Markets maintain their steadfast optimism

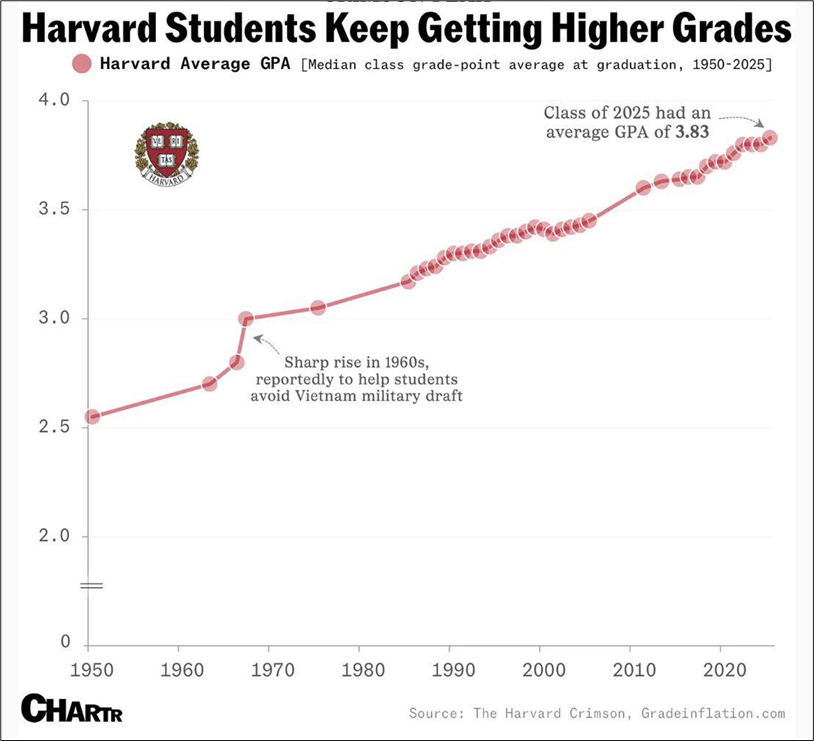

It’s not just Harvard

Markets maintain their steadfast optimism

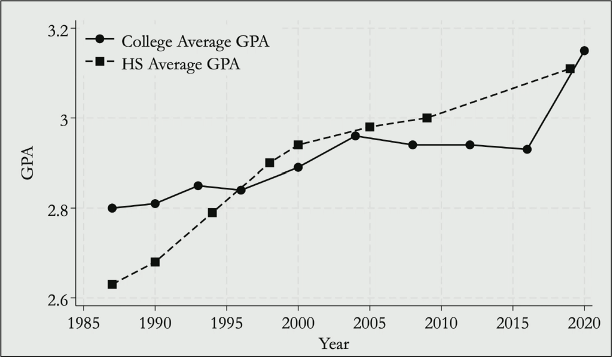

It’s not just Harvard

Flat

The rolling Iran deadline is now 20:00 tomorrow. Markets continue to lean into hope when possible as the low-credibility headlines talking about a “slim chance of a 45-day ceasefire” have triggered another relief rally.

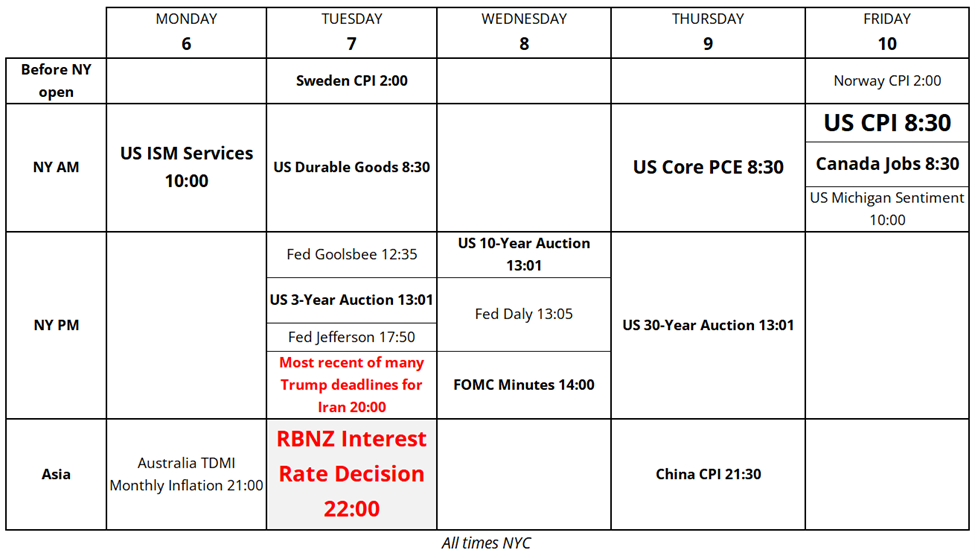

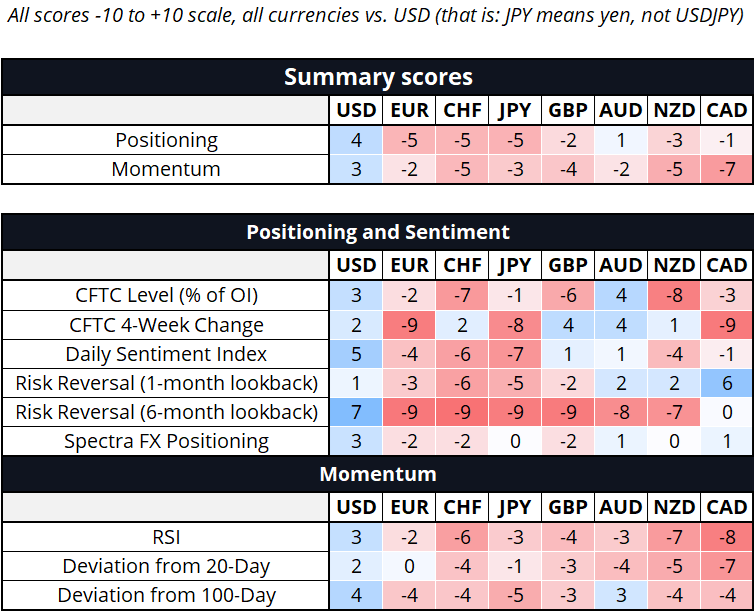

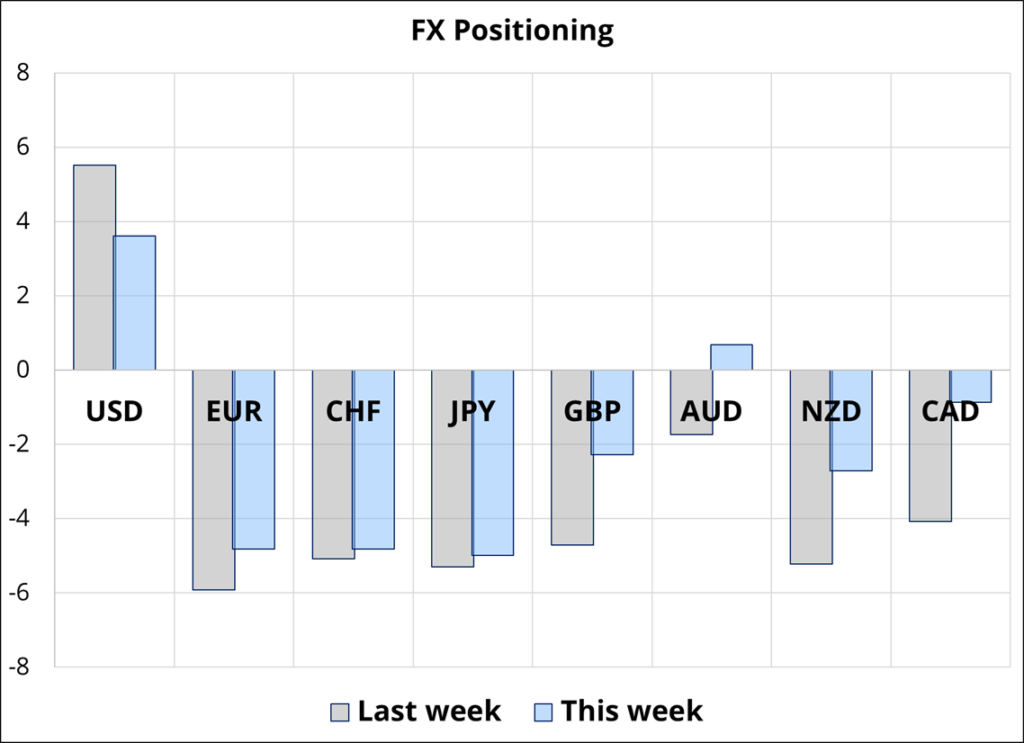

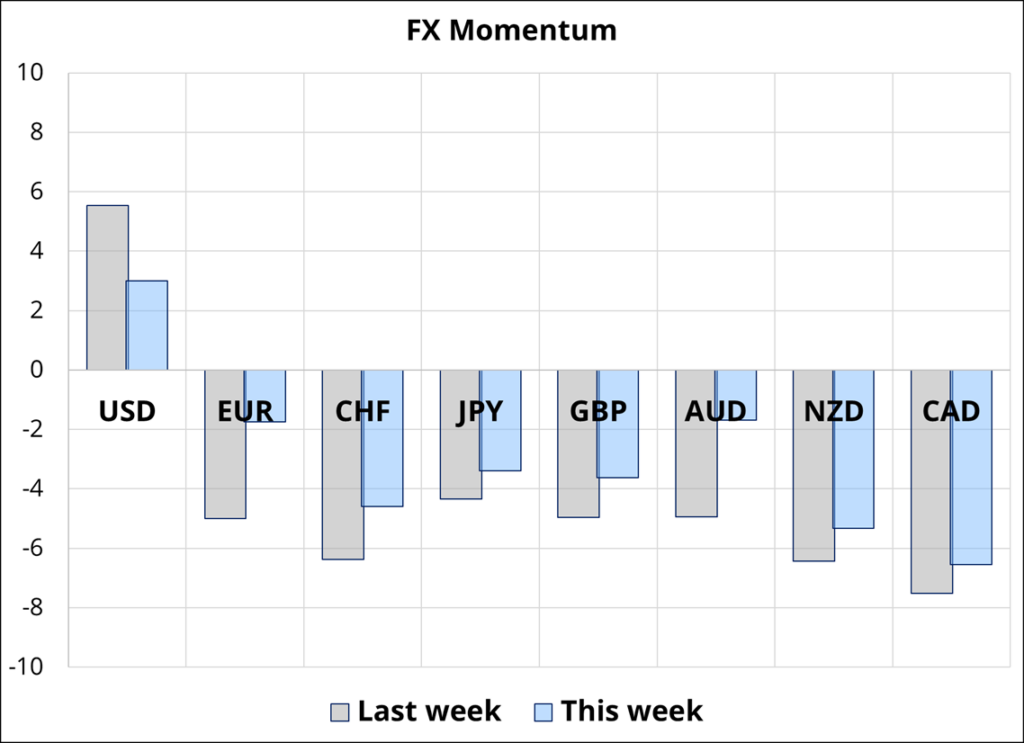

The market has hedged quite a lot in FX, as discussed last week, and options markets and the CFTC show significant USD longs out there. Today’s positioning report (below Final Thoughts) shows similar. USDCNH is also slipping lower, putting mild pressure on the dollar, but overall we are in a stalemate here marked by:

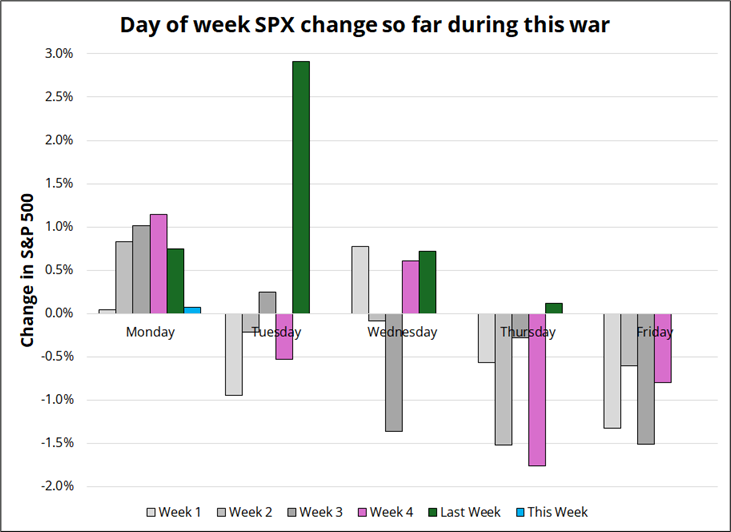

We are now in Week 6 of the war. This is the weakest Monday so far. I show SPX here, though note NASDAQ futures are up 0.7% despite flat SPX. Here’s the chart. No green bar for Friday because stocks were closed in the U.S.

It is hard to make any high-confidence predictions here, but my feeling is that the market continues to use the old “buy the dip on war” playbook. That worked most years, but this conflict might not be like all the others. I suppose we wait for 8 p.m. tomorrow and see what type of attacks Iran and U.S./Israel launch in the meantime.

Despite concerns about what is the largest disruption ever in crude oil supplies, and the fact that the clock is likely ticking on supply shocks in other areas like fertilizer, oil prices remain below the March spike highs across the board. There is some question whether oil futures are telling the full story about physical shortages, but for now, here are NYMEX and Brent, June and December 2026 and June 2027.

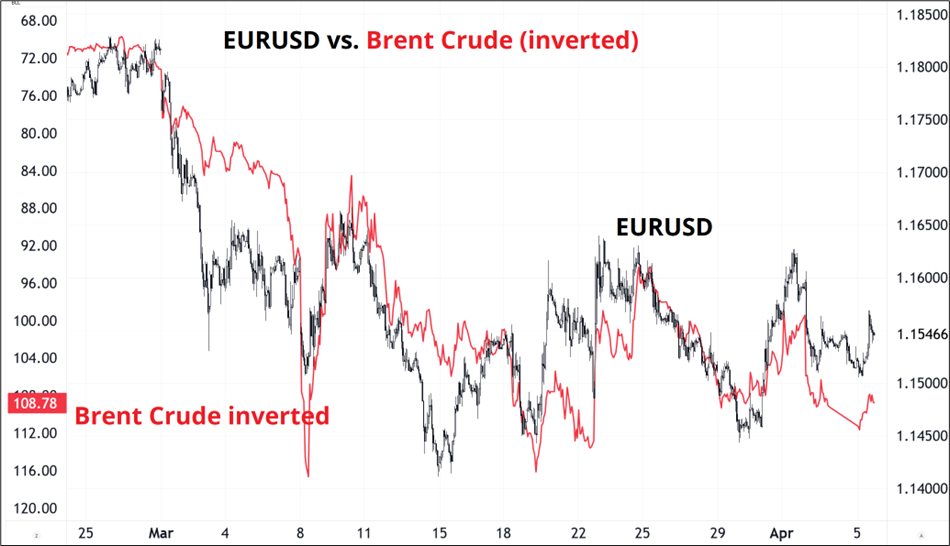

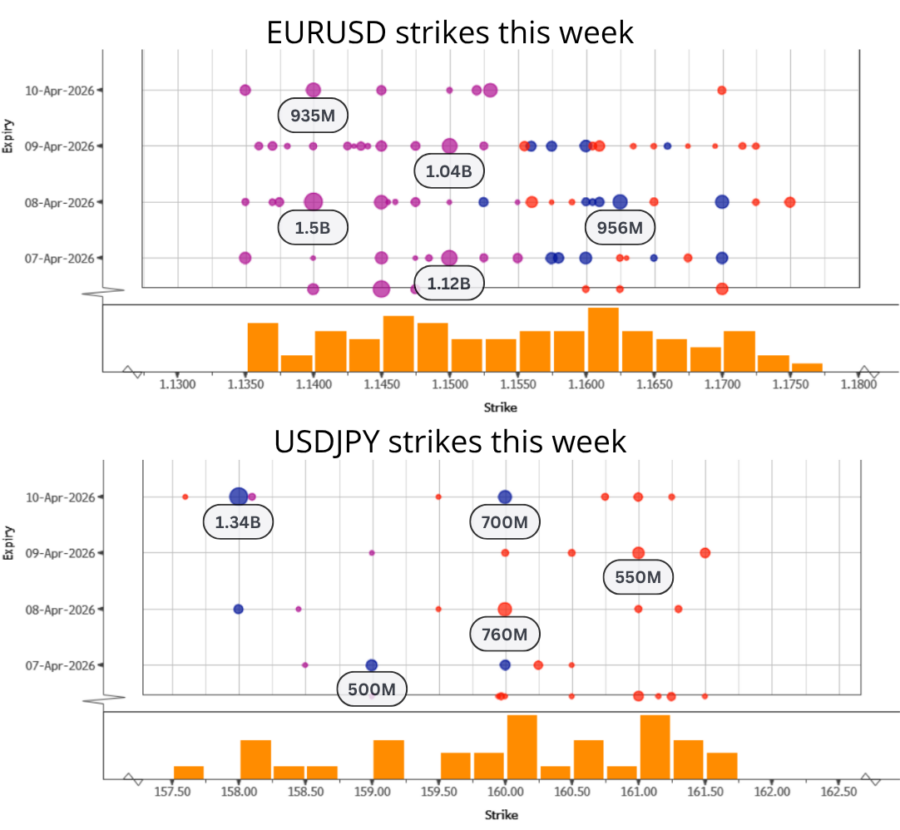

The relationship between EURUSD and oil remains consistent, as both trade in a range awaiting the next stage of the war. It’s important to remember, however, that the asymmetry in EURUSD has flipped. The market was mega long EURUSD at the start of the war. Now the market is heavily short/hedged.

Also, somewhat below the radar due to the war, the U.S. announced another debt bonanza budget for fiscal 2027. This would normally move the narrative needle, but the market obviously has bigger fish to fry right now. To maintain current levels of debt, the budget assumes real GDP growth of 3% for the next 10 years. Over here in the real world, real GDP growth has averaged 2.1% since the year 2000 and only four of the past twenty-five years have been above 3%. That’s why you get radically different debt-to-GDP forecasts from the government and from independent forecasters (as is always the case, regardless of whether red or blue is in power).

Fans of the debasement trade will be cheered by this new budget as April 2026 is far, far away from the days when DOGE was going to reduce the deficit and the story was about a reduction in defense spending. Compare and contrast these two headlines, less than 18 months apart:

Government spending decoupled from orthodoxy in 2017 and as Lyn Alden puts it: “Nothing stops this train.” For now, none of this is relevant, but the consensus view: USD strong until visibility on end of war, then USD weak… Makes even more sense now than it did before this budget was proposed. There is zero chance of fiscal policy ever coming back to reality, regardless of who is in the White House. Massive deficits for guns—or massive deficits for butter.

This is not actionable right now but is relevant to the future path of the dollar (bearish) when this war ends.

We get the first look at the initial stagflationary impact of the war.

Does anyone have a strong view on HYPE and/or PURR? I am doing some research on these things. I start from a position of extreme skepticism with this stuff, and I find myself getting bullish here. Tell me why I am right or wrong. Please.

Hi. Welcome to this week’s report. To read about how I use and trade this report, see here. Positioning has come off the boil a bit but remains heavily long USD. The CFTC, options markets, and our flows all suggest that the market continues to hedge via long dollars despite mostly medium-term bearish views. This conflict between short-term positioning and the consensus medium-term outlook is unusual and interesting.

It’s not just Harvard

https://hechingerreport.org/proof-points-grade-inflation-lower-pay/

“Students who experienced more lenient grading were less likely to pass subsequent courses, posted lower test scores afterwards, were less likely to graduate from high school and enroll in college, and earned significantly less years later.”