Oil

We are in an unstable equilibrium where most of the oil experts are cautioning this is the worst oil outage ever while markets remain fixated on how big of a rally we’ll inevitably see in risky assets and risky currencies when the war is over. Low realized vol is disguising convexity in both directions.

Stress over supply shocks in oz

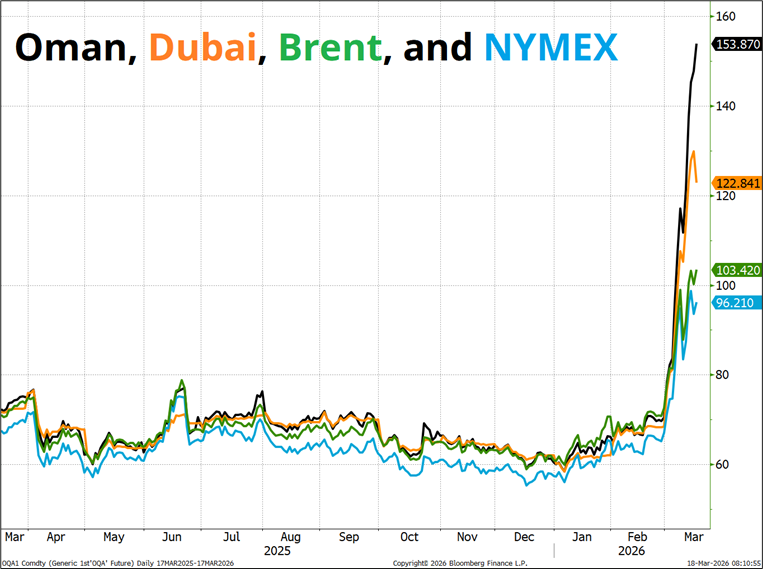

This chart (via Mehul Daya) shows the weirdness in global oil futures. Some of this is probably benchmark distortion, and the rest is due to local shortages.

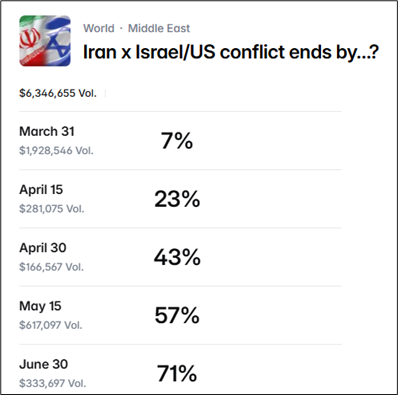

Polymarket odds on when the conflict will end are below. Important methodology note… The rules of this contract say that a 14-day period must pass without military activity by Iran, USA, or Israel and that 14-day period must start before the contract date. So if there was a cessation on March 30 and it lasted 14 days, the March 31 contract would resolve to YES.

It’s interesting to see so much complacency in equities with so little chance of a resolution priced in to Polymarket. Either people are overhedged or they think FOMO risk is greater than any economic or supply chain or stagflation risk. Or both.

I have not been doing much, trading-wise, because I am a bit confused. Here are some of the reasons I am confused:

- Oil remains well bid, odds of a resolution are low, and risky assets trade okay. Markets are often wrong, so maybe this is just a case of “plug your nose and get short stocks.” There is also a significant possibility that gamma and options related flow is keeping stocks stuck around here and after quadruple witching, we release to the downside. I am open to that as I think there is a time factor here. The longer Hormuz passages stay at zero, the greater the pressure on the global economy.

Equity volume (NDX + SPX) yesterday was the fourth lowest of the year. Normally the aphorism is that you don’t want to be short a dull market, but in this case, I don’t think that’s obvious. A convex move is possible in either direction.

- We have an insane number of central bank meetings this week, but it’s not clear what they mean. Sure, we will see each central bank’s posture on whether they believe the war in Iran is more inflation or growth shock. We will get a glimpse as to how they might respond if it continues. But they don’t know any more than we do about how long this oil shock is going to last. So we know (for example) the RBA is willing to hike here and we are going to find out whether the ECB is still using the old headline inflation playbook… Or whether they might look through the oil shock for now. But then oil could go up or down $40 in the weeks to come and everything we learn this week will be mostly irrelevant. In other words, the central banks are beholden to the same unstable equilibrium as we are.

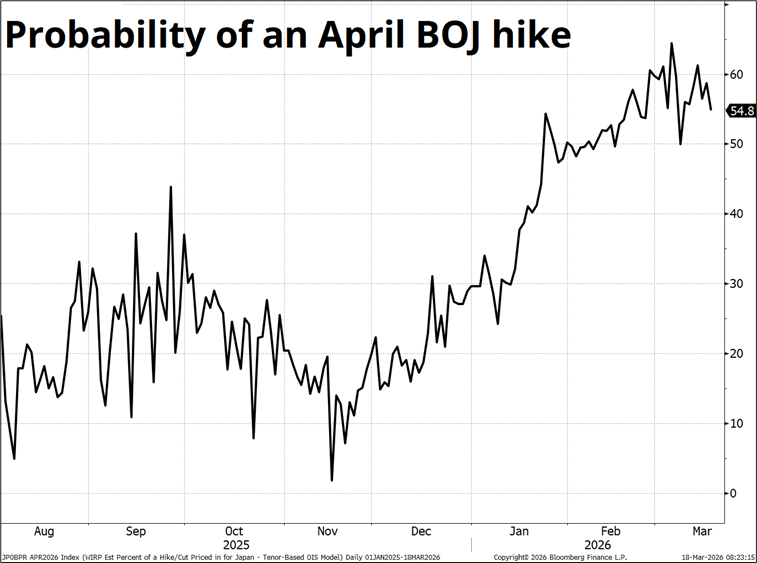

- USDJPY should be a sell here as nothing much is expected from the BOJ, we are at the top of the range for USDJPY, and intervention risk increases above 160.00. Wage growth is strong, the yen is weak, and it’s a perfect scenario for the BOJ to tee up an April hike. They can get this thing to 85% with a few well-placed comments. At the June 2024 meeting, they said that rising import prices and a weak JPY could justify a hike. They could say the exact same thing this time.

The setup in June 2024 was highly similar to today… Weak yen, strong wage negotiations (shunto), market priced 50/50 for the following meeting. That time, they teed up the hike with comms at the June meeting, then hiked in July. Here’s the chart:

So I believe the risk is a higher JPY on a hawkish BOJ tonight.

But on the other hand!

- Takaichi hasn’t been clear about the yen, and she controls the MOF and the BOJ.

- And BOJ meetings are more often dovish than hawkish (USDJPY average performance on BOJ days is +0.7%).

- USDJPY seasonality is max bullish USDJPY from tomorrow to early April due to fiscal year end.

- While Katayama is talking about “bold action,” I wonder if the sense of urgency is diminished as the market and the Japanese economy and the Japanese public are all getting more and more used to seeing USDJPY around 160.00. There isn’t much psychological shock value to this level of USDJPY anymore and the rate of change is chelonian.

Add it all up, and I think there is room for a rally in the JPY for a day or two, but I would not press my luck after that. There is no point buying a USDJPY option for BOJ right now (currently 8:44 a.m. as I type this) because FOMC is today and I do not expect that to be a market mover. I don’t want to pay the FOMC premium. So I will buy Monday (23MAR) 158.30s (25 delta) once the dust settles post-FOMC.

I am buying the extra days because: 1) Incremental days cost much less as you go out, even if you are buying a weekend. You get a bit less leverage and WAY MORE time. 2) There is a path where BOJ is dovish, USDJPY goes to 161, and they intervene and crush it to 156. You don’t get that path if you buy overnights.

- The fourth reason I am confused is the price action. Bitcoin broke out and then failed. AUDUSD looked incredible, then not so much. Gold and silver tried to rally and are now cratering again. In a similar vein, watch SNDK today as it probed well into new all-time high territory in the pre-market (ATH is $725, and it touched $748 a few hours ago). A close below $725 would be a big failure while a clear close up in the $730s/$740s is a breakout.

Final Thought

Many oil experts say this is a much worse situation for oil than the start of the Russia/Ukraine war in 2022. The price of Brent Crude could confirm this by making a new high. In 2022, the final Sunday gap was never broken.