Treasuries might just go down and downer until the government blinks

Sunset last night in Guatapé, Colombia

Treasuries might just go down and downer until the government blinks

Sunset last night in Guatapé, Colombia

Long 11MAY 168/163 put spread in CHFJPY

~31bps off 175.25

Buy EURUSD 1.1257/77

Stop loss 1.1084

CHF weakness lasted about 8 hours this week and then a massive repatriation flow took EURCHF back down to key support into 4 p.m. London yesterday. Now, we’re on a big EURCHF support zone where CHF bears pray for another appearance by the SNB. As capital flees the United States, it hangs US Treasuries and the USD (which are normally great safe havens) out to dry. This has created a shortage of safe havens and triggered feverish demand for CHF and gold.

An alarming aspect of the USDCHF move if you’re short CHF is that the pair followed the NASDAQ closely on the way down but then ignored the 12% one-day rally in the NASDAQ last week. Hmm.

The nice thing about being bullish EURCHF down here is that you know where you’re wrong: ~0.9184. A break of the multi-year lows means that the SNB isn’t down here, or isn’t serious, or is being overwhelmed by repatriation flows.

This isn’t the SNB’s first rodeo, but they have a severe credibility problem because they started intervening in EURCHF at 1.5000 in 2009 and… Well, you know the story. This is quite the triangular compression happening on the weekly chart. Has the look of something crazy about to happen.

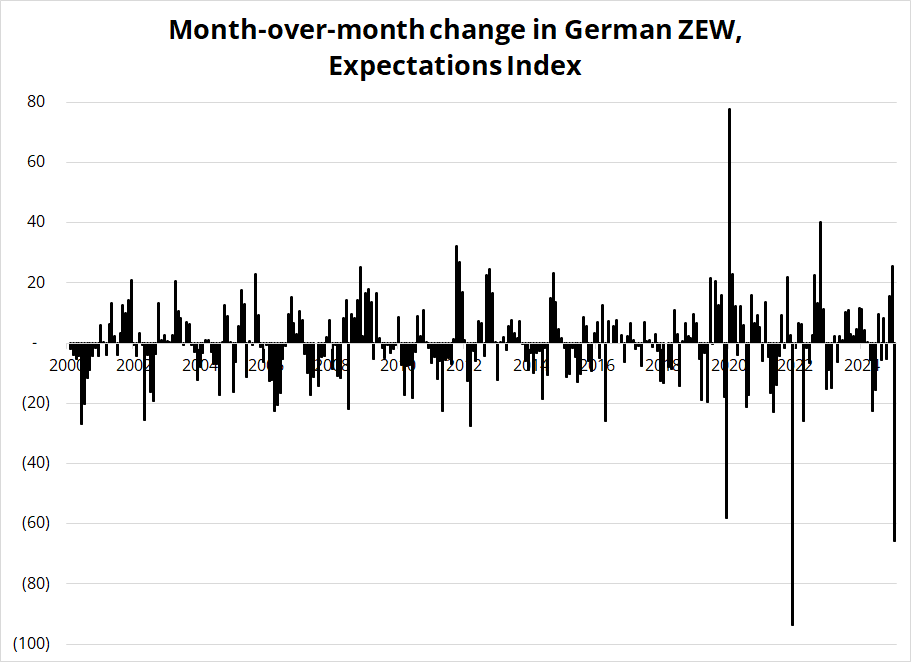

Weak German data overnight didn’t help. We are laser focused on the US story, but I suppose if Germany, China, and other big economies are crushed by Trade War angst too, then the micro around non-US economic data gets a little trickier. We went from bubbling green shoot optimism on fiscal boosts and strong equity markets to complete malaise. I would take this chart with a grain of salt as survey data has been getting noisier and there is some base effect here as we go from super happy to max sad in a single month.

Also note the survey has been getting noisier as economic volatility increases and survey reliability and sample sizes fall globally. Still, it’s not exactly bullish EUR! The three spikes lower are COVID, Russian invasion of Ukraine, and now.

“The erratic changes in the US trade policy are weighing heavily on expectations in Germany, which have sharply declined. It is not only the consequences the announced reciprocal tariffs may have on global trade, but also the dynamics of their changes, that have massively increased global uncertainty. The economic expectations for Germany and the Eurozone reflect this development,” comments ZEW President Achim Wambach

Meanwhile, the media reported Waller’s speech as dovish yesterday, but I read it more as wait-and-see. Coming from one of the most dovish voters, it felt… Not that dovish? There was no sense of urgency, just a scenario analysis. I used Claude to create a graphic summary.

If you are curious about how this was made… Prompt: Create a simple diagram in that explains the two outlooks and interest rate reaction functions in this speech (then I pasted the entire speech). It took four iterations to get something useable (I had to keep changing and coaxing out the fonts, structure, etc. with further prompts).

I hadn’t checked WIRP in a while and was a bit surprised to see that the May FOMC (in 22 days) shows a 20% chance of a cut. I get there’s an embedded S&P put in all these contracts, but 20% still seems incredibly high for a central bank that is clearly in wait-and-see mode.

Here’s are the key Fed comments post Liquidation Liberation Day:

14APR *BOSTIC: MOVING TOO BOLDLY WITH POLICY WOULDN’T BE PRUDENT NOW

14APR *WALLER LAYS OUT TWO SCENARIOS BASED ON DIFFERENT TARIFF POLICY

11APR *Collins: Appropriate for Fed to Have ‘High Bar’ for Preempting Weakness

11APR *FED’S WILLIAMS SAYS CURRENT RATE STANCE REMAINS APPROPRIATE

11APR *FED’S MUSALEM SAYS MONETARY POLICY IS WELL POSITIONED

04APR *POWELL: NOT CLEAR AT THIS TIME WHAT APPROPRIATE POLICY WILL BE

04APR *POWELL: IT FEELS LIKE WE DON’T NEED TO BE IN A HURRY, HAVE TIME

None of this smells anything like urgency. Even as a person who is bearish stocks, I think paying 20 to make 80 for a rate cut in 22 days is mega negative EV. Obviously, it’s a trade with poor leverage, but I would rather pay the May FOMC.

It almost feels obvious what’s going to happen here. Yields will keep rising as term premium and capital flight continue. The government will pop up to push back. Yields will fall a bit. Then yields will keep rising again. Until finally the big guns come out:

Bessent made it clear yesterday that we are not at intervention levels yet, and the Fed is slow-playing it too (see here). Treasuries will be a difficult long until the day the government blinks, and then they will be the trade of the year.

There is considerable headline risk for the JPY over the next few days as the market is dreaming of some kind of JPY appreciation comment. The risk is that Ryosei Akazawa is not authorized to talk JPY because he’s not the finance minister, and we just get a bunch of non-committal stuff like “Japan / US agree to work towards deal on accelerated 3-month timeline”. With positioning heavy long JPY (see report below), that could lead to a zippy unwind trade. On the other hand, the dream scenario for JPY bulls would be something like: “Bessent, Akazawa agree that JPY is fundamentally undervalued”. We don’t have a firm time or date for any presser, Akazawa lands in DC tomorrow and leaves Friday.

I need a quick favor, please. I am writing a new trading book, and for one section, I need to some aggregate data on trader behavior. If you are a trader / risk taker and if you have about 90 seconds to complete a very short survey, please click here. The survey is anonymous.

And… Here’s a good study. This website is credible, in my opinion, but I did not cross-check their results.

https://quantifiableedges.com/97-years-of-death-crosses/

Have a gloriously sunny day.

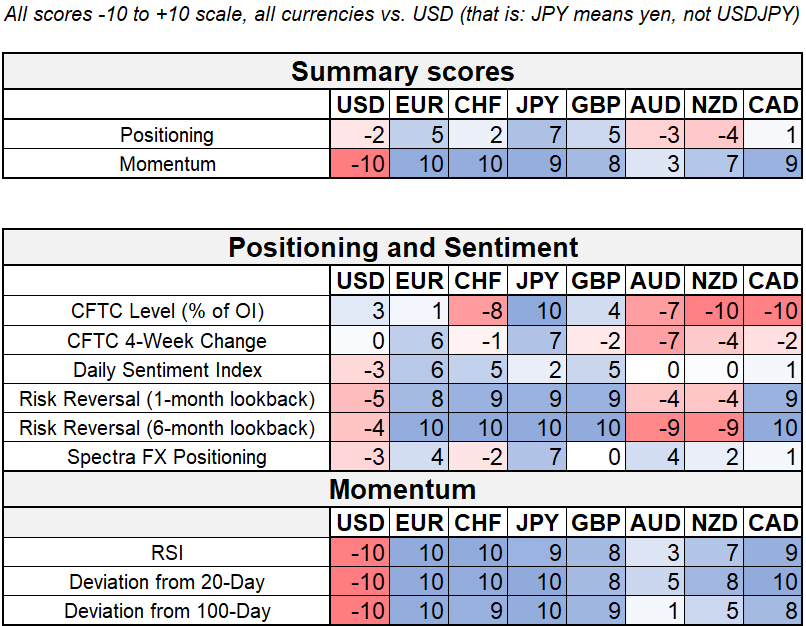

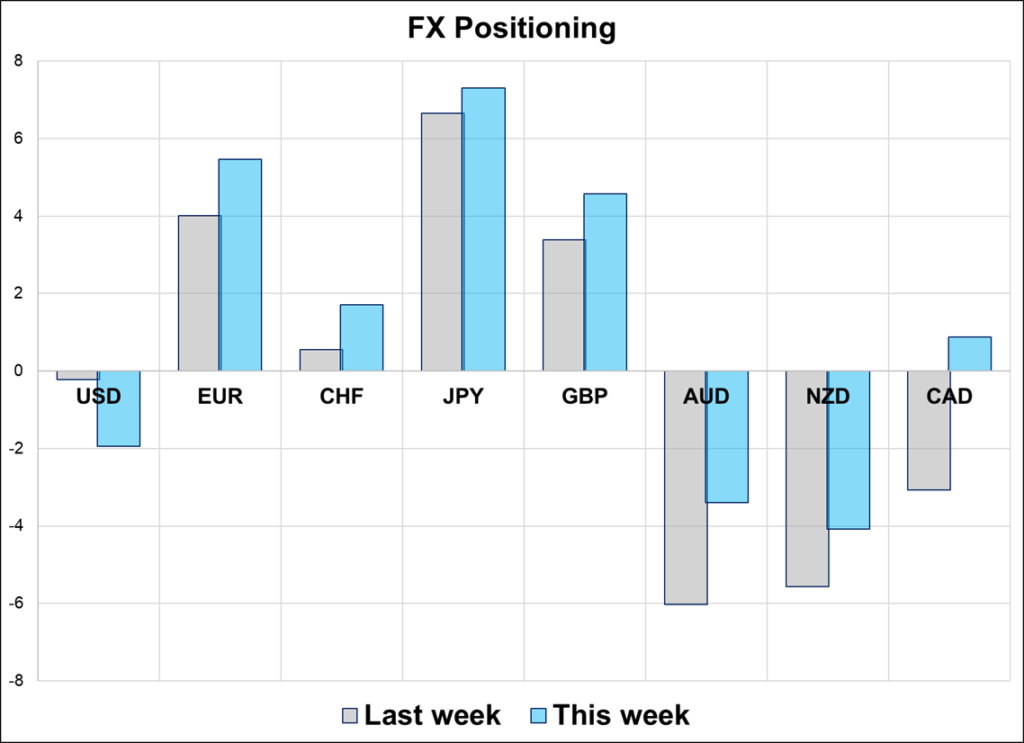

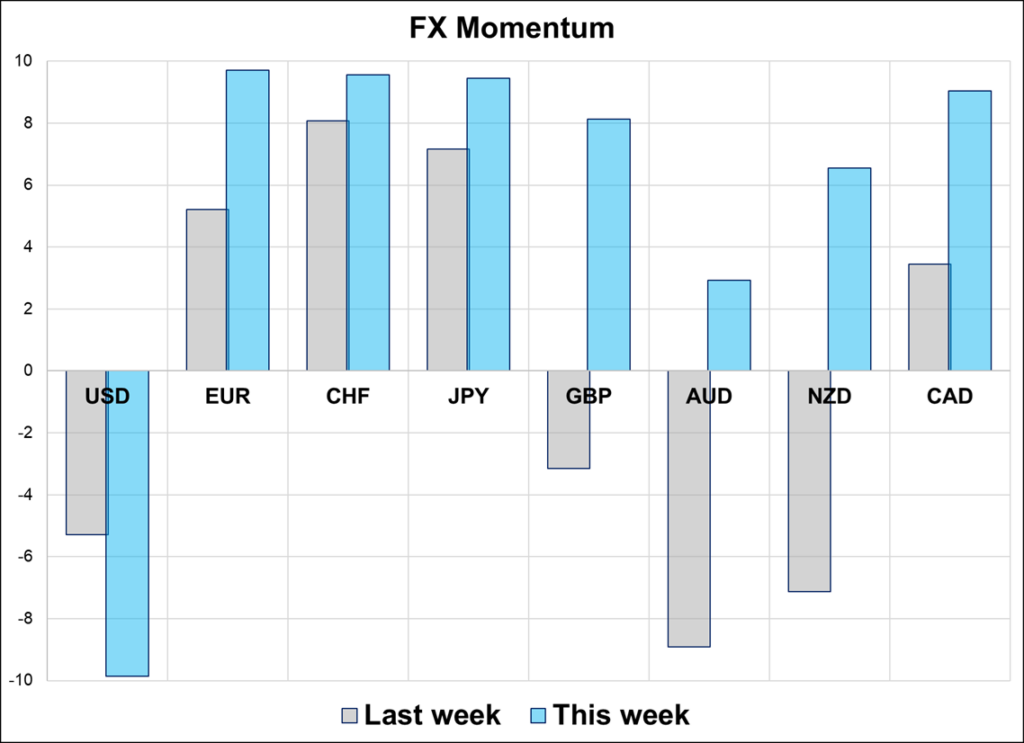

Somewhat extreme EUR and JPY but that’s probably OK

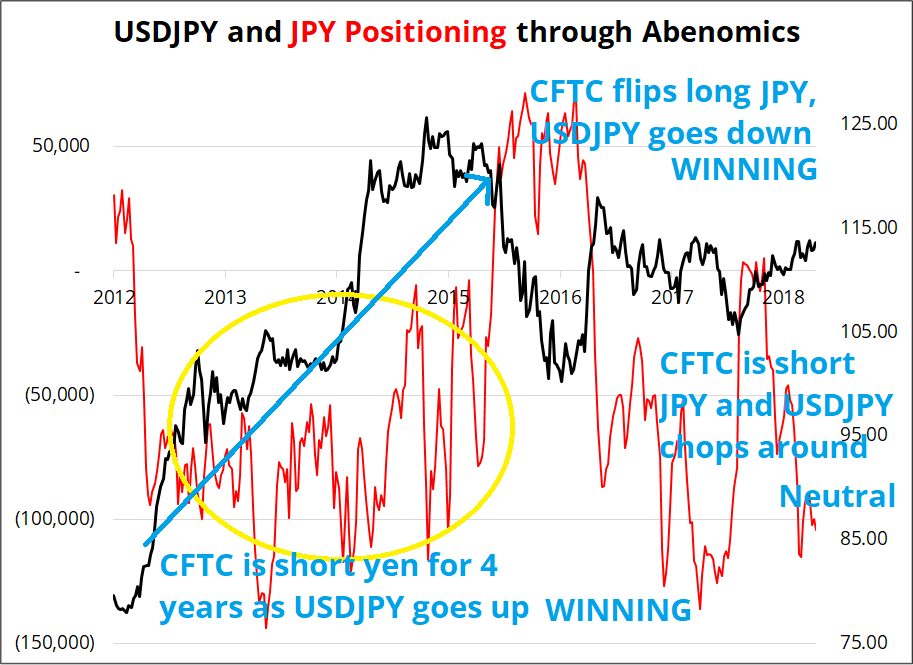

Hi. Welcome to this week’s report. The long EUR and long JPY positions are getting towards an extreme, but I feel that when there is a major macro regime shift, people tend to overweight positioning. I am sensitive to this error because I made it all the way up in USDJPY during Abenomics. There was a point where 44 out of 44 traders in FX at the bank where I worked were short JPY… And yet the JPY kept weakening for ages because the policy shift (Abenomics) was much more important than any positioning, no matter the size. You can’t ignore positioning, but it’s important to differentiate between positioning in mean reverting markets and positioning after a regime shift. Also, the JPY positions on the CFTC tend to make money because they catch all the major trends. If you fade CFTC JPY positions systematically, you will systematically lose money.

JPY is displaying strong upward momentum and significant long positioning. This puts the onus on the fundamentals to play ball. Despite my desire to avoid overweighting positioning, I’m also on high alert for adverse JPY-negative newsflow because that could have a convex impact on the yen. If Bessent signals things are not going well with Japan, or they strike a deal that doesn’t mention the JPY… Expect a massive and impulsive JPY selloff. But if the news cooperates, positioning should not be an impediment to further JPY gains.

Is the current regime shift from TINA to “sell America” as significant as Abenomics? Your call! Thanks for reading. Positioning and momentum data on the next page.

Source: Matt Gittins’ Phone

The Sunset last night in Guatapé, Colombia