The rate cut debate heated up this week and so did every risky asset in the world.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The rate cut debate heated up this week and so did every risky asset in the world.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

Here’s what you need to know about markets and macro this week

Before we get started, more feedback on Spectra School. This is from a trader on the desk of a G10 central bank:

I took your course despite the fact I have been in markets for quite some time (!!). Essentially, I wanted to see if this would work for my team as part of their ongoing learning. I take the view that I shouldn’t tell people to do stuff I shouldn’t be prepared to do myself.

I’d like to congratulate you on the quality of content, and delivery of the information. It makes a real difference to the learning experience, and I think it’s something my team can really gain some great insights from.

I really enjoyed the course, and my colleague, who is very new to markets, also gained so much from the information presented. She has certainly become something of a “spectra disciple”!

Well done and thank you for bringing quite complicated subject matter to an audience in such a well-articulated and easy to understand course.

Thank you, and keep up the great work!

Check out the video about Spectra School right here.

Let’s go!

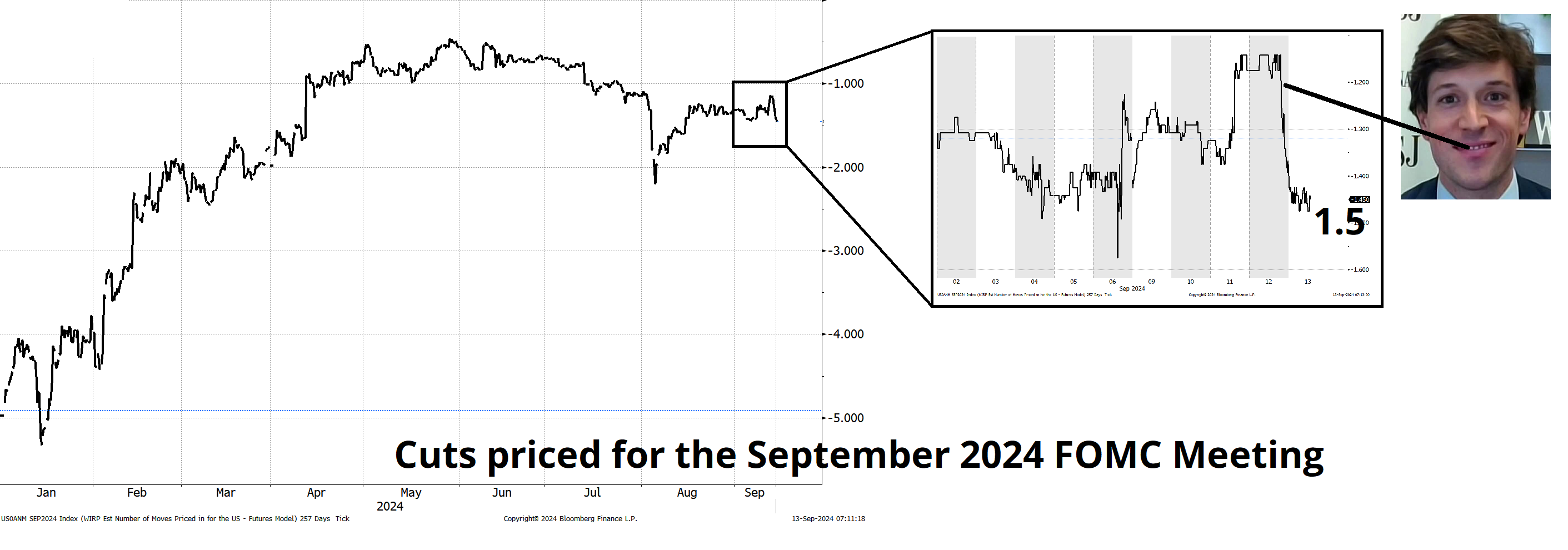

There is quite a lot of chicanery this week as the market suddenly realized… Right around 10:55 a.m. NY on Wednesday… That the world isn’t ending because of a 0.1 topside miss on one of two pieces of the CPI reading.

Then Thursday things got REALLY interesting as Nick Timiraos (who is presumed by many to be the Fed’s not-so-secret rates whisperer) came out with an article detailing why the first cut is a coin toss, not a 25bp sure thing. The FT then followed with an article that looked like a GPT-4 remix of the WSJ article.

Line going lower = more rate cuts

The most interesting aspect of this, of course, is that it means next week’s meeting is in play. It’s 45/55 or something. Another titillating aspect is that it will offer us another clue as to whether or not the Fed is leaking analysis and information to the public in contravention of its own blackout policy which says:

During each blackout period, FOMC staff officers as well as staff who have knowledge of information that is related to the previous or upcoming FOMC meeting will refrain from expressing their views or providing analysis to members of the public about current or prospective monetary policy issues.

If the Fed ends up cutting 50bps, this will likely be perceived as another in a long series of unsavory rule-violating Fed stunts following hot on the heels of all the trading scandals and the most recent determination that yet another Fed Governor joined his peers in violating internal rules designed to safeguard the reputation and credibility of the Fed.

Then again, if the Fed goes 25bps, the last 24 hours will just be a strange dream.

May you live in interesting times.

You can make pretty good arguments for both 25 and 50 bps because Fed policy is incredibly tight relative to market pricing right now (cut 50!) but there is no emergency, and inflation is still above target (cut 25!).

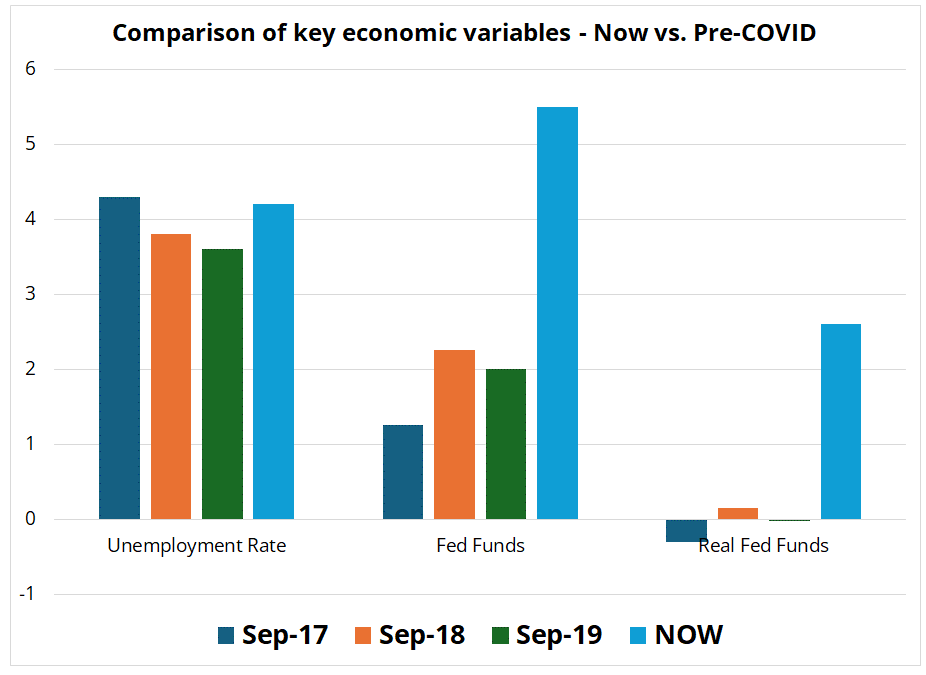

Meanwhile, the current macro backdrop (2.5% growth, 2.5% inflation, trend jobs growth, minimal firing) makes it hard to get excited about recession. In fact, it’s beginning to look a lot like pre-COVID, everywhere you go.

The standout in those charts is that the macro variables all look similar to pre-COVID, but there’s a bit more inflation and monetary policy is in a completely different universe (TIGHTER).

To give you a sense of just how tight policy is right now, here is a chart.

Markets are not always right, but they usually lead the Fed as you can see in this next chart, which shows the two variables separately.

Note how the orange line usually moves before Fed Funds. But not always. As a rule, the market tells the Fed when to cut or hike. Note, though, that there is tremendous circularity because Fed communications influence the 2-year yield and… Bonds trade every day, whereas the FOMC only meet eight times per year. Anyway, the last time Fed Funds was this high above the 2-year yield, this guy was running things.

For a full macro discussion right into your ears… Please check out my fresh new podcast with Alfonso Peccatiello. Recorded yesterday.

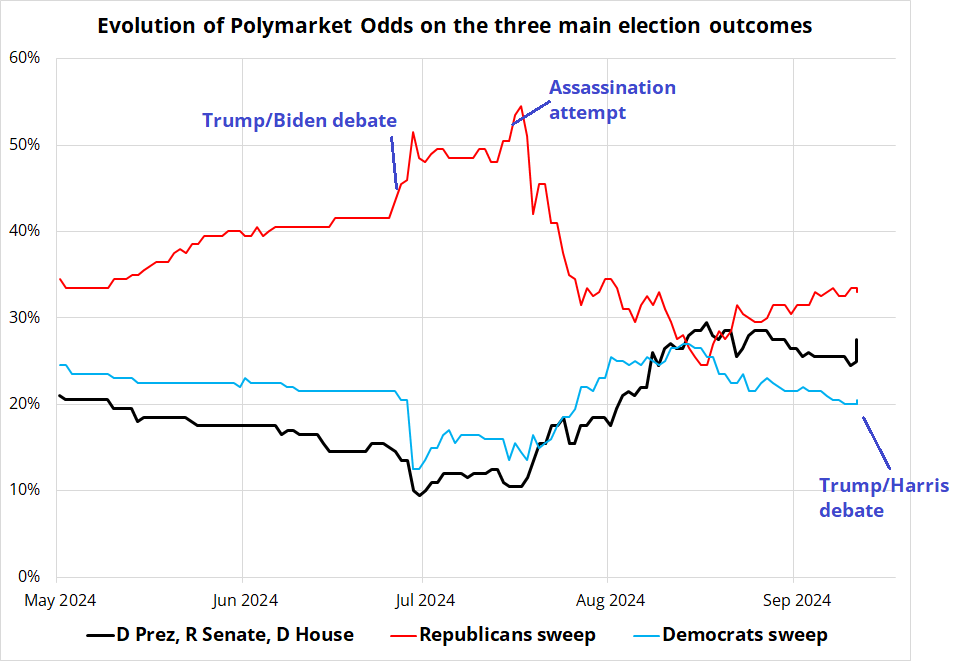

The US Presidential debate has come and gone, and while it led to some excellent memes, it wasn’t particularly market moving.

That’s because the big market moving outcomes are a Red Sweep or a Blue Wave. While Kamala’s victory odds went up a bunch after the debate, the Red and Blue Sweep odds didn’t change much. See here:

Gridlock is status quo. Boring. Sell vol. To unlock a huge move either way in the market, you would need one of the blue or red sweeps to look more highly probable.

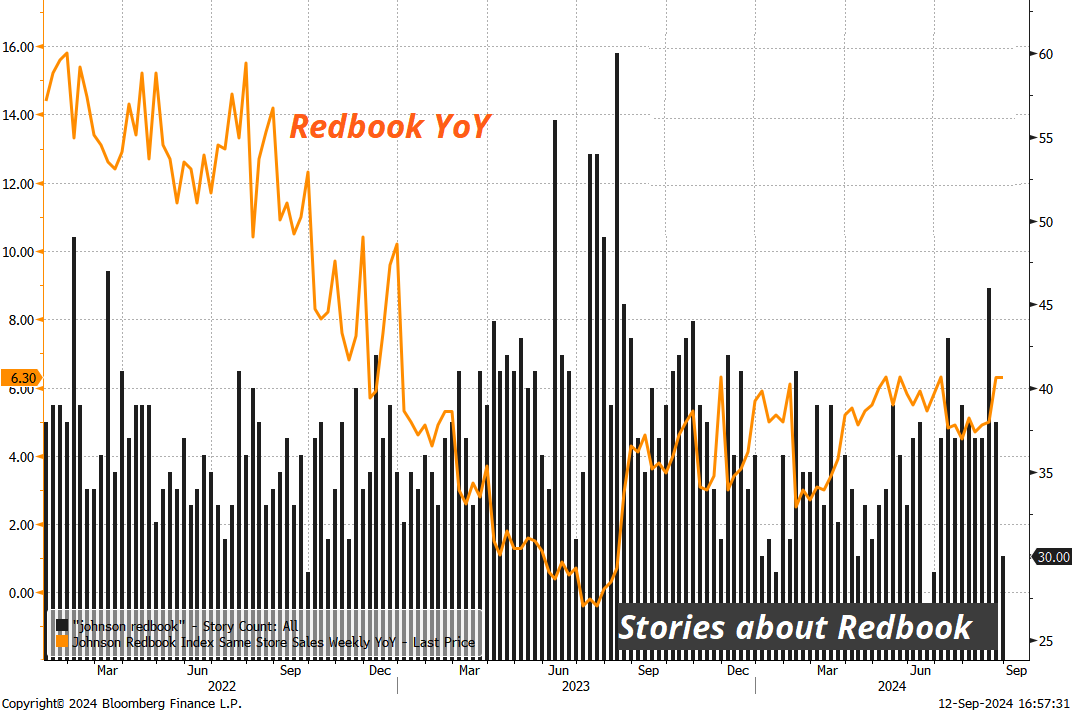

Finally: Have you noticed how you stopped hearing about Johnson Redbook? It’s a useless indicator, but it was heavily touted last year purely because it was weak—and that is how confirmation bias works. Now that it’s showing YoY gains, magically nobody cares about it. The chart I made below shows the number of stories on Bloomberg about Johnson Redbook (black bars) and the data itself (orange line).

Negativity bias is real.

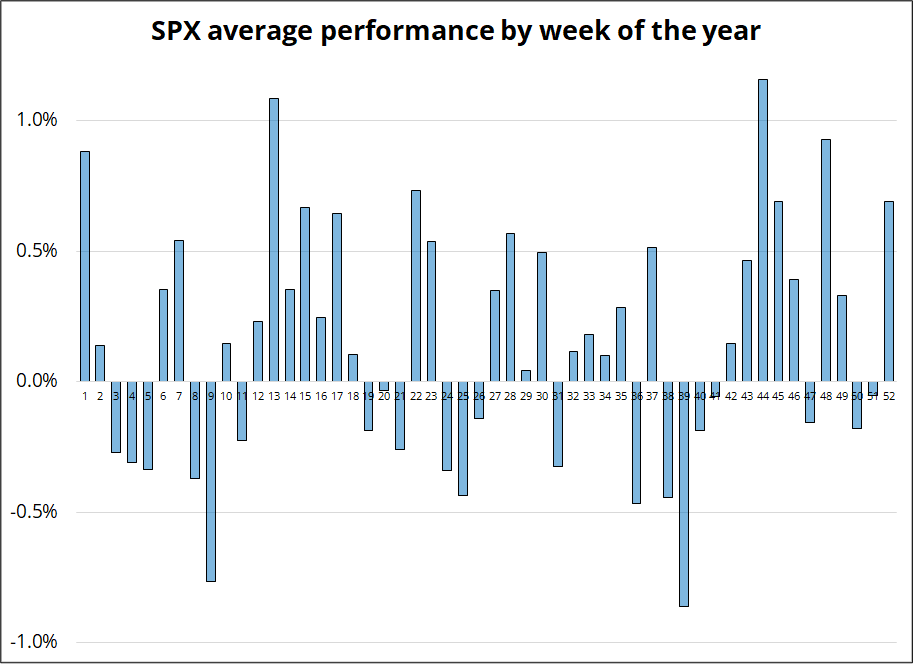

Well, that was quite a Week 37! The only bullish week at this time of year delivered, biggity-bigly, and now we go into the worst period of the year to be long stocks. Interesting how Week 37 served up a win, just like the textbook said it would.

Other than seasonality, I am not completely sure what the bear case is for stocks right now. Whether the Fed goes 25 or 50 feels kind of irrelevant. The US Consumer is fine despite some angst in ALLY and other random stocks like DG and DLTR. In contrast, other consumer-sensitive stocks like WMT and COST are at all-time highs (see next chart). And ALLY competitors like Discover look fine. It’s a mixed bag.

You can cherry-pick whatever anecdote you like on the corporate earnings side, bullish or bearish, but there isn’t much real economic data to support an imminent collapse of the US consumer. Earnings are fine. Consumer Credit is fine. The jobs market is softer than it was during its overheated 2021/2022 run, but still… It’s fine.

Retail Sales next week will be under the microscope as we continue to debate soft landing vs. Godot has arrived.

I suppose a few other boxes you can tick for the bearish equities case (other than the start of uber-negative seasonality next week) are that topside momentum is broken, the charts still don’t look that great (lots of triangular consolidations off the highs), and volatility remains high. Bull markets tend to be grinding affairs with VIX at 12, not 17-VIX seesaw face rippers like we saw this week:

As long as the NASDAQ is below 20,000, you can make some OK technical and tactical arguments for taking a bearish shot with a fairly tight stop now that we have cleansed the shorts.

Here is this week’s 14-word stock market summary:

Week 37 stays true to form and now we enter the danger zone again.

US yields were trending down at a 45-degree angle all through the month of September, until the slightly stronger CPI release allowed them to find a bottom. This, despite Thursday’s media bombs suggesting the FOMC meeting is a tossup. At this point, if you’re long bonds, this is a fair place to take some profits as positive bond market momentum has dissipated on micro timeframes and there is soooooooo much priced in.

We just went from 5.0% to 3.5% on the 10-year. In four months. I don’t think enough has changed in the world to justify much lower yields from here, and the risk now is that we stay in soft landing mode and bonds just chop.

Playing the ”too much is priced in!” game can be career-threatening at times, but it’s been the way to trade successfully for the past two years. Fed expectations have constantly become overcooked in both directions and reversion to the mean has dominated.

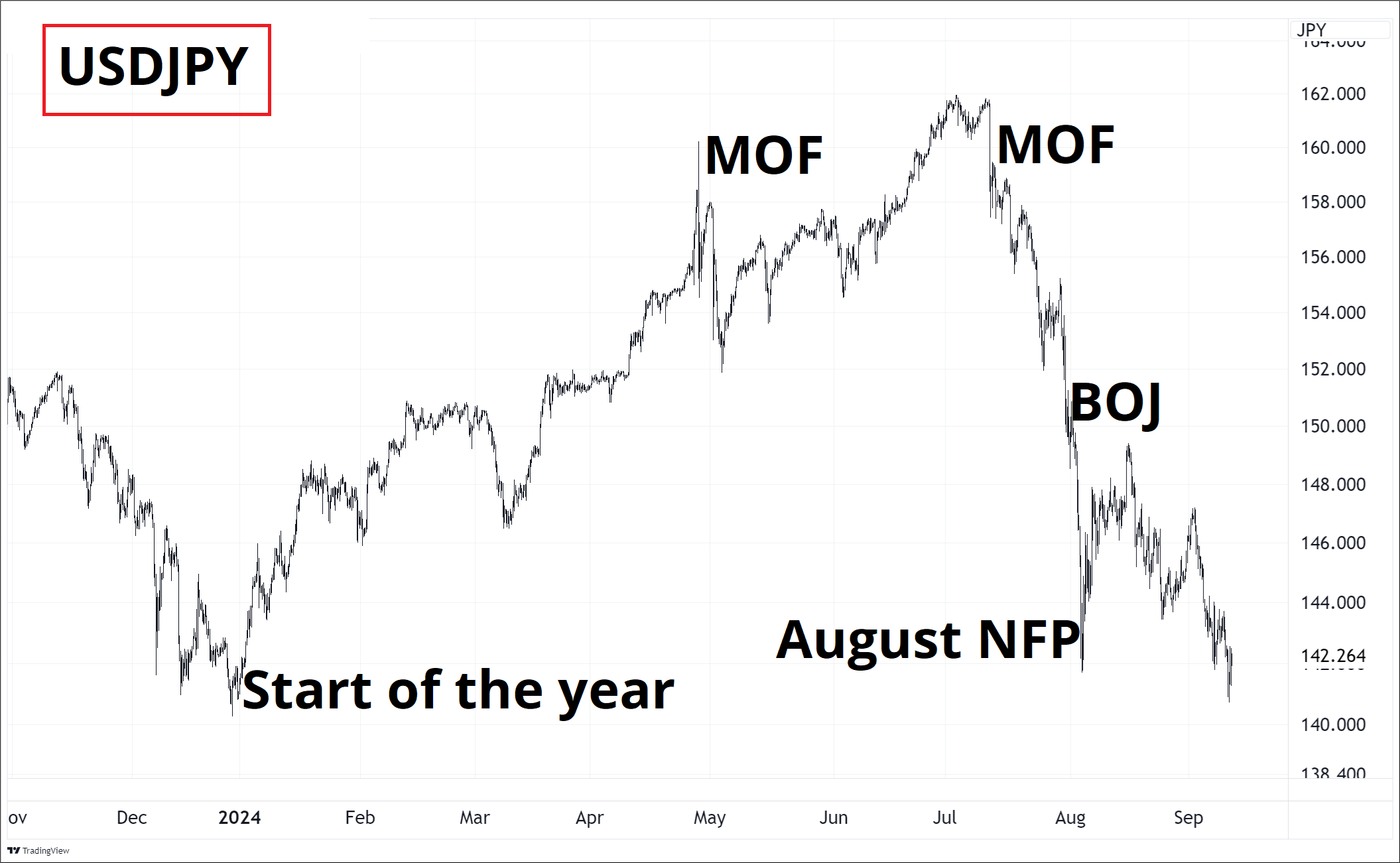

Everybody to the other side of the bus in yen.

You may remember this Friday Speedrun graphic from the peak of the panic when USDJPY was at 160.00.

The two headlines from the graphic…

… Are textbook examples of Betteridge’s Law. Betteridge’s Law states that any headline that ends in a question mark can be answered with “no.” It highlights how sensational or speculative news can often be misleading clickbait.

Here’s how it’s playing out now:

Team Japan wins the gold.

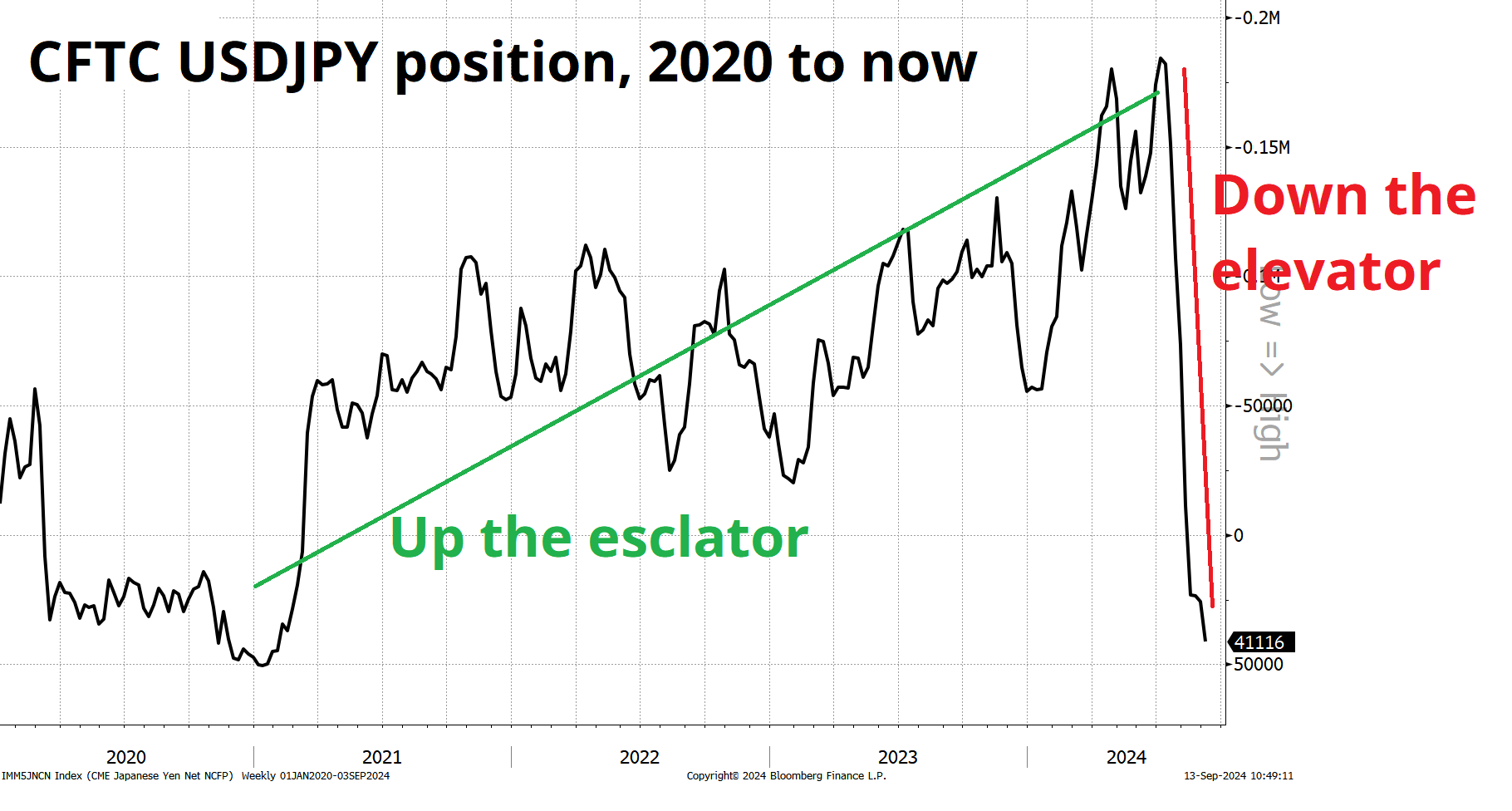

There is a cliché that says carry trades go up the escalator and down the elevator. Like most clichés, it’s true.

Outside of the yen complex, the USD traded weak this week as NickyLeaks leaked and USD longs tweaked and turned meek and safety they seeked*.

*sought

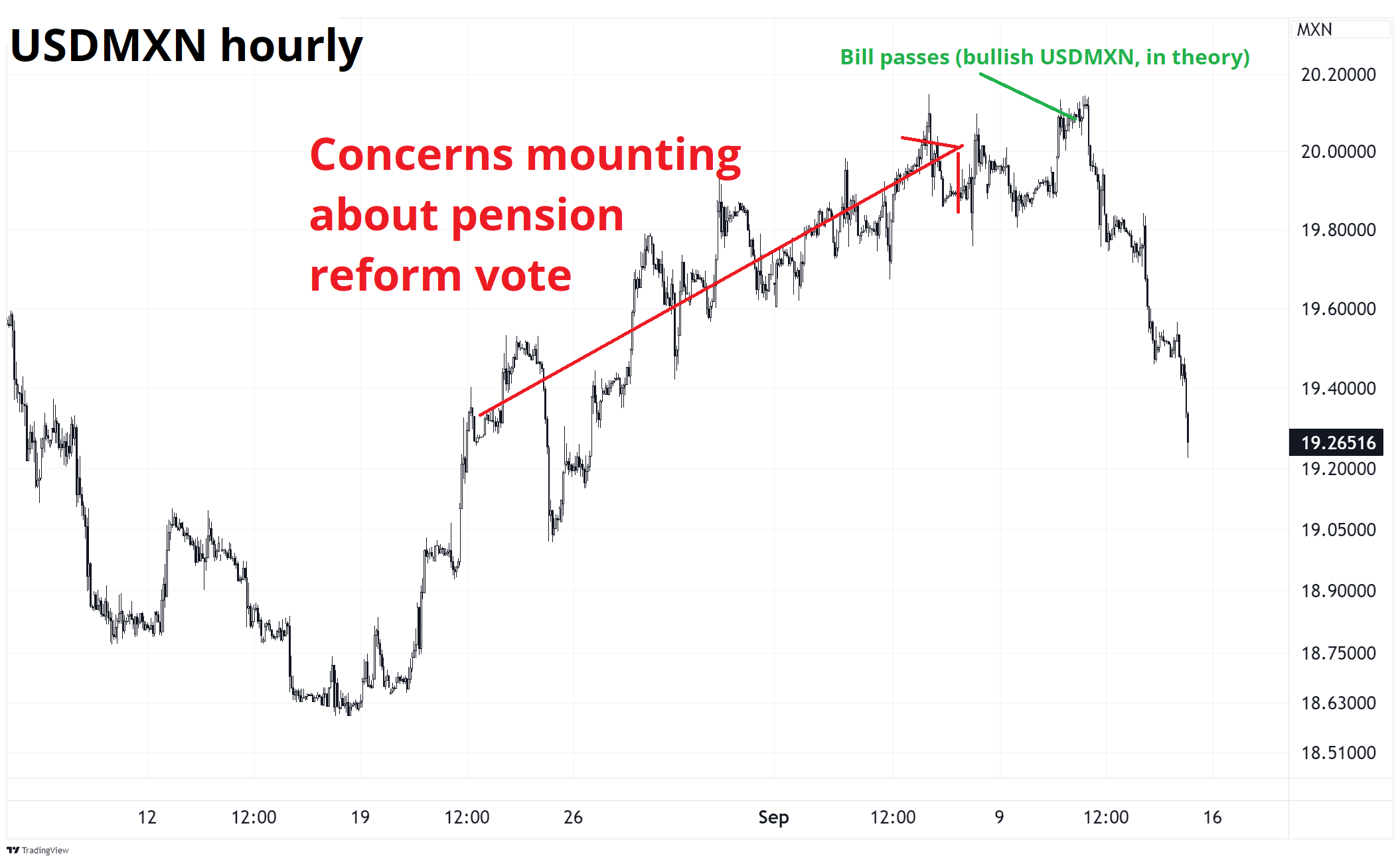

The biggest winner in FX over the past five days has been the Great Mexican peso as the bad news about pension reform has been priced in for weeks and weeks and we saw a textbook buy the rumor / sell the fact pattern. Note that bad news for Mexico makes the following chart go up (because it’s a chart of USDMXN). The bad news came out right at the ding dong high and then: whoosh.

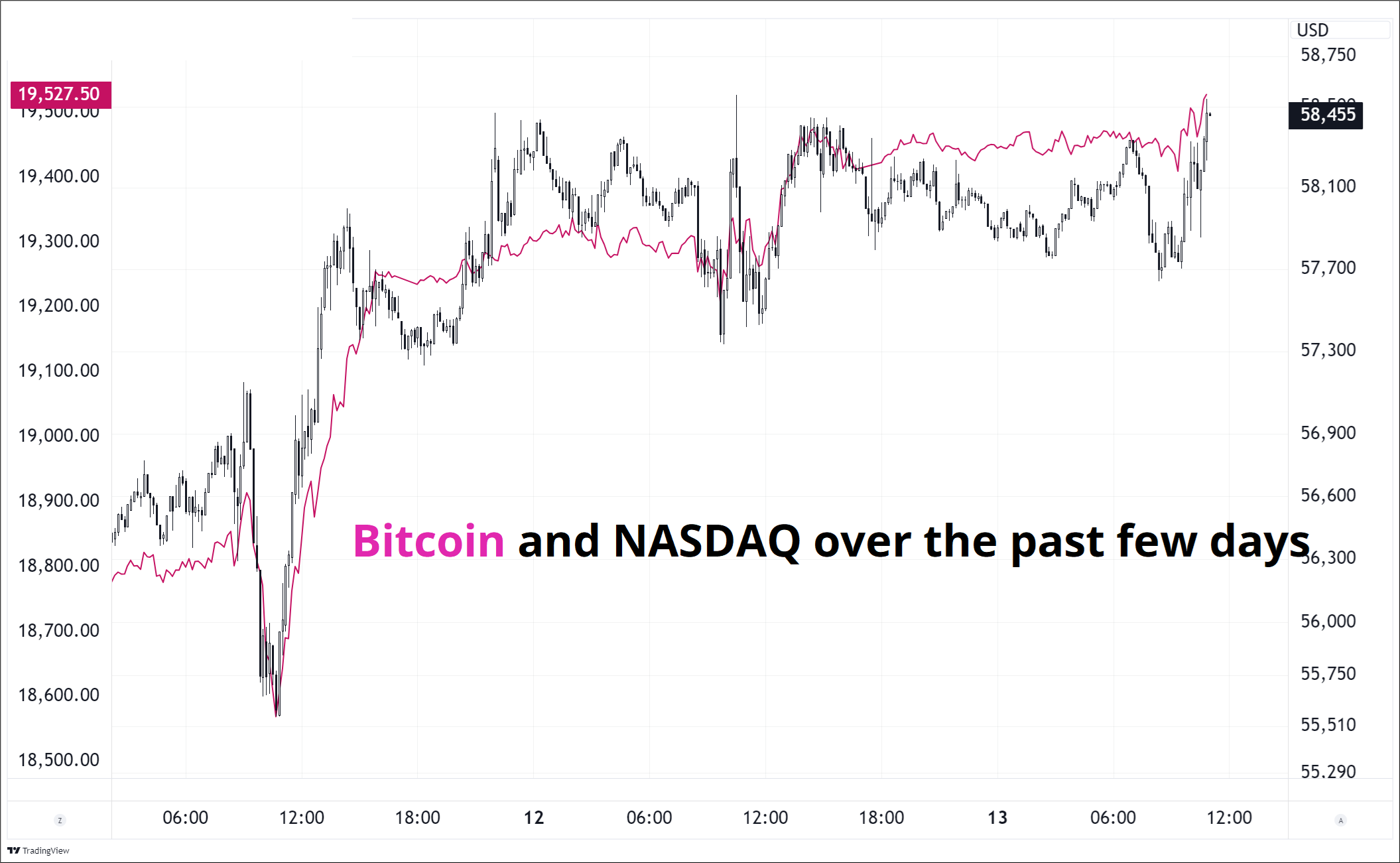

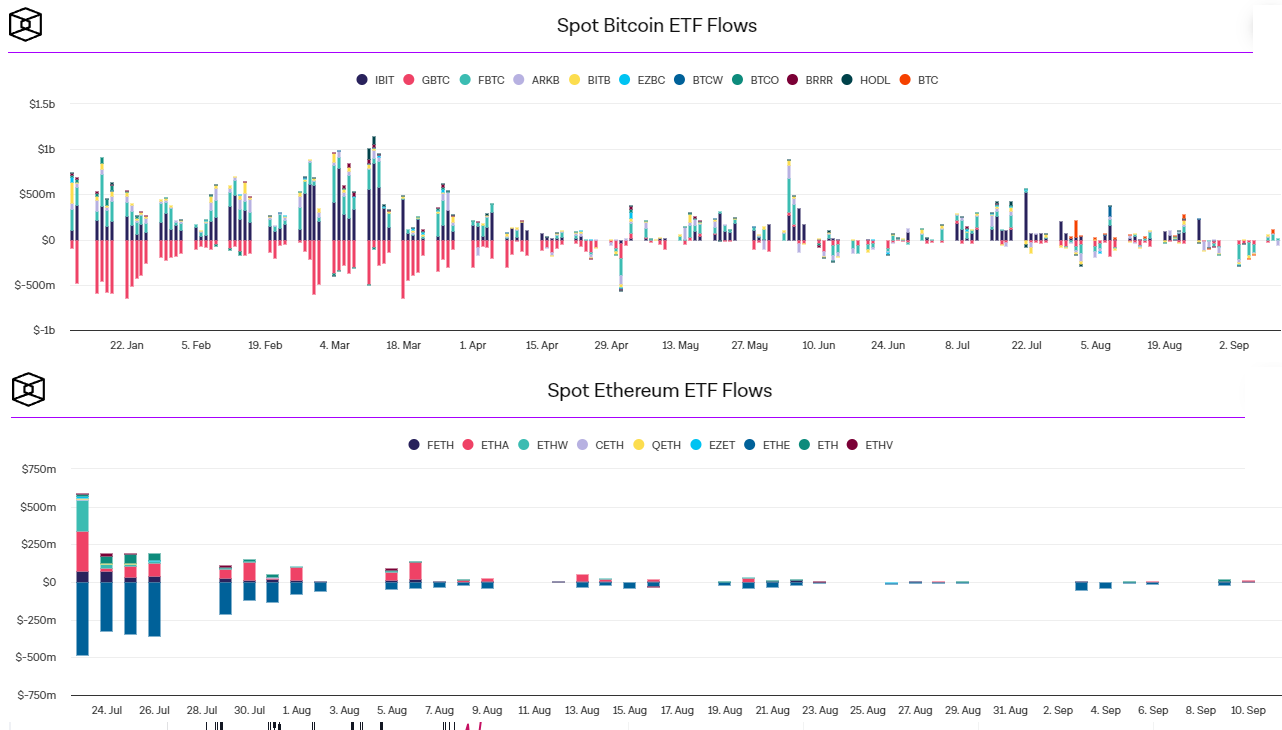

Not much to report on crypto this week as the virtual coins rise in tandem with all other risky assets. Most of the price action in bitcoin looks like high-frequency algorithms and correlation traders just following the general risky asset vibe up and down.

Despite a nice rally off the lows, BTC and ETH ETF flows remain de minimis.

My passive-aggressive ragging on commodities last week was a good behavioral (reverse) indicator as I piled on the injured commodity longs and this week they rose like Lazarus. It must be encouraging for longs to see a massive risky asset rally flow through to commods, because that hasn’t been a persistent thing in 2024.

Then again, you need a fairly up-to-date lens prescription to see the bounce on a daily chart.

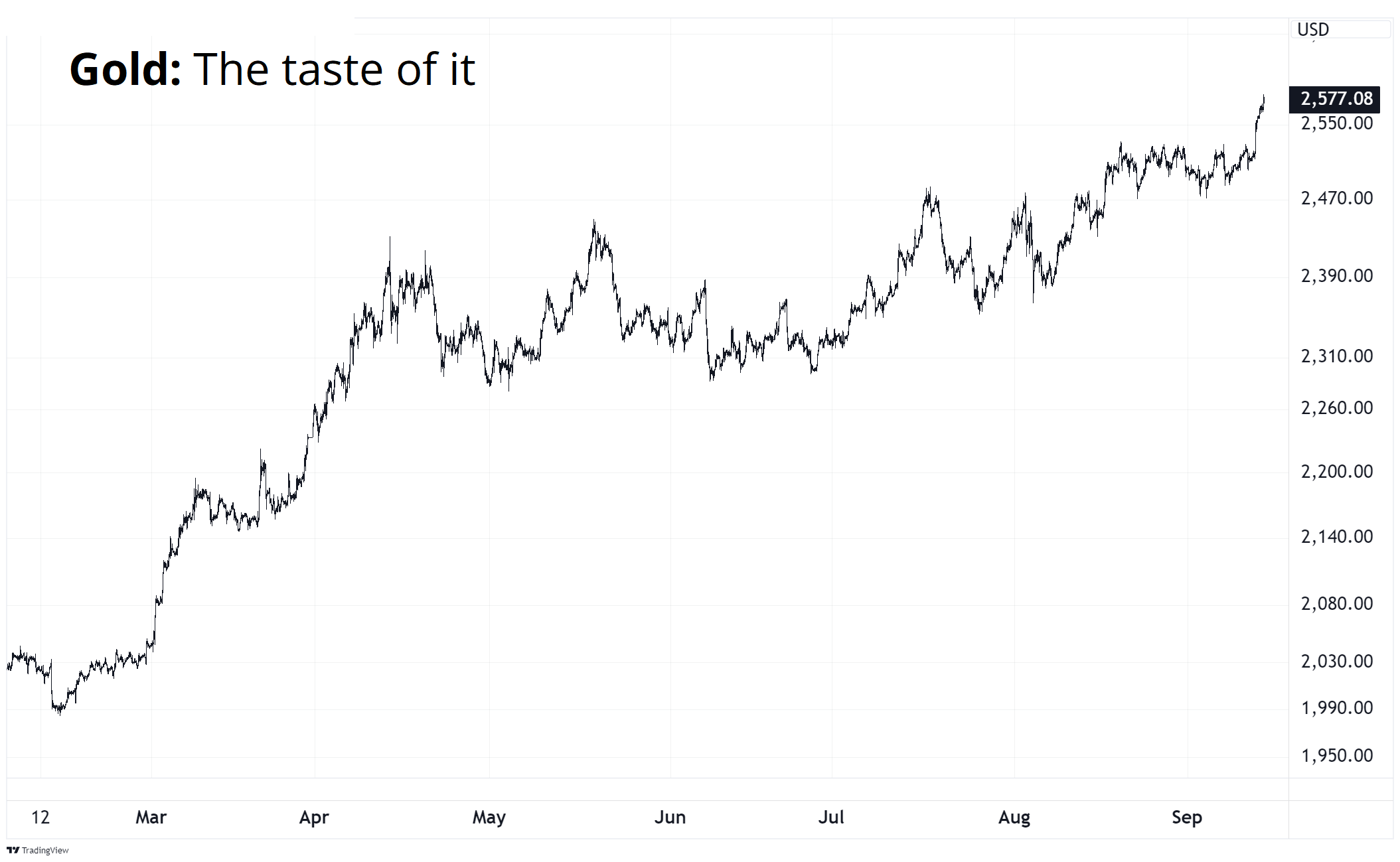

That said, one of the most impressive markets in the world right now is the price of analog bitcoin. Also known as gold. China stopped buying a while ago, ETFs aren’t buying much, early September is a bad seasonal period, most commodities are in the toilet, the USD isn’t all that volatile to the downside, US real rates are +1.6%, gold is negative carry and yet. Here we are. I suppose we just blame the deficits!

Whew! OK! That was 8.14 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

Smart, interesting, or funny

Why AI isn’t going to make art

Ted Chiang is a great writer and he knows a lot about technology and futurism.

Like many AI tools, this is fun to play with. Not sure it’s useful. But it’s fun to play with!

A well-written and angsty long-form Twitter post

5-minute read. References DFW, Nirvana, and angst.

Music

The song is called: “just stand there” by Fred Again.

Listen on Spotify. On YouTube. The lyrics.

Poetry is not dead in 2024; it just has musical accompaniment.

Speaking about his new album “ten days”, Fred says: “these are ten songs about ten days. theres been a lot of BIG mad crazy moments in the last year but i realised that almost all the ones that i was most sorta shaped by were the really very small quiet intimate moments. some of them are like the most intensely joyful things ive ever felt, and some of them are not that.”

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.