anniversary to a technology I truly wish was never invented!

:]