You can’t front run the Mar-a-Lago Accord, just like you could not front run the Shanghai Accord

On this day in 2020, the novel coronavirus was named: COVID-19

Seeing this image again makes me feel lots of emotions

You can’t front run the Mar-a-Lago Accord, just like you could not front run the Shanghai Accord

On this day in 2020, the novel coronavirus was named: COVID-19

Seeing this image again makes me feel lots of emotions

Flat

Yesterday saw a new theme plus some recycling of an old theme and the market tried to buy bonds on the combo and failed. The themes are:

Gillian Tett got the theme going yesterday in this article, but it’s worth considering that a) much of the article recaps a 3-month old Stephen Miran essay and b) the editorial contains phrases like: “hedge fund contemporaries are speculating” and “Will this ever happen? I don’t know.” And “the fact that this wild speculation is swirling underscores the following points…” It’s a bit like when someone posts a conspiracy theory on Twitter and then justifies it by saying “Hey, I’m just asking questions here!” Anyway, it could happen!

The expected value of front-running the Mar-a-Lago Accord is super negative while the expected value of selling the USD lower gap on the news is strongly positive. Moving right along… The attempt lower in yields pre/post payrolls stopped right at the 100-day moving average.

This hold, and the possibility of a strong CPI tomorrow could bode poorly for newly-minted USDJPY and cross/JPY shorts. EURJPY, GBPJPY, and CADJPY lower have all been part of a minor JPY-positive theme of late. EURJPY held major support on the daily (see next chart) while GBPJPY and CADJPY both broke support, then recaptured it in a slingshot reversal formation.

So my short term view is unch from yesterday: Higher yields, higher cross/JPY, and higher USDJPY into and through tomorrow’s CPI. This is a short-term view.

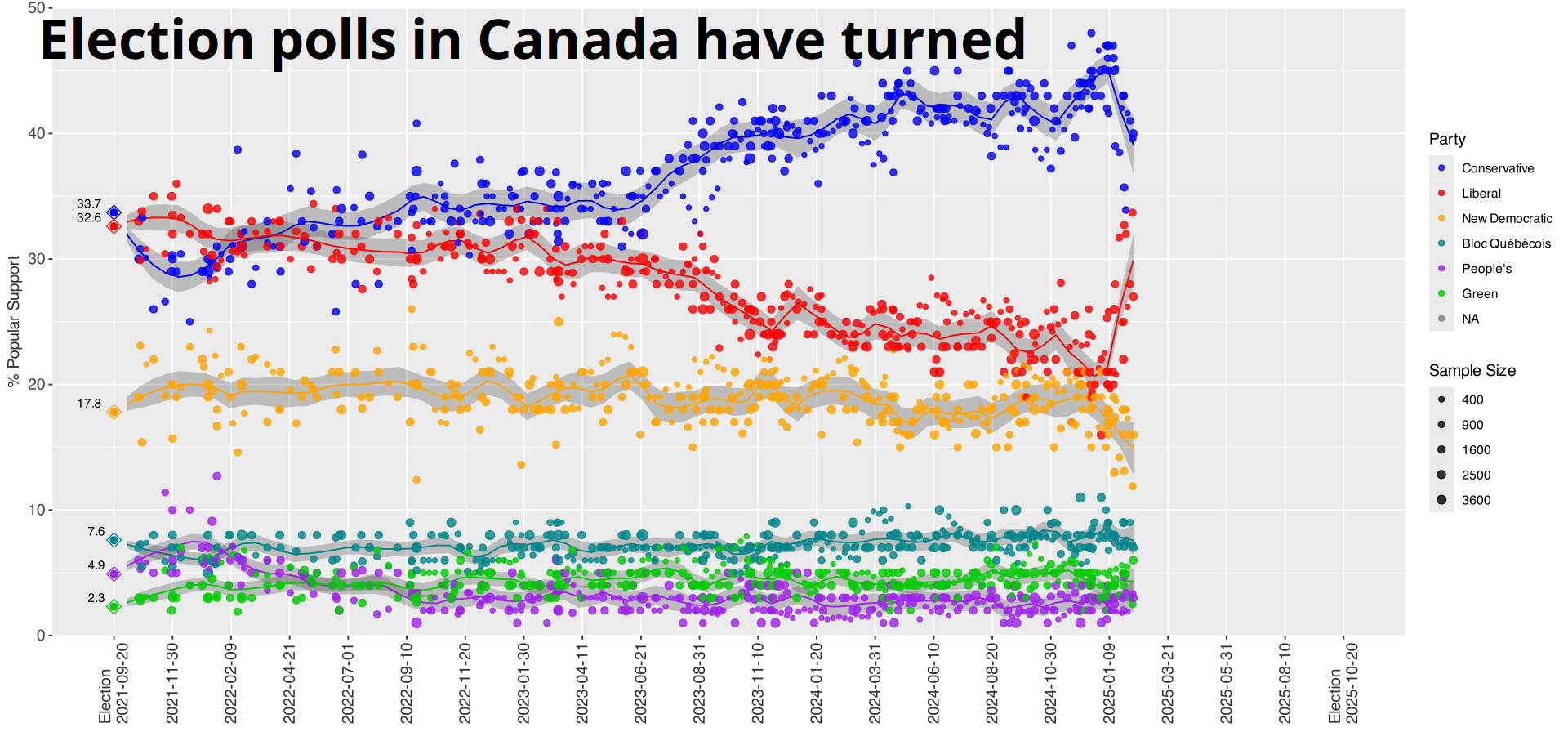

I think there is probably something to do on the theory that Trump will execute the tariffs on Canada on March 1 and punt or cancel for Mexico. The power vacuum in Canada creates a nice opportunity for a neck stomp that can be cleanly resolved with a great beautiful deal when Poilievre comes in. Then again, Poilievre is no longer a shoo-in.

Canada’s Liberal Party was left for dead, but Trump might have given it a second chance.

Oddly, Mark Carney, the most elite of the elite, is making a strong showing in a world where everyone thought that Davos Man was dead. We shall see.

Anyhoo, my idea was to buy USDCAD calls and buy USDMXN puts, thinking that if both get tariffed or not tariffed you probably do OK / break even but if Canada gets tariffed and Mexico gets punted, it’s a home run. But today is only 11FEB, and I don’t want to be long all that vol and experience potentially gushing theta bleed for three weeks while we chop around. The rise of Carney does pose a mild threat to CAD compared to Pierre Poilievre, as PP would be a closer ally to Trump. Carney has stated he will “Stand up to the Bully” and that is part of why he has risen in popularity lately. But if you were ever bullied in school, you know that standing up to the bully works well in the movies but less well in real life.

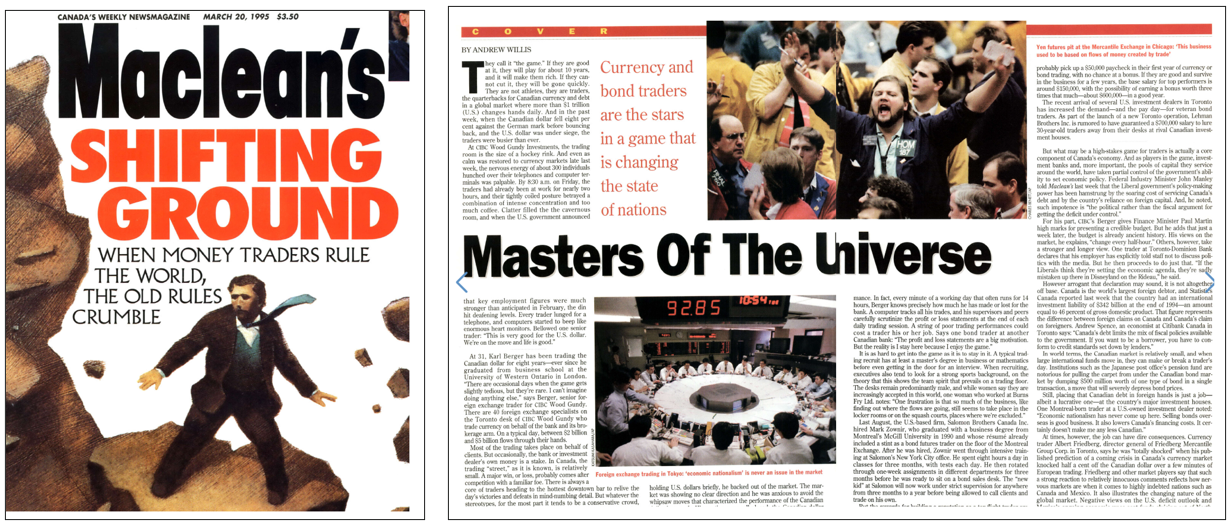

Bloomberg: Trump Tariffs Make FX Cool Again.

You know when FX trading was cool? 1995! Right after I got hired, there was a cover story about FX traders in Canada’s National News Magazine, Macleans. The spread headline was “Masters of the Universe.” This morning, I went through that back issue from March 1995 and it I will say: Going through old magazines like this really gives you a sense of how things never really change. For example, here is one of the lead articles, which echoes the current and forever-ongoing angst over DEI. This is from 1995!

And here’s the stuff about FX trading:

Me in 1995: “Look! Dad! I’m a Master of the Universe now!”

“OK, son. That’s great. I’m sure you are.”

:]

Have a game-changing day.

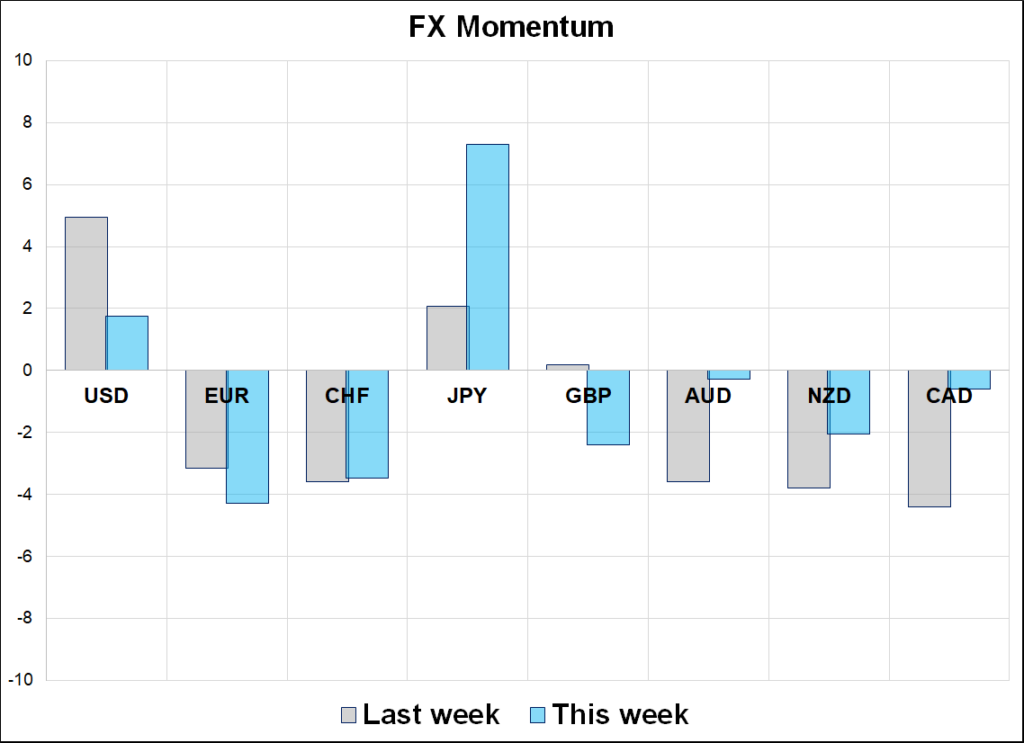

Yen gains as market loses interest in AUD and NZD

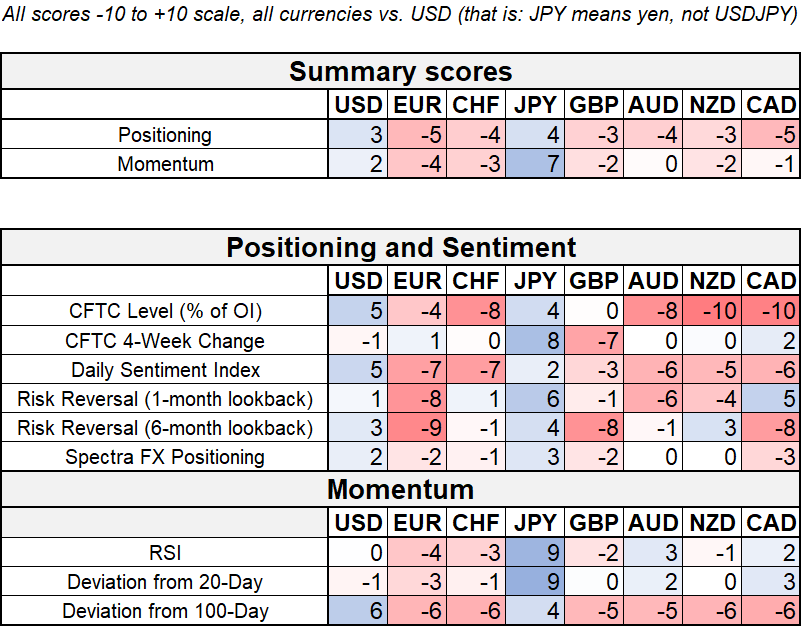

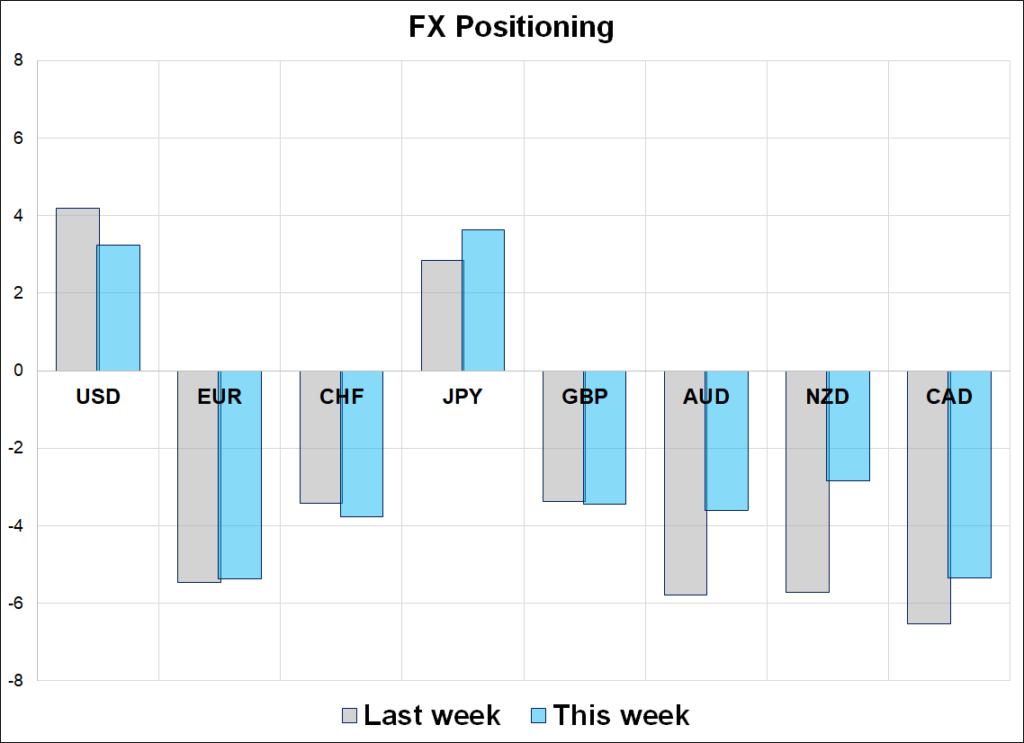

Hi. Welcome to this week’s report. USD positioning continues to come off the boil as the zone has been flooded with so many tariff headlines that nobody knows what is real and what is not. There have also been some stories circulating that would be incredibly dollar bearish (revaluing gold reserves and/or terming out debt) and these, along with the passage of time and flat USD momentum, have reduced the excitement around long USD trades.

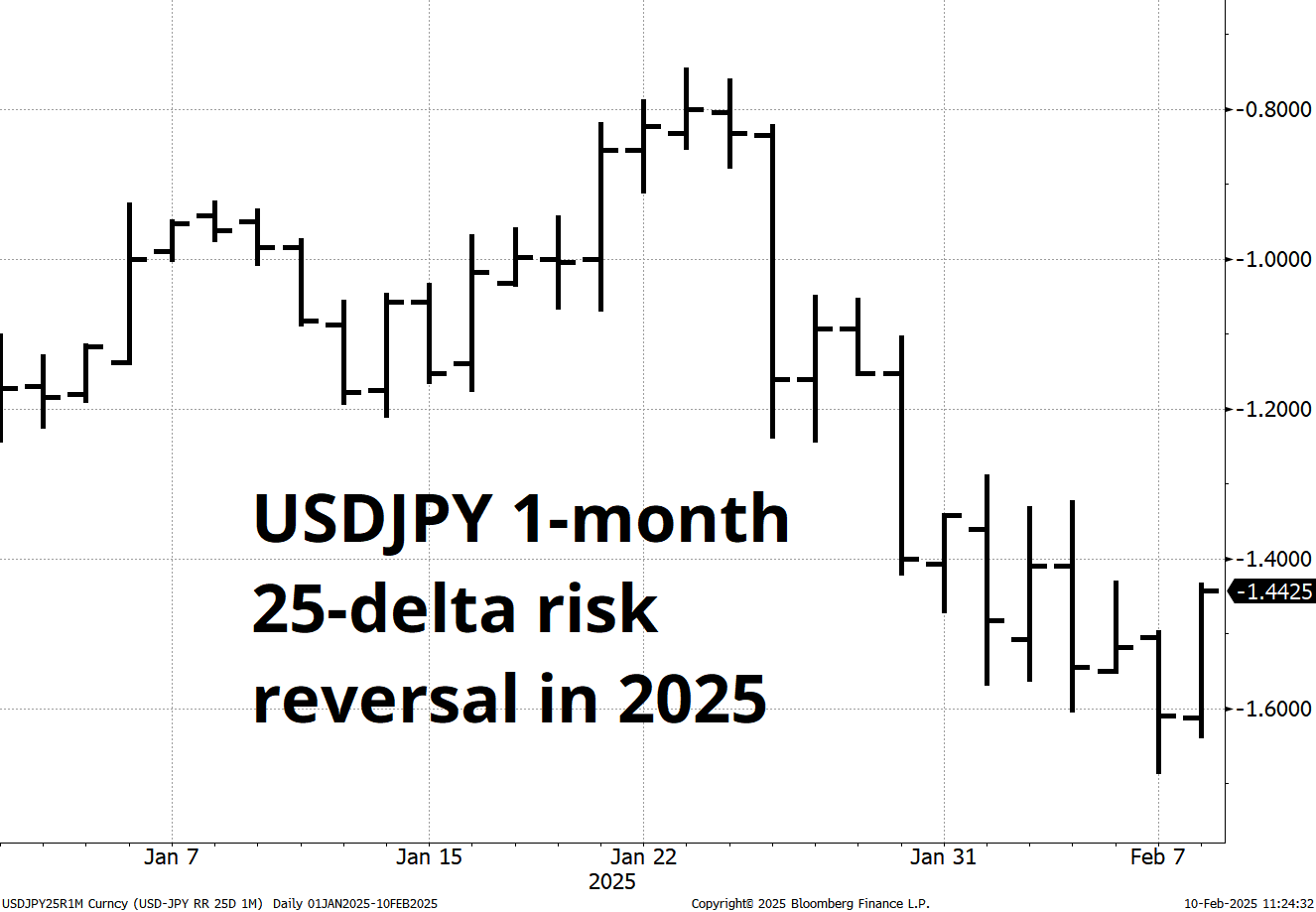

The biggest week over week change comes in JPY momentum as the dip in US yields and USDJPY’s status as the “only safe USD short” have attracted some interest in JPY calls vs. USD, CHF, CAD, and EUR. This is most-easily seen in the USDJPY risk reversal. It started the year around -1.2 (for USD puts), got all the way up to minus 0.75 and has now trended down to -1.44.

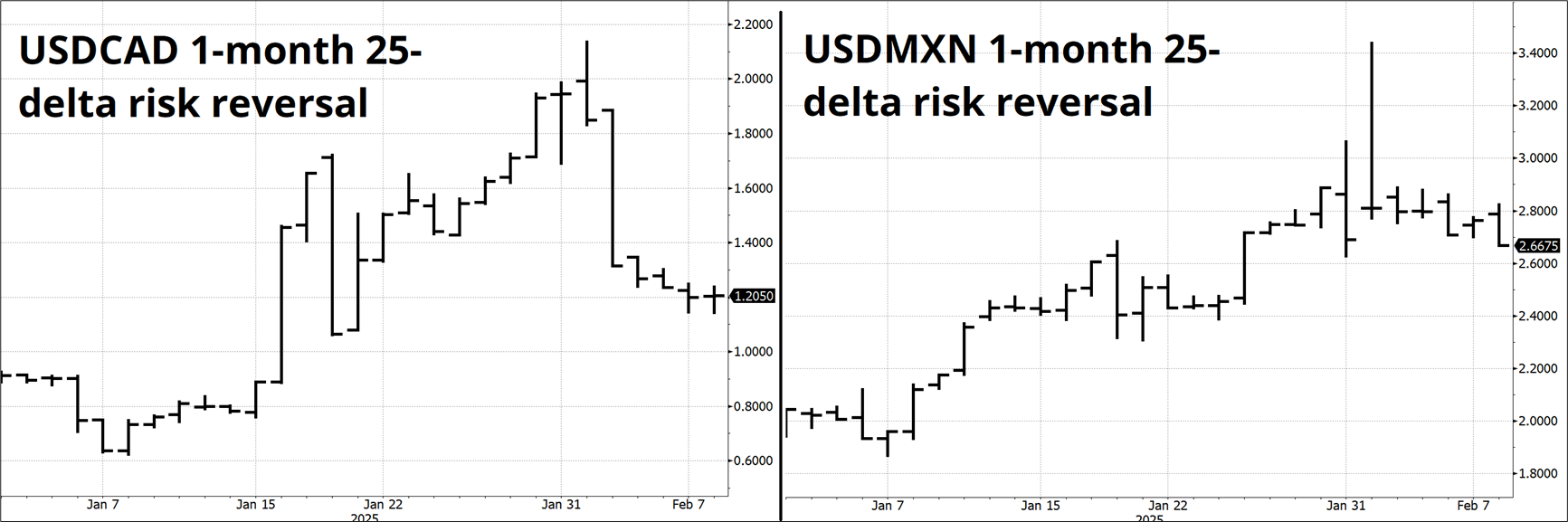

In contrast, while the CAD and MXN riskies have also repriced, they still remain solidly bid for USD calls and higher than where they started 2025.

The March 1 deadline for tariffs or no tariffs in Canada and Mexico looms large now, and there are some interesting trades to do if you have a view in either direction.

Finally, while AUD and NZD continue to show some short positioning, most of that is from slow-moving CFTC data. Hedge funds have lost interest in shorting those currencies as China inflation and Chinese yields have stabilized and commodity prices are rising.

On this day in 2020, the novel coronavirus was named: COVID-19

https://www.cnn.com/asia/live-news/coronavirus-outbreak-02-11-20-intl-hnk/index.html