The risk/reward on short EURUSD no longer looks compelling

Dutch Reverse Racing

The risk/reward on short EURUSD no longer looks compelling

Dutch Reverse Racing

Short EURUSD @ 1.1729

Taking profit today at 1.1605

Stop loss 1.1867

Take profit 1.1511

Long GCQ6 at 4610

Stop loss 4294 Take profit 5320

The more I think about the Waller speech tomorrow, the less confident I am that he is going to pivot to a more hawkish stance. Upon re-reading his April 17 speech, it seems his two main policy paths are either going back to cuts or staying on hold. Here’s how he sees the “Hormuz is closed for a long time” scenario.

The longer energy prices remain elevated and the Strait is constrained, the greater the chances that higher inflation gets embedded across a wide variety of goods and services, various supply chain effects start to emerge, and real activity and employment start to slow. I will be particularly attentive to indications that this latest price shock, on top of the effects from tariffs, has moved up inflation expectations. A slower economy would restrain demand for goods and services, and perhaps soften the increase in prices, but I expect higher inflation than in the first scenario and that it would be elevated for some time. In this case, I also believe we would have a weaker labor market. High inflation and a weak labor market would be very complicated for a policymaker. If I face this situation, I’ll have to balance the risks to the two sides of the Fed’s dual mandate to determine the appropriate path of policy, and that may mean maintaining the policy rate at the current target range if the risks to inflation outweigh those to the labor market.

So, upon further review, I am less convinced that he will flip into the hawkish camp. The thing is, if he does, the expected value of simply buying USD on that headline will most likely be higher than staying long USD into the speech and hoping for the best. So, I am covering my short EURUSD here for a gain of about 130 pips and I will trade whatever I see tomorrow. Also, as I said yesterday, the sentiment and positioning setup has changed. The market is no longer short USD.

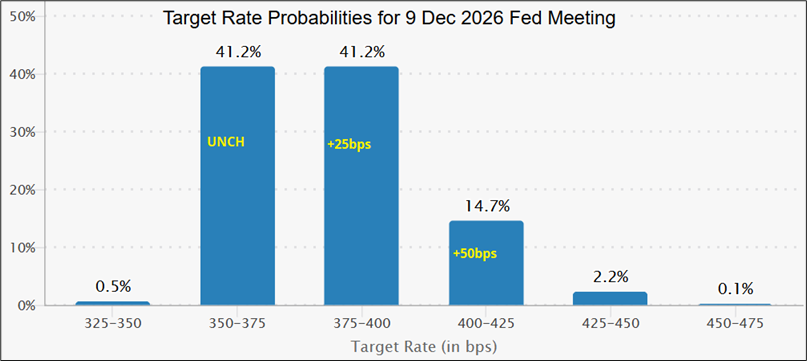

With some hikes priced in (see chart) and Warsh about to take the helm, I think it’s better to acknowledge there is two-way risk to Fed pricing from here and wait and see what Waller says.

If he’s dovish, we probably get another huge leg higher in the AI trade and if he’s outright hawkish, buy USD. So that is my plan.

Buy TQQQ on dovish and sell EURUSD on hawkish. I strongly recommend you read the April 17 speech if you have not yet done so as it provides critical context around Waller’s speech tomorrow.

The toughest outcome to trade, and my base case is a bunch of “on the one hand but on the other hand” kind of comments, something like:

Inflation is elevated and uncertainty is high. The current policy stance is appropriate. I am not ready to cut until I see clearer evidence that disinflation is back on track or that the labor market is weakening materially. If energy prices normalize, cuts later this year remain possible. If inflation expectations or broader pass-through worsen, the Committee must be prepared to respond

If he opens the door to hikes at all, that’s hawkish. If he pushes back on no cuts in 2026, that’s dovish.

“Outlook for the U.S. Economy and Monetary Policy” 10:00 a.m. tomorrow

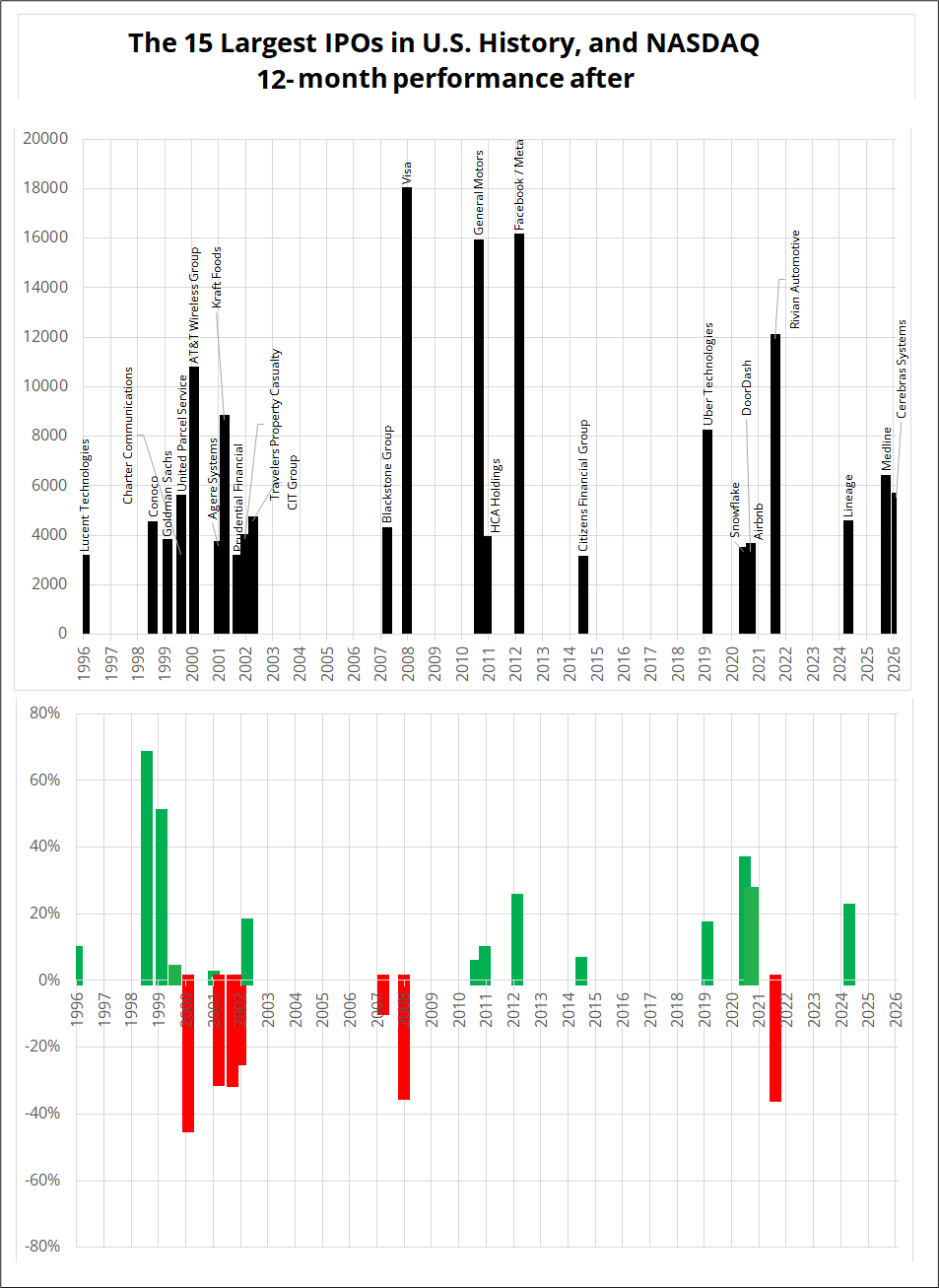

With an unprecedented flurry of ginormous IPOs imminent, many clients have asked me whether I believe the massive wave of equity supply will be bearish. The simple answer is that, yes, it is almost surely a bearish factor, but it is not tradable in isolation.

This chart shows the 15 largest IPOs by U.S.-headquartered companies and below that is how NASDAQ did in the next 12 months. You can see the flurry of IPOs preceding the dotcom bubble burst and the 2008 GFC, along with other less nefariously-timed IPOs. Note that the largest IPO on there is Visa at $18 billion and the SpaceX IPO could be around $75B(!). Largo. And OpenAI could be another $60B. Can the market absorb that much selling? Again, I would definitely mark down the coming IPO wave as a potentially bearish factor, but not a reason to exit longs or get short.

I am particularly interested to see how TSLA and VCX and a few other specific stocks play out. Tesla is a container / memestock for anyone who wants to invest in Elon Inc. SpaceX will likely dilute the Elon-lover vote and send some dollars out of TSLA into SPCX.

Tesla’s years-long persistent overvaluation vs. peers conundrum means the question is relevant because any mild reversion towards car company valuations would be disastrous for the stock.

But then again, the robots are coming right?

VCX is a bit like GBTC in that it’s a closed-end fund trading light years above NAV because retail traders can’t get access to SPCX, OpenAI, and other hot up and comers. Presumably money will flow out of that thing into SPCX as well. By the time SPCX and OpenAI go public, one might logically assume that VCX will converge from $250 currently to its $19 NAV. Not investment advice. Convergence to fair value is not guaranteed and can take longer than you or I can remain solvent.

Here is a good writeup on the current state of software and AI.

https://www.sparklinecapital.com/post/ai-disruption

If you run it by ChatGPT it says the readthrough is to buy CRM, ADBE, and INTU while Claude thinks it means you buy CRM, ADBE, WDAY, TEAM, and NOW. Most of the credible analysis I’ve been reading lately concludes: CRM and NOW will be beneficiaries of AI; they will not be Saaspocalypse victims when all is said and done. INTU got smoked last night on good earnings.

Have a high speed, forward-driving day.