2025 calling

We are back to April 2025 style markets as the bond vigilantes eviscerate the Japanese long end, Trump is fully unhinged (sending out private text messages from world leaders, posting maps showing Canada as part of the United States, etc.) and Davos Man is on edge. We got to the point where it looked like we were in some sort of equilibrium as the UK and others had properly appeased by paying tribute to the U.S. but now the EU and others may conclude that negotiating with an unreliable counterparty is pointless. Still, there is no coherent response as some are pushing for strong retaliation while others in the EU (Merz) still see the world not as it is, but as they wish it would be.

The market has reopened the April 2025 playbook and is again worried about wholesale exit from U.S. assets. It’s tempting to think that we have already seen that movie and we know how it ends. Trump backs off and everything mean reverts. But the reaction function from former U.S. allies is hard to handicap and the chaos factor could be higher here as markets first underreact and then maybe the EU decides that appeasement hasn’t worked so let’s fight back. With so many differing opinions in Europe, it’s not easy to bet on a strong, coordinated response, but why would the EU bother negotiating at this point? They might feel it’s pointless at this juncture… Like negotiating with Putin.

These are pretty mind-blowing headlines:

*DANISH PENSION FUND AKADEMIKERPENSION TO EXIT US TREASURIES

*AKADEMIKERPENSION CIO SAYS US `IS BASICALLY NOT A GOOD CREDIT’

This fund is only 25B AUM and owns just $100 million of UST. Still, the signal is potentially disastrous for US assets if large Swedish and Dutch pension funds agree.

For now, February 1 is the date to watch as there is absolutely no point in any EU response to random threats with the Supreme Court ruling still to come and the high odds of a backtrack before the tariffs are set to go into force at the start of February.

The story in Japan is getting more and more interesting as the yen has bounced a bit despite a complete meltdown in the back end of the bond market as risk of repatriation rises and the Nikkei falls. Interest rate differentials gave way to Nikkei direction as the primary correlation with USDJPY quite some time ago, and there could be a point soon where Japanese investors worry about domestic and global instability and decide to rotate money back home.

On the other side of the ledger, the trilemma remains undefeated. If this all leads to a situation where the BOJ has to intervene in the JGB market (buying bonds) then it will look like a full-on sell JPY debt crisis. So, we now have crosswinds: Weak Nikkei and repatriation risk vs. BOJ intervention risk in the long end which leads to further JPY selling.

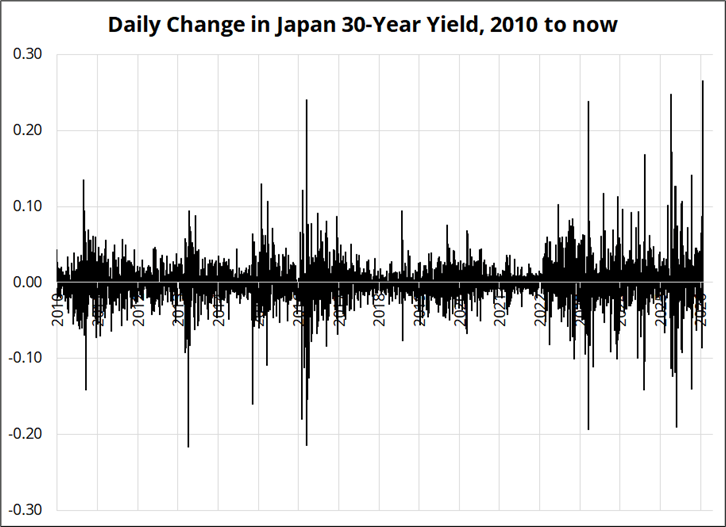

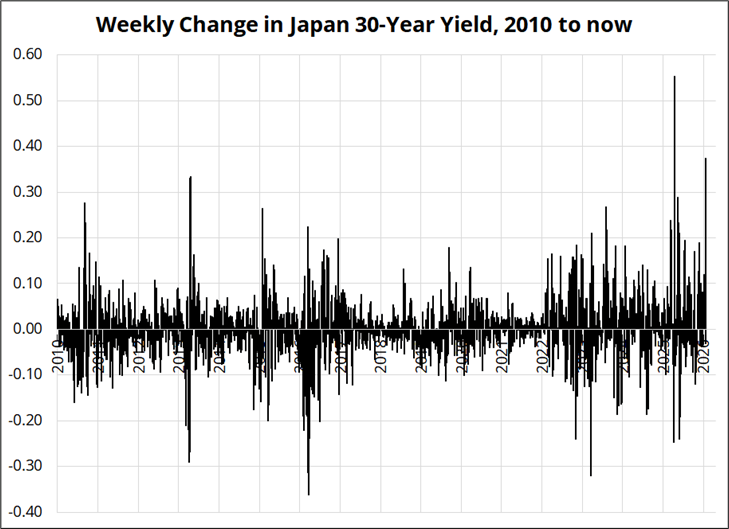

Take a look at weekly changes in Japan’s 30-year yield. The overnight move is the largest since 2010 and a titch larger than any daily move we saw in April 2025.

For perspective, there is still room to run if we are going to match the largest weekly change seen in April 2025. Note we are trading at a higher level of nominal yields now, so one can argue that 37bps today isn’t quite as crazy as 37bps a year ago, but close enough. Yields in Japan peaked on April 15, 2025, and USDJPY bottomed a week later on April 22. At that time, though, the USD was in freefall from a high of 159 in January to a low of 140 that day. The market spent all of Q1 2025 unwinding large, failed bets that the election of Donald Trump was a bullish USD event.

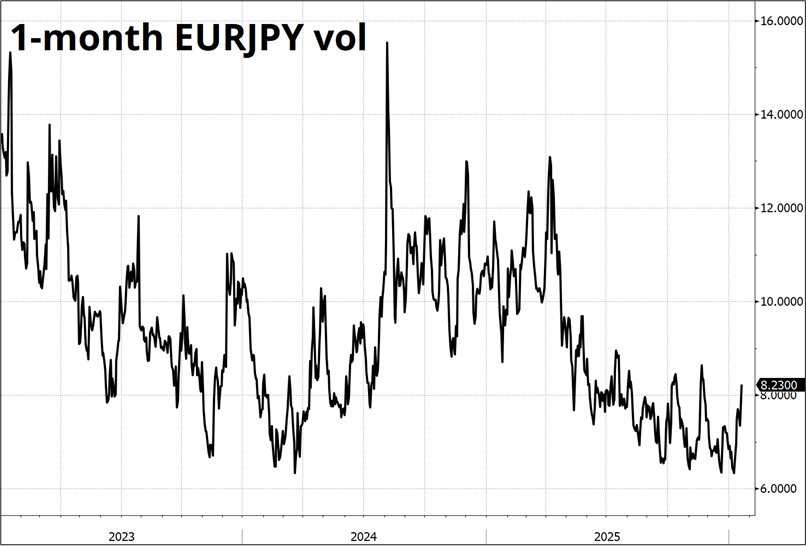

If you are a vol person, 1-month EURJPY gets you a ton of EU and Japan headline ping pong, plus the BOJ this week, the Japanese election February 8, and a possible climax to this current phase of JGB weakness. I find it hard to handicap the sequencing of JPY strength and weakness, but my experience is always that low but rising volatility is the best time to buy. That is the current situation with 1-month EURJPY and USDJPY vol. EURJPY vol at right.

You also get tomorrow’s speech from Trump at Davos (8:30 a.m. NY time). I find it hard to imagine that 1-month EURJPY vols purchased here and traded back and forth would lose much money, but they might make a lot.

Final Thoughts

1. US stocks are negative on the year.

2. EURCHF headed back towards the 0.9200/20 level yet again!

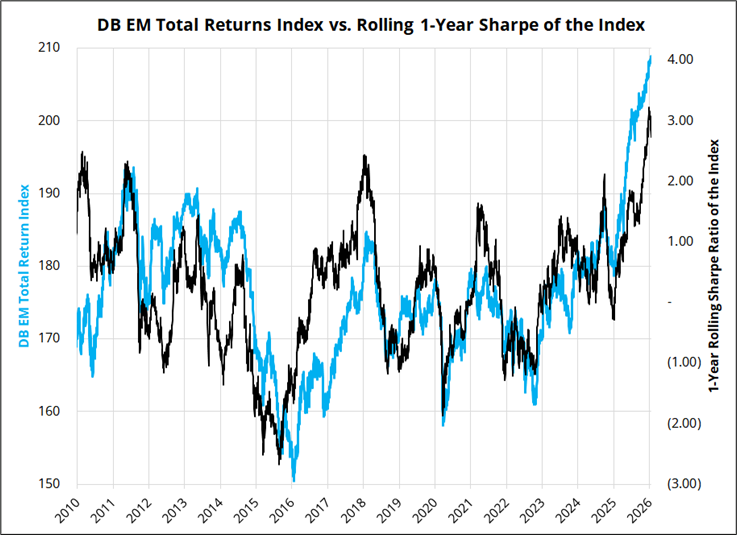

3. Is there a point at which EM can’t take the pain, and it all comes unglued? The Sharpe of long EM has been unbelievably high for a long, long time. I mention this only because it’s almost impossible to even imagine EM currencies selling off anymore because they have been so incredibly all-weather for so long. See chart.

4. Remember US bond auctions were moving yields more than NFP in April/May 2025 so make sure you are on the desk for the auctions this week and next! HT Steph.

5. Read a short essay about my 5-day silent meditation retreat here: Recreational Buddhism. 9-minute read. Not finance related!

Have a peaceful day.