A BOJ hike has been priced out and the Fed might send in the hawks.

On this day in 1995, the European council decided that the single currency would be called the “euro”. They rejected options including the ECU, the florin, the ducat, and the crown.

A BOJ hike has been priced out and the Fed might send in the hawks.

On this day in 1995, the European council decided that the single currency would be called the “euro”. They rejected options including the ECU, the florin, the ducat, and the crown.

Short AUDNZD @ 1.1100

Stop loss was 1.1361 now 1.1111

Close 31DEC 7:30 a.m.

Short EURSEK @ 11.52

Stop loss 11.7110

Cover 31DEC 7:30 a.m.

In this edition of am/FX, I will go through some events this week and handicap the outcomes and asymmetries. The event docket kicks off today at 9:45 a.m. as we get the first US data point for December (other than last week’s Claims figure). S&P PMIs will come out (both manufacturing and services) and we will get to see whether the Trump bump sustains or whether increased policy uncertainty weighs more heavily than deregulation and tax cut hopes.

With just about nothing priced in for the BOJ now, short USDJPY on weak PMIs could be nice as the bond market has pivoted to worrying about higher inflation and so a weaker PMI release might catch everyone wrong-footed.

While there is no strong reason to expect a BOJ hike on Wednesday night, this does feel a lot like December 2022, when the JPY was trading weak, the market had given up on BOJ normalization, the press was leaking dovish BOJ angles, and then the BOJ proceeded to widen the band on the 10-year yield. USDJPY went from 137 to 131 that night, bounced for a week, then finally bottomed at 127.97 on January 13.

The lessons from that episode (and all the other BOJ episodes) were a) the BOJ can surprise! It’s possible and b) BOJ policy is a short-term variable impacting USDJPY around announcements and repricings, but ultimately US yields drive the bus.

We get a speech from Bank of Canada’s Macklem today at 3:45 p.m. NY. The topic is: Economic Factors Shaping Canada’s Monetary Policy and so it doesn’t get more hardcore than this. The text will be released here at 3:20 p.m. NY time. USDCAD is relentless right now as the market needs to price in a litany of risks for 2025. Slower immigration, too-high real rates, monster consumer debt exposures, and potentially cataclysmic tariffs hang like four swords over Damocles. I have no strong view on what Macklem will say, but the last BoC meeting was kind of hawkish, and USDCAD is now making new highs, so the asymmetry continues to be weaker CAD. If you work at a bank or hedge fund: Sell 1-month 1.45 OT and buy 3-month 1.45 OT looks super high EV to me.

Tomorrow we get Canadian CPI followed by US Retail Sales, and Wednesday we see UK inflation and then the FOMC decision. I see the potential for a very hawkish-sounding meeting as the interest rate cut is possibly unnecessary, but already baked in. Jim Bianco had a nice chart in one of his tweets on the weekend, and I have recreated it going a bit further back so you can see that it’s rare for the Sahm rule to trigger then untrigger.

This was predicted by Claudia Sahm and others, and shows (yet again!) that this cycle is not like the others. Employment momentum is usually one way, but this cycle the rise in the UR is not a nefarious start of collapsing employment, but simply a return to equilibrium after an overheated economy and labor supply shock in 2021/2022.

Despite concerns about various under-the-hood issues with the labor market that go all the way back to 2022, the US labor market looks perfectly fine to me in aggregate. With so many labor market indicators to choose from, there is a huge cherry-picking problem as you will see people point to the household survey when it’s weak but ignore it when it’s strong, or point to the QCEW when the headlines are strong and it’s weak, or Continuing Claims when it’s showing weakness while Initial Claims do not. There are dozens of indicators, so if you want to find a weak labor market, you can always find one somewhere in the data.

The Kansas City Labor Market Activity Index solves this problem somewhat as it aggregates 24 labor market variables and takes a weighted average to come up with a monthly measure gauging the level of US labor market activity. These things are always subject to some issues around parameter choice (what variables do you pick? Are they too correlated to each other? What weightings do you use?) but at least it offers up a less biased look at the labor market than a perennially bullish or bearish economist’s cherrypicked data points.

Here is the chart of that indicator.

What I see here is a labor market that was pretty much the hottest ever now coming back to levels that still put it in the 60th percentile or so of US labor markets all time. I accept that this looks a lot like 2000/2001, and there is the risk that overinvestment in AI creates a disastrous capex cycle like that one and the labor market collapses similarly in 2025 or 2026. But for now, there is no evidence of that. The labor market is as healthy now as it was in 1995 when we had a similar soft landing, precautionary Fed cuts, and a Fed on hold for all of 1996.

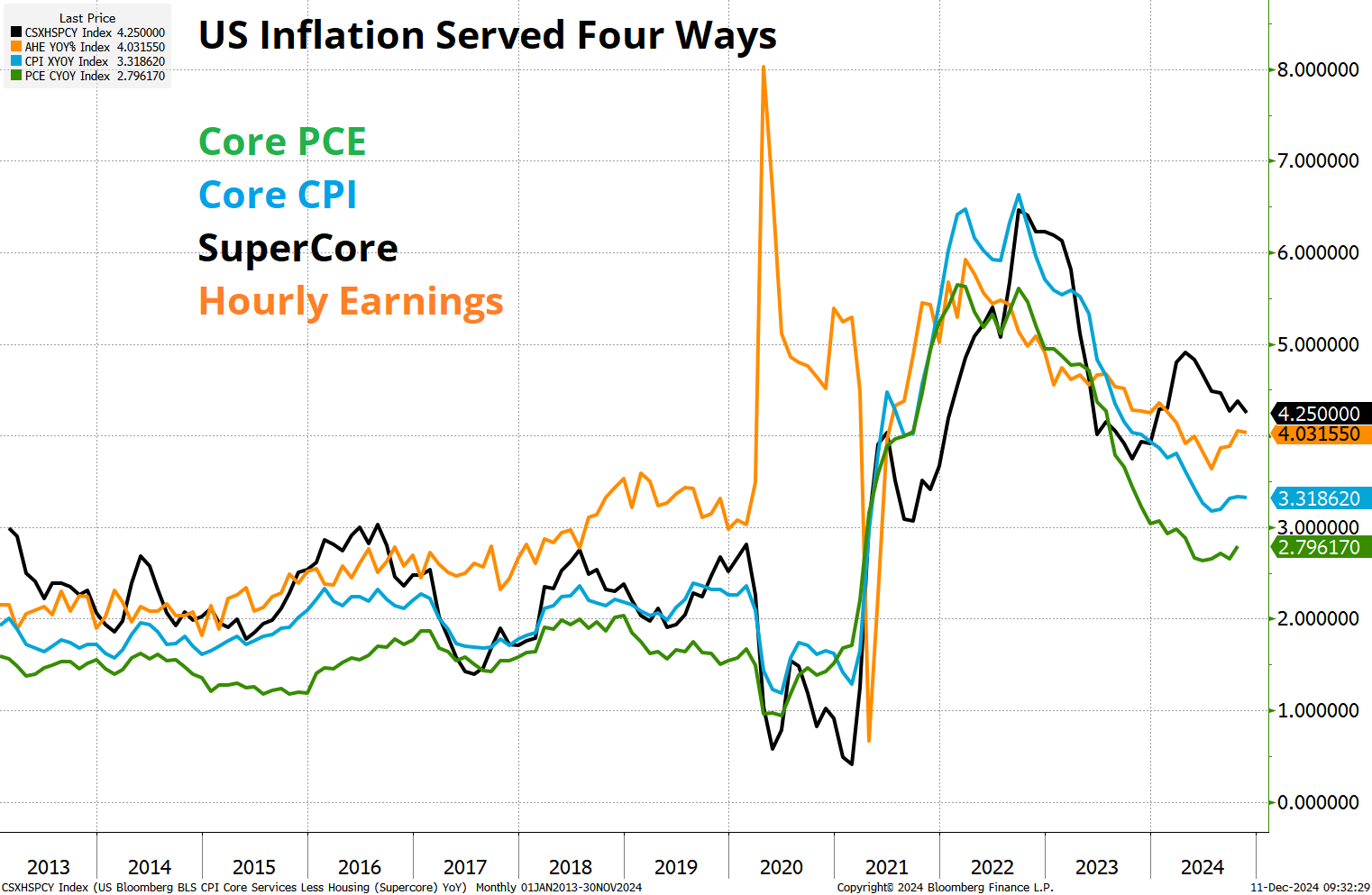

And while the labor market looks fine, inflation looks like it’s bottoming way above the Fed’s target.

I think the Fed will now be worried about a resurgence of inflation as an unknown policy mix and sticky prices create many paths for inflation to make a comeback in 2025. And therefore I think they will signal a very cautious approach going forward and lean on language that suggests concerns about inflation and a higher neutral rate.

Here is this week’s calendar, in all its glory.

The EURSEK seasonal short has started out well and AUDNZD has turned back lower after a disappointing rally from 1.0950 to 1.1050. Seasonal USD weakness remains elusive as macro remains bearish but positioning and seasonality remain bullish. Stalemate.

Have a singular week.

On this day in 1995, the European council decided that the single currency would be called the “euro”. They rejected options including the ECU, the florin, the ducat, and the crown.