Everyone is all in on the post-Trump Free Money trades.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Everyone is all in on the post-Trump Free Money trades.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Try Spectra School for free!

If you’re looking for a good way to spend 35 minutes or so, check out Lesson 3 of our flagship course “Think Like a Market Professional” for free. https://spectramarkets.com/lessons/tlmp3/ There, you will find the entirety of Lesson 3, for free, along with a link to my Learning From Legends video with Ben Hunt.

The lesson is called “Surfing the Narrative Cycle” and delves into how you can understand the stories the market is telling itself. If you like it, you can sign up for the full course and use coupon code LESSON3 for $250 off the $1200 price (i.e., you pay $950 for 16 lessons and 10+ videos.)

Markets are frothy. Positioning in equity markets is extreme as institutions and individuals are now all-in long stocks for the second coming of Donald Trump. There is much to like on tax cuts and deregulation, in theory, but trade wars are not guaranteed to make stocks go up as we saw in 2018. Down years don’t happen very often in the stock market, but 2018 was one of them as a hawkish Fed and hawkish trade policy combined to send the SPX lower.

Since Alan Greenspan installed the Fed Put in 1987, the stock market is up 74% of all years. This contrasts with the pre-Put era (1928 to 1987) when stocks were only up 64% of the time. Anyway, a tight Fed and trade wars are not 100% guaranteed to unlock a higher stock market when valuations are already frothy. I will get more into the equity market situation in the section on stocks.

Meanwhile, the D.O.G.E. is hoping to unlock huge productivity gains by cutting government spending by $2T. For context, current discretionary spending is $1.7T. The idea that two consultants named to head a new non-governmental agency are going to find cuts that will reduce discretionary spending by 117% feels incredibly far-fetched to me. As I wrote in am/FX today:

A random question that popped into my head last night: What’s the over/under on Musk staying with this D.O.G.E. project? That is, will Trump fire Musk, or will Musk quit before, say mid-2025? The idea of bringing in two outside consultants to reduce government spending by $2T when discretionary spending is $1.7T is super fun but might run into a few real-life roadblocks as reality hits. Just something to think about as “Musk Fired” would probably be a 30% one-day hit for TSLA stock and DOGE. Much as mass deportation had populist appeal but never happened in the first Trump administration due to its near logistical impossibility, this consulting effort will face similar implementation hurdles.

While I am in favor of reducing the size of government, this does not seem like a serious initiative to me and my bet would be Musk gets bored of Trump or Trump gets bored of Musk as their battle to out-shenanigan each other wears thin sooner rather than later. I don’t doubt Musk’s genius, but I do doubt this particular initiative will amount to anything other than some funny memes.

Big ideas are a dime a dozen. Execution is hard. Prepare for splashy headlines and minimal progress. That said: I hope I’m wrong! Good summary here, which politely describes the effort as “nascent and amorphous”. :]

https://www.wsj.com/politics/policy/doge-musk-ramaswamy-trump-c62291be

For context, the current odds of Musk out by July 2025 are around 21%.

https://polymarket.com/event/elon-musk-out-as-head-of-doge-before-july

In terms of macro information this week, we got some as expected US data (CPI and Retail Sales), a bunch of cabinet announcements, and some hawkish utterances from Chairman Powell.

Funny how dovish they were into the election and then how he flips hawkish right after. I am extremely averse to conspiracy theories, but man.

Don’t forget to buy the 2025 Spectra Markets Trader Handbook and Almanac here.

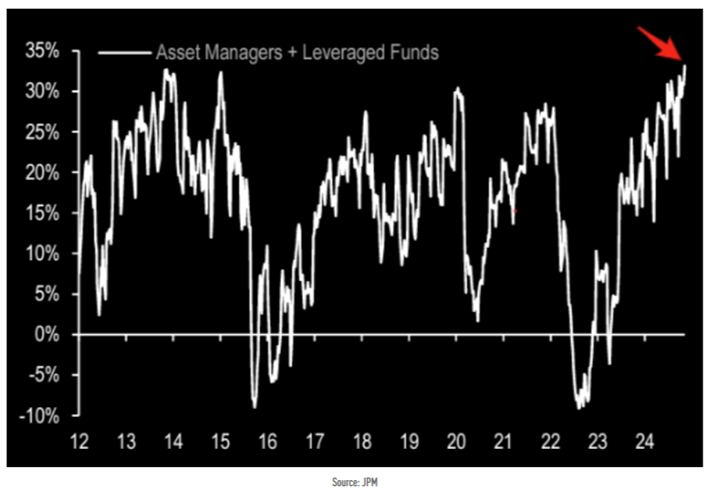

Lots of warning signs on stocks. Retail was all in before the election. Now, institutions have reloaded back to max long too as per this chart from JPM via TK.

Monday, with SPX around 6,000, I outlined in am/FX why I am reducing equity exposure in my retirement and education savings accounts:

We are in one of those periods where it feels stupid to even think about thinking about being bearish stocks, as the election has brought out mad animal spirits across the board. I am moving some money out of stocks and into cash in my retirement and education plans as I think the euphoria is getting a bit scary. While I can’t think of a single reason to be short stocks, I can think of many reasons to take some money off the table.

One: today feels a bit like this:

Two: the Nikkei has failed to confirm the rally. Similar to the 2021 peak. I acknowledge that this could simply because tax rates are presumed to be going down in the US and not Japan. But still.

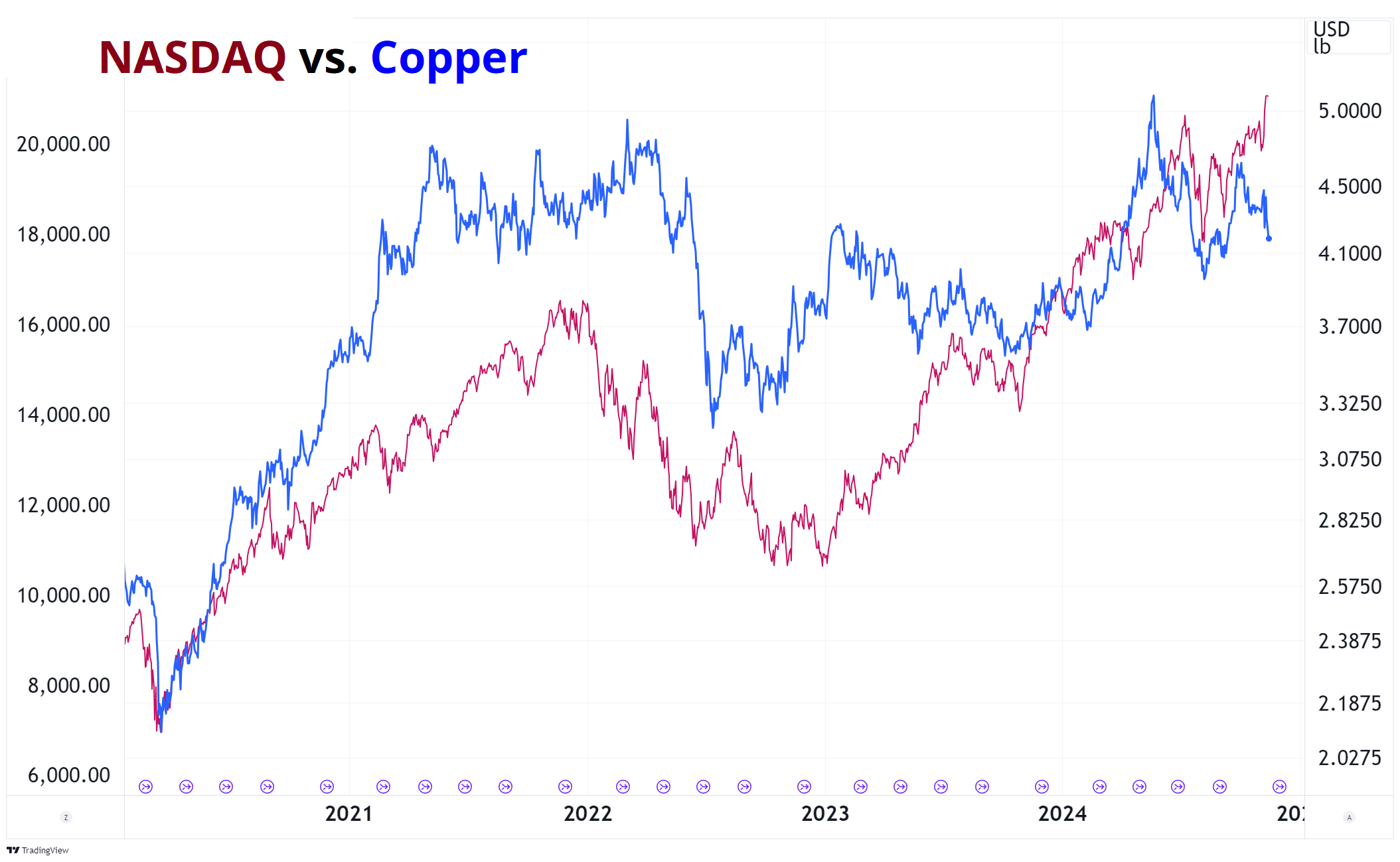

Three: Again, yes, a good part of the animal spirits in the US are idiosyncratic due to expectations of lower taxes and thus higher valuations for US equities, but it’s still a bit disturbing that commodities are not participating.

Stock market seasonality is incredibly bullish now until the end of the year but positioning probably offsets that somewhat. Retail was already max bullish before the election, and now the CTAs and vol-targeters have had a week to pile in—so here we are. Ultimately, my view is mostly a gut feel that the market is in a frenzied state of ecstatic intoxication right now. Fearful when others are greedy, yadda, yadda.

You should subscribe to am/FX and get this stuff in real time.

The flurry of ERP charts doing the rounds also make me wonder about stocks. For example, this one from Dave Rosenberg:

If you go further back, there is perhaps a counterargument that the greatest bull market of all time happened with negative ERP.

But the two regimes are not comparable. That 1980 crossover to negative ERP was the start of the greatest bond bull market in history as yields went from 15% to 0% over the next 35 years, This time, we are probably normalizing away from the secular stagnation ZLB stuff and finding a new, higher equilibrium.

So, you are not going to get a structural move lower in yields like we saw 1980 to 2019. And if you do, it’s very possibly not good news. Anyway, just something to think about. Again, I’m selling stocks to raise cash (see here).

ERP is one more thing that makes you go hmmm. The 1980 bull market started from low valuations and high yields. Now the setup is high valuations and historically normalish yields.

Also, AI Capex is still capex. And capex is always cyclical.

This week’s 14-word stock market summary:

Priced for perfection means there is plenty of room to correct to 5700 SPX.

Yields are pushing back to where we started before THE GREAT CARRY TRADE UNWIND OF AUGUST 2024 and we are tickling 4.40%, exactly where we were pre-August NFP.

If we get through 4.40%, things are going to get spicy as that opens up the possibility that we re-enter the old range which was 4.4%/5.0%. Yields to 5% is not on many bingo cards, and will probably unleash a wave of higher volatility, equity derisking, and overall pain. I’m not making that call. But it’s something to watch. A daily close above 4.40% in 2’s is probably bad news for risky assets.

USD is ripping. Whatever yields are doing, the view is that Day One tariffs are bullish USD and now we have yields onside as well. The market has got pretty aggressively long USD at the top of the range, which is always a concern, but even with China pushing back on CNY weakness, it’s hard to construct a good USD bearish thesis right now. At some point, the wheels are going to come off and the USD is going to explode higher. For now, we consolidate near key levels.

You would think multinationals are fully hedged in FX, but they never are. So, a rip through 108.00 in the dollar index (i.e., through 1.0440 support in EURUSD) is another brick in the wall of potential stock market misery. See this 2022 story, for example.

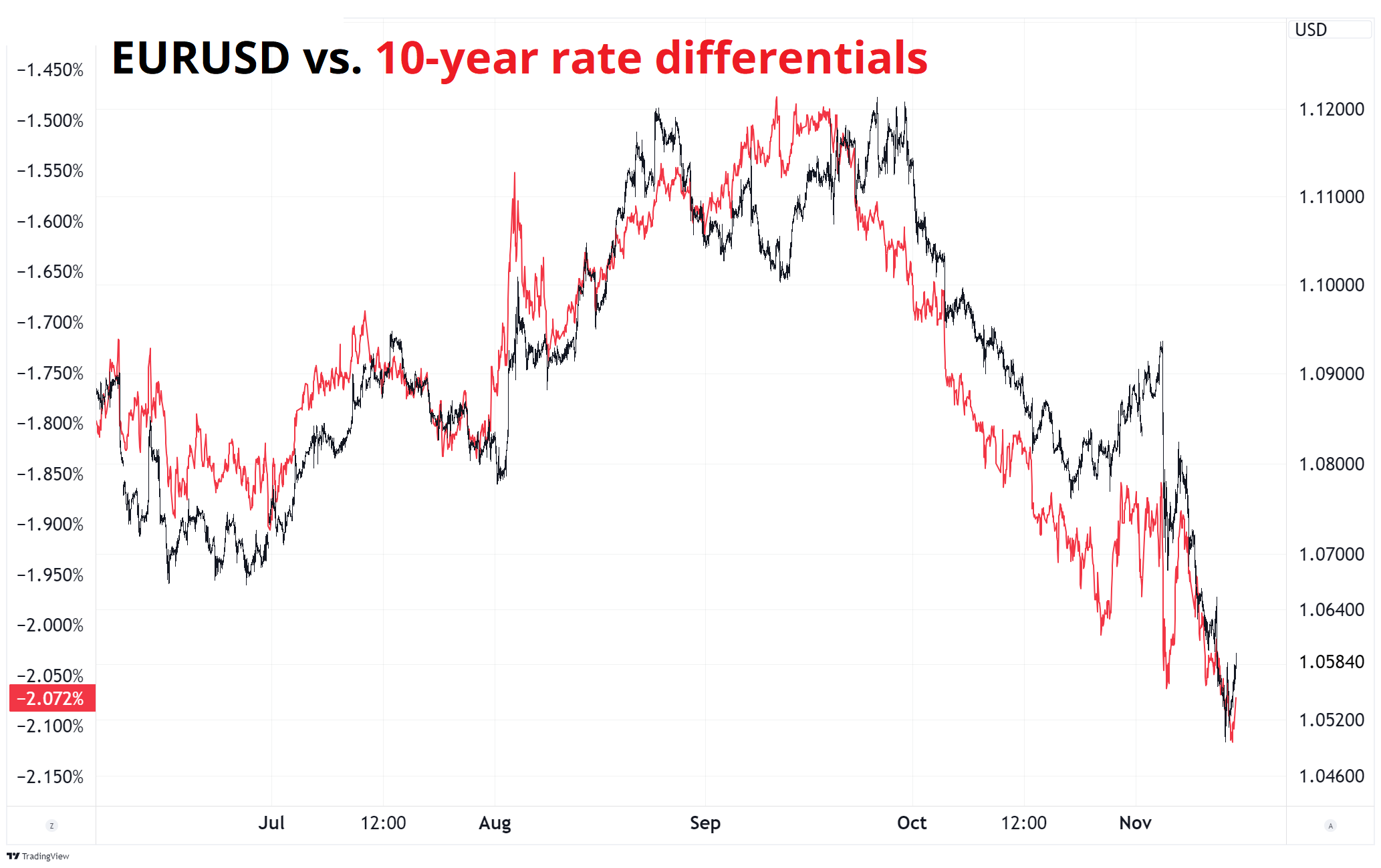

In case you are wondering, EURUSD continues to follow interest rate differentials quite closely:

While cross/JPY looks incredibly high to me across the board. I am particularly compelled to be short CADJPY given this:

Rate differentials tend to work well, with leads and lags. The leads and the lags are the hard part. As my old boss used to say about FX trading:

If it was easy, it wouldn’t pay so well.

Mamma! Crypto is raging as the prospect of Wild West non-regulation sets a fire under every meme and alt and shitcoin out there. My Twitter feed is jammed with memecoin ideas that sound a lot like investment advice but are labelled the opposite. Memecoins are a funny thing because there is not even a pretense of utility underlying the buying. It’s purely a fun way to show you can find greater fools who will provide exit liquidity for your earlier purchases. The terminal value of every memecoin except Doge is probably zero, so it’s a fun game of hot potato / musical chairs until the spec fever dies down and everyone loses interest again.

The rally in bitcoin has a bit more of a fundamental backing as the Trump administration will embrace crypto and reduce career risk for institutions that might want to own it. The moves this week further support an idea that I have long held: Bitcoin is the OG and has no competition. ETH is competing with an infinite number of potentially superior coins.

ETHBTC is supposed to rally in bull markets because ETH is the higher beta. This was true in 2018 and 2021, but is super not true in this cycle, even as altcoins rip. SOLETH is exploding higher, ETH is being made fun of, and I would assume this is structural going forward.

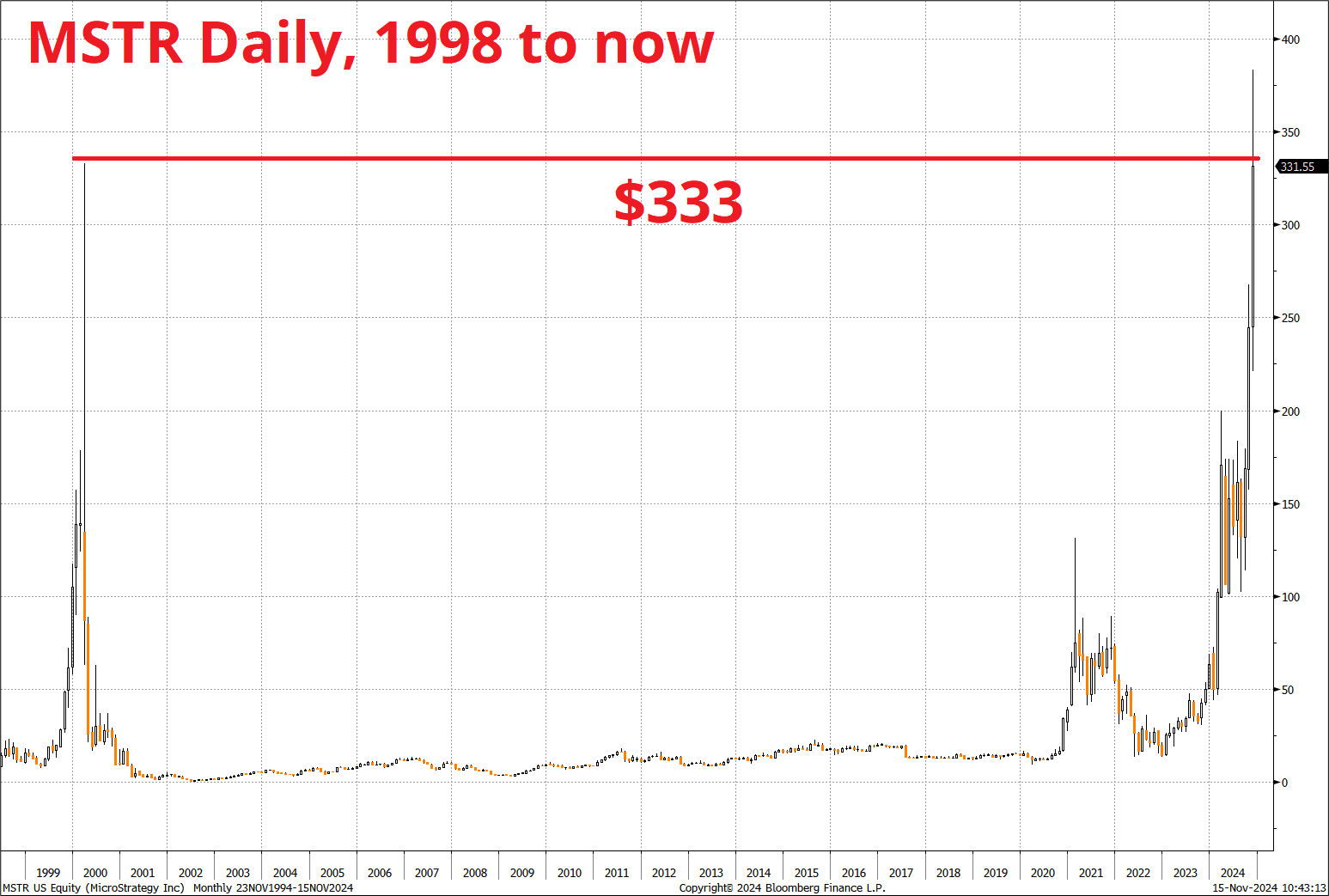

Finally, anyone that bought MSTR at the peak of the 1999 dotcom bubble is back to flat! Symmetry is so beautiful.

And in case you missed it:

Gold is doing its thing as extreme positioning and consensus longs bottle. If you are waiting to buy, $2480 and $2280 look like the places to stick out your hand. While it feels like we have come off a lot, when you look at the chart you quickly realize that a move to $2080 (the old breakout) is not completely out of the question. Things that go up fast and have no natural positive drift or cash flows can go down just as fast as they went up.

With the China stimulus theme completely dead now narrative-wise, copper has returned to Earth, too.

While that was a bloodbath of sorts, a severe decline in China A shares would be much more painful. Remember the market is short boatloads of $26 puts in ASHR and we’re now fizzling down towards $27. A break of $26 is going to trigger some nasty unwinds. Not investment advice.

Whew! OK! That was 9 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

Thanks for the music links, everyone. Here are some highlights.

Fontaines DC via SL

Kind of Oasis’ish but different and modern.

Mass Wicked Awesome PsyTrance via DL

If you listened to Sasha and Digweed in the 2000s, you will like that one.

Adam Beyer live from Drumsheds (2024) via Sergei

I need to find a way back to age 27. I fear there is no way back.

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.