There’s no NFP but we can still talk about it

Pac-Man was released in the United States on this day in 1980.

There’s no NFP but we can still talk about it

Pac-Man was released in the United States on this day in 1980.

Flat

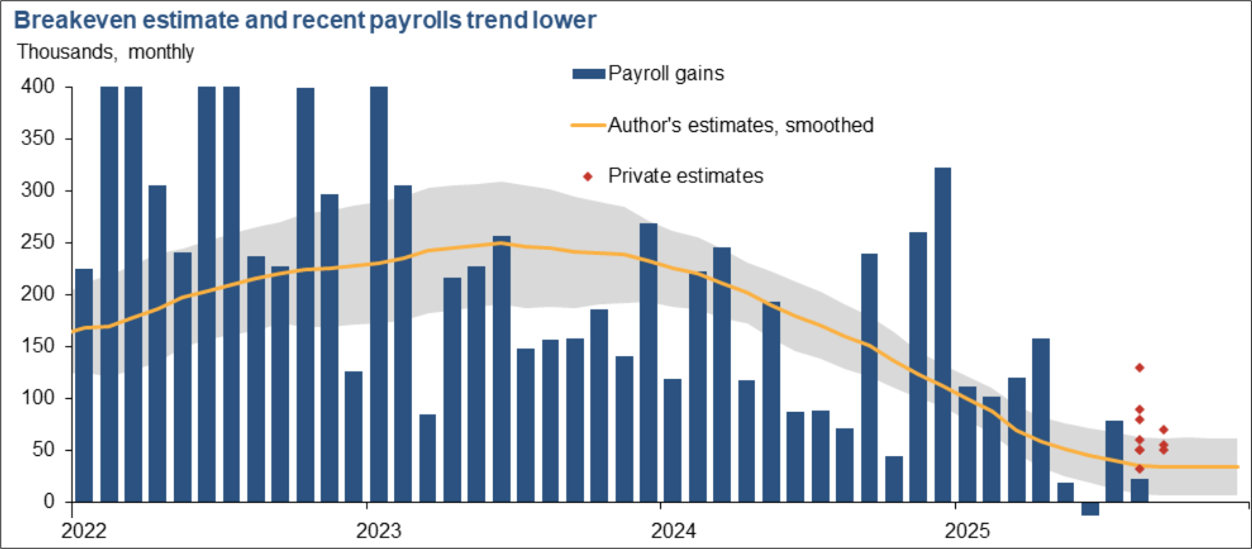

My view is and has been that most of the drop in headline NFP is related to labor supply and falling breakeven rates. That’s why the UR and Claims aren’t moving.

The Dallas Fed wrote a piece yesterday which I naturally agree with because it says the same thing.

:]

Author takeaways:

Conclusions for navigating an economy shaped by demographic volatility:

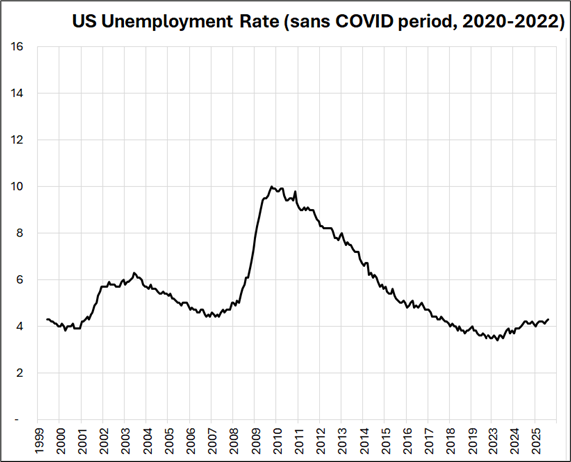

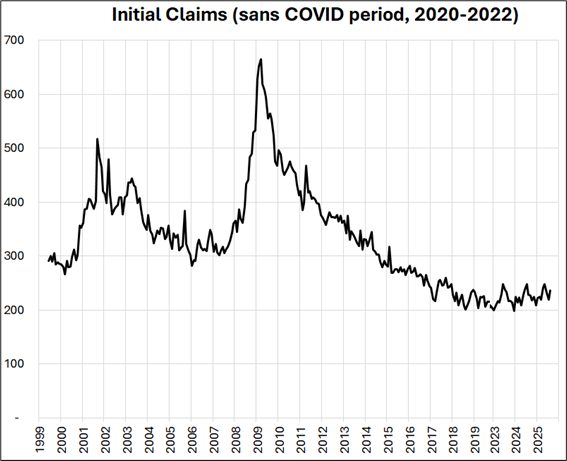

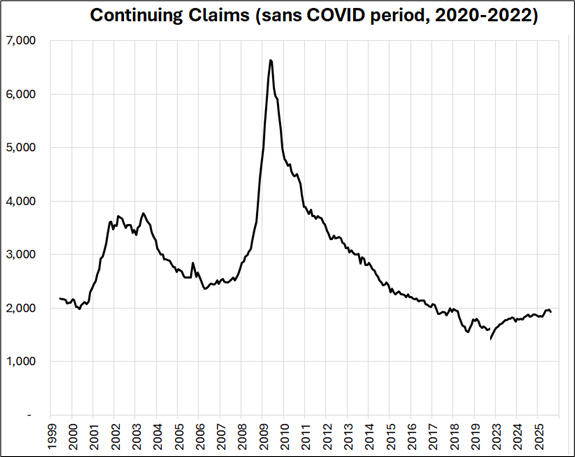

One of the most important and confusing aspects of the current economy is that rates of change in the labor market are all negative while levels are still quite robust. Much as the world got confused and bearish when M2 growth turned negative after it exploded higher then reverted to the mean in 2020/2022, the world is getting bearish as the labor market reverts to the pre-COVID baseline.

As a bit of a thought experiment, I took the major labor market data, ex-NFP and removed the COVID years (2020 to 2022).

The reasoning here is that 2020/2022 was a once-in-a-lifetime overheated labor market and thus any downward momentum off that froth is natural and thus we need to look at today’s labor market in the context of what it looked like before the overheating episode. I did not look at NFP because, as explained by the Dallas Fed, the current period is not comparable to the pre-COVID period as demographics and supply shocks have dropped current breakevens to 30,000 jobs vs. a range of 100,000 to 250,000 beforehand.

Here’s the Unemployment Rate, for example:

And here are Initial and Continuing Claims. Both show a labor market humming along at 2017/2019 levels.

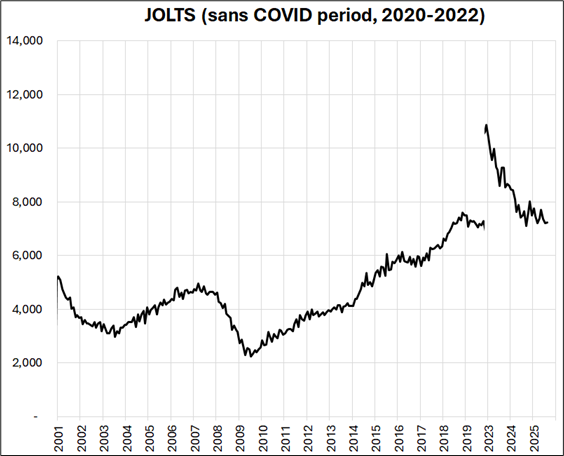

And below: JOLTS. Again, you see we are back to baseline.

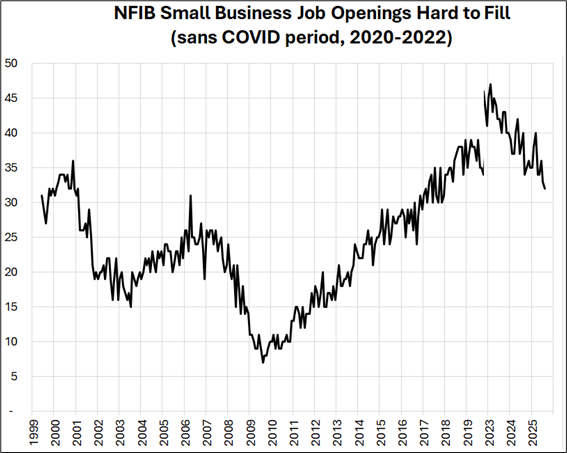

And finally, how hard it is to fill small business job openings.

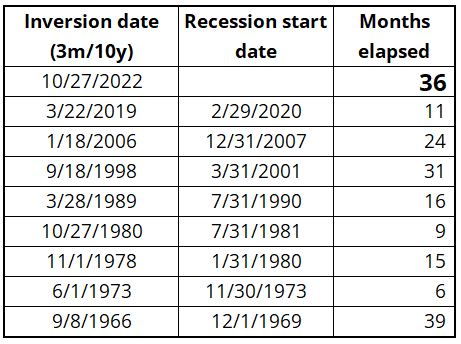

Again, back to 2018/2019 levels. Normally labor market momentum is a good indicator for forward extrapolation; that’s the logic behind the Sahm Rule. But normally an inverted yield curve is a decent predictor of recession, too. That signal tripped in July 2022 (or October 2022, depending on what measure you use) and it’s been useless. I think that when the labor market overshoots into overheating, you will get false signals from measures of momentum because the natural return to baseline looks nefarious, but isn’t.

Watch the Unemployment Rate and Initial Claims going forward, and expect NFP to be in the 0 to 50,000 range as the labor market remains in balance while demographics and immigration crackdowns reduce the supply of workers. UR>4.5%, Claims>280k, or NFP sub-zero are indicators that the job market is troubled. The economy’s reliance on data center spending is the biggest economic and financial stability risk right now, so you can also watch for any regime change in that space that might lead to a full-on countercyclical doom loop. Everything is procyclical right now and one day, everything will be countercyclical. But not yet.

Waiting for Godot Recession

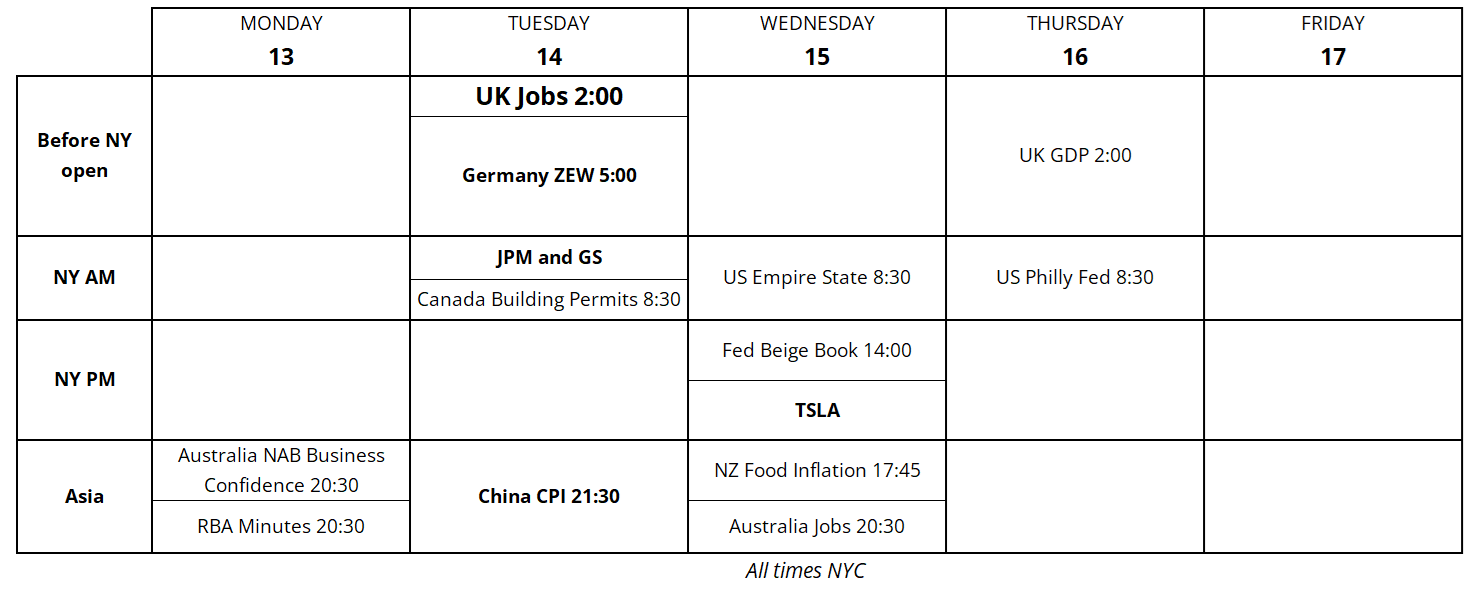

The US data blackout is in full force. Tumbleweeds roll through this week’s calendar as the shutdown deletes CPI, PPI, Retail Sales, and other US data releases off the docket. Hmm.

From Bloomberg:

The Bureau of Labor Statistics has recalled staff to prepare the September consumer price index report, according to a Labor Department official with knowledge of the matter.

The agency was directed by the White House Office of Management and Budget to bring back employees to assemble the report in time for publication by the end of the month, the official said. The OMB did not immediately respond to request for comment.

Silver is blowing up all the technicals as it ripped through the ATH, made a double top at 51.00, then crashed back below 50.00, triggering a false break signal. Then, it ripped all the way back to 51.00, triggering a false break of the false break. Ugly. Now we have a triple top at 51.00 and all the short-term momentum and technical traders are rocking back and forth in the fetal position. Silver options, forwards, and basis are all going bananas.

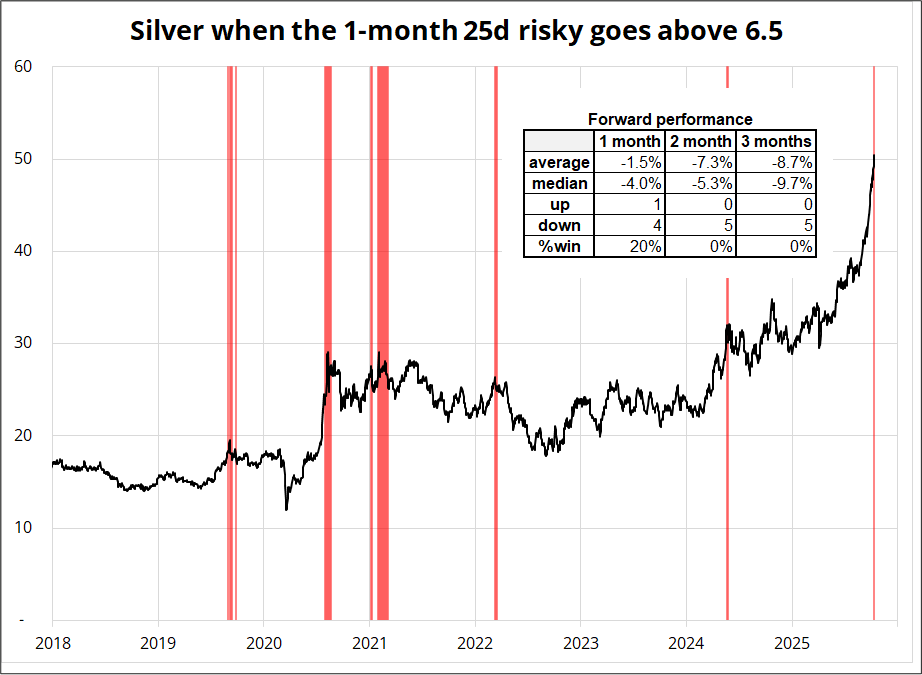

The 1-month, 25-delta risk reversal in silver, for example, has spiked in favor of calls. It’s rare for it to go above 6.5, and it’s currently at 6.9.

The spikes are mean reverting and seem to be an okay signal of topside market panic. The sample of spikes is only five non-overlapping signals since 2018 (the risky was much lower pre-2018), but all five times silver was lower two and three months later. Here are the times it happened, marked in red, and the forward performance.

It’s a bit too off piste for the am/FX sidebar, but selling 3-month 50/51 call spreads in silver makes a lot of sense to me. Essentially betting we are below $50 in three months and benefiting from the skew. Or just buy puts if you’re a degenerate animal.

Smaller, less diverse sample sizes make for weaker estimates. A longer shutdown would impede the agency’s ability to gather enough information to produce individual price indexes that feed into CPI, said Omair Sharif, the president of Inflation Insights. And if lawmakers fail to reach an agreement until late October, that could force BLS to scrap its inflation report for October.

“If we’re up to October 22, October 23? That — to me — is almost a cutoff point where we should start to think [that] we’re probably not going to have an October CPI,” Sharif said.

Homo Heuristicus: Less-is-More Effects in Adaptive Cognition

The paper is only 11 pages, and it’s not boring—you can do it! The gist is that while heuristics can appear irrational because they exclude massive amounts of information from your decision-making, they are often better than more rational analysis because of the less-is-more effect. Here’s an excerpt.

Consider how a baseball outfielder catches a ball. The view of cognition favoring omniscience and omnipotence suggests that complex problems are solved with complex mental algorithms. Richard Dawkins, for example, argues that “He behaves as if he had solved a set of differential equations in predicting the trajectory of the ball. At some subconscious level, something functionally equivalent to the mathematical calculations is going on”. Dawkins carefully inserts “as if” to indicate that he is not quite sure whether brains actually perform these computations. And there is indeed no evidence that brains do.

Instead, experiments have shown that players rely on several heuristics. The gaze heuristic is the simplest one and works if the ball is already high up in the air: Fix your gaze on the ball, start running, and adjust your running speed so that the angle of gaze remains constant. A player who relies on the gaze heuristic can ignore all causal variables necessary to compute the trajectory of the ball–the initial distance, velocity, angle, air resistance, speed and direction of wind, and spin, among others. By paying attention to only one variable, the player will end up where the ball comes down without computing the exact spot. The same heuristic is also used by animal species for catching prey and for intercepting potential mates. In pursuit and predation, bats, birds, and dragonflies maintain a constant optical angle between themselves and their prey, as do dogs when catching a Frisbee.

Monday’s a holiday here. See you Tuesday.

Pac-Man was released in the United States on this day in 1980.

The character’s name comes from paku-paku (パクパク), an onomatopoeic Japanese word for gobbling something up.

The character’s name was written in English as “Puck-Man”, but when Namco localized the game for the United States, they changed it to “Pac-Man”, fearing that vandals would change the P in “Puck” to an F. Good call!