The kneejerk on the DOJ news is unlikely to evolve into a lasting theme

A Man Feeding Swans in the Snow

(Marcin Ryczek 2013)

The kneejerk on the DOJ news is unlikely to evolve into a lasting theme

A Man Feeding Swans in the Snow

(Marcin Ryczek 2013)

Flat

I understand why the market feels compelled to sell USD on the DOJ launching an investigation into Jerome Powell (an investigation approved in November 2025), but I highly doubt the story will have lasting relevance. Jerome Powell and Lisa Cook will remain on Trump’s personal vendetta list until they are removed, or their time at the Fed expires naturally. Either way, I don’t think we are learning anything new, and I don’t think the future path of monetary policy will be affected. Sure, it’s another glitch in the old checks and balances but the Overton Window was smashed a long time ago. This is just more of the same and Powell’s a lame duck anyway.

If I were evaluating whether the DOJ news or the credit card fee caps might have a bigger impact on markets, I would bet the latter as Trump’s attempts to outdo Mamdani on price controls should be more alarming for investors than a kick in the pants for Jerome Powell as he is already halfway out the door. Bank stocks like Capital One are getting smoked as policy by fiat leaves Congress, once again, out of the loop. While I support capping credit card interest rates because high interest rates on credit cards mostly subsidize aggressive advertising to low-income households (much as non-stop pharma advertising raises drug costs), caps are still bad for investors.

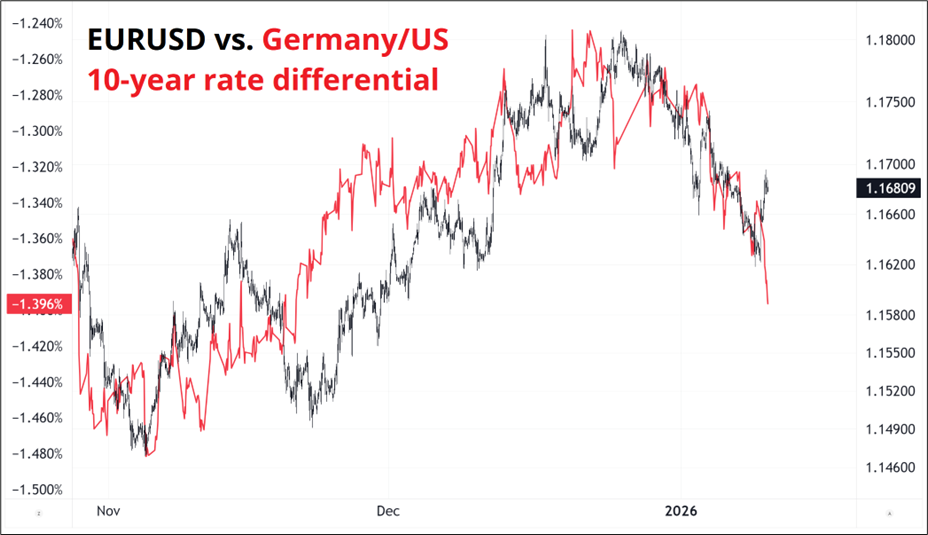

Meanwhile, US yields are back at the top of the range here and that is probably more important than the DOJ investigation or the credit card rate cap—another reason that I think this USD dip is a fade. Finally, if this was a real fear trade over US institutional independence, USDJPY and cross/JPY would be lower, not unch/higher.

I feel that this rally in EURUSD, AUDUSD, etc. is a product of mean reversion from low starting points (those pairs were slammed last week) and these are not rallies worth chasing.

At 16:00 Wall Street time today, we get the New Zealand Quarterly Survey of Business Opinion, a survey that could matter for RBNZ policy. Anna Breman just took over at the RBNZ, so all new data between now and their next meeting (February 18) takes on extra relevance. The RBNZ is priced for a small probability of a hike by the end of 2026, so if the data comes in persistently weak, there is room for the market to reprice back towards cuts.

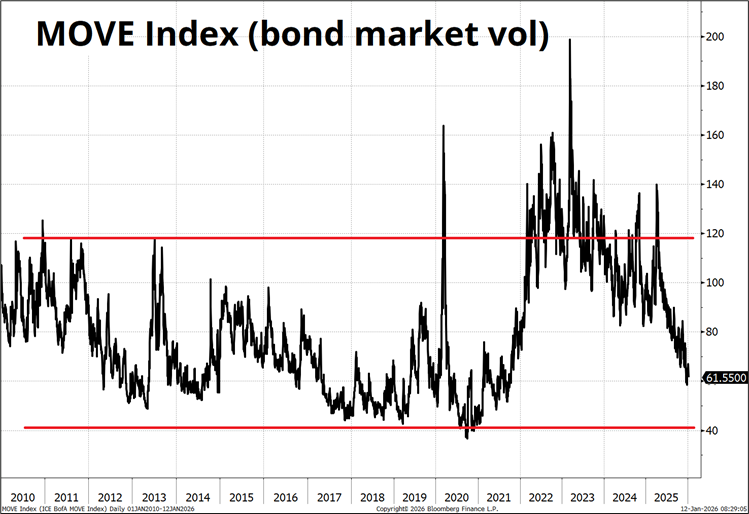

One of the more interesting (or perhaps uninteresting!) features of interest rate markets right now is the lack of movement priced in for central banks in 2026. Two cuts from the Fed, one cut from the Bank of England, zero from the Bank of Canada, ECB, and SNB, and one hike from the RBA is all we’ve got. While this partially explains moribund fixed income volatility, it’s worth noting that we are still above the MOVE Index lows seen in 2017, 2018, 2019, and 2020. The pre-COVID range for MOVE was 40-120 and we are currently plumbing 61.

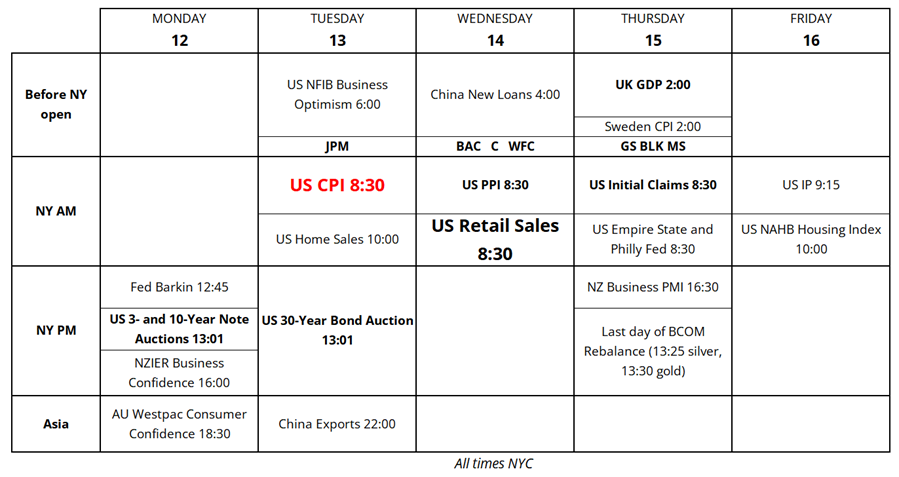

This week’s calendar features two big reports from the US along with a smattering of other data points. Plus the start of US earnings season.

Have a beautifully contrasting day.

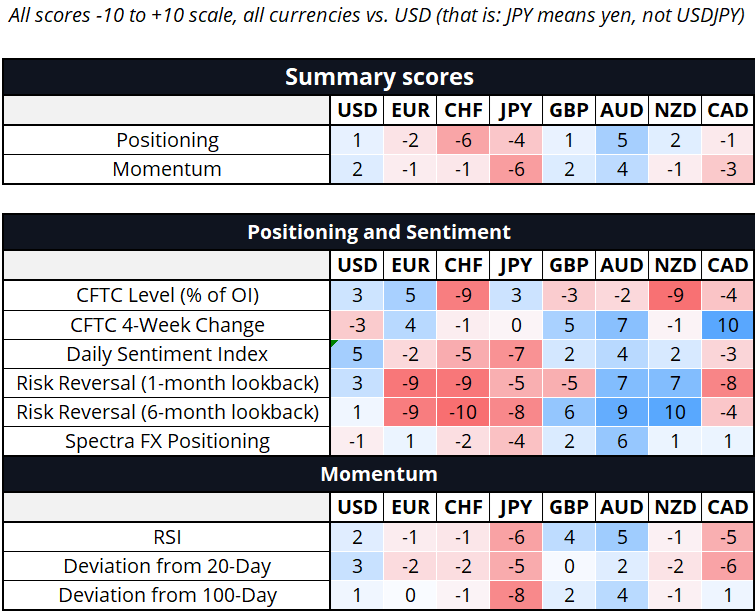

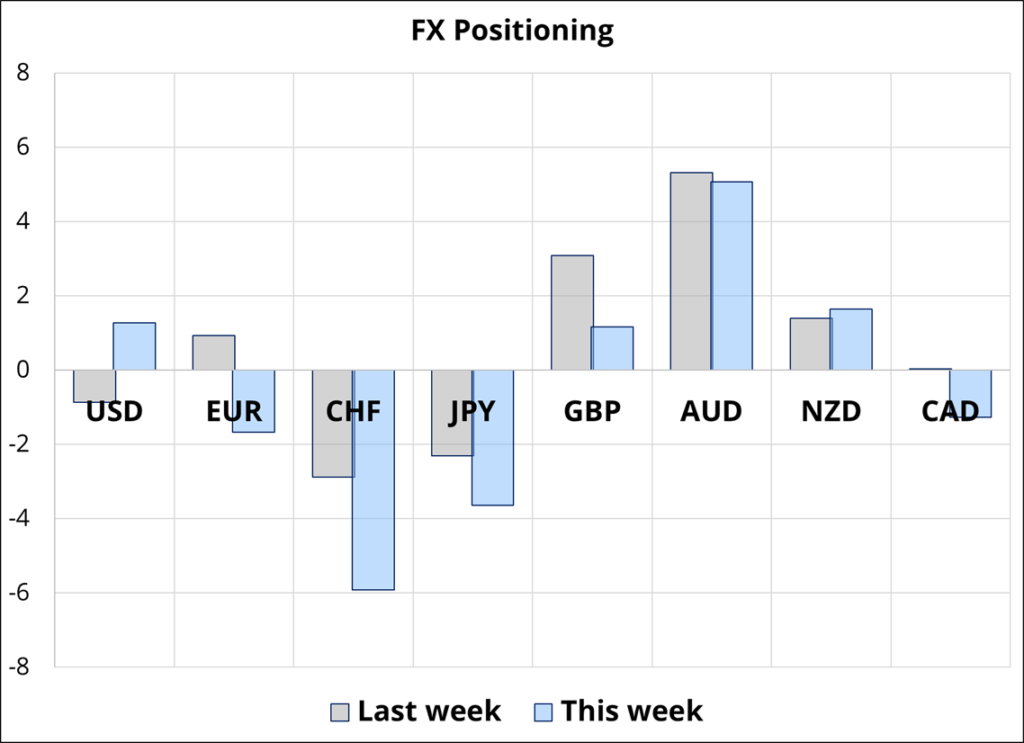

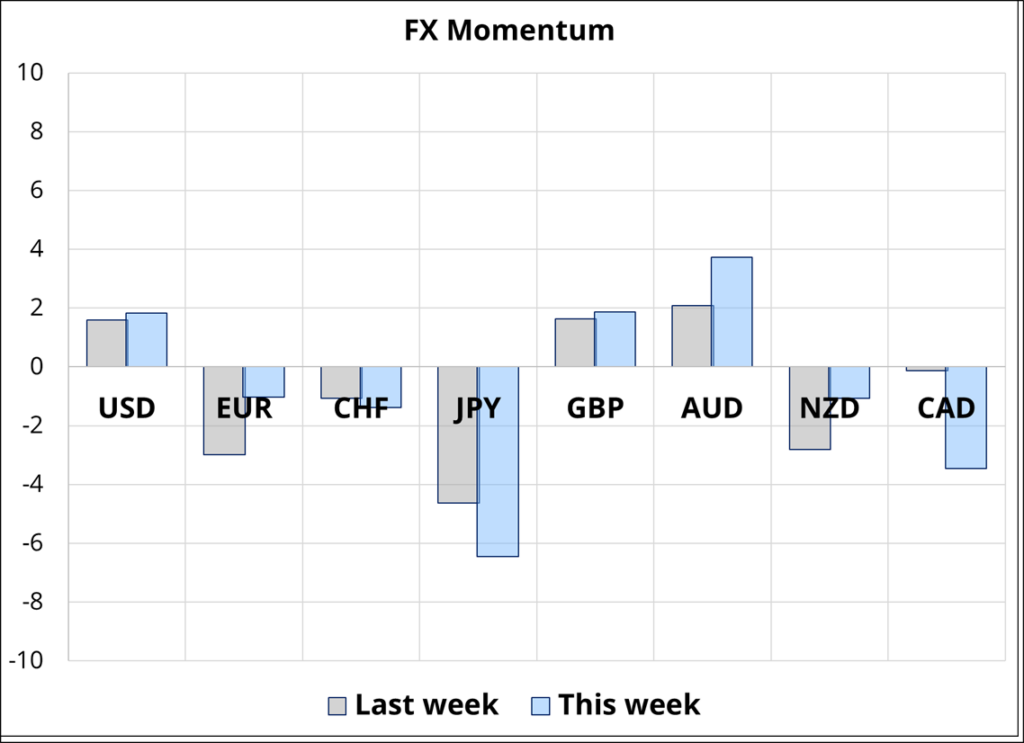

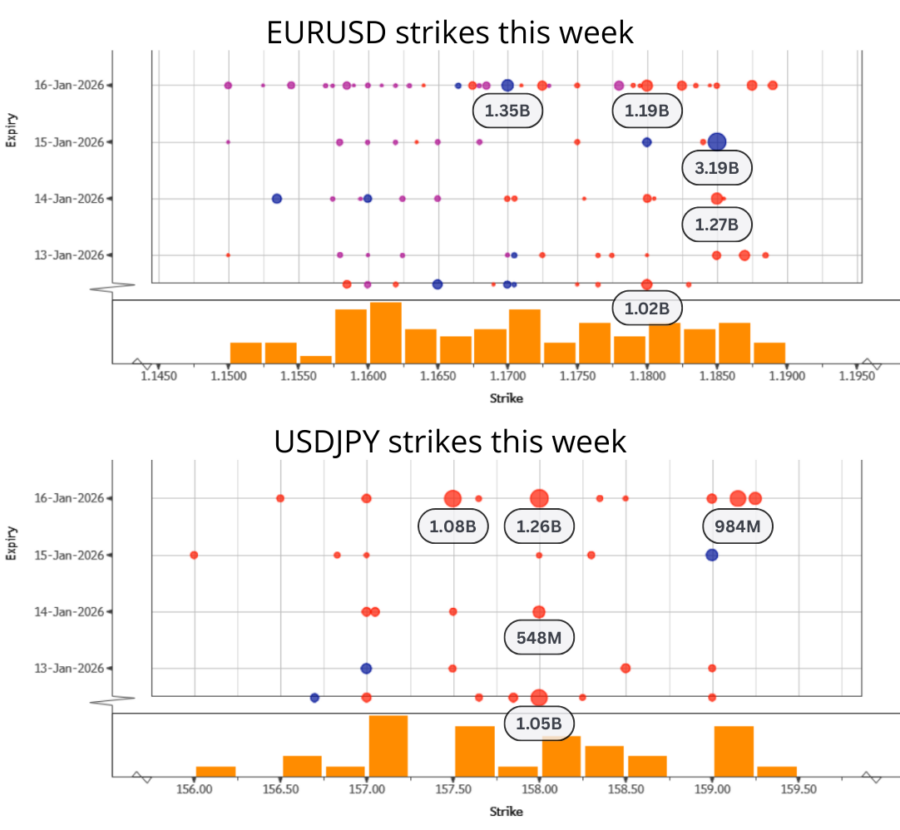

Hi. Welcome to this week’s report. The CFTC data has finally caught up, so this data should be on target again. The USD shorts disappeared pretty quick as short CHF and short JPY offset the long AUD position to yield a net close to flat or a big AUDJPY long, depending on how you slice and dice it. Note below that there are some large strikes coming off this Friday.

A Man Feeding Swans in the Snow

(Marcin Ryczek 2013)