The soft patch wasn’t particularly soft and now we’re ready to rip again

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

The soft patch wasn’t particularly soft and now we’re ready to rip again

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

I usually lay out my strong views in am/FX, but after I published that today, I came to a strong view. So—I will publish it here for now and follow up in am/FX on Tuesday. Here’s what I see as we enter September:

This appears to me to be a textbook short bonds, long gold situation. And I don’t think either trade is at all crowded right now. NFP is a huge wildcard, but if you’re long gold and short bonds, you are kind of hedged for a bad jobs report and might well make money on both if the report is hot. US monetary policy has been predetermined by dovish forces that have nothing to do with conventional economics. Or economics at all. This policy stance is unconditional, not data dependent.

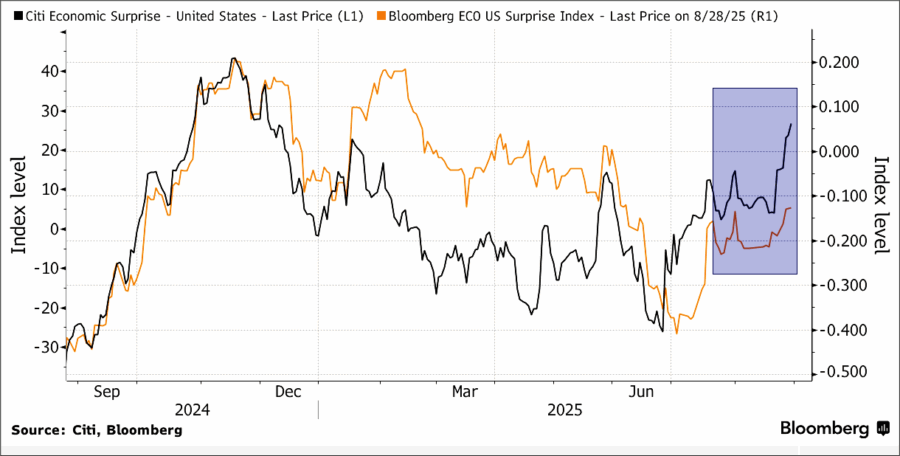

And the positive economic surprises are ramping up.

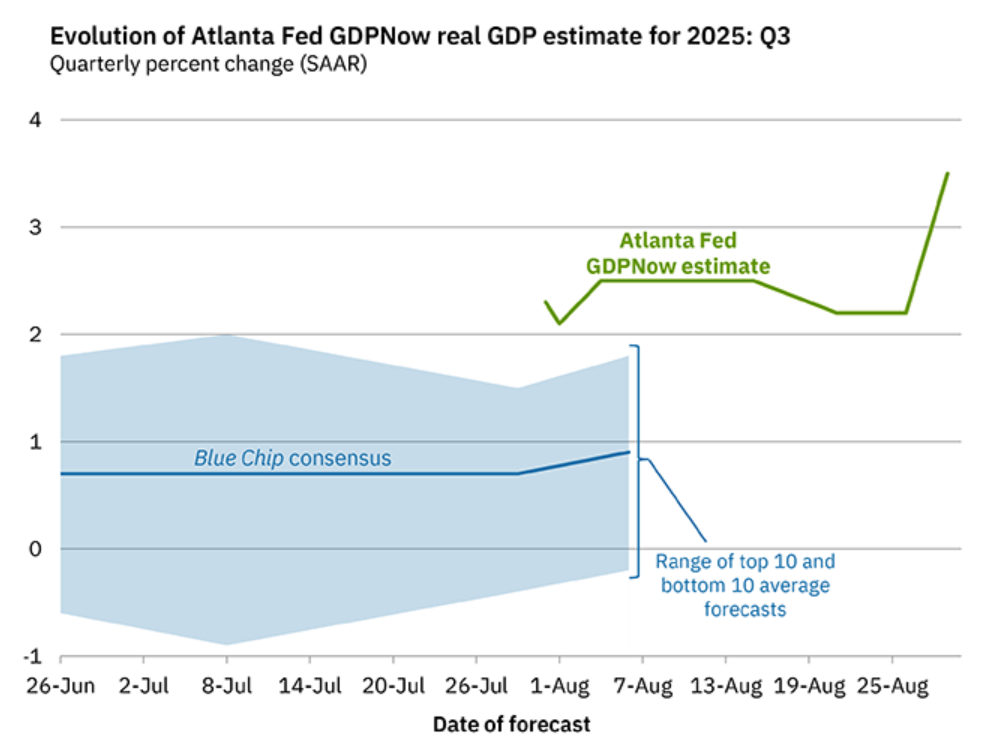

And Atlanta Fed GDPNow is ripping (it’s a good measure, despite the fact it gets a lot of hate).

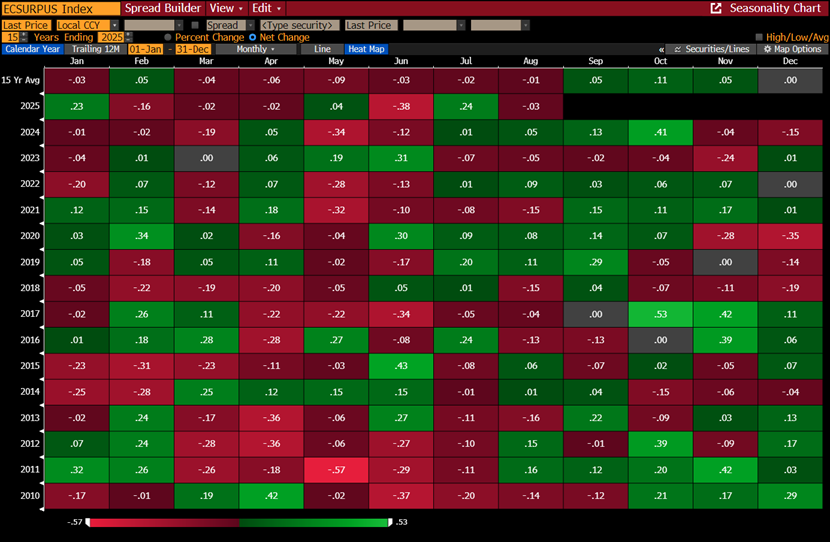

Seasonality of economic surprises is bullish from here:

Nothing in Friday Speedrun is ever investment or trading advice, but I will tell you what I have done. I bought 19SEP TLT puts and gold calls. Vol isn’t very high, and my belief is that when risk takers return from the sun-soaked shores of Southern France or wherever, they are going to see what I am seeing: Economic reacceleration and a neutered Fed that will slowly abandon inflation targeting in the name of fiscal dominance.

The story has been brewing for a while, but none of it mattered if the economy slowed. In the case of a slowing economy, the right prescription would be lower interest rates—whether they are lowered by government edict or by an independent central bank. Now, with stronger data here and more possibly on the way, the batsh*t is about to hit the fan.

Again, I am wrong all the time. Don’t copy my trades unless you have a personal belief in the view.

September tends to be a great month for trading because if you put stuff on in late August that seems logical, you get follow-through as macro traders return and amp up risk. Everyone is shooting for the big push into year end and that all starts the day after Labor Day.

Click on the ad to subscribe. If you’re not happy, just email me and I’ll refund you. Risk free. Unlimited upside.

The view espoused above is probably bullish stocks eventually, but could be nerve-wracking at times if the bond selloff is zippy enough. As such, I don’t think there is really a stock market trade here. NVDA and friends trade poorly after earnings as the second derivative of revenue growth stalls, and crypto has no friends as the DAT fad fizzles, halving seasonality is bearish, and there is no coherent bullish narrative for BTC in the short run.

Some inflation is good for stocks, but too much inflation is not, so we will have to see where this lands. My guess is that real world things like small caps will outperform digital things like AI for a few weeks if the market jumps on board my view of US reacceleration.

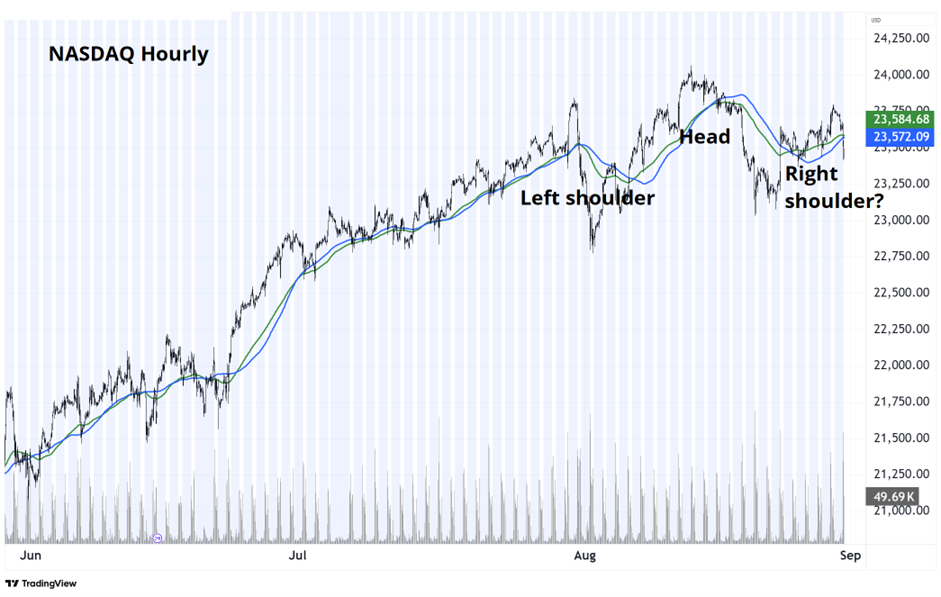

Meanwhile, the technicals in stocks are kind of sus as NVDA looks like massive distribution and double top 183.00/184.50 and the NASDAQ is tracing out a head and shoulders.

So I would buy a panic selloff and avoid trading here in the middle of the 22750/24000 range.

Here is this week’s 14-word stock market summary:

NVDA came and went and the AI story is alive but not accelerating.

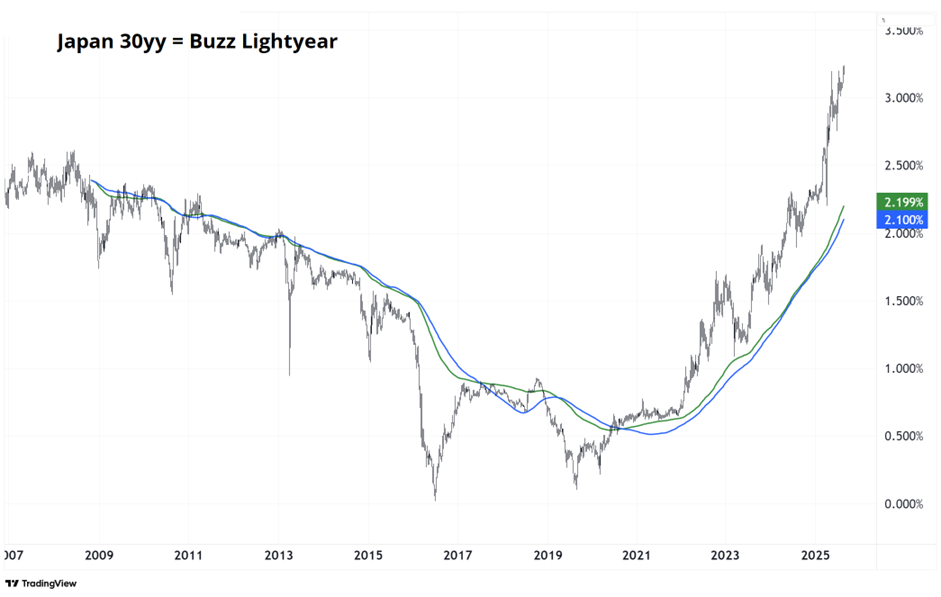

US 10-year yields have been doing nothing for eons, even as there has been tons of action in the front end of US rates and back end of Japan. In fact, Japanese 30-year yields hit an all-time high this week!

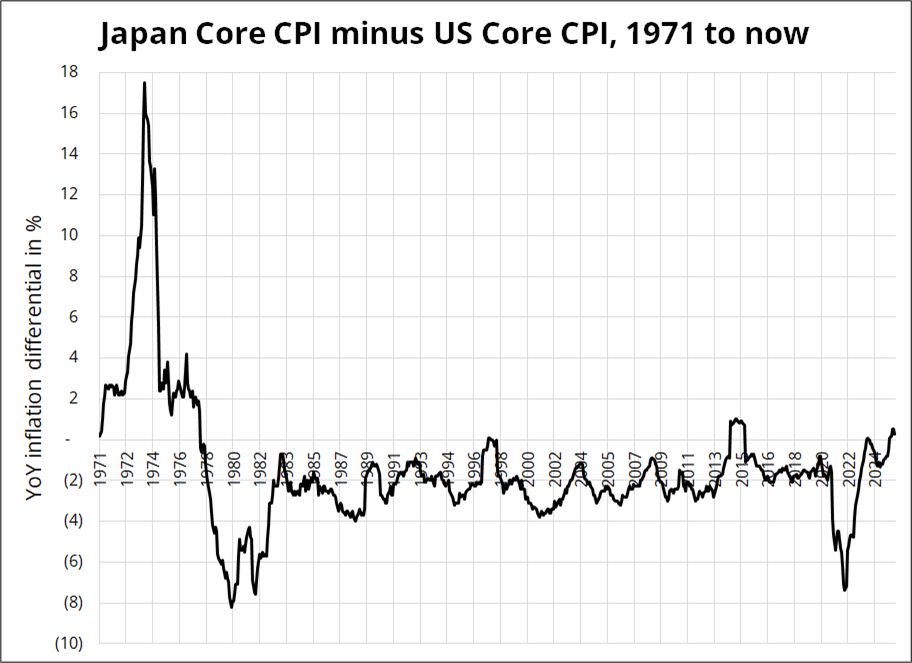

The BOJ continues its highly unorthodox policy stance, even as Japanese Core inflation is above the USA for the first time since Brent Donnelly was born.

That blip above zero in 2014 was the consumption tax.

With nerves a bit jangly on fiscal issues in the UK, the US economy reaccelerating, and Japan a permanent basket case, I think we see higher back-end yields in September.

A US acceleration is normally bullish for the dollar, but if the Fed is going to cut into it instead of hiking… Maybe not? Higher US yields almost always lead to a mechanical move higher in the dollar, though April proved that the opposite is possible. Still, short USD will be hard sledding if US yields start to go higher, while long USD doesn’t make a ton of sense given the macro context. Better to short the fiscal sinners (GBP, JPY and USD) vs. long the fiscal winners (CHF, TWD, EUR).

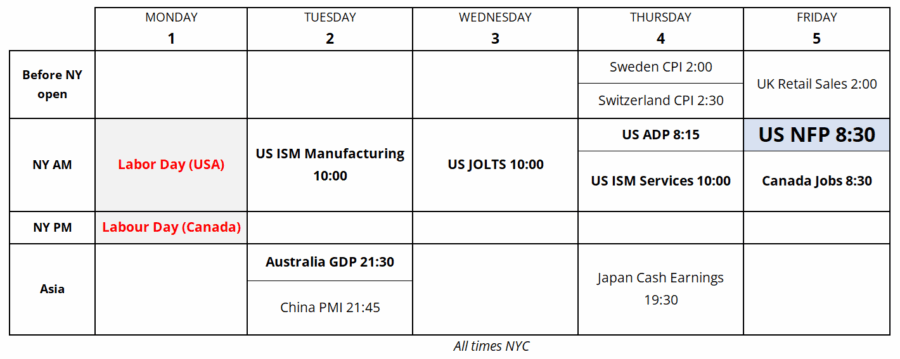

This week’s data calendar is odd in that it’s almost exclusively a USA thing, as the rest of the G10 is mostly data-free. Here is the calendar:

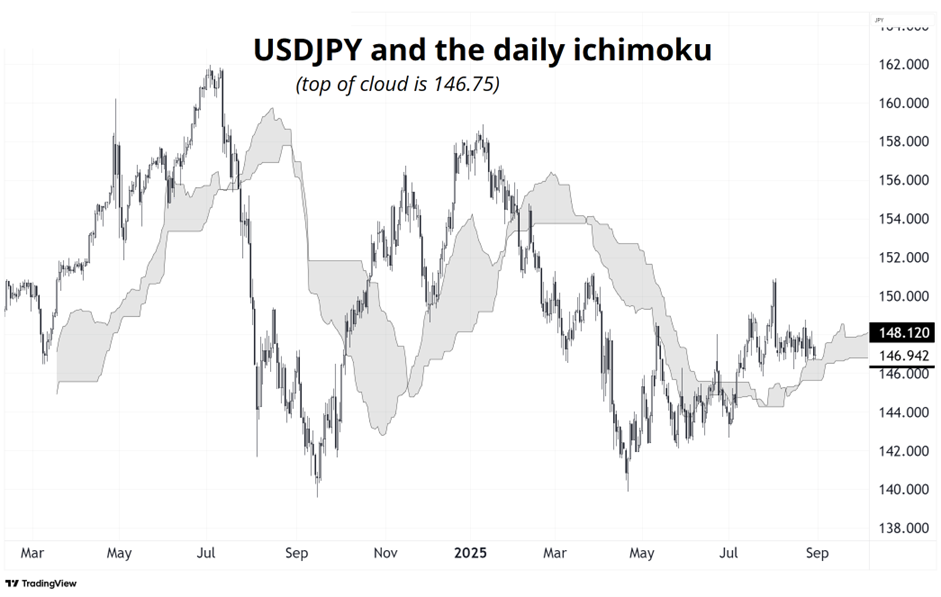

USDJPY is in a critical zone as we are perched just above the cloud.

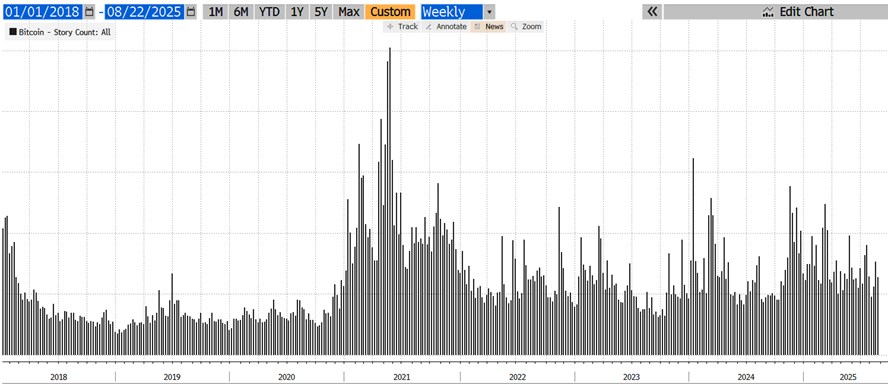

I get the impression that people are a bit bored of bitcoin as they seek lotto-like returns elsewhere due to bitcoin’s falling volatility. Here is the frequency of news stories about bitcoin on Bloomberg:

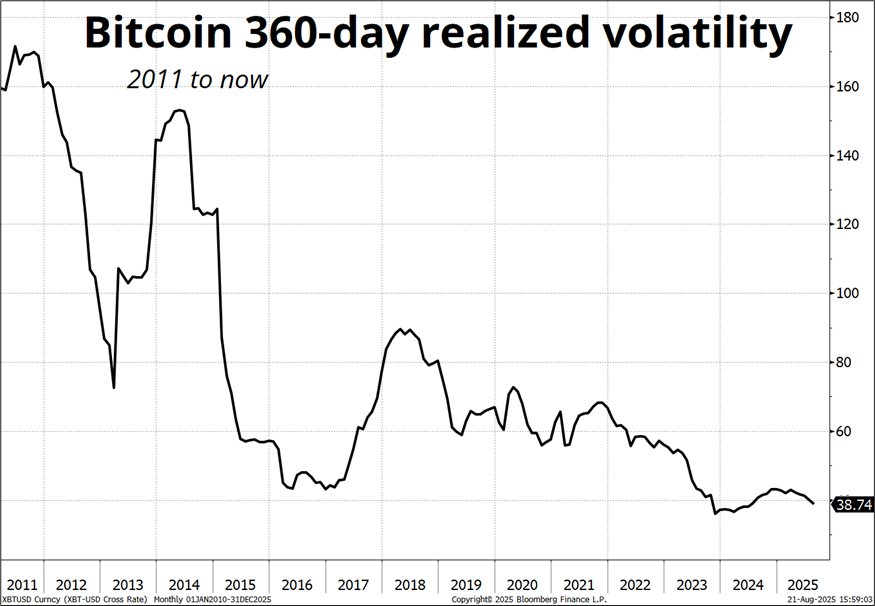

And here’s BTC vol:

Everyone was excited about ETH for a bit on the Tom Lee stuff, but with many other copycats failing to replicate MSTR’s stock price gains, that fad is fizzling fast too. I have been writing about and shorting these crypto treasury stocks for about 8 weeks now as they are the most preposterous fad since the NFT and SPAC fads of 2021. Much of the juice is now out of those trades as BMNR and friends have all cratered. One day we will get a chance to buy them all below NAV, I bet.

Anyway, I guess bitcoin’s weekend dump after the “dovish” Jackson Hole speech from Powell was a red flag and now we have a double top in BTC with the first one on Crypto Week at the White House and the second on the ETH party hosted by Bitmine. Remember that Microstrategy and Saylor executed a massive contrarian call, buying bitcoin at 11,400 in August 2020 when the world was on fire and everyone thought he was insane. Now, DATs are buying ETH at the all-time highs after a 400% rally in an effort to copy the OG.

Smells like stale broccoli.

If my view on reacceleration, fiscal dominance, and Fed-as-puppet-show is right, bitcoin will eventually benefit. But today it’s trading like a risky asset, not a store of value. And there is no coherent short-term bullish narrative.

I will leave bids at 94k and 82k in case of a freakout.

Note that bitcoin just broke through the bottom of the cloud and that’s not generally bullish short-term.

Any view I express in here could change at any time. I could buy BTC at those levels if I stick to my plan. But my plans often change. Trade your own view. Thank you for your attention to this matter.

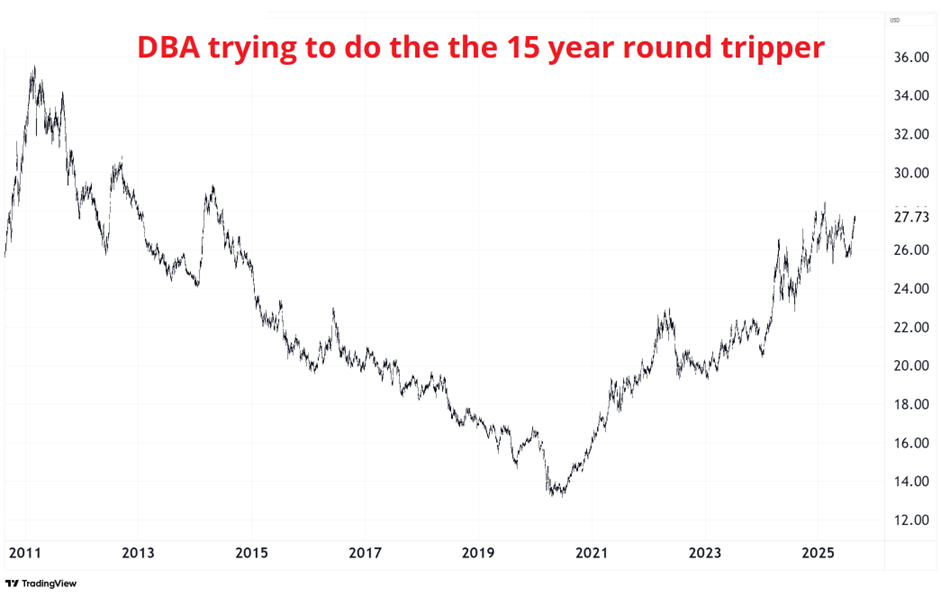

The corn trade was a bit of a bust as I only got tiny out above 11 in CORX and then squared the rest near flat. Decent idea, but my exit timing whiffed by one day. Fiscal dominance is bullish commodities, so gold, DBA (the ags ETF) and other things like that should find themselves in a good regime if the economic data stays strong while the Fed stays dovish.

Here’s a chart of DBA. It’s kind of boring to trade, but if you time it right, options can be juicy because the vols are low.

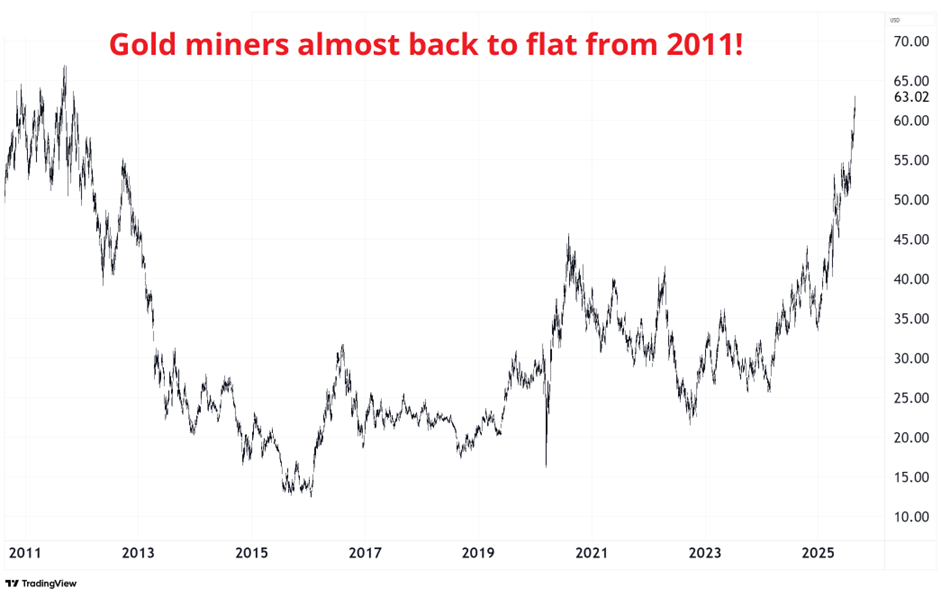

If you look at a ton of charts back to 2010, you will see that the same trades that have been working now were working back then in 2010/2011 because we had a sort of fiscal dominance trade going on back then too as central banks did mega QE and “whatever it takes”.

GDX, the gold miner ETF, is a great example of this.

If you bought XHB (housing) in 2011, you’re up 10X, if you bought NASDAQ you’re up 5X, and if you bought gold miners… Well. Sorry, eh? QE wasn’t as inflationary as everyone thought. In fact, it was deflationary.

It’s amazing how many truisms in finance and economics have subsequently proved to be exactly backwards. Tariffs are bullish USD. QE is inflationary. Tax cuts will pay for themselves. Interest rate hikes will kill the economy in 2022/2023/2024/2025…

Economics is an art, a science, a religion, and creative writing. All in one.

That’s it for this week.

Get rich or have fun trying.

From last week:

I bought some 57.50/60.00 Cracker Barrel (CBRL) call spreads as I would guess they will roll back to the old logo soon. Not investment advice.

Possibly the stupidest trade ever. And it worked!

![]()

We are on the stupidest timeline.

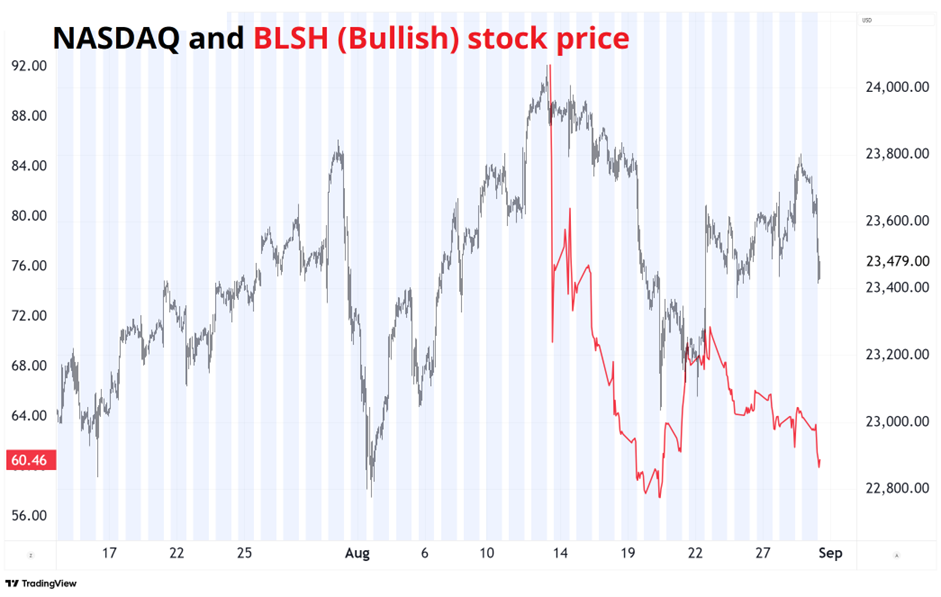

Meanwhile, the “Bullish” IPO continues to mark the exact high for all risky assets.

We are on the stupidest timeline.

*************

French language cover of Radiohead’s Creep, by Chloé Stafler. Très belle.

I mean the song is beautiful, not Chloé. I mean. Like, she’s fine. Just I am married. The point is the song is beautiful. Not her. She nails the high notes there at 2:42! Capo on 6.

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.