Many meetings, rates unchanged, lotta pressers

St. Patrick’s cane looks like π, but that’s 3.14, and today is 3.17

Many meetings, rates unchanged, lotta pressers

St. Patrick’s cane looks like π, but that’s 3.14, and today is 3.17

Short 07APR EURCHF 0.9010/0.8960 put spread +

long 07MAY 0.9110/0.9160 call spread for 2bps

Idea is that EURCHF holds around here due to SNB intervention and then we rally when the war is over

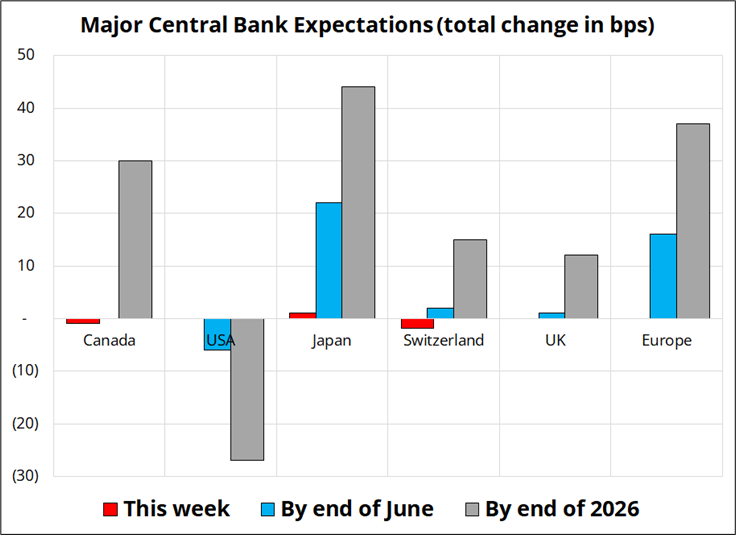

It is our job to get excited about central bank meetings, and while market pricing for any change at the flurry of CB confabs this week is minimal, there will be quite a lot to chew on in the pressers (as we saw last night with the RBA).

The forward outlook in a world of tightening financial conditions due to war and stagflationary vibes due to higher oil prices make things tricky for central banks who target inflation.

Below I show what’s priced for this week, into summer, and all of the rest of 2026.

You can see that this week’s meetings are not expected to deliver any change in rates, but you have some hopes for cuts in the US and for hikes elsewhere.

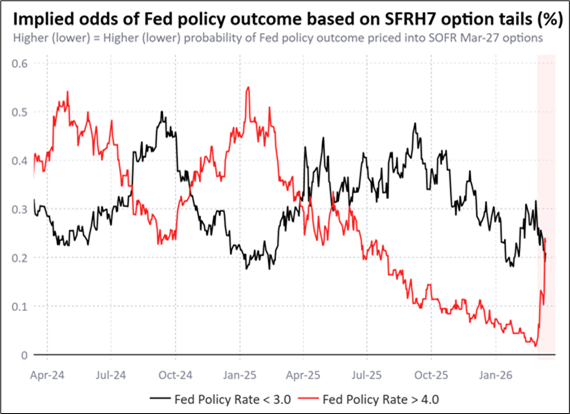

While the modal outcome for the US is cuts (i.e., gray bar is negative), the probability of a hike has moved higher as the war in Iran creates new complications for monetary policy (see lovely chart from Vanda).

The discussion of whether an oil shock is inflationary or deflationary continues to rage on and the answer is probably both and neither. It’s inflationary until it isn’t, as we have seen time and time again.

By tightening financial conditions, squeezing consumers, and cultivating stagflationary malaise, the inflation of an oil shock sows the seeds of subsequent mean reversion.

History has not always been kind to those central banks that hiked into the teeth of an oil scare as the ECB hikes in 2008 and 2011 are viewed as badly timed. The global rate hikes after the Russian invasion of Ukraine in 2022 were more necessary and appropriate as fiscal largesse was flooding the world with money at the time and labor markets everywhere were tight. Global economies were strong enough to take the hikes in stride, and we eventually landed at a point where economists convinced themselves that rate hikes were good for the economy because reasons.

One would have to presume that the starting conditions here are dramatically different from 2022 with global yields much higher and economic cycles much older. In March 2022, the ECB deposit rate was still -0.5% and Fed Funds was 0.25%! That’s amazing to think about given the global economy was already absolutely raging in 2021. So yes, central banks have cut from the high levels seen in 2023/2024, but still global policy rates are not exactly tickling the zero bound (ex-SNB ofc).

All this to say that the commentary from the central banks will be the most interesting aspect this week, especially the ECB (will they hawk up right away, or pray for an end to the war before their next meeting?) and the BOJ (will they greenlight rate hikes with USDJPY up here, or is Takaichi keeping them constrained?) It can get complicated quite quickly in FX land, however, as there is a point not far from here where the market will start to think that a too-hawkish ECB is actually bad for the currency because it will be judged a classic overreaction.

The Bank of Canada is the only central bank that looks mildly mispriced to me as inflation is below 2% and the UR continues to make new highs. 36bps of hikes by the December meeting seems almost impossible to me, even if oil stays above $100 for the rest of the year. That said, there is no way they can cut, either, given inflation base effects become less favorable just as the oil shock hits. The problem with most of these front-end rates trades is that there is not that much juice in either direction as it’s crazy for anyone to cut and insane for them to hike.

Fading these rates moves is tricky because of course pricing can go anywhere and while in the end the actual policy is the anchor, you need to go quite far out (December 2026) to get any juice. So, you need to wait a long time for the anchor to find bottom.

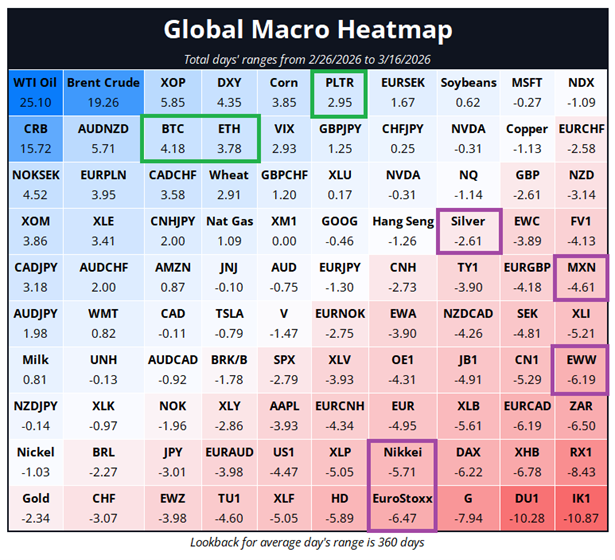

Yesterday I wrote about the well-known effect where positioning comes undone during times of risk aversion. This has been clear in the opposite direction with crypto as the digital coin world was max bearish going into the war and so bitcoin and ETH refused to go down and have now rebounded like beach balls underwater. The grid here shows performance of various assets 26FEB to 16MAR, with moves expressed in number of average day’s ranges.

I marked some of the most hated assets with green boxes and some of the most loved ones with purple boxes. The only thing that was popular, and performed, was AUDNZD as AUD got support from RBA expectations and mega dividend buying seasonality.

Many noticed bitcoin’s resilience in the 66k/67k area, and I did too, of course. I thought this would lead to a huge breakout up through the key 74k level, and I got long at not great levels (73k). Last night, we spiked to 76k and have now crumbled back below 74k. That is disappointing for the bulls, and I think it relieves the “bitcoin trades well!” condition that had prevailed over the past six weeks or so. It doesn’t trade that well, suddenly.

I cut my longs at flat, because I find the attempted rally last night to be supremely disappointing. You could argue that as long as we are above the moving averages and the cloud on the hourly (72500/72600) longs look okay, but it looks to me like the thing has failed and so I am moving on. Below 72000 is a full rejection of the up move.

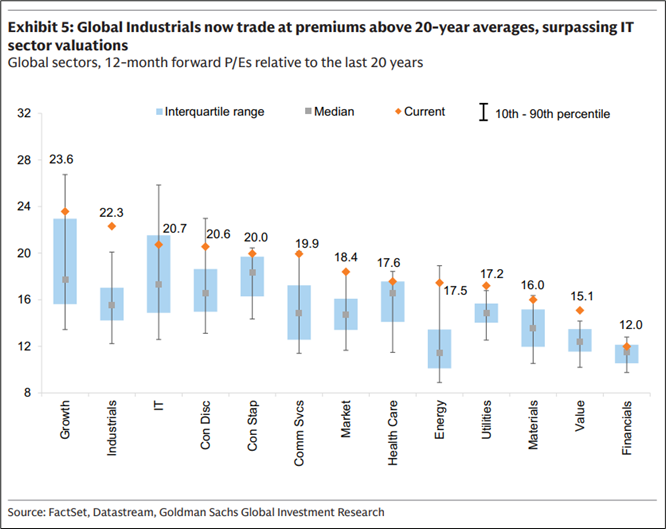

Nice chart from GS. Industrial valuations: wow.

Have a magically delicious, green day.

St. Patrick’s cane looks like π, but that’s 3.14, and today is 3.17

Saint Patrick’s Day is a public holiday in the Republic of Ireland, Northern Ireland, the Canadian province of Newfoundland and Labrador, and Montserrat.