FX and other thoughts for a Thursday

The relative importance of Greenland to financial markets

FX and other thoughts for a Thursday

The relative importance of Greenland to financial markets

Flat

I got some rational pushback on the GPIF thesis laid out yesterday. Two main points people made:

Maybe it will be Japan Post or Kampo that leads the way if this were to happen, then. Or, in an emergency, I still think GPIF could be the one. But it’s difficult to define what might qualify as an emergency as markets have been freaking out about Japanese yields for at least a year and the Japanese government is pretty chill.

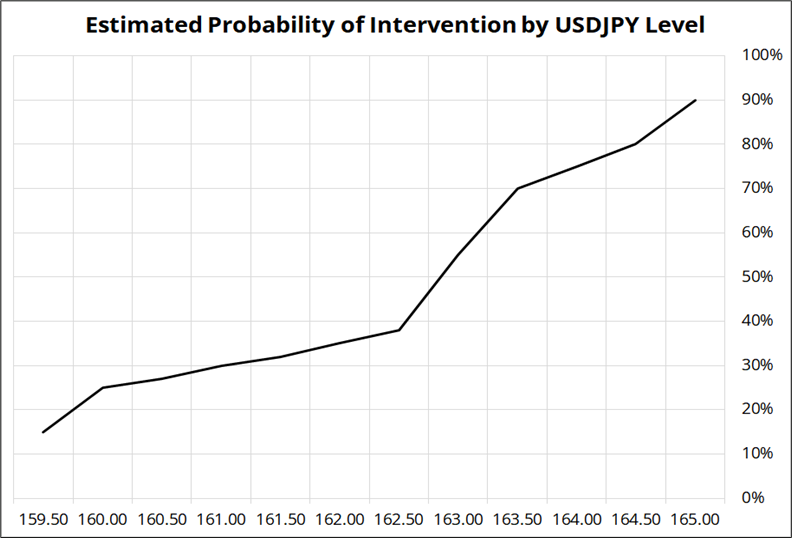

Zooming back in, we have the BOJ tonight and then the election on February 8. There is a small tail risk for each event. For BOJ, they could be hawkish or hike. For the election, Takaichi could have badly misplayed her cards and voters don’t give her the mandate for as much fiscal zippiness as she intends. On top of those, there is non-zero intervention risk as USDJPY nears 160. That risk gets higher as USDJPY rises. Here is my estimate of intervention probabilities, by USDJPY level (assuming we get to these levels within the next 10 days).

The line steepens significantly above 162.50 as that would not only be new cycle highs for USDJPY, it would trigger the 4% in four weeks and 5% in six weeks triggers. 165.00 triggers every single rule of intervention possible.

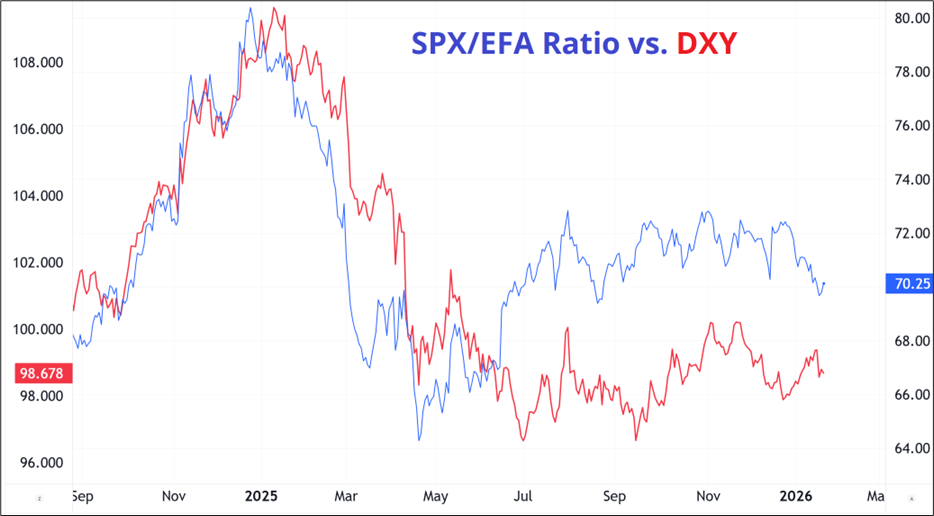

Geopolitical tensions have thawed considerably and while markets were on ice for 24 hours, they landed quickly back in the green yesterday. Showmanship! This puts to rest the SELL AMERICA theme that lasted less than 48 hours and now we can go back to wondering whether foreign money will change its mind on US exceptionalism. Ratios of USA to everything else did not bounce much after yesterday’s cancellation of threats.

Here is the ratio of non-US equities (EFA ETF) vs. US stocks (SPY). As with many asset classes (bonds and FX, especially) this shows a rough equilibrium was reached shortly after Liberation Day and there was some mean reversion, but not a return to the pre-election levels of exuberance about the USA.

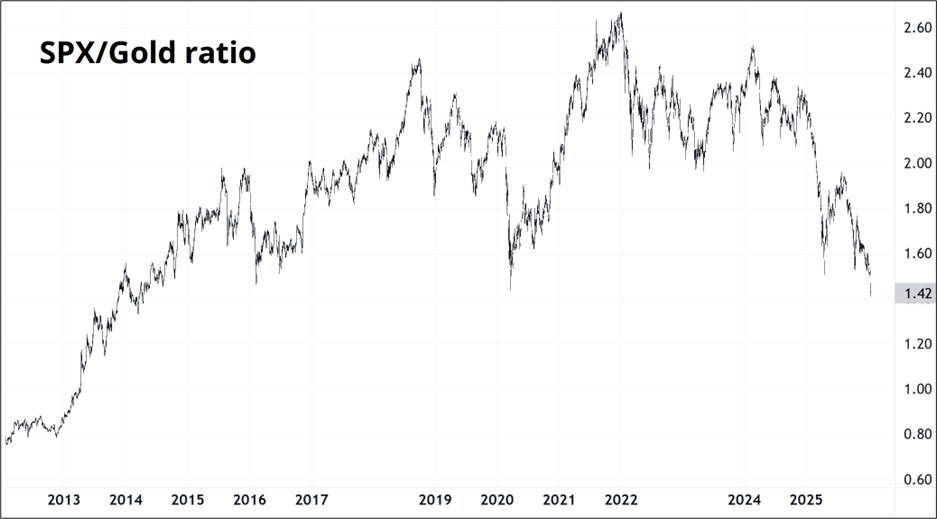

And while diversification into global equities remains a popular idea, the move into precious metals shows a stronger aversion to the global policy mix. Here’s the SPX vs. gold ratio back to 1952, just for kicks. This chart massively overstates the attractiveness of gold, of course, because SPX offers another 2% per year, compounded. Still, you can see that US equities (relative to gold) are back to where they were pre-COVID.

I am not sure you can run technical analysis on this sort of chart (maybe you can!) but if we zoom in to the post-GFC period, we are right on support. The 1.40/1.45 level was touched on the China deval shockwaves and oil collapse in early 2016 and again in March 2020 on COVID. We are currently at 1.42.

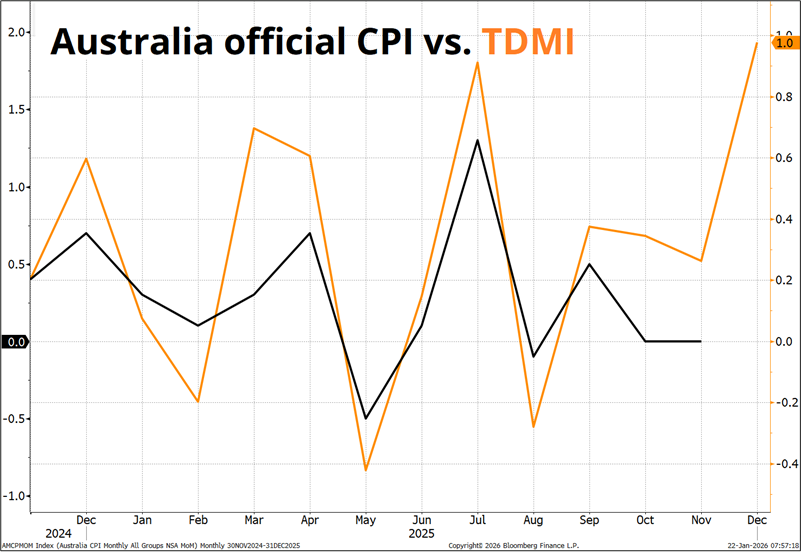

AUDUSD is finally doing what it was supposed to do and last night’s stonking employment data helps considerably as the RBA is the only central bank in the world that could potentially hike rates in the near-term. Note that we get Aussie CPI next week and the unofficial data from the Melbourne Institute (TDMI) came in super strong for December (+1.0%). You can see here that the TDMI data tracks the official monthly data quite well. So, it’s good to be ready for a strong CPI in Australia next week. People are probably aware of this relationship and so that should keep AUD bid into 27JAN.

The RBA meets on February 3 and it’s 60% priced for a hike. With a strong inflation print on 27JAN, that will go to 100% and AUDUSD could be another 100 pips higher. I will be looking to get long AUD into CPI but that’s a trade for early next week, I believe. GBPAUD and GBPNZD lower are becoming themes with room to run.

George Orwell: Politics and the English Language (1946)

Have an ice-cold day.

The relative importance of Greenland to financial markets