After all the election drama, January 20 is almost here.

JRR Tolkien would have been 133 years old today.

In contrast, Treebeard is at least 11,000 years old.

After all the election drama, January 20 is almost here.

JRR Tolkien would have been 133 years old today.

In contrast, Treebeard is at least 11,000 years old.

Flat

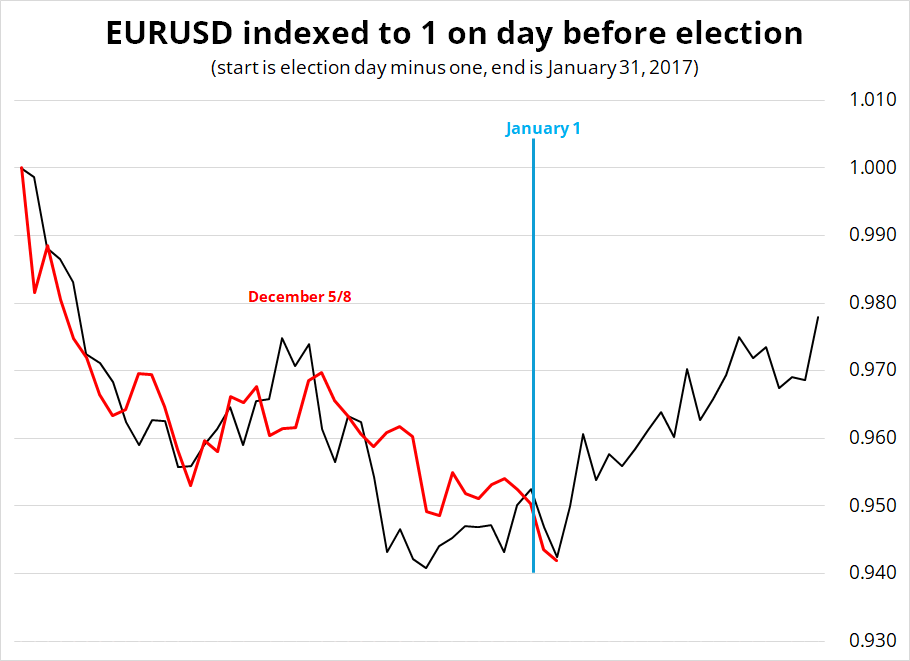

EURUSD continues its freakishly accurate replication of the price action after President Trump was elected in 2016.

This analog will make sense until it doesn’t, of course, because if Trump enacts a 10% global tariff or a 25% tariff on Canada and Mexico on January 20th, the USD is going up, not down. That said, it remains an eerily-similar setup with the market max long USD at the highs and the clock slowly ticking as we await the policy principles.

There were many different features to the market in 2017, including a dovish BOJ that was holding rates negative, but there were also many similar features. The most strikingly similar aspect is that EURUSD rallied in August 2016, peaked just above 1.1200, consolidated in September, dropped to 1.08 in October, rallied a bit, then sold off down to 1.03 in November/December.

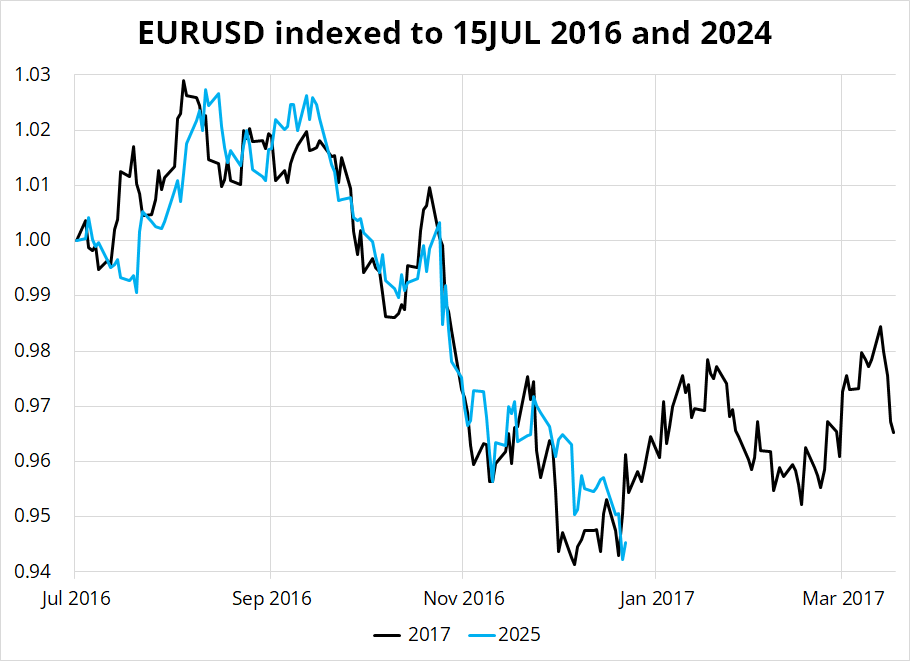

You can see in the chart above that the fit is kind of incredible. The two series are indexed to 15JUL of their respective years but given EURUSD was mostly trading on the exact same handles, the chart looks similar if you just use a normal y-axis. This year’s action is all just about exactly 150 pips lower than the 2016/2017 action. The summer high in 2016 was 1.1350 and this summer’s high was 1.1206 and the low in 2016 was 1.0388 and this low was 1.0226.

I don’t want to overstate the importance of this thing, but it’s hard to completely ignore the parallels. The onus on the newsflow is now to deliver some shock and awe, or bonds will rally, and the dollar will sell off.

USDCNH is decaying higher as January 20th approaches and we are 27 basis points away from the all-time highs. You can see that 7.3750 is kind of a line in the sand here as that was the 2022 high that saw significant intervention and the 2023 high, too.

There’s not much the authorities can do when the yield differential (red line) approaches 3%, but there is not nothing they can do either. In early 2017, they engineered a huge funding squeeze and then got lucky as Trump slow-played the tariffs by beginning a long negotiation process. They might not get lucky this time.

While Chinese yields buckle under the weight of deflationary impulses and Chinese equities tread water, praying for Team China to come in buying, the currency is on the verge of a dislocation. Curiously, AUD and emerging markets have traded incredibly well to start the year despite mega drops in EURUSD and GBPUSD.

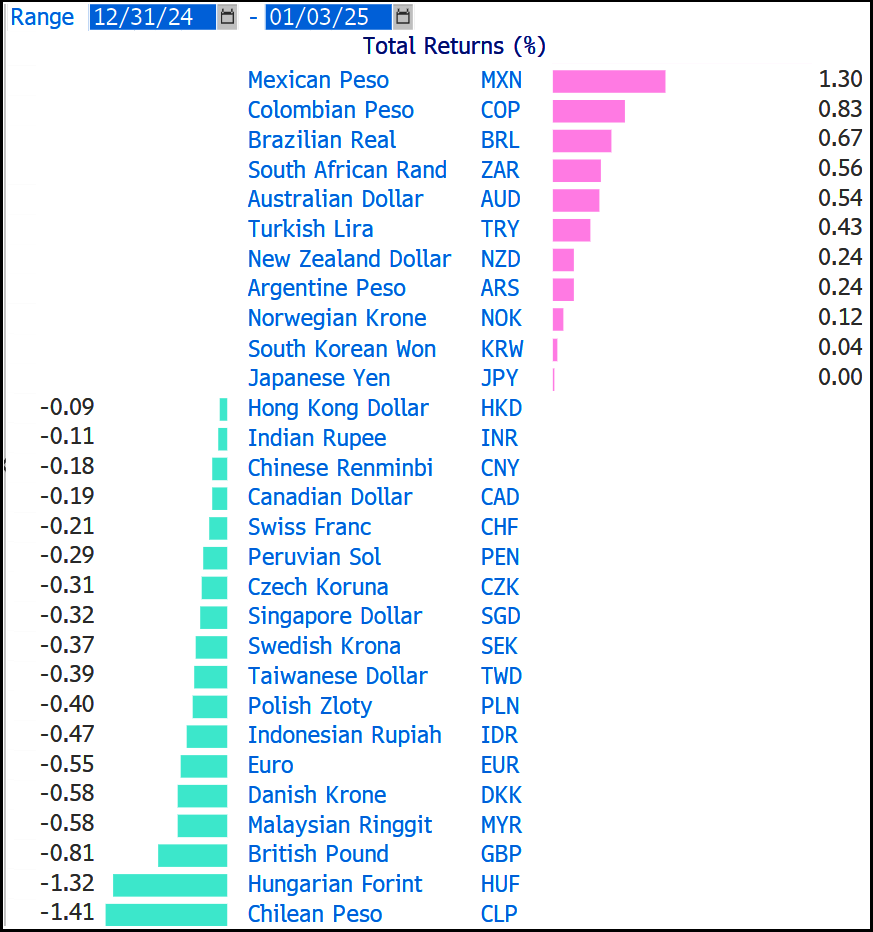

The dispersion in FX performance yesterday (see table) suggests large LHS flows in EURUSD and GBPUSD, not a real macro move in the USD. In fact, rate differentials have moved in favor of the EUR vs. the USD so far in 2025. As discussed yesterday, I don’t see any reason to chase the USD here given positioning and the risk of scaled tariffs and a repeat of 2016/2017, but I also see zero reason to be short USD yet as a shock and awe result on January 20 is still possible. It’s OK to be flat.

Next week’s calendar picks up a bit after this week’s holiday-compromised event schedule, with German CPIs on Monday morning, Services ISM (the only one that matters), JOLTS, ADP, NFP, three auctions, and the start of earnings season. Financials are almost as popular as AI stocks right now, so BAC, WFC, and BLK will matter. Note that stock markets are closed for President Carter’s funeral on Thursday.

I often write about how it’s impossible to make accurate predictions beyond a week or two out because of the nature of complex systems like weather and financial markets. Here’s a great piece from Bob Seawright on the topic of bad predictions and the impossibility of accurate forecasting in complex systems.

https://betterletter.substack.com/p/2024-forecasting-follies

Have one weekend to rule them all.

Today is JRR Tolkien’s birthday. He was born in South Africa on January 3, 1892 and died in England in 1973.