Smells like Liberation Day.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Smells like Liberation Day.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Editorial note:

Before we start, a quick note: War is not a joke and I understand that real mothers and fathers are out there mourning dead sons and daughters. Honestly, I would rather not write about war and its effects on markets because I think the whole thing is gross. But this is my job, so I carry on.

Same deal with politics. I hate it. I dislike almost every U.S. politician on both sides equally. But normally you can quietly ignore all the political idiocy and hypocrisy because it doesn’t leak into the world of markets. In a sane world, good government works like a good referee: present, enforcing the rules, but invisible.

Bad and self-centered showboat referees and umpires make themselves the center of the game. The current government is the biggest, most interventionist, and most publicity-seeking of my lifetime and is constantly intervening in markets via direct state intervention or random policy shocks. So as much as I would prefer not to write about politics or war, I don’t have much choice.

My only other option would be to move to Maine and write novels—but I’m not quite ready to do that yet. Soon, but not yet. So while it often sounds like I am anti-Trump… Really I am anti-big government, anti-war, and anti-politics. I hated Biden’s 2021 fiscal stimulus and I hate the relentless government interventions in 2025/2026. I am an equal opportunity hater.

End of intro. Let’s get started.

The textbook moves in early March are done and now the dust settles and everyone is trying to figure out what matters beyond the kneejerk. For example, can the US economy survive a 35% rally in crude and the tighter financial conditions and higher gas prices that come with it? Can stocks go up while the Strait of Hormuz is closed? Can Iran become a newly confident global power earning ginormous toll revenues without blowback from the U.S. at the end of the two-week ceasefire? And so on?

I do believe there is a world where oil prices can remain high, supply can remain an issue, and stock prices just ramble on back up to the highs. Much like the cacophony in 2018 with China and the Liberation Day on/off switch, this feels like another situation where the fire gets hot enough that the arsonist finds a firehose, and that eventually leads to calm as people see the random policy shocks are fundamentally mean reverting as some or all of the actors have a finite pain threshold.

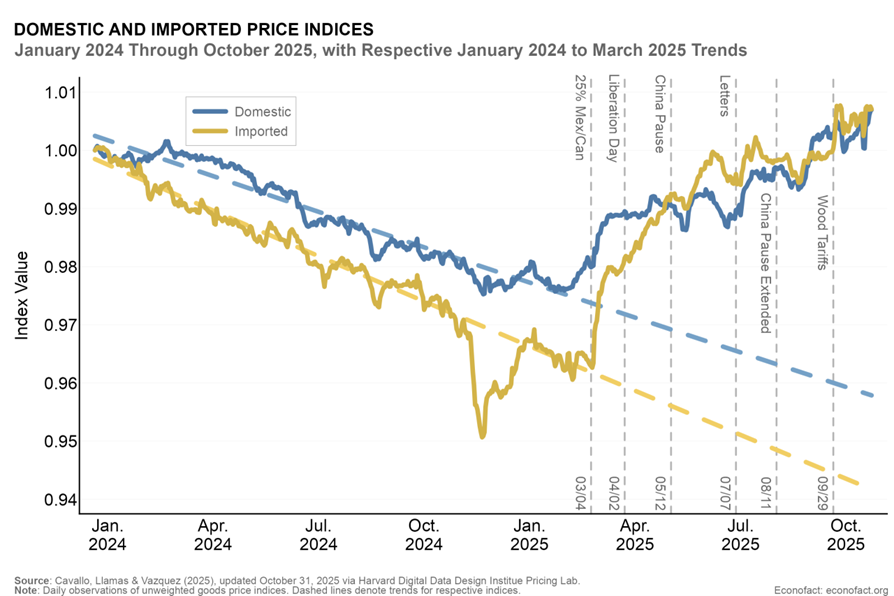

The simplest question in a world where 40% of the stock market is tech or tech-adjacent is: Will this thing hurt tech earnings or valuations? If the answer is no: ramble on. In 2022, the market thought the answer was: Yes, Fed hikes will torch long-duration assets. But that was not the case. Same deal in 2025 with the tariffs. Manufacturing is a tiny part of the U.S. economy and American consumers were able to pay the new tax. Even as tariffs created a new wave of inflation, it came on the heels of a disinflationary period so it all kind of cancelled out.

https://econofact.org/are-tariffs-raising-u-s-retail-prices

While there have been zero new jobs created in the U.S. since Liberation Day and inflation is a problem again, the world just keeps on moving forward. It’s weird. It’s almost like nothing matters.

So I suppose we have to keep two thoughts in our heads at all times:

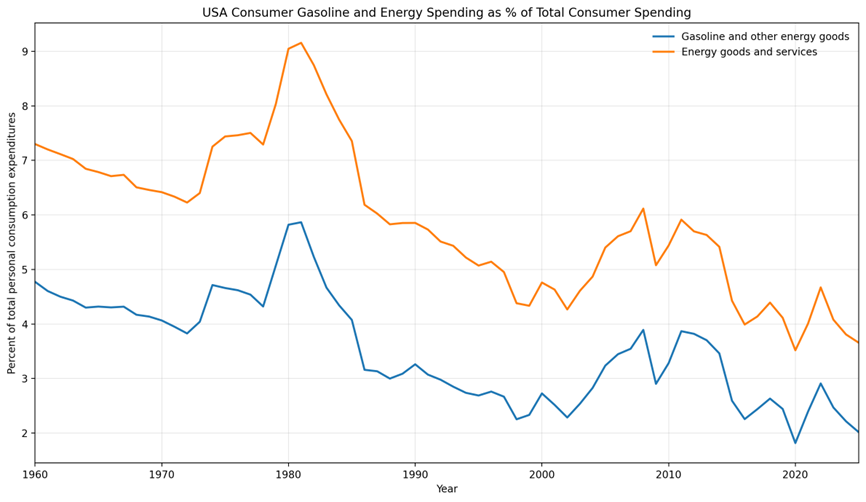

The annoying thing about these one-off policy shocks is that it takes about a year to see the true impact in the economic data. So now we spend the next 6-12 months trying to parse out how much of this oil shock is inflationary, and how much it is deflationary via growth and spending channels.

Energy as a proportion of consumer spending has been falling for years, so it’s not 100% certain that an energy shock today is anything like an energy shock 25 or 50 years ago.

I was bearish stocks and bullish USD for most of March because the market was weirdly complacent and there was zero visibility on the end of the war. Into March month end, I covered both and for now I am not really feeling too strongly about stocks either way. If I was forced, I would be long equities. This all just feels so ridiculously familiar, as I mentioned earlier on. If you look at the S&P 500 and its moving averages, the setup around Ultimatum Day looks similar to the one around Liberation Day.

The charts that follow show the S&P 500 and the 200-day MA. In the last four exogenous shocks, the S&P crapped out, and then once it regained the 200-day, it never looked back.

This is unlike the slower and more organic selloff in 2022 as the Fed gradually raised interest rates over the course of 18 months or so. I am very, very slightly lying, because in 2019 the S&P 500 did zippity dip below the 200-day very briefly, but you get the gist. Bottoms tend to be V-shaped and there’s not a lot of retesting these days.

There is no rule that says this time things need to be the same. In 2015 we had a double dipper where the S&P recovered above the 200-day then plunged to new lows before recovering again. But given the script of the 2018 and 2025 movies are basically identical to this one, why not expect the same outcome in stocks? At least as a baseline.

I acknowledge that there is plenty to worry about. Private credit, zero job growth, rising inflation, and all that. There’s always plenty to worry about. Let’s see what happens.

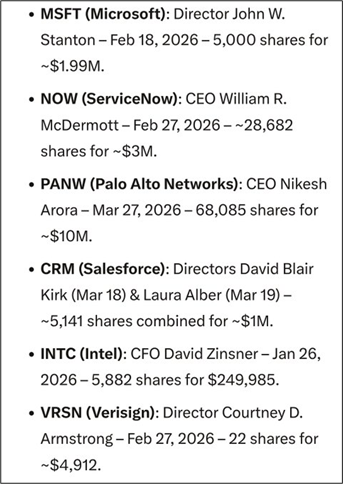

Insiders are buying software stocks.

https://x.com/jaykaeppel/status/2042286993581682816

Nice symmetrical round trip in Mr. Softee. Yes, that was the actual nickname for Microsoft stock in the 1990s. We were a more earnest and happy populace back then.

Here is this week’s 14-word stock market summary:

We did the big rinse. Rates, FX, and equities have been cleansed. Let’s see.

https://www.spectramarkets.com/subscribe/

Disastrous March returns at some hedge funds were mostly the result of bad bets in interest rates and while that may have pushed things a tad beyond reasonable, I am not a believer in the “too much is priced in” story. Inflation is going to be significantly higher with oil in shorter supply and labor markets in many countries are not nearly slacky enough to justify accommodative monetary policy in the face of an inflation shock. Sure, higher oil is bad for consumption and potentially disinflationary, but that’s not guaranteed.

People like to make fun of the ECB for hiking in 2008 and 2011 but ultimately in the face of an oil shock, you have to make a decision. It could be right or wrong in hindsight, but you don’t have a time machine. If you don’t hike, oil might keep running and inflationary expectations could spiral out of control. If you hike, you crush demand, and oil prices will eventually drop in response. Sure, they can’t print oil, smart ass, but they can sure as heck dampen demand for it. :]

It is common for humans to wonder about market pricing during times of stress. The flawed framework that newer traders or non-STIRT traders apply to central bank pricing is to think it’s the modal or median forecast of what people actually think the central bank is going to do. Like a survey. It’s not. There are many ways that market pricing is different from a survey:

Expectations for the Fed are still leaning towards cuts while the market absolutely does not believe the market pricing on ECB or BoE. It feels logical to want to fade the pricing, but it’s an easy view to hold intellectually and a hard one to risk manage in real life. If oil goes up $50 from here, you need to absorb some hefty mark-to-market losses, and even if it doesn’t—if oil hangs around here and headline inflation is 3.5% in Europe, the ECB could easily hike twice. All this to say: I don’t think interest rate markets are off base here. They seem to be pricing logical modal outcomes.

It’s quite amazing to think back to a time when Trump was screaming for interest rate cuts, people thought the Fed was about to be captured, and three more cuts were priced for 2026. Forecasting is hard.

The basic gist is that going into the start of the war, the market was max short USD. This created a problem when the war started and so everyone covered and the USD ripped higher. Hedgers also piled on, using EURUSD shorts (for example) as a hedge for DAX longs or TT shorts or whatever. Then, two Mondays ago, our positioning report showed the market finally reached max long USD. The max long or short USD reading only triggers a few times per year, so it was notable.

The war chugged on, but the USD wouldn’t rally anymore because all the buyers were done buying. This coincided perfectly with month-end, a most pivotal and high-volume day in FX markets.

AUDUSD shows the whole story perfectly. The low in AUDUSD was, not coincidentally, at exactly 11 a.m. NY time on the last day of the month. Real money benchmarks against the 11 a.m. fix and that is the highest-volume 5-minute period of the entire month.

The war continued into April, but there were no USD buyers left. So the USD consolidated until ====> Ceasefire and massive hedge removal.

And here we are.

The dollar is not a safe haven and it’s not a risky asset—its response to a major risk aversion episode is almost fully and completely dictated by positioning beforehand. For example, in 2008 the market was massively short dollars for the carry trade and liability issuance and so the dollar rallied in that crisis. In 2025 the market was massively long dollars into Liberation Day so when that policy shock hit, the dollar sold off.

This time, going into the war, the market was mega short dollars again on the debasement trade and Fed capture and big deficits and all that. So when the bombs hit and risk aversion spiked, the USD rallied. You can develop all sorts of dope cross-border capital flow models, but in the end, the simple and easy and accurate way to forecast the dollar’s reaction to risk aversion is to simply know positioning going in.

I ventured into the muddy altcoin waters this week, but sadly I came up with a neutral view. I will share it in case anyone is interested. If you agree or disagree, please email me; I am eager to learn.

Here’s the excerpt from am/FX earlier in the week:

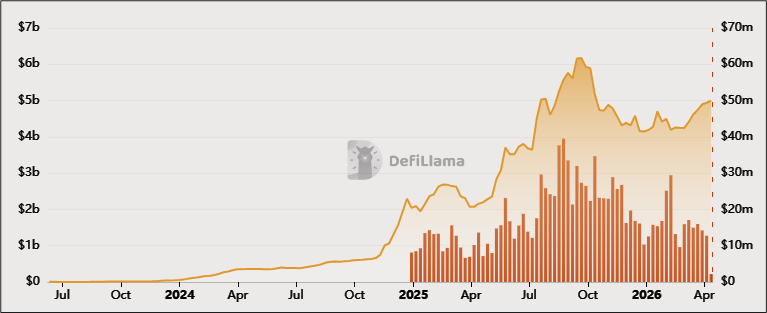

Thank you to everyone who sent me their thoughts on HYPE and PURR. I decided not to do the trade, mostly because despite all the coverage, the revenue story isn’t that impressive so far. In fact, HYPE TVL and fees peaked in the summer of 2025. I found that surprising given the amount of excitement around it.

https://defillama.com/protocol/hyperliquid?groupBy=weekly

The idea behind HYPE is compelling. But there is also a ton of supply ready to be unleashed each time it rallies. And while it has become the go-to for weekend prices of crude oil and equity futures, that is not yet translating to rising fees. The fees appear to me to be the key reason to be bullish because the way it works is that roughly 97% of all core trading fees are utilized in a “burn flywheel,” where the system automatically buys back HYPE tokens and permanently burns them. The model is cool, but as a noob, there is zero chance I am early. And every time it rallies, it gets smacked back down by insider selling.

It’s too hard to figure out whether the model (bullish) or the large future supply (bearish) will win out. Seems like the alpha comes more from buying low on panics and selling high before the next wave of insiders slam it back down. Too hard.

Iron condors in PURR (the HYPE DAT) … Selling $3/$4 put spread vs. selling $6/$7 call spread might actually be the play. The options market is extremely thin but you can do stuff like this if you’re patient and you know what you’re doing.

All this said, next time I am bullish crypto, I will buy HYPE or PURR simply because HYPE appears to be a token that has a believable narrative. If we get a crypto bull run, I would guess it’s a good horse to ride.

Not much else to report on crypto. Bitcoin and ETH have become super low beta risky assets and the fun-lovers have all moved to AI, then silver, and now oil. Here’s a good article on quantum risk from the Director of the Digital Currency Initiative at MIT. Thanks CR for the link!

https://nehanarula.org/2026/04/03/bitcoin-and-quantum-computing.html

Commodities are front and center again this week as the Strait of Hormuz remains under Iranian control and appears to be turning into a toll canal instead of the free-flowing international transport throughway it was before Iran was attacked. You can find analysis telling you this closure will soon result in end of the world type supply shocks, and you can find analysts who tell you it’s fine. The oil will come from somewhere and we will figure it out because that’s what markets do. There could be a world-threatening food shortage around the corner or there might just be a temporary and not super important rise in fertilizer prices.

It’s either like COVID, or nothing like COVID, or neither.

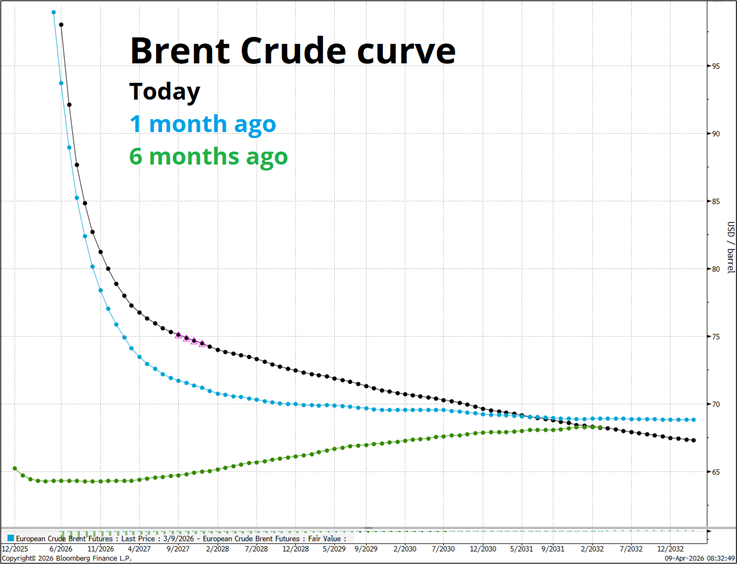

The Brent crude curve looks like this:

You can see that the curve was pretty flat six months ago (green) $65/$70 and now it’s super backwardated (inverted) more like $70/$80 depending on where you look. Yes, it’s higher, but certainly not catastrophic if things were to normalize around there. Then again, some people are paying $150 for barrels in various locales simply because they cannot find enough actual molecules of oil for the real-world things they need to do.

So there is some part of the market that kind of doesn’t believe the futures markets and thinks that oil is mispriced due to physical shortages. I dunno, let’s see.

Gold is a risky asset these days. That makes it much less useful in a portfolio right now. It might become a safe haven again, though, of course. But for now, it’s not.

You can see that S&Ps and gold diverged for a couple of hours at the start of the war, but then have been tangoing like Al Pacino and Gabrielle Anwar in Scent of a Woman ever since. Since the start of the war, S&Ps have outperformed gold, which is a testament to how overowned gold has become with r/wallstreetbets becoming enamored and a multi-year bull market attracting all the specs. Gold and silver are surely less crowded now and will probably work well again once the dust settles post-WW3.

That’s it for this week.

Get rich or have fun trying.

A singer with x-factor

At the risk of damaging my credibility with people who mostly like the same music as me (house, EDM, metal, speedy stuff, etc.) … Someone sent me this clip of a guy from American Idol and I am hooked. Unusual pitch-perfect voice with a bit of the Post Malone tremolo and I don’t know what else exactly.

I can’t quite put my finger on what it is, but I find there is something special and moving about his voice. In the link below, he sings a cheesy mid-tempo electropop song from 2010—but hey, I have no bias against something just because it went mainstream.

The song (Dancing On My Own, by Robyn) was good then and this guy does an excellent rendition of it. I have to show you a picture of him because his voice doesn’t match what he looks like at all, which is weird. And dude works in an assisted living facility for dementia patients in Maryland. Easy guy to root for!

The song captures the pain of young unrequited love. Yes, trading stocks and currencies and changing jobs and getting married and having kids and facing down your demons—these are all high stakes endeavors. But nothing you ever do in life will ever be as high stakes as asking that one girl to slow dance with you in high school. Dry ice fills the dark air, the song begins. Sweat condenses and trickles down the high school gym walls. Hearts go thud, boom, thud, boom.

Whether she says yes or no, you know: your whole life is about to change.

:]

Brooks: Dancing on My Own on Spotify

*************

*************

Something feels off about this headline.

*************

Baseball Insanity One of the craziest things I’ve seen in baseball—and I been watching for decades. Final score 1-0 is the chef’s kiss.

*************

*************

The AI imagines a Mad Magazine comic about U.S. policy shocks

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.