Hawkish Fed and American Exceptionalism

Porsche 911 Dakar

I saw one of these in the parking lot outside my office yesterday. Not an everyday sight!

$365,000 car.

Hawkish Fed and American Exceptionalism

Porsche 911 Dakar

I saw one of these in the parking lot outside my office yesterday. Not an everyday sight!

$365,000 car.

Long 1-week 149.50 USDJPY call

Cost ~30bps expires 05AUG

Spot ref. 148.75

50% hedged by EOD 31JUL25

Long 26AUG 1.8050 EURAUD call

Cost ~36bps Spot ref. 1.7790

Long 26AUG 0.8760 EURGBP call

Cost ~33bps Spot ref. 0.8680

It all feels like American Exceptionalism is back. Unreal. Here are my Fed takeaways:

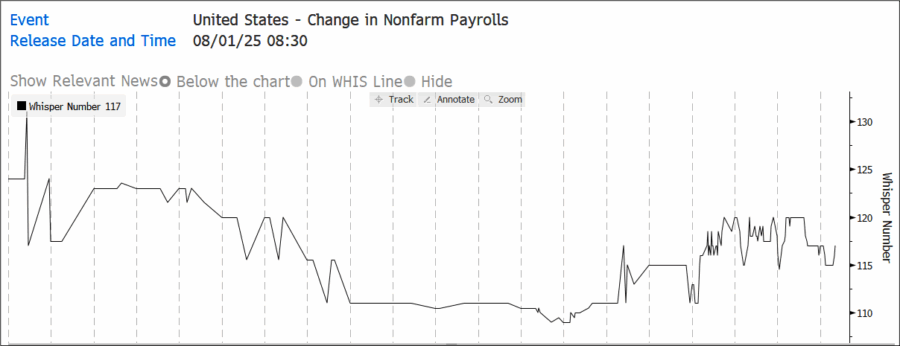

I did my usual slicing and dicing of the jobs data looking for some way to beat the consensus. There is no uncaptured seasonality and the normal lead indicators point in opposite directions. Challenger hiring was low, ISM Services Employment is low, but Initial Claims shows few applicants for UI and it seems like slowing job demand is meeting slowing supply and the labor market remains balanced.

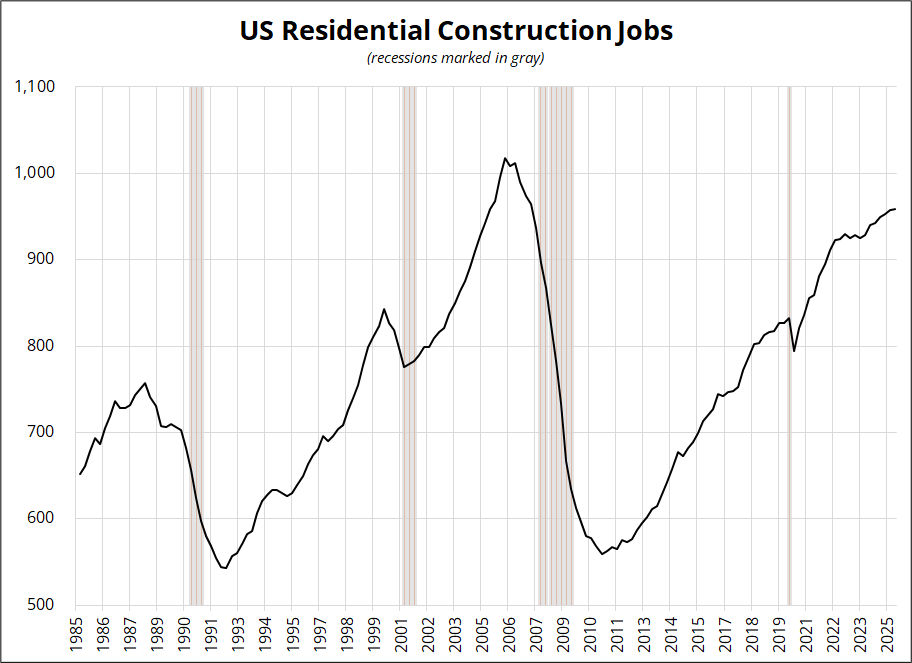

Like I said earlier, I think the market will increasingly trade off the UR, not the headline number. Much as we saw in 2021/2022, it’s not just about labor demand now, it’s about labor supply. I am not completely sure how much immigration crackdowns impact labor supply, but they don’t increase it. The market repeatedly made the mistake of trading the headline number when the UR ended up dominating by the end of the NFP trading day in 2021/2022.

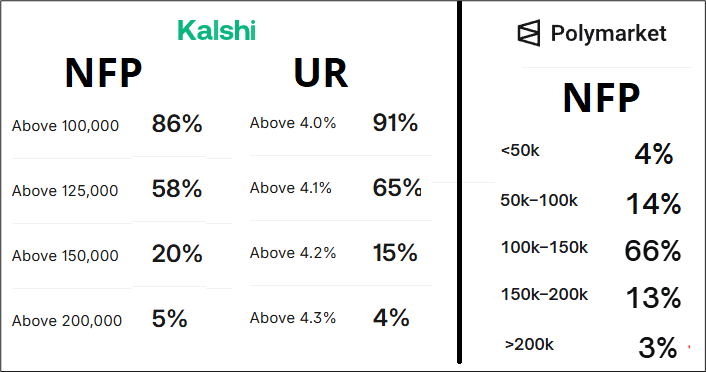

Here are current expectations. Quite tightly wound around 125k or so.

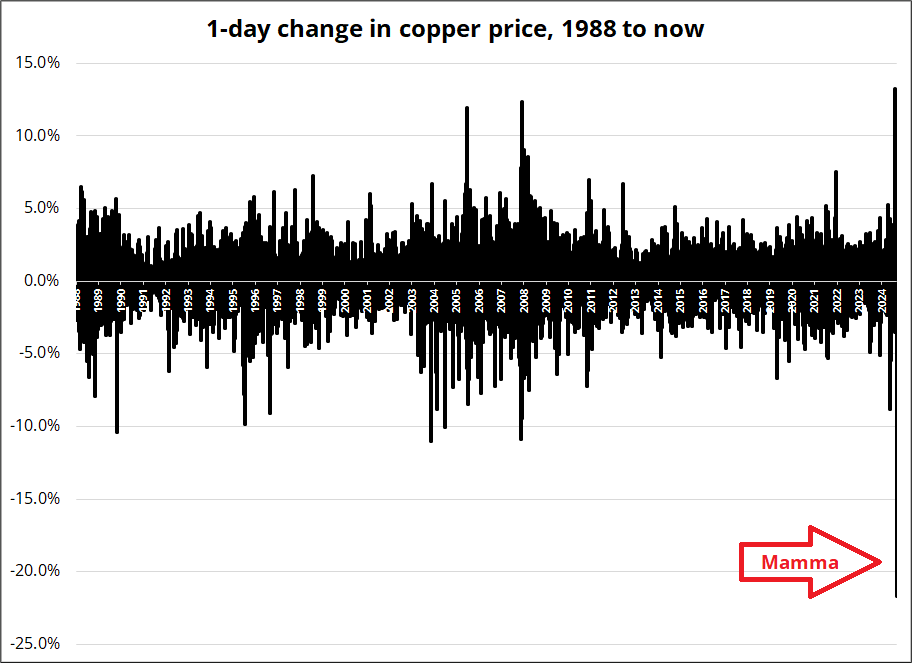

In case you missed it, the copper tariff announcement was a massive surprise as only products, not the metal itself, were tariffed. There has been a massive basis and arbitrage trade raging for months and anyone who didn’t quite get their metal onshore in time is toast. I wouldn’t be surprised if we hear about a failure of some small commodity fund or firm as the move is absolutely Gigantor.

Not normal.

Microsoft fiscal 2025 profit is the same as all the profits of the 50 largest companies in Canada, combined. That includes RBC, TD, BMO, CIBC, CNR, Suncor, Enbridge, Manulife, Imperial Oil, and a ton of other huge behemoths. The MAG7 flywheel is so big it completely dwarfs anything in any real economy, anywhere. Not normal. Until the AI capex peaks, it kind of feels like nothing else matters. The rest of the economy is a rounding error as far as profits are concerned.

The USDJPY option is currently ITM and I plan to hedge into NFP, selling 50% of notional today. Given I don’t have a strong view on the release vs. expectations, I like the gamma. I plan to be completely out of the option if we reach 150.90/151.15 (regardless of jobs) because that is a massive double top and I don’t think we’re ready to rip through that yet.

Here is a short excerpt from an evergreen 2023 Corey Hoffstein piece that I came across yesterday.

A backtest is just a single draw of a stochastic process.

As the saying goes, nobody has ever seen a bad backtest.

And our industry, as a whole, has every right to be skeptical about backtests. Just about every seasoned quant can tell you a story about naively running backtests in their youth, overfitting and overoptimizing in desperate search of the holy grail strategy.

Less sophisticated actors may even take these backtests and launch products based on them, marketing the backtests to prospective investors.

And most investors would be right to ignore them outright. I might even be in favor of regulation that prevents them from being shown in the first place.

But that doesn’t mean backtests are ultimately futile. But we should acknowledge that when we run a single backtest, it’s just a single draw of a larger stochastic process. Historical prices and data are, after all, just a record of what happened, but not a full picture of what could have happened.

Our job, as researchers, is to use backtesting to try to learn about what the underlying stochastic process looks like.

For example, what happens if we change the parameters of our process? What happens if we change our entry or exit timing? Or change our slippage and impact assumptions?

One of my favorite techniques is to change the investable universe, randomly removing chunks of the universe to see how sensitive the process is. Similarly, randomly removing periods of time from the backtest to test regime sensitivities.

Injecting this randomness into the backtest process can tell us how much of an outlier our singular backtest really is.

Another fantastic technique is to purposefully introduce lookahead bias into your process. By explicitly using a crystal ball, we can find the theoretical upper limits of achievable results and develop confidence bands for what our results should look like with more reasonable accuracy assumptions.

Backtesting done poorly is worse than not backtesting. You’d be better off with pen and paper just trying to reason about your process. But backtesting done well, in my opinion, can teach you quite a bit about the nature of your process, which is ultimately what we want to learn about.

Have a three-hundred-and-sixty-five-thousand-dollar day.

I saw one of these in the parking lot outside my office yesterday. Not a common sight!

https://www.topgear.com/car-reviews/911/dakar/first-drive