I would guess the runup into NFP (and NFP itself) is USD bullish

I would guess the runup into NFP (and NFP itself) is USD bullish

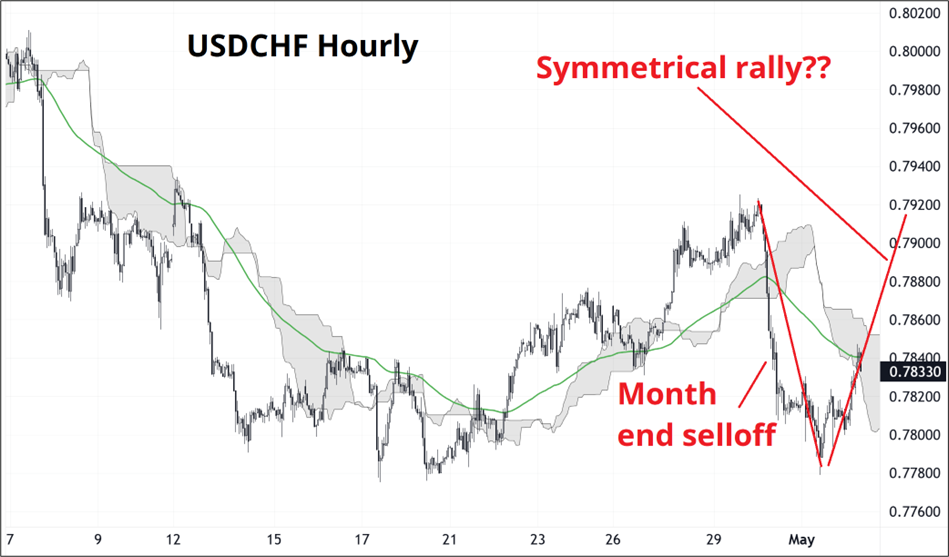

Long 1-week (11MAY) 0.7870 USDCHF call

cost ~22bps off 35 spot

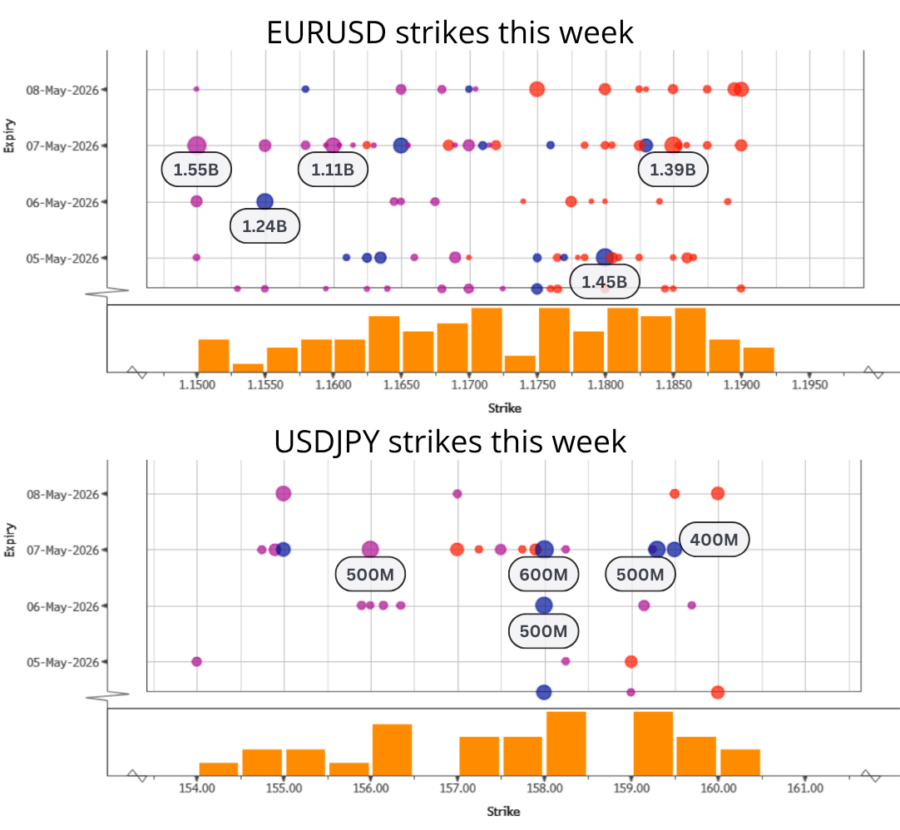

First up: While I might regret this if the MOF returns, I have changed my mind on USDJPY for now as I’m less excited about oil’s reversal lower and I am worried about strength in nonfarm payrolls on Friday. Furthermore (and maybe more importantly), I think the run-up trade into NFP will be for the market to buy dollars in anticipation of a strong release.

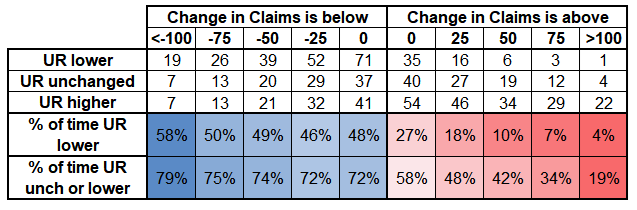

Initial Claims and Continuing Claims are falling right now. If you look at the change in those weekly series and compare the change in the monthly Unemployment Rate (UR), there is a strong and linear relationship. This table looks at all data back to 2000, excluding the COVID period 2020-2022. I simply look at the sum of the changes in Initial and Continuing Claims and then see what the Unemployment Rate did that month. Here’s the table. The more claims fall, the more likely the UR falls.

The number this month is -87 as Initial Claims ended February at 214 and are now 189 while Continuing Claims ended February at 1847 and are now 1785.

You can see that in the -75/-100 zone, you have about a 75%-80% probability of the Unemployment landing unchanged or lower.

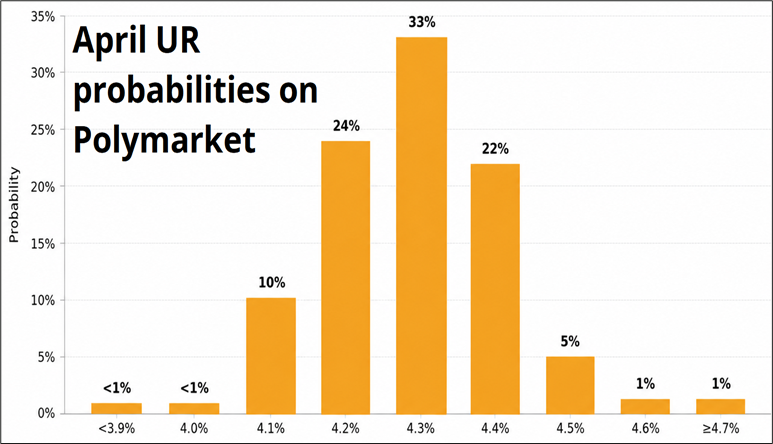

But the Bloomberg survey shows most economists at 4.3% and slightly more at 4.4% than 4.2%. In other words, the skew of the forecasts is the wrong way (if you believe my table). Polymarket skews the other way, slightly, as you can see in this graphic.

A booming NFP puts the MOF in a tricky spot as the “FX should reflect fundamentals” mantra makes it hard to intervene on the Friday of a strong U.S. jobs report.

It’s nice to care about economic data again—as we enter week ten of the war, we cannot stay on high alert for Axios headlines forever.

To play my higher USD view over the next week (into and through NFP), I like buying 1-week 0.7870 USDCHF calls for ~22bps off 35 spot. The play is for a symmetrical unwind of month-end USD selling.

I suppose with U.S. bond yields and mortgage rates substantially higher due to the war, there is an outside shot of something unexpected from the Treasury Financing and/or Refunding announcements this week. While I have no idea what that might look like, the US 10-Year yield at 4.41% is directly in defiance of the U.S. Treasury’s stated goals. Then again, 10-year yields have not really moved since mid-2023, so maybe they don’t care.

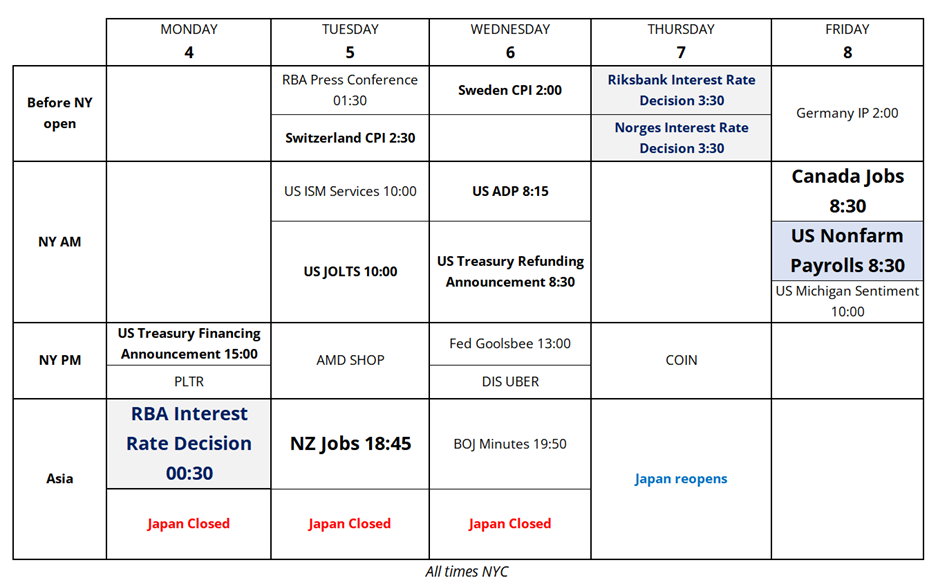

There are three central bank meetings on my calendar. The RBA and Norges are expected to hike, and the market will be watching for forward guidance there while the Riksbank is on hold with less than a full hike priced this year.

Happy birthday to my beloved wife. Here’s to 46 more.

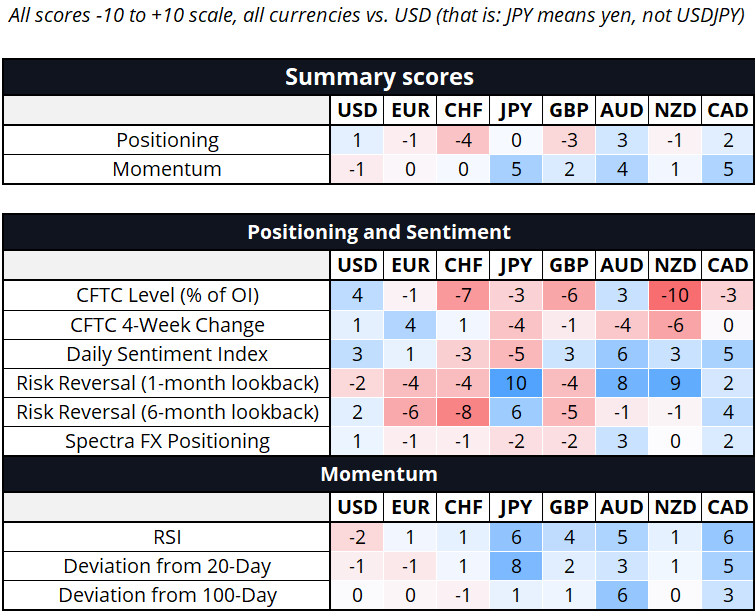

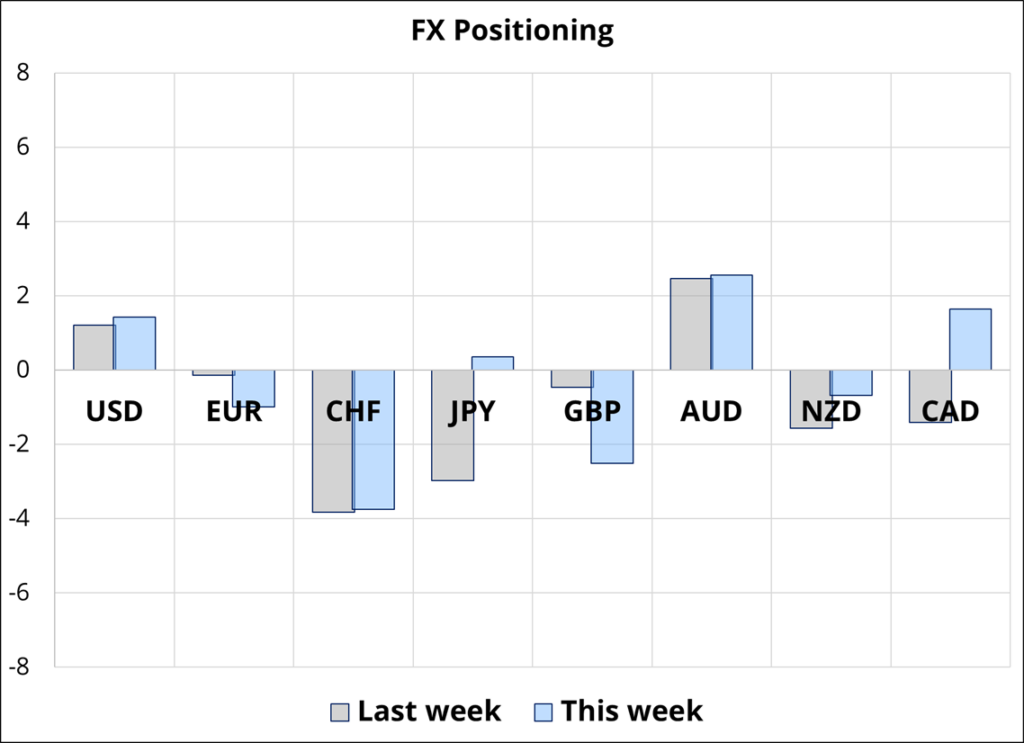

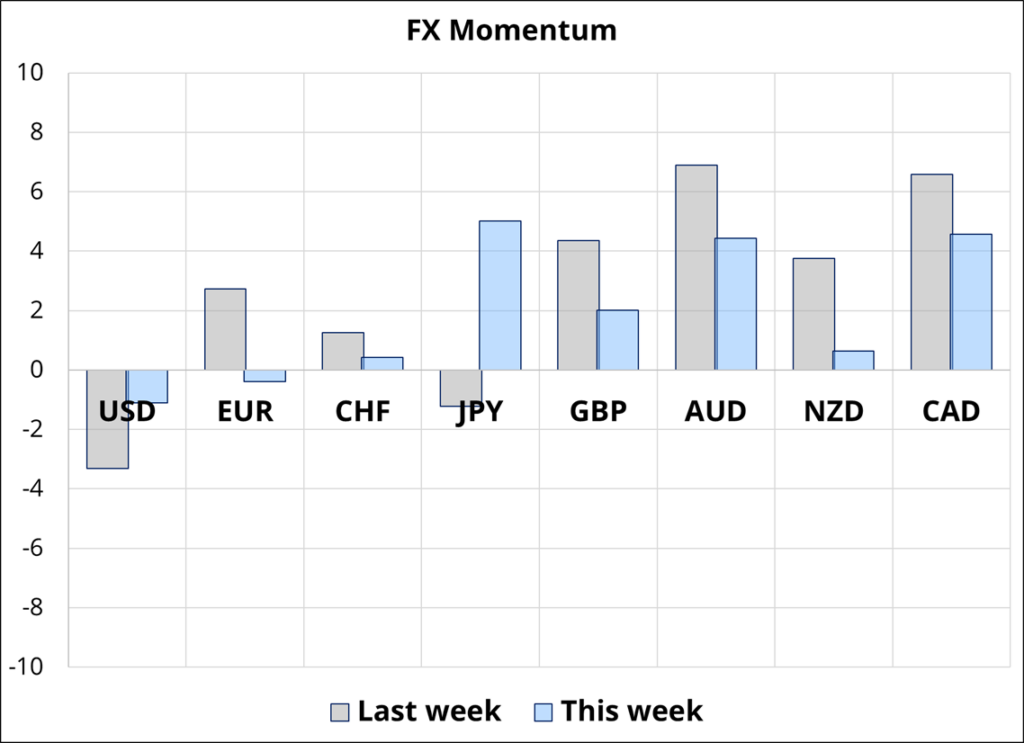

Hi. Welcome to this week’s report. (To read about how I use and trade this report, see here.) Positioning has settled into a boring zone of non-committal. The market is dabbling in short GBP and short CHF, with low conviction overall. The USD crosswinds I have been describing in the past week or two are creating low-conviction conditions for G10 FX.

HT Dave Nadig

If you are at all interested in how time flows through comics, check out the book “Understanding Comics” by Scott McLoud—it’s one of my favorite books of all time.