2025 was the year of overreaction to tariffs. Now we might underreact.

Ray Bartkus mural painted upside down to achieve right-side up reflection

2025 was the year of overreaction to tariffs. Now we might underreact.

Ray Bartkus mural painted upside down to achieve right-side up reflection

Take profit on short USDJPY from 159.23.

The EU is in a tough spot as the trade deal they signed last year is worthless and new tariffs could be on their way, or not. After trading tariffs as a bullish USD phenomenon in 2017, 2018, and early 2025, the common knowledge is now that tariffs are bearish USD, but the reality is that nobody has a clue. When those threatened tariffs are a prelude to a threatened US invasion of NATO territory, it’s tricky. Will the EU continue to bend down and pay tribute to the hegemon as the UK first did in 2025, or will there be a regime shift where they feel negotiation with a bad-faith actor is pointless and they invoke the anti-coercion measures?

The tariffs are scheduled to be imposed on February 1, so markets are inclined to underreact for now as there is such a high probability Trump changes his mind or delays the tariffs as this could just be another unserious instance of maximalism without intent. Furthermore, the Supreme Court will rule someday soon on whether this type of coercive tariff is even legal by US standards. The confusion over whether tariffs are good or bad for the USD and the question over whether they are legit or simply a bully on parade explain the minimal market reaction.

While one might think that EURJPY should be 150 points lower on this sort of thing, history has shown us that the actual financial market and economic impact of tariffs has been much less than initially feared. That said, we’re probably at a point where instead of overreacting like we did in April 2025, we are now underreacting.

Speaking of yen. We get the BOJ this week, and there is exactly zero priced in, which makes it mildly interesting. There is potentially tiny scope for a hawkish outcome to protect the yen and JGBs, although I cannot say for sure whether the BOJ thinks that hiking rates is good or bad for the long end. There seems to still be this idea in Japan that a dovish BOJ keeps borrowing costs low, but that is clearly not the case beyond the 2-year point. There is no particular reason to expect anything from the BOJ here, especially with elections coming February 8, but the lack of expectation makes the potential for a move higher than it would be otherwise, if you know what I mean.

I went short USDJPY at 159.23 on rising odds of MOF intervention, but clearly that trade was right for the wrong reasons and there is no real chance of an appearance or rate check by the MOF down here. Therefore, I will take profit here and reassess the situation if we get back above 159.00.

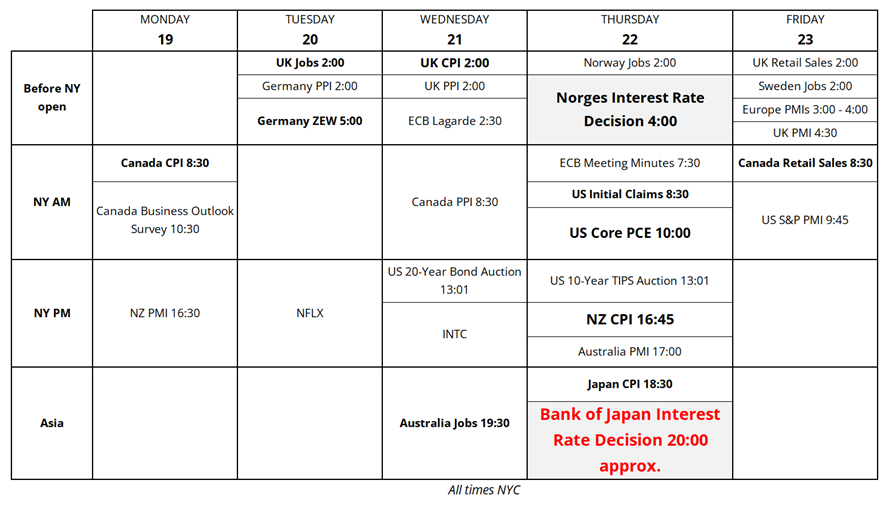

The calendar has some spice this week with various CPI releases, a Bank of Japan meeting, and other data worth monitoring. Note that Core PCE, normally an 8:30 release, comes out at 10:00 a.m. on Thursday. That’s weird.

I had written on Wednesday about how the 98400 level remains the key pivot in bitcoin and the rally peaked at 98000. So that reinforces the double moving average and key pivot zone from February/March 2025, May 2025, June 2025, and October/November 2025. Here’s the updated chart. Bitcoin continues to disappoint as there are many other timelines of the multiverse where the current macro regime would benefit assets with no counterparty risk such as bitcoin. It is holding okay, but not exactly silver or gold style performance here.

A bit of a slap in the face for equities here as the price controls on credit card interest and the escalating beef over Greenland is a reminder that we were priced for perfection last week with every strategist in the world climbing over each other to raise their expectations for 2026 growth in the US and their equity forecast for the SPX this year. This is probably just another zig before a new ATH, but it’s worth considering that the permabears are the only economic bears remaining. The AAII survey shows an extreme reading with Bulls 21 points above the Bears for the first time since late 2024.

And remember the typical pattern after the New Year is that people pile into the most popular trades from mid-December until mid- to late-January and then we see a nasty correction. 19JAN is a tad early for the peak, but close enough. NASDAQ futures have been above the 100-day moving averages since May 2025 and made an aggressive test thereof in late November. They come in around 25,000/25,100 right now. A daily close below 25,000 in NQ will bring out CTA and humanoid selling.

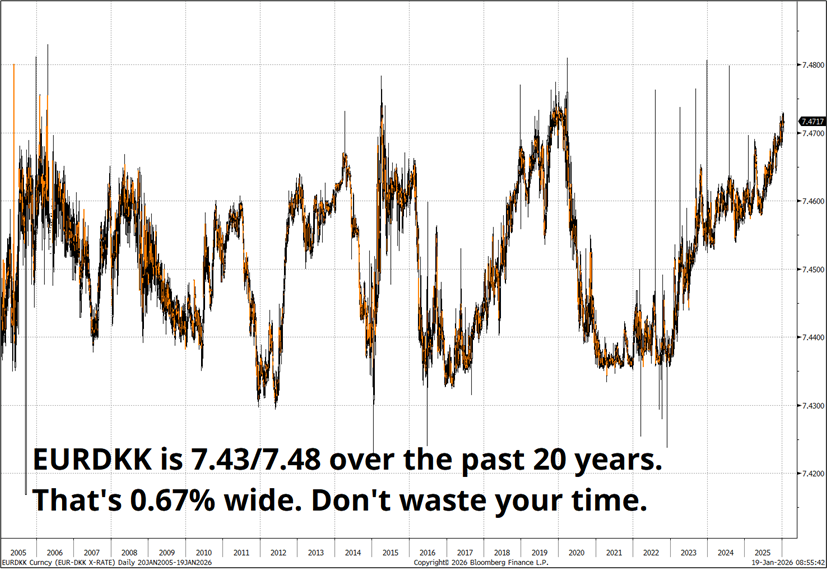

There has been a bit of noise about EURDKK in various circles. The Danish krone is managed via the ERMII mechanism and there is no trade here. Every now and then, speculators get the idea that it might be fun to take on the peg, but it never works because there are simply not enough capital flows to scare the Danish central bank. They are not going to be intimidated and trading EURDKK is a complete waste of time. Even if the US moves airpower and elite forces into Nuuk, a EURDKK peg break isn’t the way to play anything.

I am just back from a 5-day silent retreat at a monastery in NY state. If you are curious what that feels like, check out my side essay tomorrow. It’s not exactly finance-related (!) and some might find it too cringe for this venue, so I will keep it as a separate writeup, outside am/FX, and link to it.

Have a right-side up day.

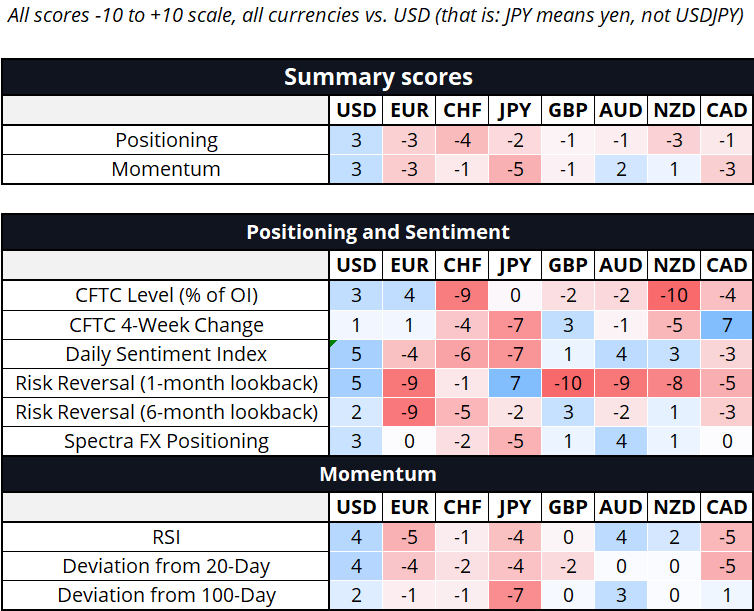

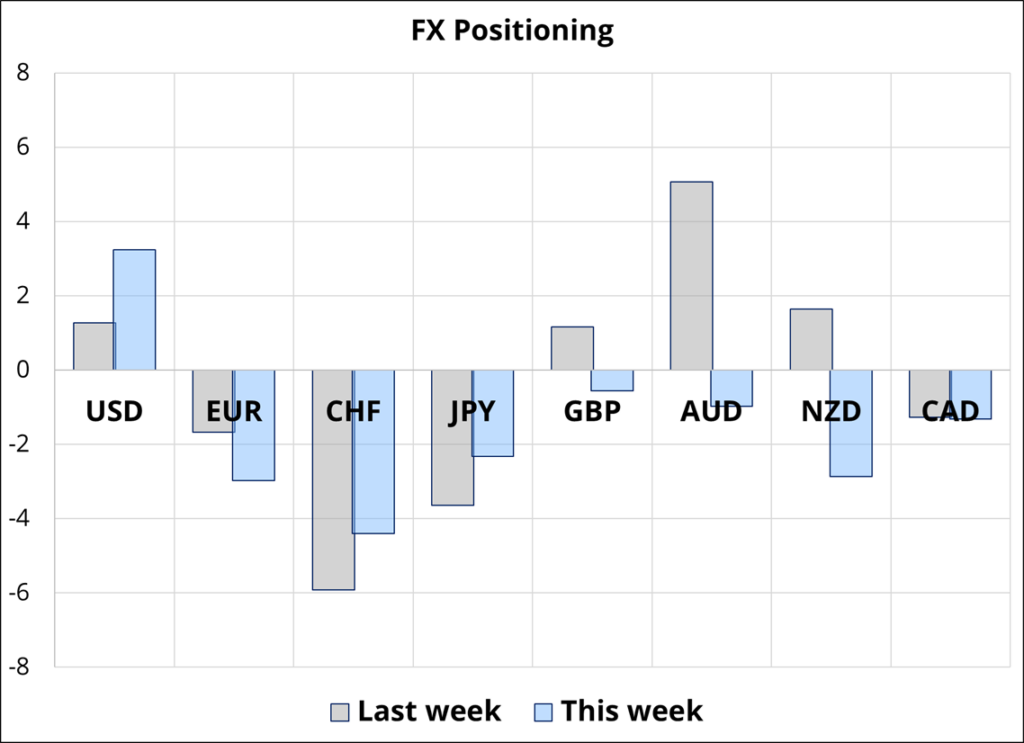

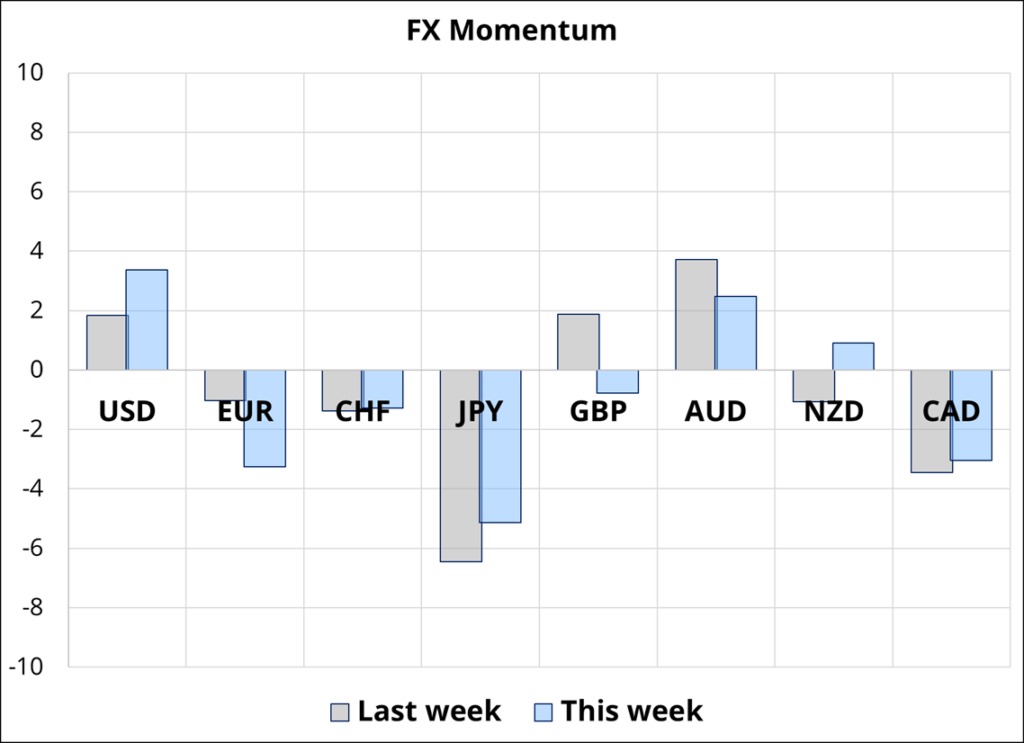

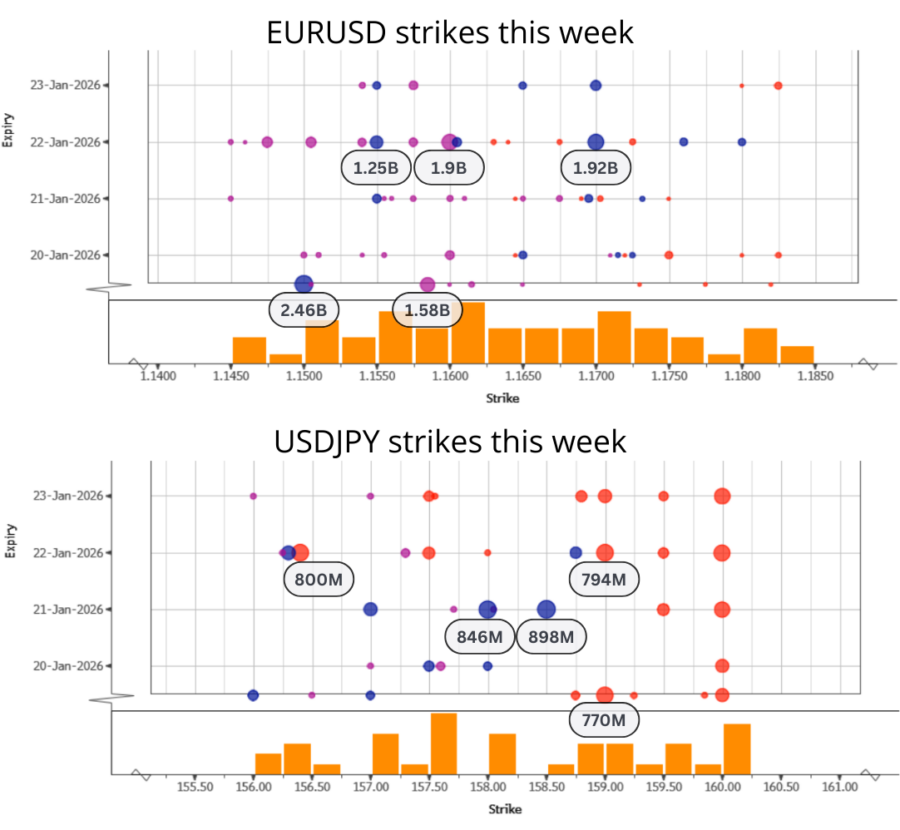

Hi. Welcome to this week’s report. The USD longs are getting bigger again as there is a net short position in every currency right now, even AUD. I am surprised by the AUD reading because almost everyone I talk to is bullish AUD and long in some way, shape, or form. The AUD reading is somewhat skewed by the aggressive move lower in the risk reversal, so maybe we can take that with a grain of salt or deduce that some longs are hedging. Lotta big strikes Thursday.

Ray Bartkus mural painted upside down to achieve right-side up reflection

https://raybartkus.com/street_art.html

HT CnD