A quick story, then the normal FSR

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

A quick story, then the normal FSR

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

I like to start my books with quick war stories from real life trading because they are fun and because I always remember how Raiders of the Lost Ark started with a really exciting moment right away and that is a cool way to start any work of “art” whether it’s fiction or nonfiction. No boring rolling credits or character backstory and such. Action out of the gate.

I have a good trading story to tell, but my latest book has been sent for proofreading and layout, so it’s too late to put it in there.

So, I will tell the story here. When my kids were younger, they used to love to read Prima guides for games on the Nintendo Wii. The guides provide detailed walkthroughs for each level of the game and offer specific steps you can take to clear each level.

This story is a walkthrough in that spirit, with a high level of detail.

I want to note that I made a lot of money in this story, but there are tales in my new book about large losses, too. The point isn’t to flex, it’s to entertain and teach some useful lessons. If it comes across as a flex, I apologize and I hope that people who know me will understand that I get excited about trading and like telling trading stories (win or lose) and so that’s what I do. And if all the gory details are omitted, the story does not ring as true, so I like to include the real details.

I have traded account sizes of $40,000, $400,000, and $400 million and I wasn’t a better or cooler person because my account was bigger or smaller. I have just as much respect for a small retail trader grinding consistent gains as I do for a hedge fund PM that puts up numbers every year.

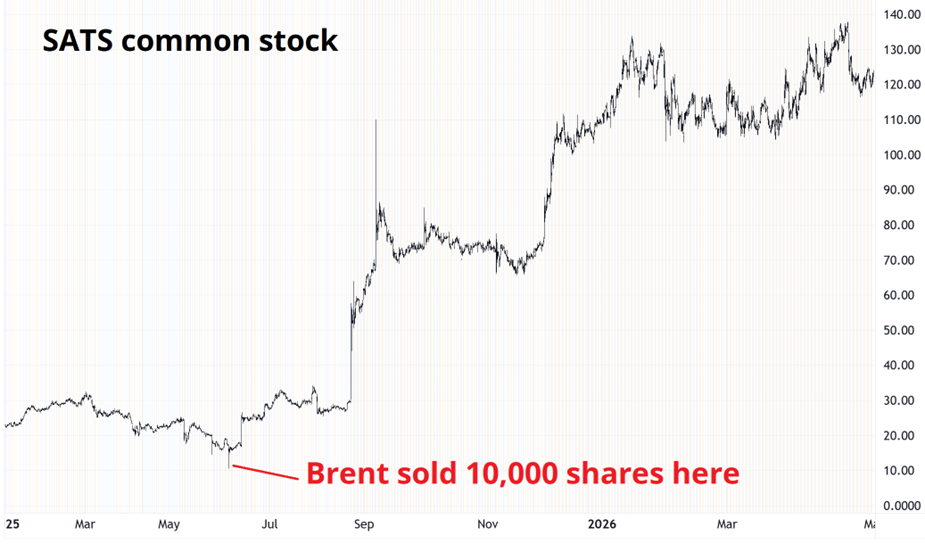

And for the record, one of the stories in my new book is about how I sold SATS below $11 post-market not too long ago, even though it has never really traded below $15 and is currently $125.

If you wanna know how that happened; you will have to buy the book! It is called Alpha Trader 2: Outside the Box and it comes out sometime in late May or early June, depending on how long the indexing lady takes. And no, I’m not still short SATS lol.

OK. I am intrigued by short squeezes and retail bubbles and always attracted to them much as mosquitoes are attracted to those electric zappy machines on your patio. I have had some success fading these microbubbles, and I am increasingly a fan of selling call spreads on the stupid r/wallstreetbets rallies in junk like OPEN, KSS, DNUT, etc. That is a good way to sell a high implied vol with limited downside. But you don’t get a ton of leverage doing that, so I usually short the stock outright as well. Always with a predetermined stop loss and set amount of $ at risk.

As Avis started to rally in April, I became intrigued. There are many boring and technical reasons for the Avis short squeeze, but basically it’s a low-float stock where a fund or two control a major portion of the float and so liquidity is poor. The business is a turd legacy business and so there should not be much upside for the stock and thus it’s heavily shorted.

After the March expiry, the float got smaller and Avis (Ticker: CAR) started to rally. Unlike the insta-short squeeze in CAR in 2021, this thing was a slow burner. It looked a lot like the 2017/2018 Bill Hwang squeeze in WB and had some of the same characteristics (total return swaps causing massive short gamma, etc.)

When I fade a bubble like Avis, I have extremely high conviction that it will do a round trip, but I also know that there is a pretty good chance it will do a round trip and I will still lose money. Shorting these moves is incredibly difficult to risk manage because there is no limit to how high the stock can go. I have a whole chapter in Alpha Trader 2 about why shorting is the hardest game to play—everything is stacked against you. But it’s still worthwhile at times.

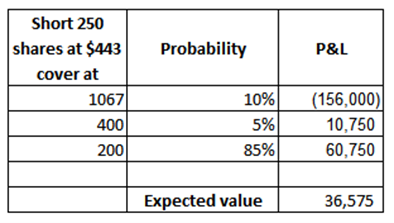

I decided this was a high conviction trade and I was going to risk $200,000 on it. The math is insane when you do this stuff because if you sell at $443 like I did, and you figure worst case scenario is you stop out above $1000, a position of 250 shares is risking $156,000. So I sold 250 shares at $443, leaving me a budget of $44,000 for whatever other structures.

My target was a return to the $200 area, so it might seem odd to risk $600 to make $200. But I saw the EV as positive because I felt a stop above $1000 was far enough away that the expected value looked something like this:

Expected value is weighted average of all outcomes

I had already lost $18,000 selling a $350/$355 call spread the week earlier, but my conviction was getting higher because the price had now quadrupled, we were nearing the old high of $550 (2021 bubble spike high) and the major April options expiry had passed (17APR). Since March options created the start of the short squeeze shenanigans, I didn’t really want to get fully involved until April options had expired.

So I went short 250 shares at $443 on Friday, April 17, risking $156,000.

Then, bum-clenching time. I will show a chart later, but for now just know that Monday, April 20, the stock rallied. Again. Early in the day, with the stock at $550, I sold a $400/$405 call spread, collecting $3 for a $5 spread. I did 75 contracts and received $22,500. Worst case, on this structure, you lose $15,000. That is (($5 – $3) X 7500). Best case, the stock collapses and you make $22,500. Not very exciting leverage but another structure to have on just to vary it up.

Later that day, with the stock trading around $590, I took a peek at the options market and was surprised to see that the Friday $400 puts were only $9. Sure, in implied vol terms, that was stupidly high, but my view was that if/when the stock cracks, it’s going right back to $200 or lower. So, I bought 15 of those for $13,500 or so ($9 X 15 X 100). These two tack-on trades provided me some excellent insurance in case I got stopped out of the short position and the stock collapsed right after. It’s a good psychological hedge and also good EV to have various structures.

The way you structure a trade can determine whether you make money or not and help solve the “I was right and I lost money” problem. Outright shorts can get stopped out while options can survive. But if the stock goes nowhere, options are expensive. And if it goes down slowly, you are correct and you lose money on the options while you make money in cash. By attacking a trade with various structures, you reduce the path dependency of your P&L.

Pre-market on Tuesday (April 21) the stock took out $700, and I was feeling rather jejune. It chopped around for most of the main session, then started grinding towards $750 post-market. On Wednesday morning, we were trading $820/$840 just before the open and I was down about $100,000. I had my automatic stop loss loaded at $1067.

There are many risks to automated stop losses in thin stocks, but the risk of blowing up is the risk that is most important to mitigate. When a trade gets to my stop: I get out. If that happens, I will almost certainly miss the inevitable collapse because it’s too expensive to keep stopping out and getting back in. But without a stop, you’re risking your entire account on one trade, which is stupid. CAR could go to $2,000 or $10,000 if it wants. There is literally no limit. GME went from $5 to $500. Avis could go from $200 to $20,000. You never know.

So, I am white knuckling the pre-market action and then the regular hours trading on Wednesday the 22nd of April brought some relief. The stock went down in pretty much a straight line, TWAP style, all day and closed at $420. Price cut in half from the previous pre-market high. Zippy.

Fortunately, the next day (Thursday, April 23) I was travelling and my wife really hates when I trade when we’re together. So I only checked the market while in the bathroom at rest stops on the drive up to Canada. Almost every time I checked, the stock was halted and it was in free fall. If I was at my desk, I probably would have taken some profit way too early. But since I was not at the desk, I stuck to my plan which was to cover everything near $212. Right before I left for my trip that morning, I published this in am/FX.

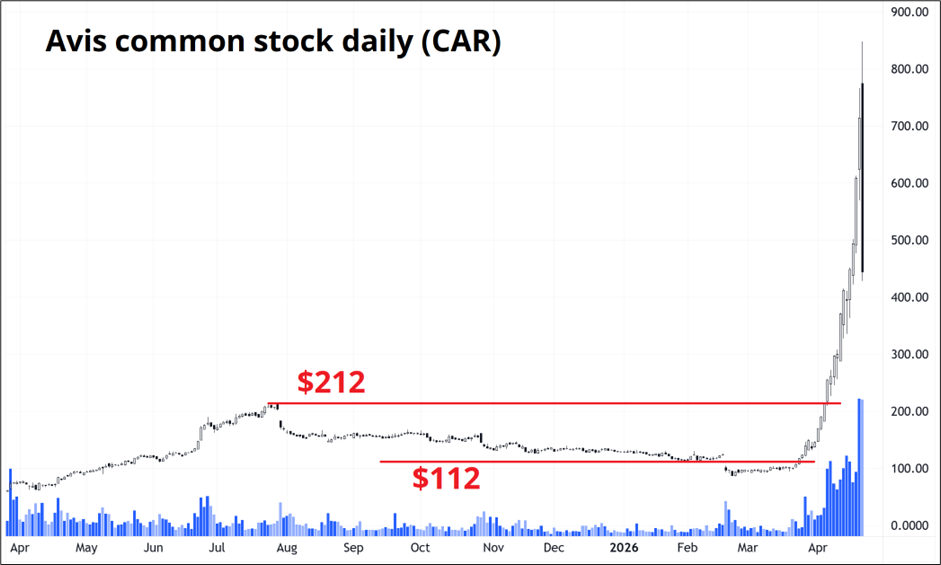

AVIS

If you are trading this bringer of tears, the big supports are the old 2025 high ($212) and the important $112 pre-short-squeeze pivot from Q1 2026. This Avis short squeeze will go down in history along with Porsche/VW, Bill Hwang WB, and GME 2021. And Avis 2021 ofc lol. Note those dollar volume numbers are completely insane as the stock traded 20X normal volume with the stock price up 800%.

The next time we pulled over and got Burger King, the stock was $215 and so I sold the 15 puts for $185 each. I had left a bid earlier to buy the cash position back way higher ($383) because once the stock took out $400, my puts were ITM and so the cash position became an irrelevant part of my risk.

Net, the cash position made barely anything (~$10k) because I covered it close to $400, the second call spread netted $22,500 and the puts yielded $264,000. I did one more trade selling 1000 shares at $198 on April 27 and simultaneously selling ten 01MAY $185 puts to collect another $14,000 of premium. I will probably get exercised on the puts so that’s an extra $27,000.

I did that last trade because once a bubble pops, vol stays too high for a while even though the likely result after the collapse is a boring consolidation. You saw that in silver and you see it many burst bubbles. They chop around and go nowhere once the dust settles but IV sometimes hangs around too high for a couple of days due to burnt fingers in the options market.

All in, this was an outstanding trade and the funny thing about it was that the puts, which were a bit of a side bet at the time, generated about 85% of the P&L. The lesson is not to buy puts on bubble stocks. The lesson is that using various structures in the same trade can give you more staying power and let you make more money in a wider range of scenarios. I don’t buy puts very often. I usually short outright with a stop loss because more often than not, buying puts is a waste of money. This was a huge exception.

Takeaways:

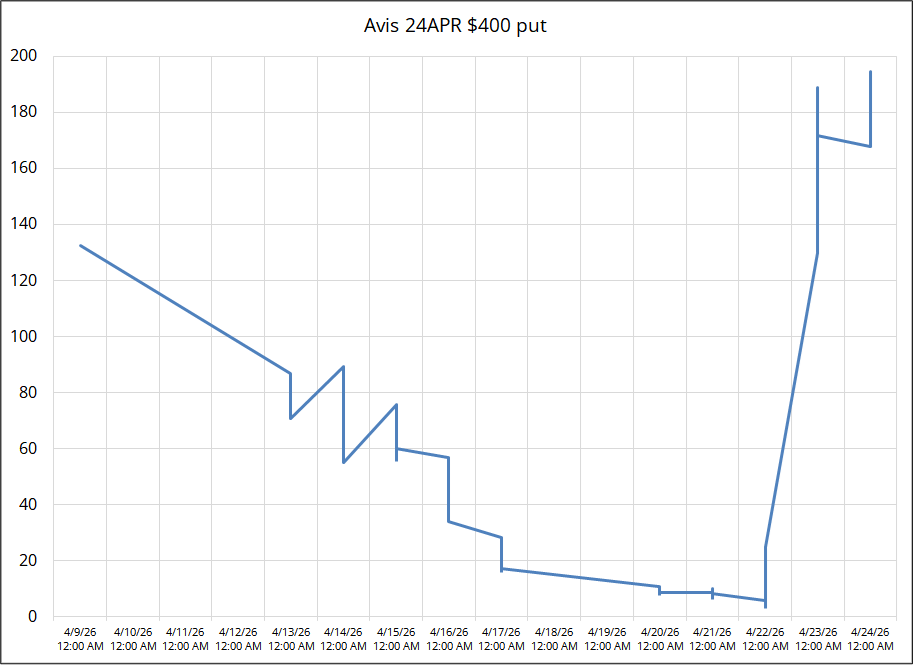

Here’s a graphical summary of the whole thing:

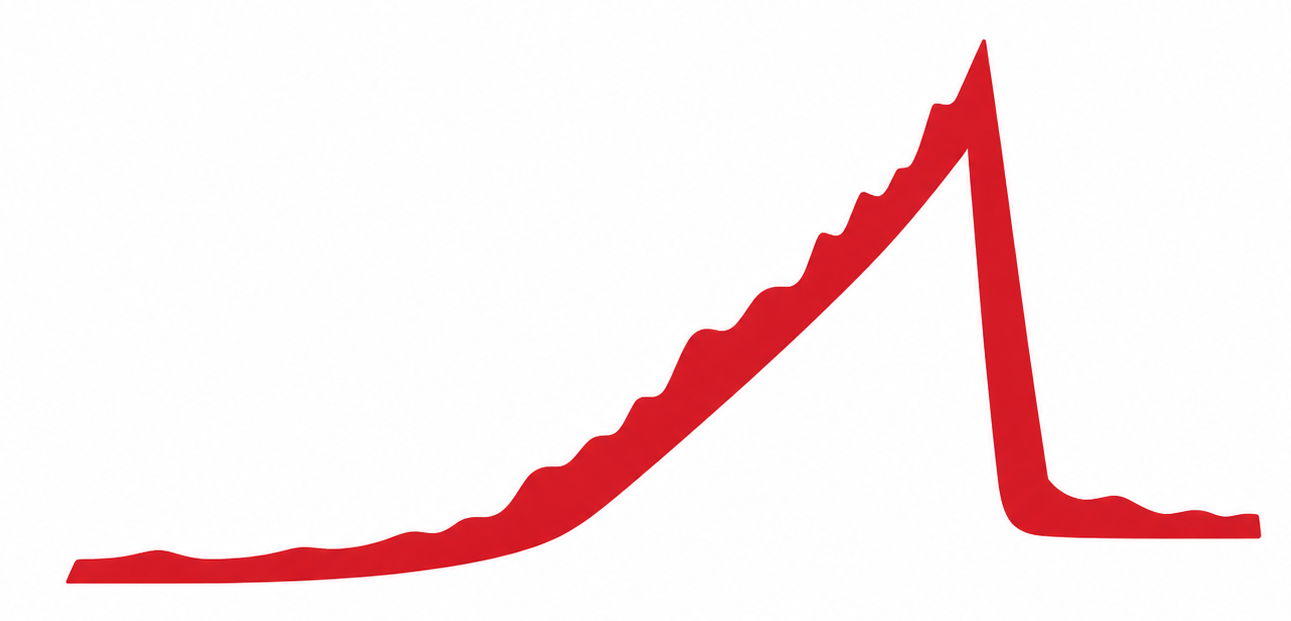

The price of the $400 puts went like this (very thinly traded hence the weird chart):

Ok, that’s my story. Let’s do the normal Friday Speedrun thing now.

As discussed in the last Friday Speedrun, the world is still more worried about the shortage of generative AI tokens than it is worried about the shortage of crude oil. The four-week war is entering week ten and still the predictions of a supply shock have not come true. This could still be a timing thing, but each week that passes without shortages or any real evidence of a supply shock puts the burden of proof more and more on the bears. The world continues to spin, tilted at approximately 23.5 degrees relative to its orbital plane around the Sun, despite the most-calamitous possible outcome (SoH closure).

The war in Iran is barely front-page news at this point, as there are few developments and it’s a stalemate with both Iran and the U.S. claiming to be in control of the Strait. Or “Straits” as some say.

It bugs me when people say “Straits of Hormuz” because there’s only one, but apparently both forms are correct, and the plural is just a quirk of English usage. Historically, English often used “straits” as a singular concept, the way we still say “in dire straits” or talk about “the Straits of Gibraltar,” “Straits of Dover,” “Straits of Malacca,” and “Straits of Magellan.” It comes from the Old French estreit (narrow), and the plural form became conventional for naming these narrow sea passages, possibly because a strait often has multiple channels, narrow points, or shipping lanes. The Strait of Hormuz, for instance, has separate inbound and outbound traffic lanes.

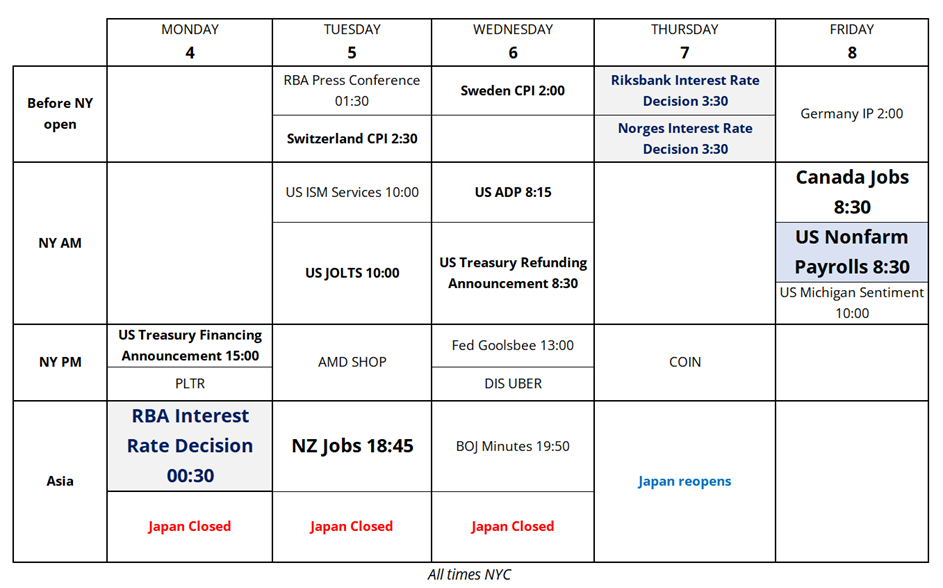

Anyhoo. The calendar next week is interesting because we are going to be caring about economic data for the first time in ages. There seems to be some evidence that the U.S. jobs market is strengthening (see Initial Claims, ADP Weekly data, etc.) and while the market is extremely shy about pricing rate hikes for the U.S.A., it could happen. The ECB and many other central banks are in hike mode and there has to be a point where the Fed blinks.

3% inflation and 4% unemployment and they have been cutting. Fed policy is increasingly difficult to predict because they have abandoned their inflation mandate with five-plus years above the target and nary a flinch from the committee.

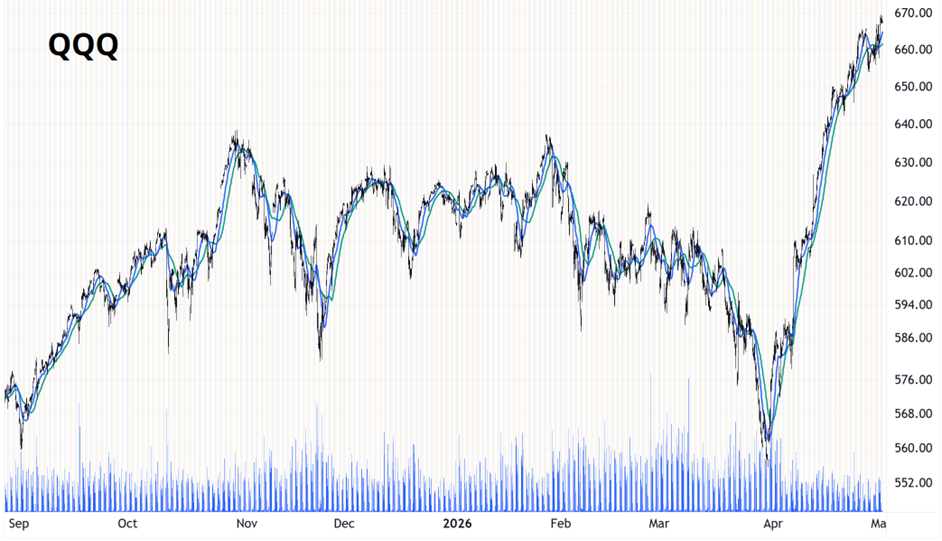

The bulls are in control and the U.S. tech trade is back although stock price performance post-earnings this week was mixed. META dumped, GOOG ripped, and AAPL is looking pretty okay as the market assesses which companies will win the AI Capex madness and which will lose. The size of the capex spending in the U.S. (especially compared to China, where similar AI outcomes are being realized) is an evergreen concern and if you read too much Ed Zitron you might be inclined to trade from the short side all the way up. To me, it’s a good trader’s market because there are many idiosyncratic single stock moves and you can trade Russell as a completely different product than QQQ.

The chart of QQQ says it all. America is so back.

Here is this week’s 14-word stock market summary:

We are back in a VIX 17, new all-time highs market. Trade accordingly.

https://www.spectramarkets.com/subscribe/

The ECB is set to hike in June and most of the central banks look like they are priced reasonably. The Fed has nothing priced in for the next year, which also makes sense because they probably should be hiking but that side of the distribution is still truncated for now. We will see how Warsh tries to steer the committee. To me, he’s a continuation of the orthodox, mainstream policy approach that Powell followed and while it’s fun to talk about balance sheet reduction, it’s also fun to talk about deficit reduction. Neither are happening.

U.S. yields are remarkably stable.

While many global yields have made new highs.

My view has been that there are offsetting forces in the dollar and therefore it should not move too much. I wrote about that in the last Friday Speedrun and most major G10 pairs are close to unchanged since then.

Interest rate differentials are pushing down on the dollar, but U.S. tech exceptionalism and economic outperformance are supporting it. The impact of the energy market moves is hurting Europe while it helps the U.S. In fact, NG in the United States is down since the start of the war, for example. All this push and pull means the USD is just kind of fluttering around in the wind.

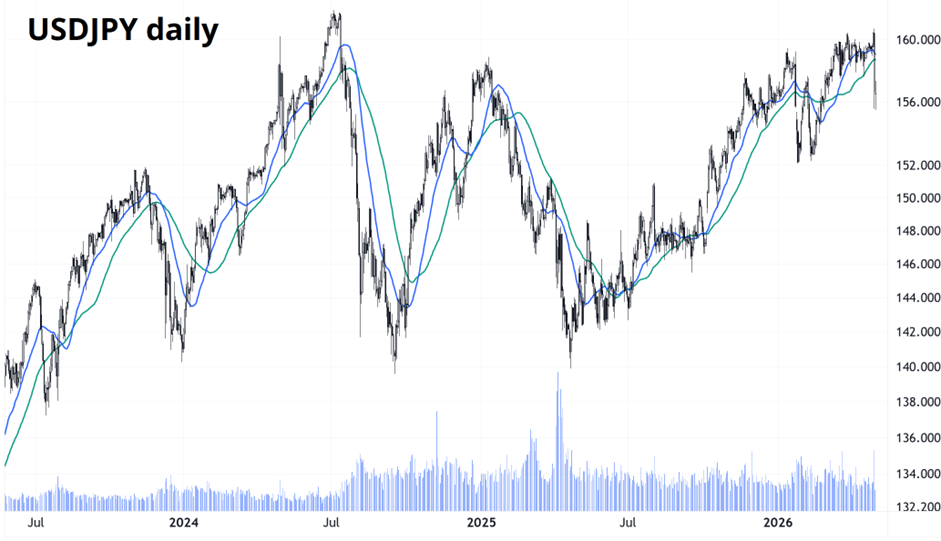

The big exception is USDJPY, which was hammered by the MOF yesterday. They have been the boy who cried wolf for months, but the break of 160.00 finally triggered a final warning, then a hammer drop.

Then again, for perspective, this is the daily chart.

So the battle will continue. Ultimately, the price of oil is the primary determinant of the JPY these days, so this intervention buys some time until oil prices come back off. If oil goes to $200, the MOF is going to have a big problem, but the nature of intervention is not to turn the market instantly, it’s to stop the momentum and allow time for an organic macro reversal.

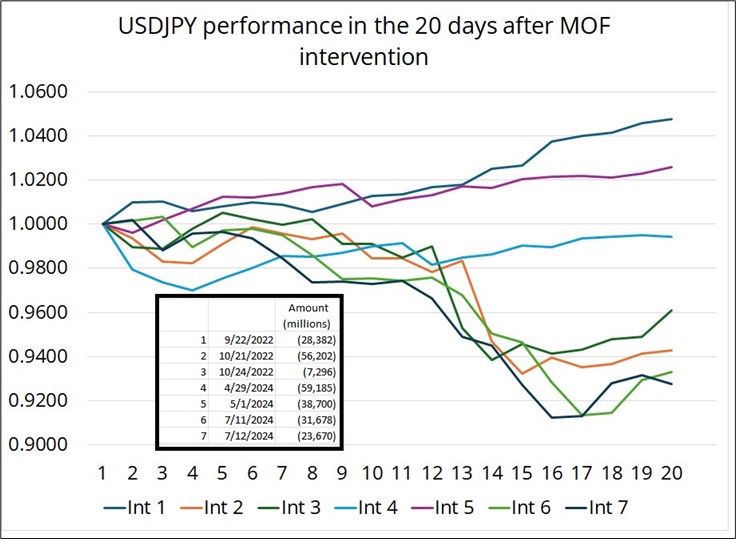

I generally respect the direction of the MOF. They have many tools, including the BOJ policy rate at their disposal. Here’s how USDJPY has traded in the 20 days after past interventions:

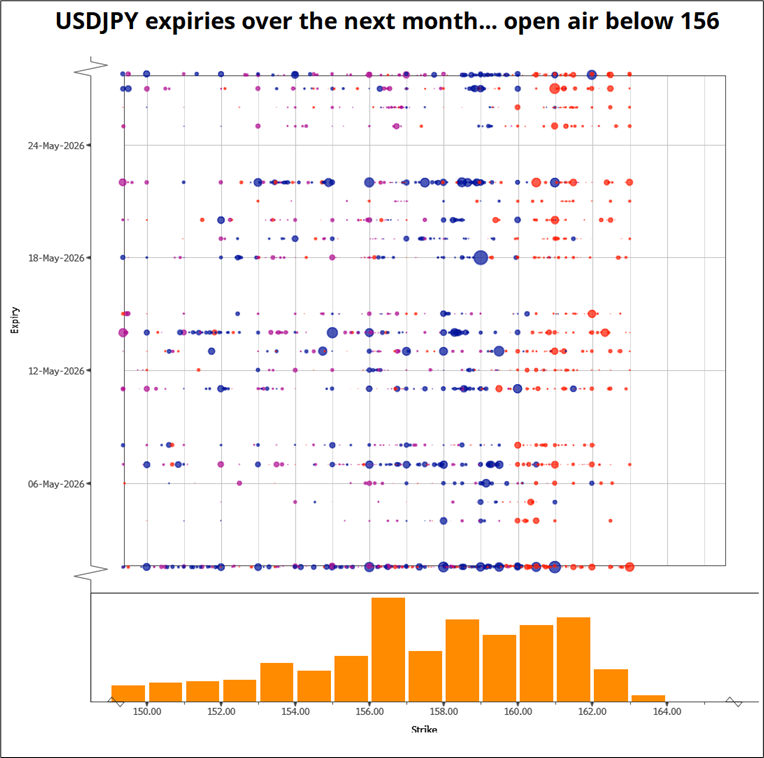

And note how there are very few strikes in the USDJPY options market once you get below 155.00. That makes it easier for USDJPY to accelerate lower if it can take out 155/156.

Someone tell me what to get excited about in crypto because I’m not sure.

The news flow out of the Middle East has not been great and the Straits of Hormuz remains shut. While front month Brent took out the early March highs right before it expired, most contracts remain below their early-March highs.

And the ultimate contrarian signal dropped this week:

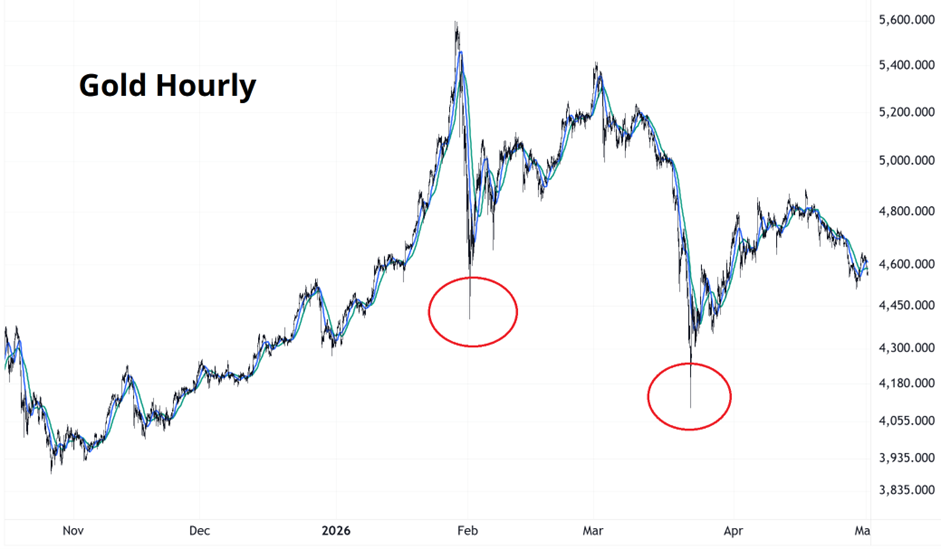

Gold and silver have lost their mojo as retail ruined them both for the time being. Those two blowoff bottoms in gold look to me like retail stop outs and so my guess is that positioning is pretty clean at this point and we are basing for an eventual retest of the 5500 area. It probably makes sense to start accumulating in the 4350/4450 zone if we get back down there.

That’s it for this week.

Get rich or have fun trying.

*************

Seether by Veruca Salt

*************

Waitress by Live

*************

Schism by TOOL

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.