As MAG7 eats the world, the real economy becomes a rounding error

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

As MAG7 eats the world, the real economy becomes a rounding error

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

For your weekend listening pleasure, here is the latest podcast with Alf.

https://www.spectramarkets.com/library/podcasts/

This week was a bit of a nothingburger in macro even as stocks recaptured nearly all their losses from last week and the president did some more central planning. The president implored a large public company to fire its CEO and installed a current government employee into the Federal Reserve, but the market and the world just shrugs this stuff off because it’s all part of the new normal.

The economic calendar was sparse, with the only real highlight being a rare, tied vote at the Bank of England. Four voters wanted no cut, four wanted to cut 25bps and one wanted to cut 50bps. They settled on a cut of 25bps. The market was short GBP for the meeting, and so we saw a pretty zesty dump in EURGBP, but overall, the reaction was not all that exciting.

The situation in the UK is similar to the one in the USA and Canada: Demand for labor is falling, supply of labor is shrinking, wages are firm, and the consumer is stretched but not dead. Sticky inflation and slowing jobs demand makes for a tricky cocktail for central bankers. They want to assume that the inflation is definitely definitely transitory this time, but they also don’t want to be wrong.

Economists tend to focus on the demand side of the economy because that has mostly been the only side that mattered for the past 30 years, but in 2021/2022 we saw that ignoring the supply side can be problematic. We got some low headline NFPs in those days but coupled with a low unemployment rate as the supply of labor was super tight. We might start to see the same thing as immigration crackdowns in the US and Canada start to bite. Less demand and less supply of labor is not deflationary. There is no labor market slack and thus inflation is more likely to annoy than comply with central bankers’ wishes.

I could see a Q4 where stagflation becomes a major concern as growth falls but inflation does not. Inflation usually responds to changes in growth with a lag, and tariffs will distort the CPI data upward for the rest of 2025.

Stephen Miran has been named to replace Kugler at the Fed, and while this could have been an exciting piece of news in other multiverse timelines, the market kind of shrugged it off in this one. Punters sold dollars on the news, but the USD was back to unchanged within a few hours. Miran could easily vote for 50bps at the September meeting if he is confirmed by then but maybe the final verdict is that the Fed’s institutional credibility is intact for now as there are still enough orthodox voices to quell the more rabid rate cut rebels.

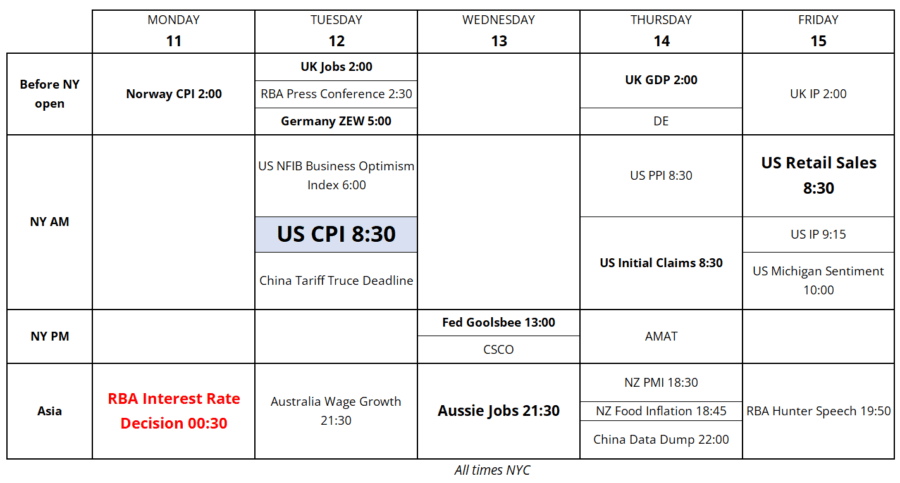

Next week’s CPI data will be the highlight of the calendar next week:

Click on the ad to subscribe. If you’re not happy, just email me and I’ll refund you. Risk free. Unlimited upside.

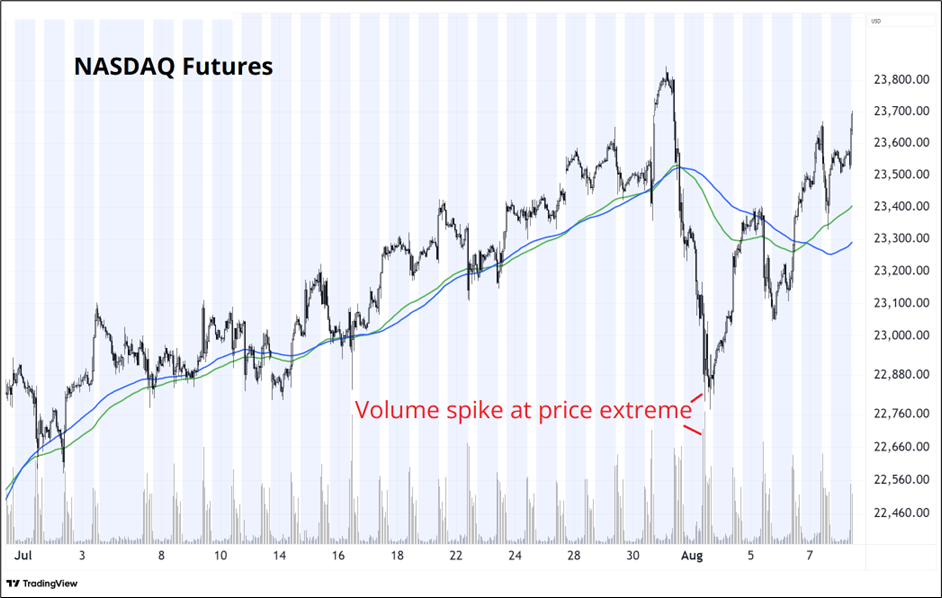

Last week’s fear trade feels like months ago as the rejection in QQQ after META and MSFT beat has mostly been reversed. We had a huge volume spike at the lows and then one quick subsequent new low and now the bulls are back for more.

The entire economy and stock market is now a function of AI Capex and animal spirits at this point, and the weakening consumer and labor demand stories thus only hold water for a day or two at a time. The real bear trade will not begin until a conference call from MAG7 where one of the CEOs says something to the effect of: “OK, we’ve done enough AI Capex for now.” Then, it’s lights out. Until then, as Chuck Prince says: Keep on dancing.

Palantir continues to make me look stupid as it’s now trading > 100X sales. Sure, their earnings were solid. But it’s unusual for a stock to trade above 40X sales—even a hypergrowth company. PLTR currently trades at 126X sales and rising. What was once the most overvalued megacap ever is now the moster mostest overvalued megacap ever.

It matters when it matters.

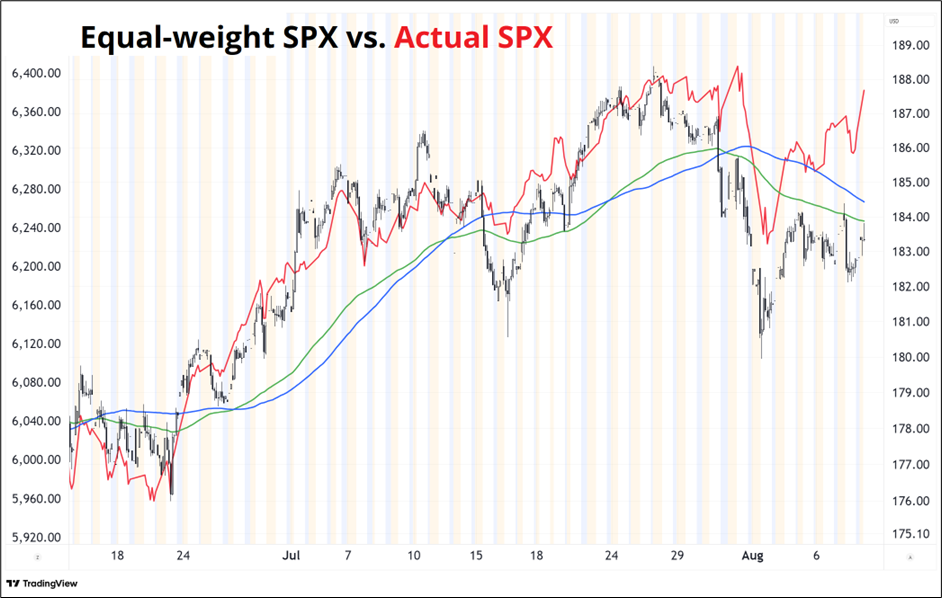

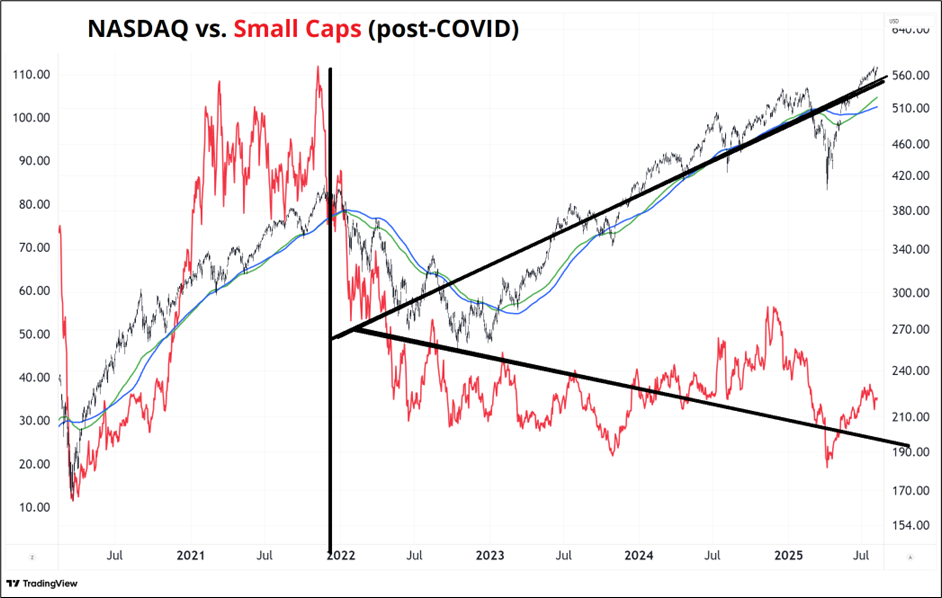

The mega earnings from megatech and the administration’s choice to exempt the largest US businesses from tariff pain has driven a wedge between equal weight and regular weight SPX as you can see here.

The k-shaped economy has been chugging along for five-plus years now and the stock market is quite k-shaped too.

It’s not clear what might bring megacorps back to Earth. They make all the money and they have all the government access. What else would you want to invest in, I suppose?

Here is this week’s 14-word stock market summary:

Last week’s market swoon was soon a boon, creating BTFD bargoons.

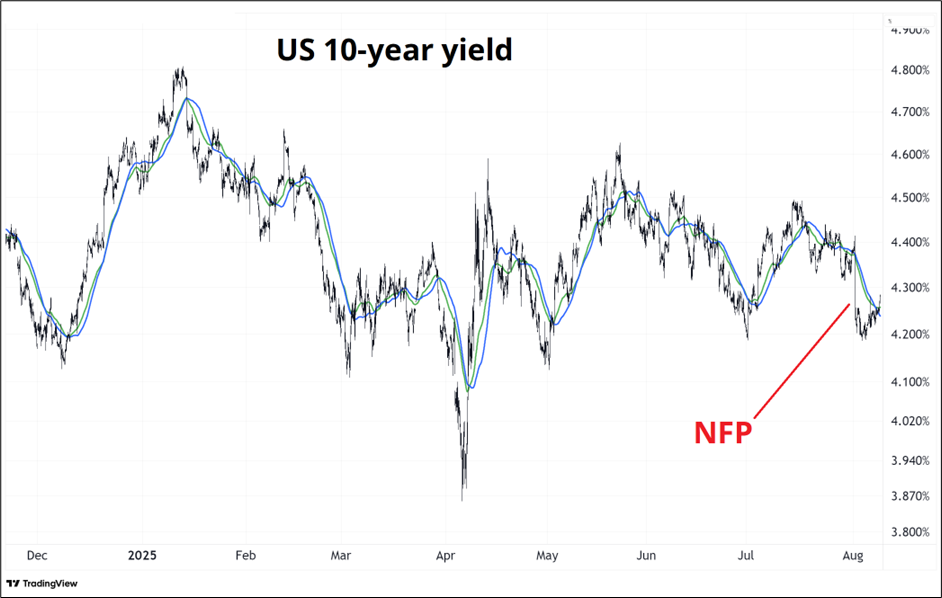

Yields flashed lower on NFP last week, then spent all this week grinding back up. This continues the rangebound theme in yields as a succession of sexytime narratives cannot unlock anything outside 4.10%/4.60% in 10s.

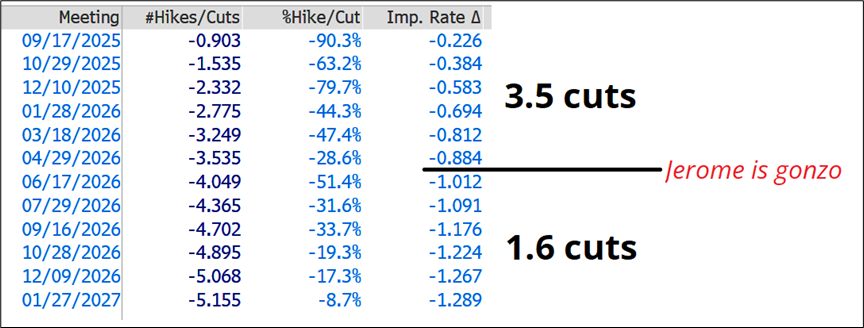

The Fed is pretty much fully priced for September again, and even as we fret over the coming annihilation of Fed independence, most of the cuts are priced for before Powell leaves, not after.

My feeling has always been and continues to be that Fed cuts are 90% conditional on economic data and the state of the economy and 10% conditional on who is the Fed Chair. Maybe 75/25 at the most. If CPI is running at 3% and the Unemployment Rate is 4.1% in Q4 2025/Q1 2026… You really think they’ll cut 3.5 times? I doubt it.

I wrote a piece today about how EURUSD is very hard to map against any variables that used to drive it in the past. Rate differentials, relative equity prices, terms of trade, gold, and bitcoin all do a fairly bad job of explaining EURUSD recently. Even shorter term news like Miran going to the Fed hasn’t had much zip. Sometimes flat is the right position.

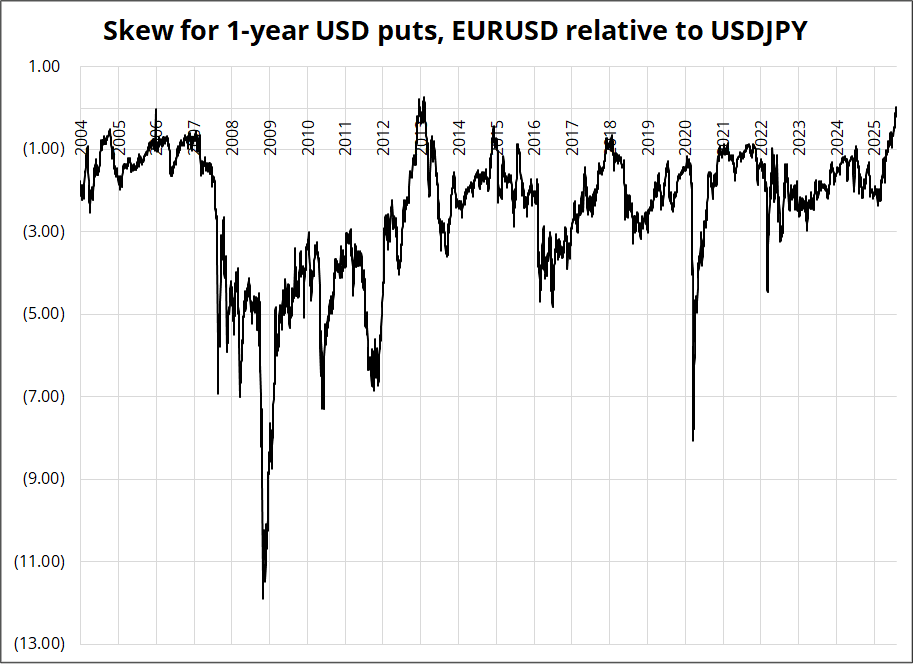

Tim Power pointed out that something unusual is happening in the vol market as the market appears to be viewing the EUR as relatively more of a safe haven than JPY vs. history. Here’s the chart:

This probably reflects:

The rip in 2013 was the result of Draghi’s “Whatever It Takes” speech and was probably more about unwinding “THE END OF THE EURO” trades than it was about strong EU credibility. This time, the change could be more structural. This has implications for portfolio hedging (EUR/XXX better hedge for SPX weakness than XXX/JPY, etc.) and it’s also relevant to correlation traders. If you think the VIX is going higher, you might be better off long EURAUD than short AUDJPY, for example.

Some of this will depend on why VIX rises (if it does). If it’s because of stagflation or higher bond yields, EUR will almost certainly be best. If it’s because of a US recession, JPY could still outperform and the options market will mean revert aggressively back towards more historical norms.

On this week’s podcast, Alf asked me if maybe it’s a fade because it’s at such an extreme. In other words “Is this time really different?” My bias is always to fade, but I think this is a true regime shift. The euro is a better store of value and safe haven than the JPY and I think that will continue. Options market pricing is reflecting a regime change, not a speculative fervor.

Bitcoin has been in a zag pattern as the Crypto Week highs hold and BTC is pinned in a 112/120 kind of range. There have been big moves elsewhere with a ripper in ETH and XRP, for example. I still can’t shake the idea that most of the ETH buying lately is corporate treasury stuff that will burn itself out fairly soon, but the bull case for ETH as expressed in a recent email from Bankless is somewhat convincing, so I am keeping an open mind.

Here’s what they said:

—

excerpt

Yesterday, the new SEC Chair Paul Atkins gave a speech that delivered what was probably the single most bullish statement made by a U.S. regulator. The tl;dr? The SEC wants to move America’s financial markets onchain. In his announcement, Atkins specifically points to five things he wants the SEC to do for the crypto industry, in order to pursue that end:

Each one of these topics could warrant an entire discussion by themselves, and frankly more clarity here would be welcome (Paul Atkins on the podcast soon?).

When you read Atkins’ introduction to this latest statement, he emphasizes the costs when the regulations and technology around markets lags behind modern demands. He discusses how the pre-electronification of financial markets led to a disaster in market confidence because antiquated technology could not keep up with the market.

“In the 1960s…—Wall Street was riding a bull market. But behind the scenes, our market machinery was straining to keep up….Rising stacks of paper stock certificates had to be physically delivered by clerks wheeling carts up and down Wall Street and in other financial districts all across America… The breakdown over an antiquated system was described by the SEC chairman at the time as ‘the most prolonged and severe crisis in the securities industry in 40 years…’”

Why is Chair Atkins including this historical anecdote? In my opinion, it’s because he wants to emphasize the importance of proactively, rather than reactively, getting America’s financial markets upgraded into the blockchain technology era.

Paul later adds explicitly:

“To achieve President Trump’s vision of making America the crypto capital of the world, the SEC must holistically consider the potential benefits and risks of moving our markets from an off-chain environment to an on-chain one.”

Paul Atkins wants to put America’s Financial Markets onchain.

But which chain??

Paul and the SEC have no bias toward particular chains in the statement. From the perspective of the SEC, which chain benefits from America’s financial markets moving onchain is up to the market.

So, what does the market want?

I’ll make a few claims here:

Mike from Blockworks broadly agrees:

Yes, tokenized assets can go on any chain. Do centralized issuers need Ethereum’s level of WWIII-resistant blockspace? Perhaps not? Does Ethereum’s 10 years of uptime matter when asset ownership is actually determined by offchain processes?

Anatoly, the founder of Solana, says security doesn’t matter. I think that’s midcurving it.

Ethereum’s brand of security and decentralization is huge, and in Wall Street, brand matters.

Blockchains like Solana or Avalanche, both of which have had multiple hours of downtime in the last 1.5 years, today still look far too much like corpo-chains than decentralized ecosystems.

Yes, I am certain that some RWAs and other Wall Street action will find itself on juiced Alt-L1s like Solana or Avalanche. But the bulk of America’s financial markets will find themselves on the one chain that doesn’t have a counter-party.

Ethereum.

end of excerpt

The big story was news late last night that the US will tariff gold. This is crazy news for spot/futures basis, potentially, but the price of gold itself didn’t move much net/net. I am surprised by this, especially as it came on the heels of the Miran announcement and a moonshot in most other liquidity sponges. I bought gold on the news and sold it at the same price 24 hours later. Hmm.

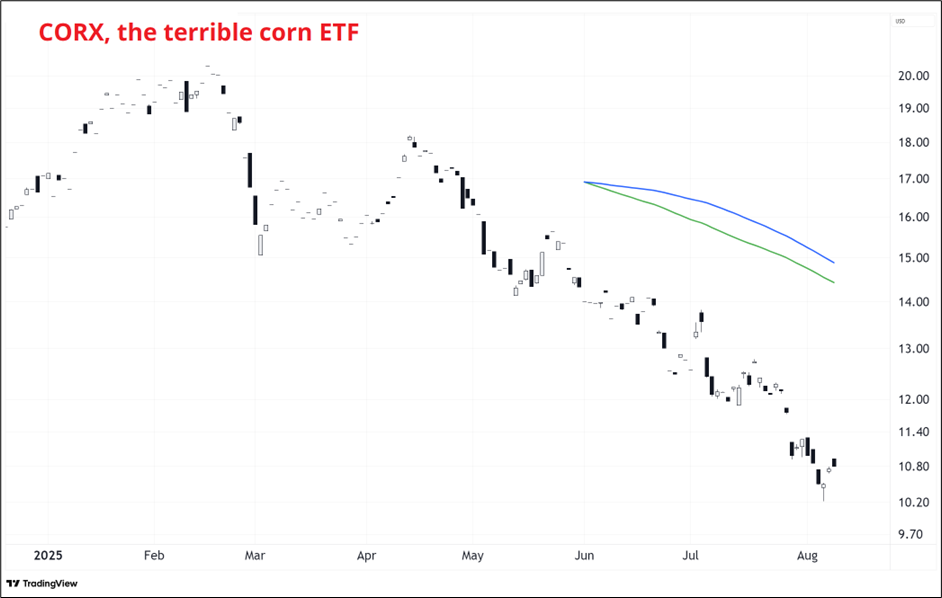

There is a service called DSI that has been around since 1987 and they do a daily survey of retail futures traders to check on sentiment. The resulting data runs from 0 to 100 and numbers below 10 or above 90 are super uncommon. The DSI for corn this week was 8. I don’t trade corn, but I did have a peek at the CORX (double corn futures ETF). It’s a hideous ETF as liquidity is gossamer thing and the fee is 198bps, but since I can only trade listed products, I figured why not take a shot. Risking 1 to make 2.8.

Gotta love those moving averages when you don’t have enough data to build them properly. I could have taken them out but for some reason they seem funny to me.

That’s it for this week.

Get rich or have fun trying.

https://nealstephenson.substack.com/p/emerson-ai-and-the-force

*************

In honor of the k-shaped stock market: A song about K

Timo Maas and Placebo … yes guy! … one of the top 50 songs of all time.

Gravity: Don’t forsake me.

*************

*************

Gucci Gang by Joyner Lucas, an old favorite of mine.

*************

Interesting article here:

https://www.quantamagazine.org/at-17-hannah-cairo-solved-a-major-math-mystery-20250801/

Includes some solid quotes, including:

“Growing up, I didn’t really know if I was talented,” she said. “I like to play piano, and people around me would tell me that I was really talented at math and at piano. And in retrospect, now that I look at it, I can see, sure, my piano was above average. But it was by no means exceptional. While on the other hand, it looks like mathematically I’m, like, whatever.”

“I didn’t have many social experiences, so I still had to learn how to interact with other humans,” she said.

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.