Hawkish Norges, equity neutral

Hawkish Norges, equity neutral

Long NOKSEK @ 0.9546

Stop loss 0.9324

Buy GCM6 @ 4033 limit

Stop loss 3544

2APR .69/.68 AUD put spread

21.7bps off 0.7025 spot

Short EURUSD 1.1527

Stop 1.1677 Take profit 1.1367

Short 07APR EURCHF 0.9010/0.8960 put spread +

long 07MAY 0.9110/0.9160 call spread for 2bps

The Norges Bank meets tonight, and their policy settings are way stale as inflation is sticky in Norway, unemployment is super low, and a huge new inflation shock wave is 25 yards offshore. First, let’s look at initial conditions in Norway.

Interest rates are 4%, which is mildly restrictive.

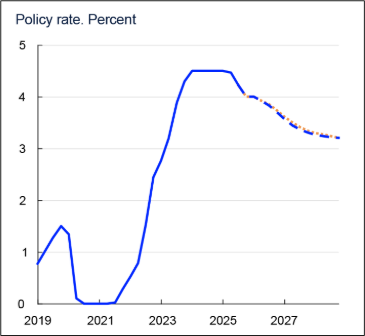

The policy path forecast is stale. It shows cuts. See first chart.

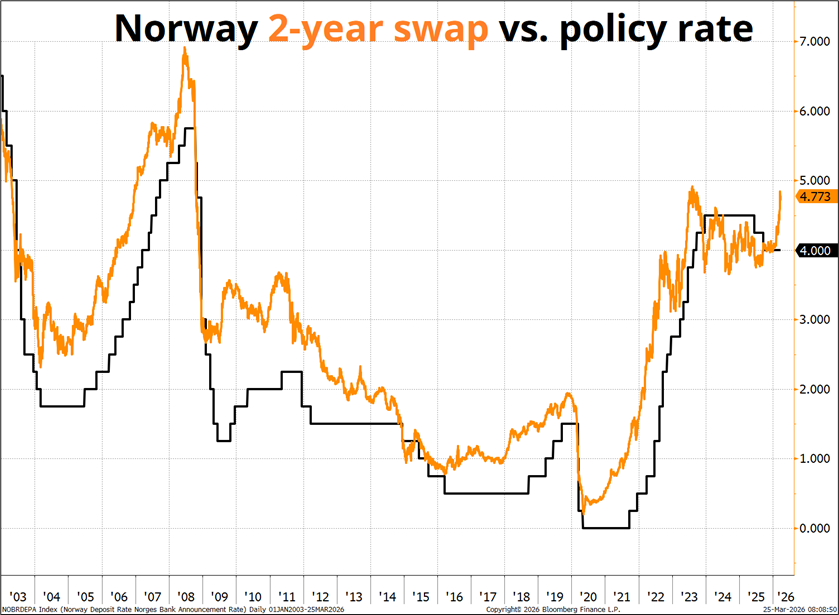

The market 2-year yield is moving higher along with global rates. The next chart below shows Norway 2-year swap yield and the Norges policy rate. The market leads the policy rate in most instances, similar to the U.S. and other countries.

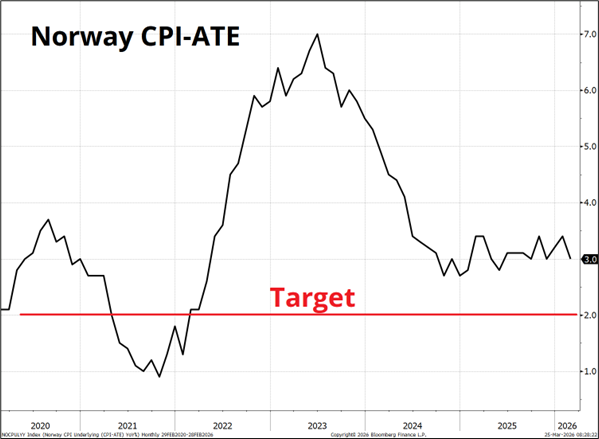

Inflation is 3% and has been above target for a long time. In her annual speech in February, the head of the Norges Bank (Ida Wolden Bache) said:

“Excluding energy prices, inflation has been close to 3 percent since autumn 2024. According to figures published this week, inflation increased in January and was higher than we had expected. We will ensure that inflation is brought back to 2 percent.”

And she concluded with:

“The past years have reminded us that the outlook can change abruptly. That is why we do not make any promises about the policy rate.”

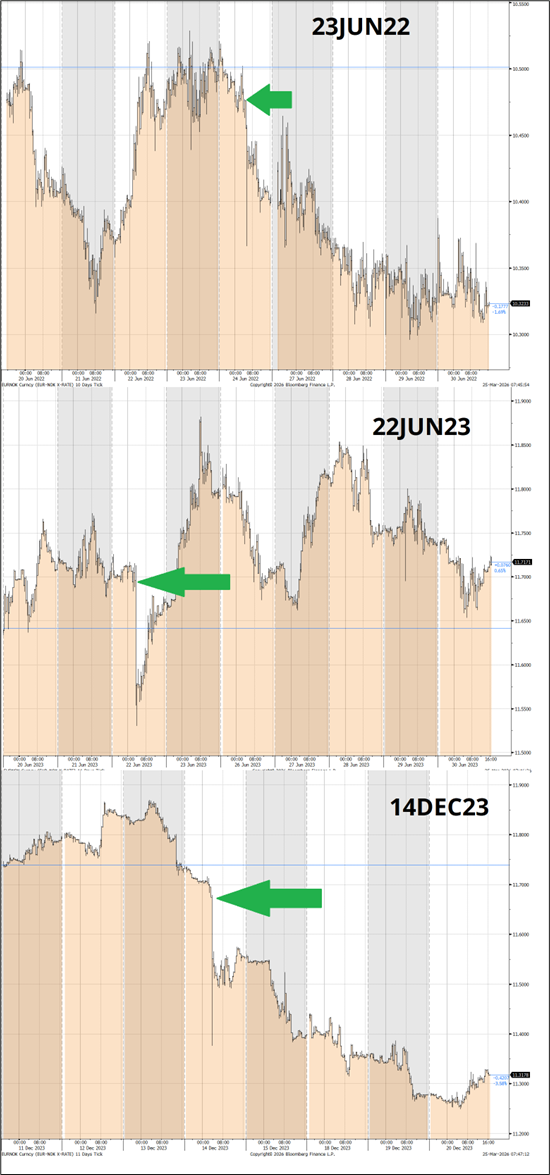

This last statement from Bache is relevant and true. The Norges hiked unexpectedly three times in recent years: June 2022, June 2023, and December 2023. They are willing to make moves that are not priced in. Meanwhile, the chart of unemployment in Norway is pretty much not a real chart.

What we see today with the war in Iran is the kind of stagflationary shock that normally puts central bank growth and inflation objectives in tension, at least in the near term. If you follow the Norges Bank’s own playbook, the implication is modestly higher rates, because supply-driven inflation pressure generally needs to be leaned against if the bank wants inflation back to target on a reasonable timeline.

Norway is not Europe here. Households are cushioned from the electricity shock by subsidies, so the squeeze on purchasing power is much smaller than elsewhere. And with oil and gas prices higher, petroleum investment is likely to rise too. Net-net, there is no stagflationary domestic macro hit for Norway. The main downside comes indirectly, through slower growth abroad.

So while the odds of a rate hike tonight are fairly low, I think they are way higher than people think. And June should be a sure thing. The Norges will need to do a quick pivot here to acknowledge that they have been wrong on inflation (it is not returning to target—they forecast 2.6% and we are seeing 3.0%) and there’s significant new information, the Iran War. The market is showing the way for the Norges. I.e., Higher rates.

The two biggest caveats here are 1) rates are already mildly restrictive with the neutral rate probably somewhere around 3.4% and 2) it’s hard for a central bank to move so quickly from a path of lower rates to one of higher rates. If it wasn’t for inertia, they would be hiking for sure.

The big charts below show what EURNOK did on the last three surprise hikes. 10-15 big figures lower right away and then two of three times it trended lower and in June 2023, it ripped back.

Things are complicated a bit here by the equity beta of EURNOK, as discussed last week. If stocks crater (and they might!) … You are not going to be happy short EURNOK, even if the Norges is super hawkish. Therefore, I prefer NOKSEK as the way to play this thing. You strip out the equity beta somewhat and have a cleaner play on straight NOK. Lucky for me, NOK has been browbeaten over the last week, for no real reason, and so the entry point on NOKSEK is super attractive.

I think the EV of a spot trade is way higher than options because there are many boring outcomes where Norges threads the needle and NOK is unchanged. You obviously get way more leverage in short-dated options, but I think you get lower EV.

So… New trade idea. Long NOKSEK here (0.9546) with a stop loss at 0.9324. Below I show a chart where you can see that 0.9400 is nearby support. Given the event is tonight, I want a wide enough stop to survive a mad jiggle.

Some bad prints / bad data on here, that’s why you see all those weird wicks

Have a gloriously synonymous day.

Top 5 banks in the United States (by assets)

PS: Quite a lot of you asked why I did not include the CHF 1000 bill in yesterday’s fact of the day.

Switzerland is not part of the G20. That’s why!