Sticky inflation + DOGE cuts = Stagflation narrative?

A larger version of these maps at the bottom of the page.

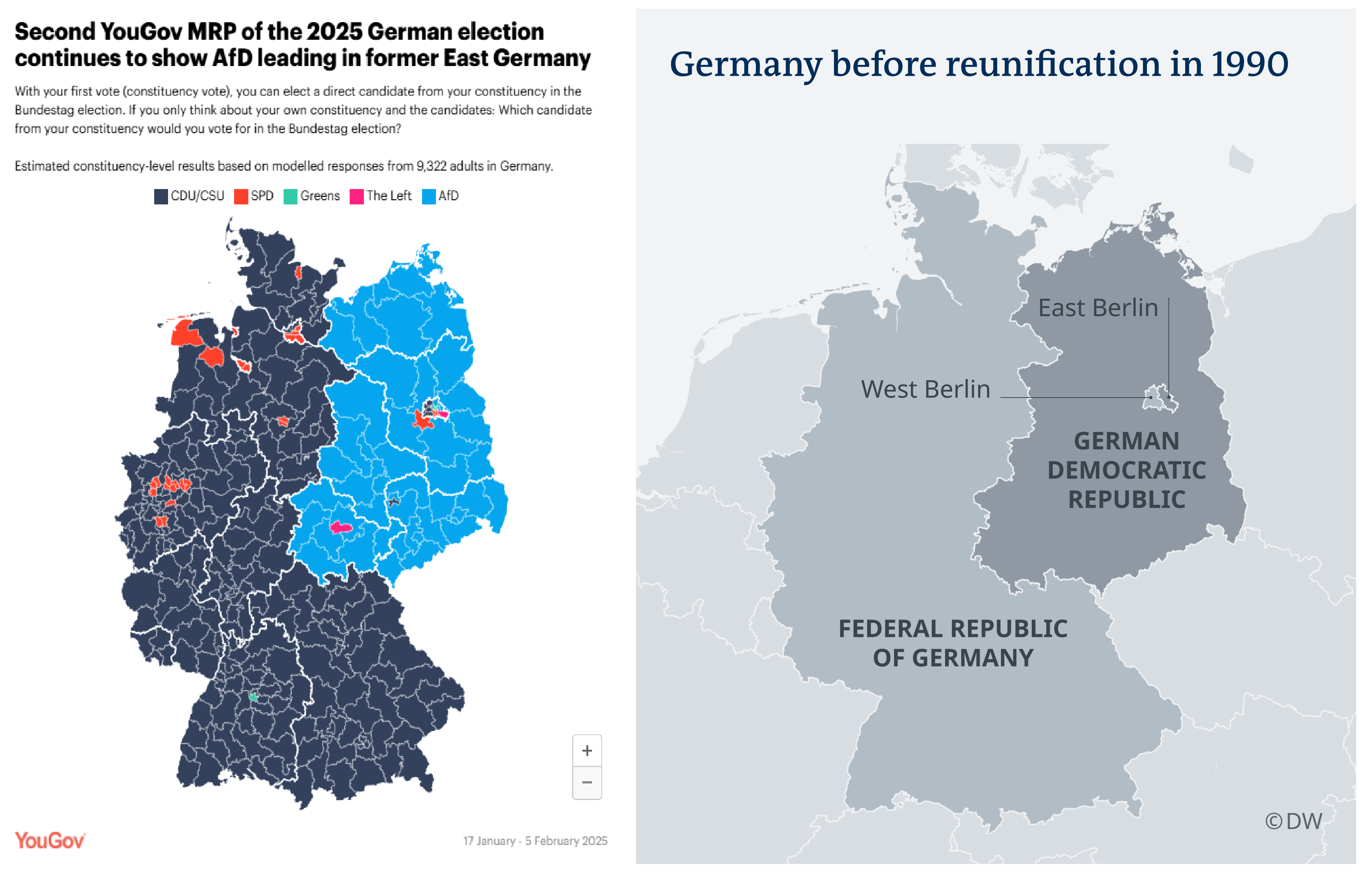

The image compares current German voting preferences (CDU/CSU in dark blue, AfD light blue) to a pre-1990 map of Germany.

Thanks Phil.

Sticky inflation + DOGE cuts = Stagflation narrative?

A larger version of these maps at the bottom of the page.

The image compares current German voting preferences (CDU/CSU in dark blue, AfD light blue) to a pre-1990 map of Germany.

Thanks Phil.

Short gold at 2940

Stop loss 3011

Take profit 2805

Things look a bit stagflationary. Commodity prices are going up (ex-oil), there are no eggs on the shelves, agricultural prices[1] are at 10-year highs, and Prices Paid indexes in the regional Fed surveys all point to trouble. Meanwhile, government, the largest driver of employment growth in the post-COVID period, is being axed by DOGE and the surrounding ecosystems (defense, lobbying, and consulting) tremble in fear as they cling to a wobbling Leviathan.

In case you’re not familiar with it, Thomas Hobbes’ Leviathan (1651) uses the metaphor of the “Leviathan”—a powerful sea monster from the Bible—to represent the state. His claim is that society needs a strong, centralized authority to maintain order and prevent chaos. Hobbes argues that without government, humans exist in a “state of nature,” where life is “solitary, poor, nasty, brutish, and short” due to constant fear and conflict.

To escape this, people form a social contract, surrendering some freedoms to a sovereign (the Leviathan) in exchange for security and order. The Leviathan metaphor underscores Hobbes’ belief in strong, centralized authority as necessary for societal stability. This is the original cover of the book.

Anyhoo, as tiny bits of the Leviathan are dismantled, the result is that jobs in Washington, DC and other cities will be lost. In the long run, transferring energy away from government and into the private sector theoretically increases productivity, but in the short run (i.e., the next year or two, at least) it’s bad for growth. The handoff to more productive work takes time as the fired workers are not immediately re-employed into the workforce. In the meantime, confidence and spending fall.

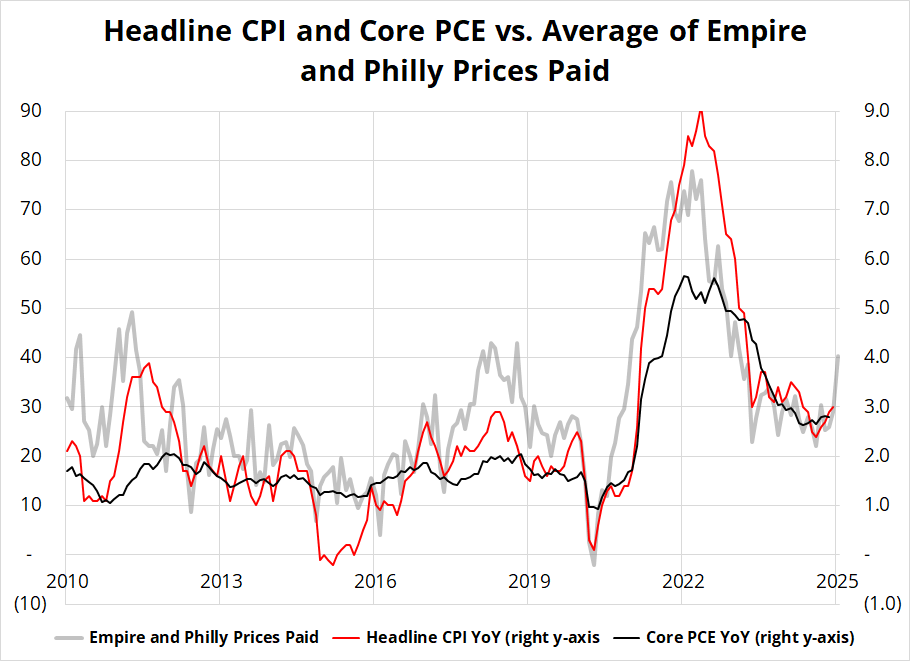

Rising inflation and rising unemployment are a rare pair. Take a look at the regional Fed surveys and Prices Paid vs. Core CPI and PCE. Here are a couple of charts.

We’ve got limited February economic data so far, but the Prices Paid components of the regional Fed surveys are moderately alarming:

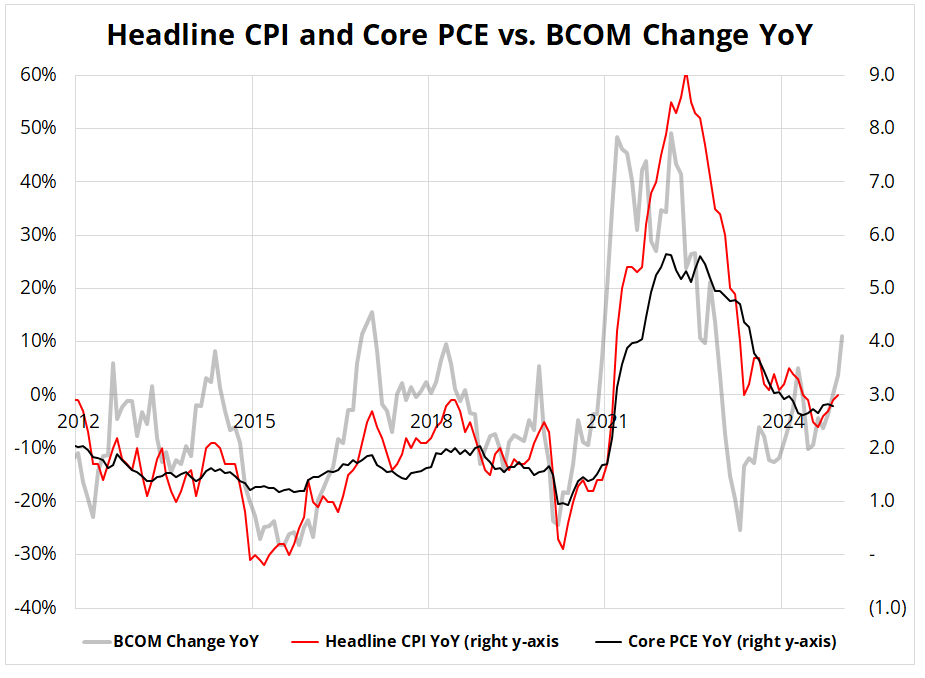

And here’s the same chart, subbing in BCOM instead of the Prices Paid measures. Obviously, this is mostly the same chart as the purchasing managers will be noticing the skyrocketing price of inputs and responding to the surveys with higher Prices Paid. That is, the Prices Paid indexes listen to BCOM.

But comparing the two charts does help confirm that inflation, which tends to be strong in February, generally, isn’t heading towards the Fed’s 2% target anytime soon. It’s probably going to move away from it.

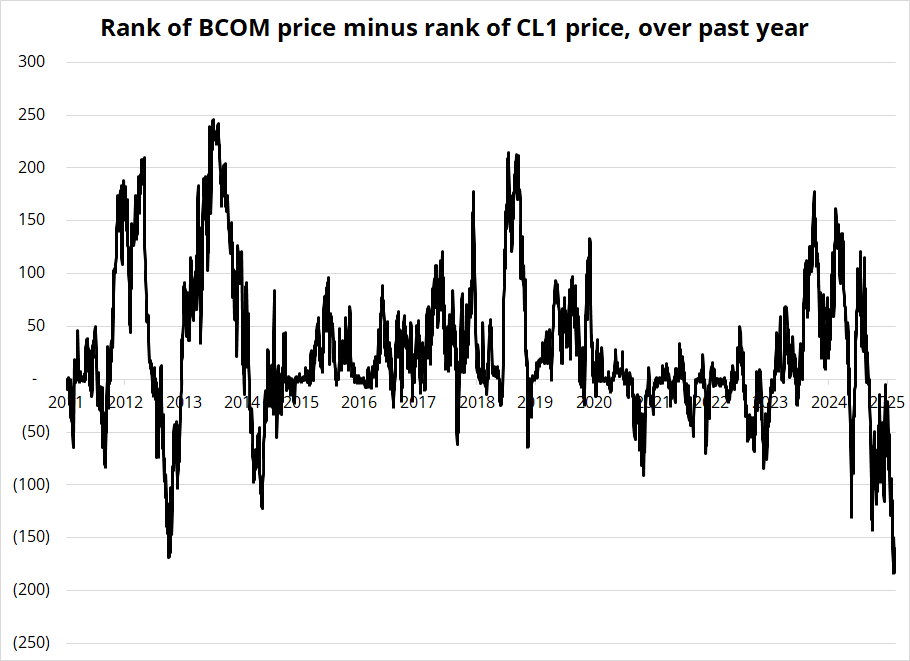

Speaking of BCOM, I mentioned yesterday that BCOM is wildly outperforming oil, and that is rare. Here is the chart I showed yesterday.

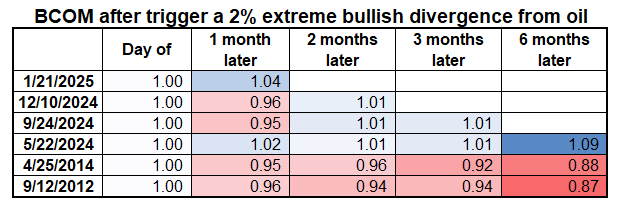

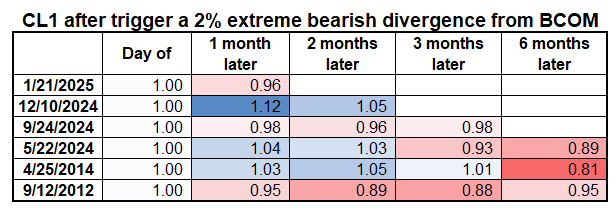

If you filter for the most extreme 1% of moves in this relationship, you get three out of three signals of a peak in BCOM.

Filtering for the most extreme 2%, you get three bearish signals and one bullish.

And here’s what BCOM did after the first trigger:

And here’s what oil did:

Small sample size, but these rips in BCOM unconfirmed by oil have been bigger picture sell signals for commodities, mostly. I suppose you could argue that given oil is a big input into almost all commodity prices, it’s hard for commodities to go to the moon when oil is anchored. Still, the sample size is small, and we have been triggered for a while so I wouldn’t read too much into this. If you find this output compelling, the simplest trade is probably to sell one or more of the DBA or BCI or DBC ETFs.

I have mistakenly been saying that March 1 is the tariff deadline for Canada and Mexico but it’s 30 days from February 3 which is March 4. I apologize for the error. So, to be clear, March 4 is when the 25% tariffs take effect unless there is a deal or another punt. Canada is rudderless right now and Mexico just hit back on the terrorism designations, so either or both country still looks at risk. Mexico fears that by designating the drug cartels as terrorist organizations, Trump is laying the groundwork for military incursions into Mexico. Sheinbaum.

Here’s the calendar.

I acknowledge that I’m talking about BCOM leading to stagflationary risks at the top of the page, then down lower I am saying that BCOM could well be peaking. One is a comment on current prices, and one is a low-confidence forecast.

The PLTR and WMT trends broke. Now the trend in JGBs broke (a bit). The trend in China yields has also broken.

Hmm.

Ich hoffe, dein Wochenende ist großartig.

—

[1] Using the DBA ETF.

Amazing maps via Phil V.