Stocks can’t wait forever for good news.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Stocks can’t wait forever for good news.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

The pessimists and oil experts are increasingly in control as the War in Iran drags into its fourth week and dreams of a rapid bomb and run campaign evaporate. The goals of the war are opaque and ever-changing and anything is possible at this point. What we do know is that oil has been sky high for almost a month, permanent damage has been done to multiple oil and LNG facilities, the Strait of Hormuz is effectively closed and there is no visibility on any sort of endgame. Neither side can be trusted to provide any useful information as war is fought with drones, bombs, and propaganda.

For markets dreaming of a binary “we won!” announcement from Trump, the odds look less and less likely. Even a de-escalation by the United States and Israel at this point does not guarantee that the IGRC will reopen Hormuz and it does not bring back the capacity already lost to bombings. Iran is incentivized to drag things out, and that’s what’s happening.

The result has been nearly-unbelievable moves in interest rate markets this week. They are believable in the context of what we are seeing today, but imagine telling someone a few months ago that by March 2026 the Fed would be priced for hikes, the ECB would be priced for multiple hikes, and bond yields around the world would be tickling 2008 highs. U.K. 10-year yields and U.S. 30-year yields are back to 5%. More on this in the fixed income section.

This wicked tightening of financial conditions comes from a starting point of extreme bond bullishness, max equity longs, and 18 years of BTFD mentality in stocks. My view is that we are in an unstable equilibrium. Oil is going to be $40 higher or lower in six months, and in the meantime the path to that end result is going to be hella volatile. Same deal with stocks. It feels to many like that lazy period going into COVID and Russia’s most recent invasion of Ukraine in 2022 where the majority of traders and investors are more afraid of missing the rally than hedging for the dump.

Stocks often take a long time to roll over, even in the face of what looks to me like super bad news. This was the case in 2007/2008 as stocks made new all-time highs well after the subprime crisis started, it was the case in 2020 when tech was peaking in February 2020, long after Wuhan was flooding the news, and in 2022, long after global rate hikes and a terms of trade shock from energy were threatening ebullient animal spirits. There are large buy flows that are passive (retirement money, NISA flows, etc.) that don’t care about price or news. They just get done. And they’re always there. So bears need excellent timing because the faintest whiff of good news creates brief but terrifying sellers strikes and everything spikes just high enough to trigger short covering / capitulation.

The interesting aspect of the current moment is that stocks currently have negative drift. That is highly unusual. Normally, the path of least resistance is up for stocks, but right now, each day that the Strait of Hormuz is closed, the vise closes a bit tighter on financial conditions and the global consumer. Every day oil is above $100, it costs the world more.

So for now, the NASDAQ is in familiar territory as behemoths like NVDA pretty much have not moved in 10 months.

I am bearish today and into next week. I feel that equities are doing their best Wile E. Coyote impression right now, but I think they will go lower in the next two weeks because:

There is a tendency for stocks to stick around into option expiry and then do what they were going to do afterwards. This seems like one of those setups.

This product does not offer investment advice, but I am focusing on SNDK, KORU, and PLTR as shorts. These are stocks that have a heavy retail participation and with retail mostly in hiding right now, lack of participation on the bid side could lead to disproportionate drops if the bottom falls out of the indices. The PLTR chart is a pretty clear setup, risk management wise as it should not go back above $175 or I am wrong.

Here’s PLTR with the 100-day and the cloud.

Note the waning momentum and the 20% rally you can now sell into.

I prefer setups like that where the “I am wrong” point is pretty obvious. This avoids getting in a fight with a stock that won’t cooperate. Sitting short things that are going up for more than a few days is a good recipe for poor mental health. Preservation of mental capital is just as important as preservation of financial capital.

I barely ever buy puts because they are almost always overpriced. I would rather be short a high-vol stock that I hate and sell 20-delta puts against it. This is harder to risk manage than buying puts, but much higher EV.

Here is this week’s 14-word stock market summary:

Wile E. Coyote doesn’t hang in the air forever. He is saved, or falls.

https://www.spectramarkets.com/subscribe/

One of the most boring debates in economics and on Twitter is the question of whether oil shocks are inflationary or disinflationary. The answer, of course, is BOTH. And the size of the inflationary and subsequent growth shocks are conditional on starting conditions and the length of the shock. So let everyone argue all day about whether it’s inflationary or deflationary. It’s not that simple.

For a Google Deep Research analysis of the topic that I thought was pretty good: Read here.

Anyway, here’s what the UK front end did this week.

The five most dangerous words in trading are: There’s too much priced in.

Of all the hedge fund blowups I can think of… A great many of them involved fading a rates market that had too much priced in. Yes, these markets are eventually anchored on the final central bank outcome but unless you’re sizing tiny or work at PIMCO, you run the risk of getting stopped out. Editor note to avoid litigation: I’m not saying PIMCO is bad at risk management; I’m saying they are so huge they can ride stuff longer than you or I can.

Furthermore, you might think (as I do) it’s insane to see the ECB about to repeat the same mistake it made in 2008 and 2011, but that’s just what they do. They target inflation. And part of the philosophy is: Hey, we can’t control oil prices, but we sure as heck can control the demand side of the economy. So we will crush demand, and oil prices (and inflation) will fall. That’s not wrong! It’s just painful.

Central banks only have demand side tools. So they do what they can or what they feel they must. Anyway, the point is really just that no matter how stupid rates pricing looks to you… It can get stupider. It can always get stupider.

I am supposedly an expert on currency trading after 30 years or so of doing it, but Ben Hunt has done a better job of summarizing the current situation with the USD than I have been able to do.

A paradox is emerging in which the war simultaneously strengthens the dollar’s short-term position through traditional crisis demand while eroding the institutional foundations that support its long-term dominance. Treasuries are not functioning as a safe haven, fiscal deficits are expanding under wartime and stimulus pressures, and the media language that once argued forcefully that there is no alternative to US largecap growth is fading. The convergence of rising inflation expectations, weakening growth signals, and retreating confidence in dollar-denominated assets points to a market caught between competing time horizons—seeking dollar safety now while quietly pricing that the post-war world may look structurally different.

This accurately reflects the view of our clients. People don’t love being long USD because it seems like a bad situation for the U.S. But you have no choice sometimes. So macro PM’s are using EURUSD as a hedge for equities and short natural gas and whatever and buying AUD puts and other USD calls as protection, too. But nobody is really aggressively long USD, other than super short-term punters.

This is reflected in the option market where short-dated stuff is bid for EURUSD puts while longer-dated stuff is bid for EURUSD calls. My time horizon is always sub-two-weeks and I am bullish USD for now because I believe oil is going to keep going and stocks are going to crap out next week. AUDUSD could go 2% lower and EURUSD could be 1.1400 in a week or two. I am short both but my views change all the time so subscribe to am/FX if you want to know what I am doing IRL.

I am going to drop a fairly large excerpt from am/FX today because while it discusses EUR/NOK and I know you don’t care about Norway, it has broader implications for anyone that uses correlation in their trading. I would have included this in my new book, but it’s in proofreading and layout and it’s a real beyatch to make changes at this point.

EXCERPT!

Whatever you are trading, you are trading oil. Actually, that’s not completely true. I think what we are trading here is a combination of oil and equities. The regime of OIL UP/STOCKS DOWN is a radically different one from OIL UP/STOCKS FLAT or OIL UP/STOCKS UP. Bigger picture macro, this is pretty obvious because in a regime where global demand is strong, you have a happy story and assets perform well. In a supply shock, you have a bad story, and risky assets tend to suffer. The current situation is somewhere in the middle as it’s clearly of the bad variety in theory, but if it’s binary and temporary, there’s no reason to sell stocks or be scared. Everything will mean revert and anyone who sells the hole will be disappointed.

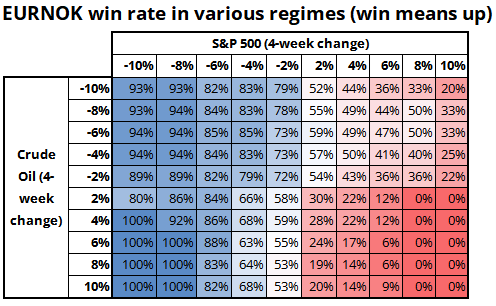

Nowhere is this regime-dependent disparity of performance more evident than EURNOK. While higher oil prices should benefit Norway, in theory, that’s not how currency markets behave. Hedging of Norwegian foreign asset holdings dominates if U.S. equities sell off hard. Here is a matrix showing four-week win% for EURNOK in various oil vs. SPX regime combos.

Most of the time, raw correlation numbers don’t mean much. It’s not usually that simple. It’s either non-linear, or there’s a second critical variable, or both. I think this is an important thing that not everyone always understands. Now you may look at that table and wonder about the sample size when you see numbers like 0% and 100%. The sample sizes are mostly quite good.

For example, the regime where oil is up 6% or more and SPX is up 6% or more in the same 4-week period, EURNOK is up 2 times and down 34 times. It’s remarkably consistent. The lessons here apply to many correlation observations. If you look at one variable (oil) in isolation against another asset, you miss the complexity of the oil vs. risk appetite interaction. You can’t just overlay oil and EURNOK, you need to be aware of the fact that higher oil is good for NOK but only when equities are stable. If equities crap out, NOK selling by equity hedgers completely dominates the oil-positive story. Note: When I say “crap out,” the meaning is “fail” as in, rolling a 2, 3, or 12 in craps. It has nothing to do with anything scatalogical.

Looking at single variable correlations to FX or to any other asset class very often misses all the nuance and is completely useless. Those huge correlation grids are an okay starting point, but they are overused.

END OF EXCERPT

I was briefly bullish bitcoin there for a bit but the attempted recapture of 74,000 failed and now we are back into low-vol, what are wӬ doing hӬrӬ? Kind of trading. All the people that crave vol have moved to oil and silver and gold and the use case for crypto in a portfolio remains confused as it has stopped trading like a risky asset, or digital gold, or anything. It’s as random as I have ever seen a market trade.

If I can’t explain why it’s moving, and the technicals aren’t working it goes in here…

Gold is not good. Copper not good. Platinum not good. Corn good. Oil best. Hormuz is an energy and fertilizer story and potentially an economic headwind and so it all makes sense unless you think of gold as a safe haven. It’s more like a safe haven half the time and a risky asset the other half, and when r/wallstreetbets is limit long, it’s down $900 on a massive surprise war.

Rule number (I can’t remember what number) from my book titled (I don’t remember which book):

It doesn’t always have to make sense.

The Brent crude chart is interesting because when Russia went into Ukraine (again) in 2022, oil never took out the highs after the initial explosion. That is true now, too, as we have made a huge double top at 119.50 so far. If the experts are right and this is the biggest shutdown of oil capacity, ever, we are going to make new highs barring a rapid de-escalation. Problem is that de-escalation doesn’t guarantee how far energy prices will fall. There is permanent damage to some facilities, with LNG capacity in Qatar, for example, unlikely to come back to previous levels for years and reopening of Hormuz likely to take weeks or months.

And yes! Wile E. Coyote’s middle name is Ethelbert

That’s it for this week.

Get rich or have fun trying.

A beautiful song and equally uplifting video

*************

A banger from the early 1990s.

*************

*************

US college application rates are lower when students experience bad weather during the campus tour.

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.