With the blowoff top in crude and big moves elsewhere, risk/reward has changed

highlights

Risk/reward improving

Current Views

Short 07APR EURCHF 0.9010/0.8960 put spread +

long 07MAY 0.9110/0.9160 call spread for 2bps

Idea is that EURCHF holds around here due to SNB intervention and then we rally when the war is over

There is a margin of safety now

The debate over when and where and if to buy the dip in risky assets continues and while I have been mostly bearish world, bullish oil, and short risky assets since the war started, I think the risk/reward is starting to flip. There is a pretty juicy risk premium in markets now.

It will only feel completely safe to buy risky assets well after they have exploded higher, so I think it’s worth sticking a couple of toes in the water now. That said, there are plenty of reasons to be scared still. Let me go through some of the pros and cons of the current situation.

Cons

Most of the cons are well known, but I still want to think them through:

- The best oil experts mostly agree that prolonged closure of Hormuz is the worst-case scenario for oil markets.

- Even if the U.S. and Israel look for an offramp as they run out of attractive targets to bomb, Iran does not necessarily have to play ball. Their best strategy is to drag out the conflict, as the political and economic costs of the war rise with each day.

- Regime change isn’t happening right now. Air attacks and the killing of a leader have never successfully led to regime change in the Middle East. Now, there is a younger, harder line leader of Iran and the people of Iran are not out in the streets like they were in the weeks before the U.S. started bombing. So far, the experts were right.

- Opaque objectives mean a prolonged war is very much possible. Objectives in the Middle East tend to evolve over time with no clear visibility to what might mark the end of the conflict.

- Soft landing is dead if this continues. Central bank pricing has moved to stagflation worries as U.S. jobs growth is negative.

- Higher yields around the world and lower stock prices are hurting confidence and tightening financial conditions.

- Fast money has probably exited foreign equity overweights and EMFX longs, but real money is still hugely long Nikkei, KOSPI, DAX, and MXN, BRL, HUF, etc.

- Oracle continues to pull back on its AI capex ambitions, possibly reflecting peak AI optimism is in the rearview.

- Private credit was already casting a pall over the market before the war.

- Fear factor is still fairly low.

Those negatives are meaningful given there has not been all that much downward movement in equities. On the other hand, we have seen massive moves in oil, front end rates, EMFX, and other asset classes. It looks to me like the risks posed by the War in Iran have gone from grossly underpriced to something like fairly priced. I would rather be dabbling from the bullish side here now. This is not a strong view that the worst has passed; it’s a medium-conviction view that the risk/reward now mildly favors the bulls.

Pros

Here are some reasons to be optimistic:

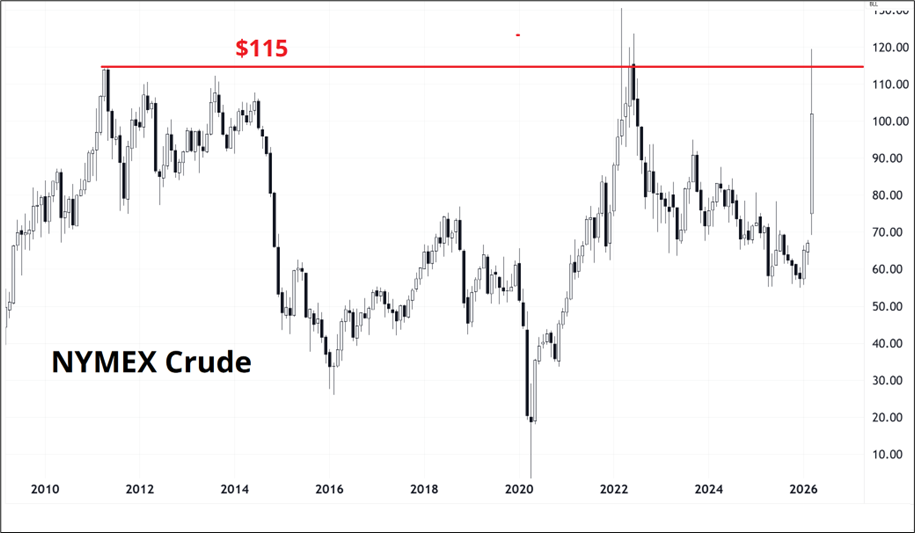

- The Sunday night blowoff in oil took us close to the same level as the Russia/Ukraine Sunday night blowoff. This sets up potential for a triple top in oil. One might argue that technicals don’t mean much in a news-driven environment, but I disagree. We topped out at $119 last night and have dropped $14 on no news. Exogenous and endogenous factors work together. NYMEX crude has rejected every move above $115, going all the way back to 2010. This could be meaningless given the tremendous increase in the broad price level ($115 in 2026 is not the same as $115 in 2010) but whatever. The chart is the chart. For now, we have rejected a famous level on a Sunday night. That’s not bullish for oil.

- Probability of a declaration of victory is higher now that oil prices have exploded. My base case (as discussed last week and in the podcast) is that Trump will feel the pressure of rising gasoline prices and the falling stock market and that is the ultimate limiting factor on war policy. Recall that Liberation Day was April 5, and the administration capitulated on April 9. As discussed in the cons, this isn’t as easy because there are two sides here, but any walkback by the U.S. will trigger a huge fall in oil prices, regardless of what Iran says or does. I don’t know exactly what a walkback would look like. Anything from “We did it! We won!” to “Halting strikes for one week to assess impact.”

- US not happy with Israel bombing fuel sites. Cracks in the alliance may point to deescalation?

- Kharg Island untouched so far. See FT article here.

- ORCL right-sizing its AI ambitions could be seen as a positive. The completely ridiculous numbers in their initial announcement (numbers written on napkins, not in enforceable contracts) triggered the 50% collapse in the stock. Maybe this right-sizing will stabilize things. As for NVDA, I am sure they can use the Stargate chips somewhere else if Oracle doesn’t want them. Note Oracle releases earnings after the close tomorrow.

- Overall asset pricing shows much more stress now than it did last week. For example: Risk reversals in FX made another huge move, and front end rates market pricing is getting fairly wild (see chart).

To summarize my view:

- Path of least resistance is no longer higher oil and weaker EM as the market is no longer complacent.

- Risk/reward for the White House has now changed with oil above $100 and many targets bombed. That means market risk/reward has changed too.

- There are still many paths in each direction, but risk/reward is starting to favor the bold.

- Risk management is key because tail risk is meaningful in both directions still.

If you are looking for bullish ideas…

- EURHUF lower for the election via put spreads or calendar spreads. Incredible entry point here. If you are a Spectra FX Solutions institutional client, please ping me on Bloomberg for some ideas.

- AUDUSD higher. Holds well. No new low. Positive relative strength.

- Long KOSPI. The big levels in Korean equities have held. Here is the KORU ETF, which continues to hold the key 275/300 zone. Below $260 this thing is wrong.

- Long EURCHF. You get SNB kicker and a clear stop below 0.8950.

- Long bitcoin, stop below 64,000. It is showing a ton of relative strength. Leveraged longs all gone, I suppose.

Calendar

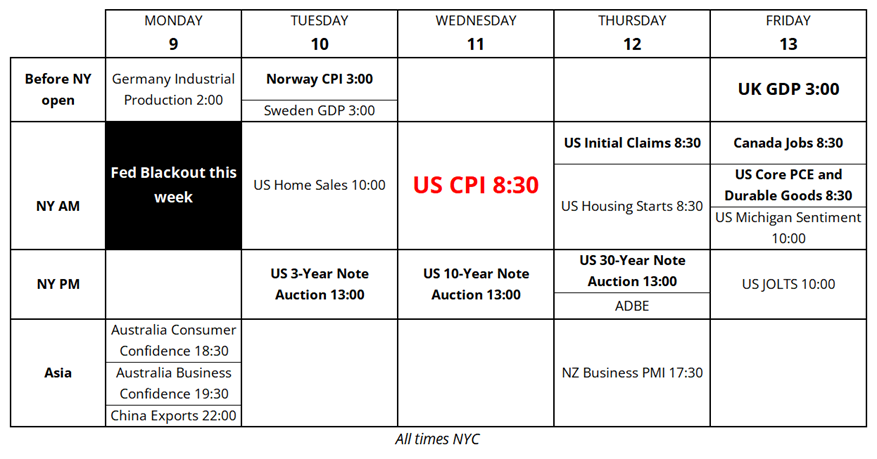

CPI at the center of this week’s calendar, with some other tidbits like Norway CPI and UK GDP. Obviously the old CPI figures don’t mean much in a world where crude oil prices have almost doubled in two weeks.

Final Thoughts

- A common question I get is: “How do I use the Spectra FX Positioning Report?” It’s a good question requiring a detailed answer. I will publish a full explainer on where the numbers come from and how I use them next Monday (16MAR).

- On this day in 2009, the S&P 500 traded below 700 for the last time.

- I’m off Wednesday, Thursday, Friday this week. FYI!

I hope you spend no time underwater this week.

The Spectra FX Positioning and Momentum Report

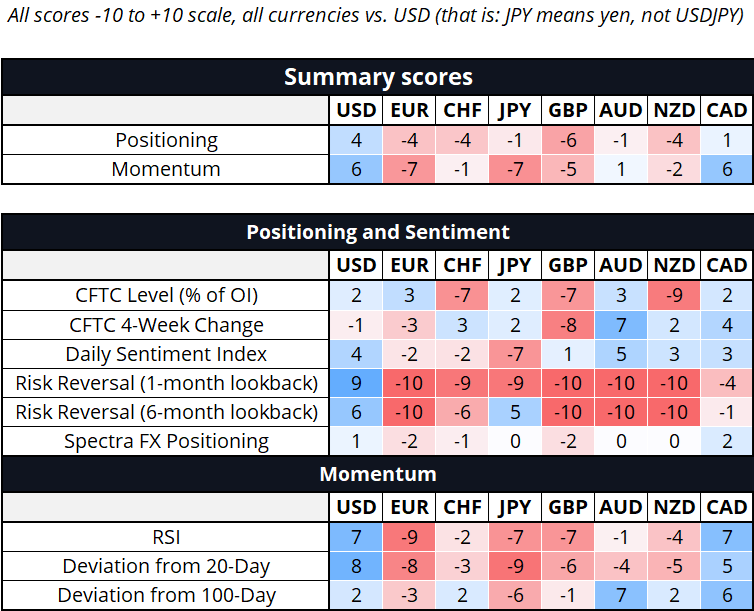

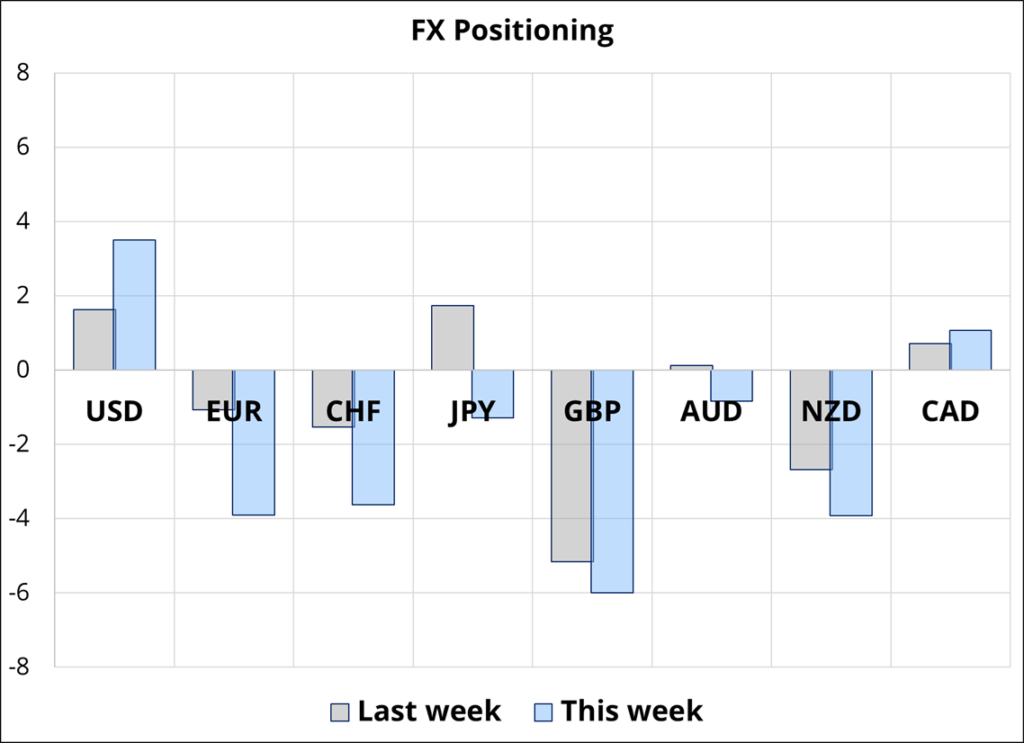

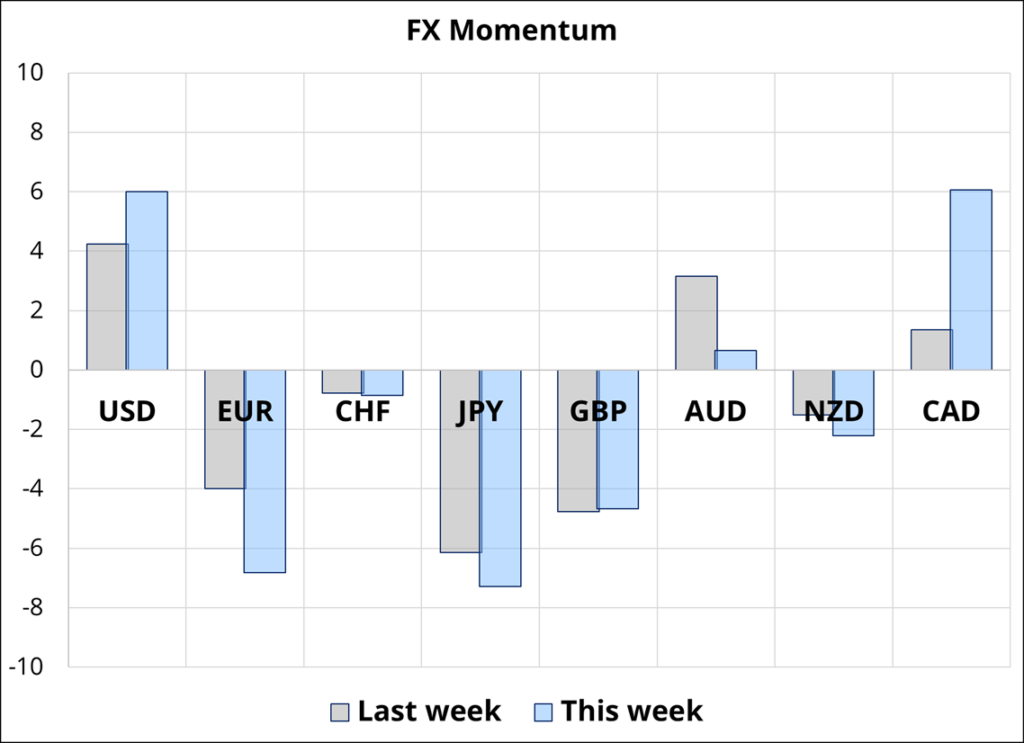

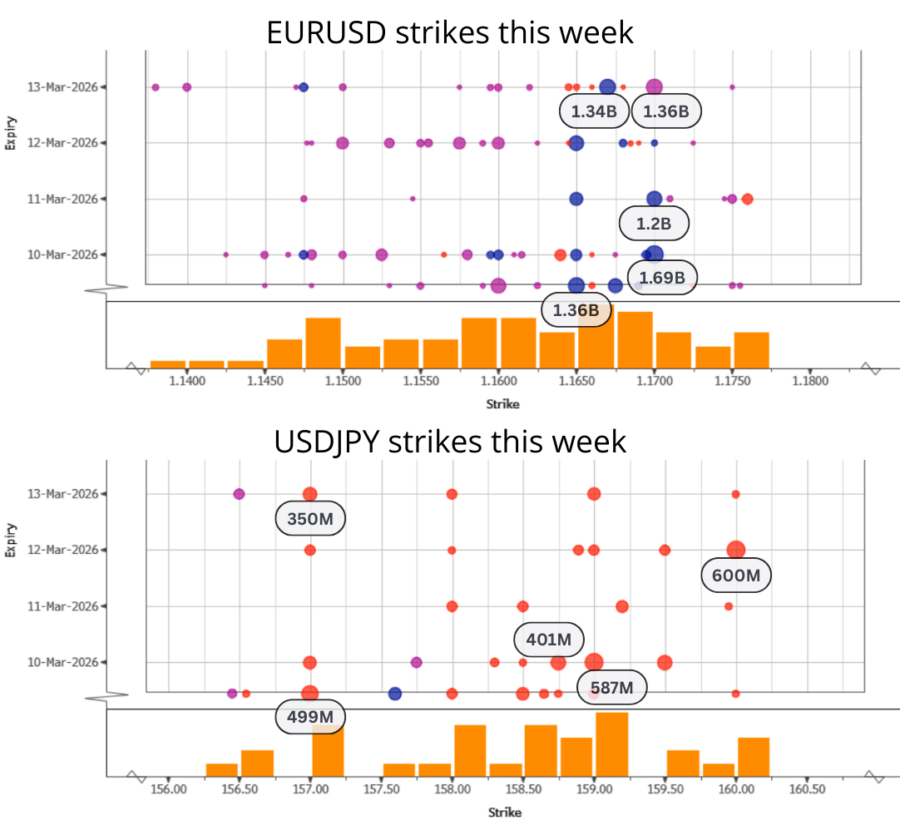

Hi. Welcome to this week’s report. Giant moves in the risk reversals are indicating that the market is hedging short USD positions and/or going long USD. The CFTC is also dumping GBPUSD and cable shorts are nearing 5-year extremes. There is room for a huge rally in GBP and AUD particularly if visibility on the end of the war is somehow achieved. We don’t run the data for EM because of sample size issues, but EM would look similar to AUD here. Cartloads of 1.1650s and 1.1700s coming off in EURUSD this week.

G10 FX Positioning and Momentum Scores

Big Strikes

Thanks for reading.