The market is slowly grokking that the TACO stand is closed

The market is slowly grokking that the TACO stand is closed

2APR .69/.68 AUD put spread

21.7bps off 0.7025 spot

Short EURUSD 1.1527

Stop 1.1677 Take profit 1.1367

Short 07APR EURCHF 0.9010/0.8960 put spread +

long 07MAY 0.9110/0.9160 call spread for 2bps (TP TODAY)

The market is finally coming to terms with the fact that statements from bad-faith negotiators engaged in a war are not representative of the truth. Also, the TACO concept does not apply in this scenario as you need a reopening of the Strait of Hormuz to relieve pressure on energy markets and that decision is in Iran’s hands now, not the hands of the U.S.

The market has PTSD from one year ago, particularly from the day when stocks rallied 10% on the Trump tariff delay, but the delay of the bombing of Iranian energy assets is not a similar story. Hence the diminishing returns from these headlines…

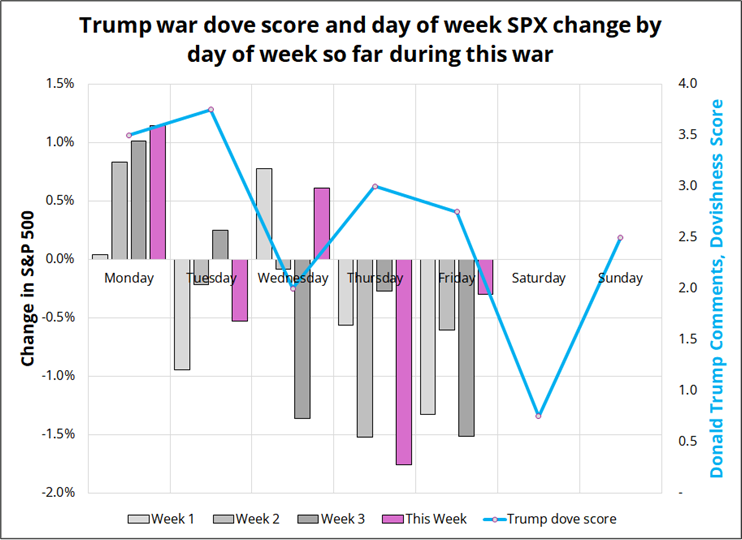

Stocks are following the same pattern this week as they have been following throughout the war as Monday hope turns to late-week despair.

One can sensibly wonder what Trump could possibly say that would be bullish at this point. There is no offramp where he can simply say: “We won!” anymore given the situation in the Strait.

And you can add “the cure for high memory prices is high memory prices” to the list of bearish stock market factors now[1] as SNDK and MU have cratered on the Google news. Memory prices are always cyclical, and we may have just hit the top of the cycle. High prices encourage innovation towards greater efficiency.

I like to keep things short on Friday, so let me transition to some quick hitters.

Still bearish stocks (but). Zero sign of capitulation or panic yet. I start to get antsy when I am short stocks for this long because history shows that shorts often meet sadness at some point. But I am hoping to buy into an aggressive capitulation move. Maybe that will happen between now and Monday. Looking at QQQ as a barometer, max oversold tends to be around 3% below the 100-hour MA (see chart). That is 23444, which is not THAT far away. If we get to 23500 in NQ between now and Monday, I am going to square up all equity shorts and just re-evaluate from a place of objectivity.

No position in NOK. I whiffed on the Norway trade, even though it was a good idea. NOKSEK rallied so much in the time it took me to type and send out am/FX that I never got the trade on. Unfortunate because it rallied 200 points in a straight line.

Sticking with short AUDUSD (put spread). The break of 0.6900 has been a tad disappointing but now we get corporate month end (today) and Real Money month end (Tuesday). Both should be AUDUSD selling.

Tiring EURUSD short is tiny ITM! The market has been ripping EURUSD on every Trump headline but diminishing returns apply there too. Maybe it’s finally ready to crumple.

Taking profit on bullish EURCHF trade. I am not going to bother taking off the put spread that I am short because it’s so far away. I will sell the call spread to take profit. The idea was to get long ahead of round number bias for SNB intervention at 0.9000. Strong winner considering a war in Iran happened and EURCHF went up, not down. Gold, CHF, JPY, and bitcoin are all terrible safe havens when bonds are selling off. This is an unfortunate characteristic because the time you most need an alternative safe haven is… When bonds are selling off. Now gold is stabilizing and while the move here makes sense to me, further upside in EURCHF does not.

Mentally preparing for USDJPY to go crazy. Policymakers are busy wargaming and are less likely to be concerned about G10 FX rates at the moment. Still, the JPY TWI is plumbing new all-time lows and USDJPY is back to the zone where intervention has taken place a few times. The rate of change of USDJPY is near zero, and given the macro backdrop I don’t think Japan is keen to intervene because if oil goes to $170, they are going to be wishing they hadn’t. That said, a zippy move through 162 will probably force their hand. 1-week USDJPY is bid for calls (!)

We are in the juicy seasonal period where USDJPY tends to rally (25MAR to 06APR). If those flows trigger a reverse waterfall upcrash through 162.00 and into new all-time high territory, I expect the MOF will intervene. A path that looks something like 163.10 paid, intervention, 157.10 given… Is looking more and more like a reasonable base case. Importers need to buy USDJPY, seasonal outflows have begun, and fireworks are possible.

Yesterday, I attended Exante’s / Vanda’s 10th anniversary conference featuring Scott Bessent, Alan Taylor (BoE), Anna Wong, and other bigshot celebs. Thanks Jens! Great conference. Here is the full agenda. Here are some quick bullets.

Have a sunny weekend.

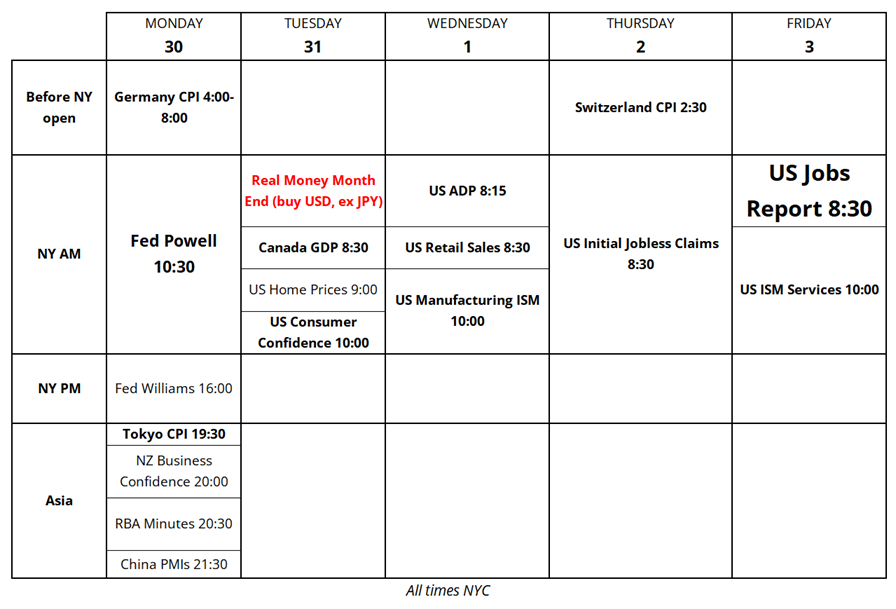

Next week’s calendar!

—

[1] Private credit blowups, tight financial conditions (rate cuts turned to rate hikes), MAG7 move from capex lite to capex heavy, huge corporate debt issuance on top of weaker credit fundamentals, zero jobs created in the U.S. since Liberation Day, tax refund money peaked, etc. etc.