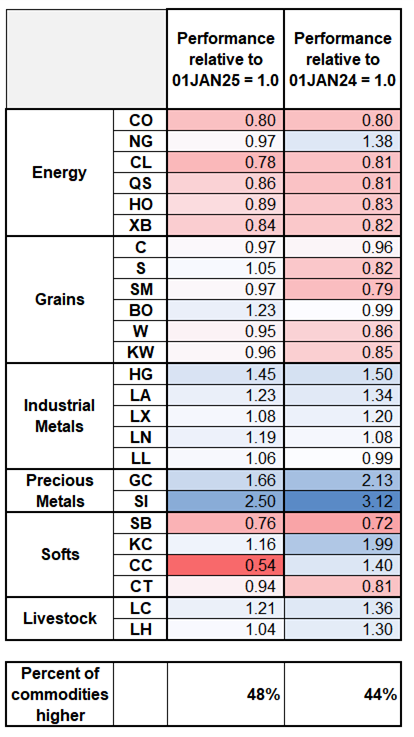

It’s just metals, really (and cattle)

The February 2026 calendar is incredibly satisfying.

It’s just metals, really (and cattle)

The February 2026 calendar is incredibly satisfying.

Flat

I used the term “commodity boom” in am/FX yesterday and others have pointed to rises in the BCOM and other indexes to suggest some sort of reflationary impulse or bull market or supercycle in commodities. This has also been described as a “fiat debasement” trade, though I have been less comfortable with that terminology because when I look around, I don’t really see the hallmarks of debasement. Zero revenue stocks aren’t performing that well, crypto trades like it’s never going to rally again, and many commodities are doing nothing, or going down = Not debasement.

This is more than just semantics, because it’s hard to forecast what is going to happen in markets if you don’t have a reasonable explanation for what’s going on right now. A friend of mine who trades commodities emailed me yesterday and said that it’s not accurate to call the current thing a commodity bull market. He said: “I would describe the commodities environment as ‘bearish’ with metals as a bullish outlier”.

This is a significant reframing compared to what I had been thinking and compared to what you read in the financial media. Below I show the performance of the main commodities, indexed to 01JAN24 and 01JAN25.

I accept my friend’s assertion! Since January 2024, it’s metals and livestock. Since January 2025, it’s just metals.

So we can hardly call this a debasement trade, or a commodity bull market. Metals are rallying on the global energy transition and a geopolitical change (metals are now strategic) and retail and financial speculators are pouring gasoline on the fire. There is no reflation trade here. That’s why bonds aren’t selling off, inflation is unlikely to soar, and bitcoin and whatever else aren’t rallying. And there is probably no catchup trade unless you can make the case for substitution of crude oil for metals. Which you can’t.

Changing how you view the commodity story might also make you less bullish AUD if you believe a narrow commodity bull market has less bullish implications for the Oz than a commodity supercycle. AUDUSD is the most crowded FX pair out there right now and once again, it’s not being very nice.

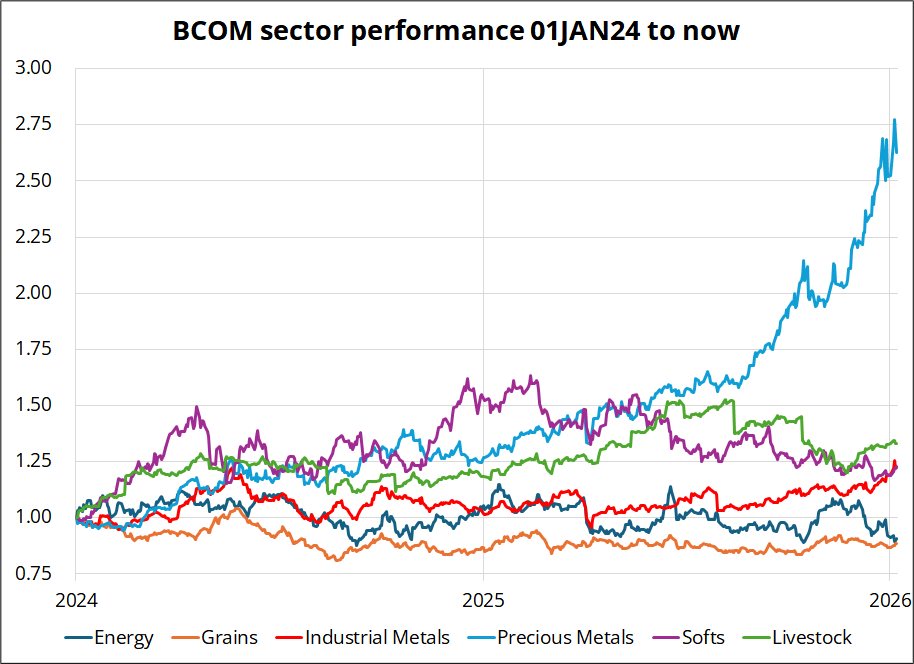

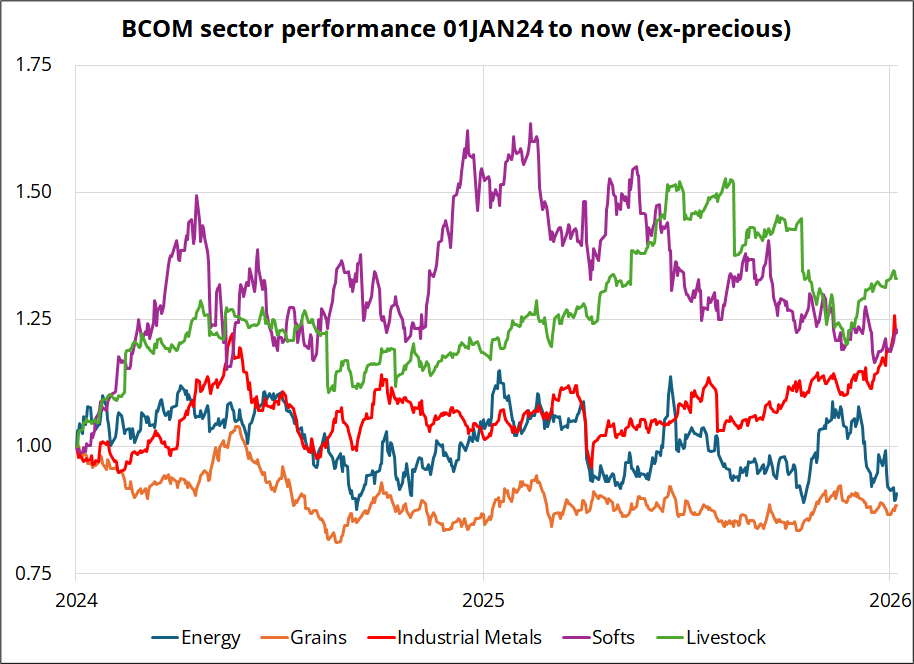

Here are the sector baskets within BCOM, if you’re curious. All rebased to 01JAN24 = 1.0.

Tomorrow’s jobs number is somewhat important at the margin, mostly because if it were to come in negative with a big jump in the UR, you could guess that January FOMC might be in play. Anything other than an apocalyptic release will see the Fed pass on rates. If the data comes in at all on the strong side, you might see a significant capitulation of USD shorts as the trade doesn’t make a ton of sense from a cyclical point of view and yet the market has put it on in size anyway. The market owns medium to large dollar shorts in AUDUSD, USDSEK, USDNOK, EURUSD, and USD/EM. While the EM longs are likely to be resilient, people are not going to hold onto USD shorts vs. AUD and SEK for very long given the amount of pain those currencies have inflicted over the past two years. There will quickly be a feeling of “here we go again.”

Looking at the higher frequency indicators for December, there are signs of strength all over the place. UR back to 4.4% or 4.5% and 99k jobs makes sense to me, e.g., because:

The 2025 angst over the US jobs market feels stale. Let’s see.

Have a 4X7 day.

The February 2026 calendar is incredibly satisfying.