February 6, 2024

PDF version

Back in the USofA: Part 2

One thing that came to mind on my travels to Brazil is that the world is just incomprehensibly large. I left the 20 million people of the NY-Tristate Area to visit two huge cities and perhaps met 100 out of 30 million people in the two cities I visited. When you step out of your bubble it really blows the mind how big the world is.

Following yesterday’s writeup, here are the remaining discussion points from my trip.

USA and The Dollar

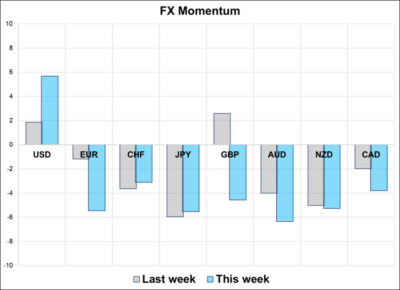

Clients on the trip to Brazil were pretty agnostic on the dollar. There was a clear bias to be short EUR vs. something, and long BRL vs. something, but no clear USD view. As with most of our clients, Brazilians are sympathetic to a higher USD but struggling to get involved as the Fed turns from hiker to cutter and levels look generally unattractive. I don’t think the levels matter that much. USDJPY can go back to 152 or higher. EURUSD can go back to 1.05. GBPUSD can go back to 1.23.

The challenge for trading the USD is that most rate differentials (Germany/US and UK/US, for example) are essentially unchanged since last October and rangebound. We need divergence in yields to get a substantial move either way in the USD. Most currency pairs and rate differentials are about where they were when CPI came out on November 14, 2023.

The biggest story for the dollar post-COVID is the regime change as the US has become a net exporter of energy and thus removed a major USD down regime from the matrix. In the past, the easiest short USD trade was when energy prices were ripping. Now, that regime is USD-positive! With one major USD down regime crossed off the bingo card, it’s harder to be bearish dollar.

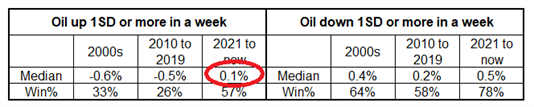

Here’s a look at a few regimes and how the USD performed. I looked at the 2000s, 2010 to 2019 and 2021 to now because I feel those are the three main FX regimes in my career. 2000s was USD diversification ending with the GFC, 2010 to 2019 was secular stagnation and ZLB regime and 2021 to now is the post-COVID hypercycle.

The first regime to look at is oil up or down. You can see that oil up more than 1 standard deviation used to be sell USD and now it’s tiny buy. This is using change in CL and DXY in any given week.

The other regimes have been somewhat constant. Here’s 2-year yield vs. DXY.

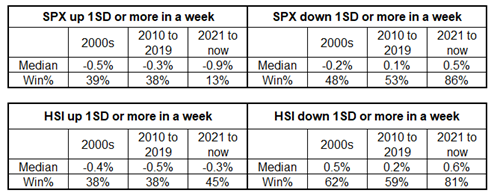

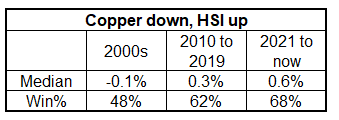

Despite the American Exceptionalism theme that percolates now and then, the reality is that big moves up in stocks have been associated with moves lower in the USD, even post-COVID. And lower stocks = higher USD. You can see the relationship with HSI has been more reliable across regimes than the relationship with SPX. This makes sense because Chinese outperformance is a good proxy for the middle of the USD smile. Tables show 1-week performance of DXY in various regimes.

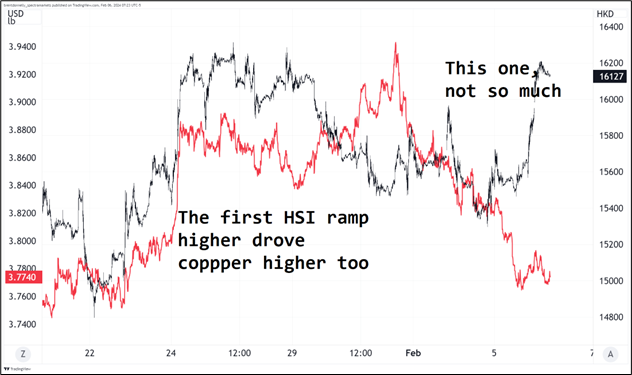

That said, the conversation in Brazil frequently touched on the idea that the current round of stimulus from China is financial, not economic stimulus and therefore the impact on the USD is less clear. If China stimulates and that boosts growth, investment, and commodities, you sell USD. But if they stimulate and that just rips stocks higher with little impact on the real economy… Is that a reason to sell USD? Probalby not. We got an interesting example overnight as unlike the first rally in Chinese stocks on the “China mulls stock market stimulus” story, the second ramp higher in Chinese stocks saw no rally in copper.

Hang Seng Index vs. copper futures

This made me curious whether it’s copper or HSI that’s the better indicator of the middle of the USD smile. You can test this by looking at weeks when copper went down and HSI went up. The results are clear: Copper down HSI up is a USD bullish regime—it’s not the middle of the dollar smile. Here’s 1-week DXY performance when copper is down and Hang Seng is up. While this was neutral in the 2000s, it’s USD bullish now.

Overall, I am more bullish USD simply because I have never been a believer in all these rate cuts, and I think the path of least resistance is higher USD. But we really need more interest rate divergence to get a meaningful move in currencies. If everyone is just priced to cut about four times this year and that doesn’t move… It’s hard to get super excited either way. For what it’s worth, I don’t think the MOF will intervene above 150 this time. 160/162 will be the new 150/152.

Other G10 topics

With such strong population growth, Canada’s economic performance is bad. The slack and vulnerabilities of the Canadian economy are on display, similar to NZ. It seems hard to believe the Fed will cut more than the BoC this year and yet Canada is priced for 3.3 and the US is priced for 4.5. Still, without a catalyst, USDCAD just floats around. Directionless.

There is quite a lot of attention on this Friday’s revisions to CPI. Remember that on January 16, Waller said:

One piece of data I will be watching closely is the scheduled revisions to CPI inflation due next month. Recall that a year ago, when it looked like inflation was coming down quickly, the annual update to the seasonal factors erased those gains. In mid-February, we will get the January CPI report and revisions for 2023, potentially changing the picture on inflation. My hope is that the revisions confirm the progress we have seen, but good policy is based on data and not hope.

I’m not a fan of the way everyone looks at 3-month and 6-month annualized and extrapolates benign YoY outcomes. If you did that in 2021, you would have thought inflation was going to 15% or something. 3m annualized changes dramatically each month as you drop 33% of your inputs and get a new replacement figure. If the structure of the past inflation data changes due to adjustments and they drop the back-end data and raise the more recent figures, the 3m and 6m annualized figures will look less rosy. More background in a Fed blog here. The data should come out on the BLS website at 8:30 a.m., though the first headline I could find on Bloomberg for last year was stamped 8:53 a.m.

Europe is stuck in the middle of a trade war and there is a high likelihood trade wars will escalate over the next 12 months. China has been subsidizing various industries like EVs, defense, and semis while the US has been funding multinational factory building in the US, but the EU has a much harder time with tariffs and subsidies due to the fragmented, multinational political system. China and the US can slap on tariffs and do internal subsidies much easier than the EU.

Related:

https://www.noahpinion.blog/p/tariffs-are-coming

Trump is bullish USD because of tariffs, not economic policy. While most agree Biden and Trump would run similar MMT-style procyclical fiscal policy (Trump tax cuts, Biden domestic investment)… The big difference is the 10% global tariff envisioned by Trump. That’s mechanically USD-bullish.

Finally, a couple of thoughts on the US data.

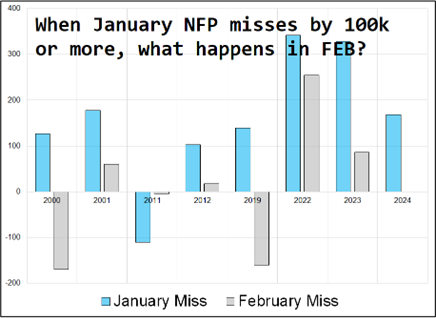

- Large January misses in NFP are random, not mean reverting.

- Many commentators continue to ignore Occam’s Razor, which would suggest that if every major headline economic data point says the US economy is strong—it’s probably strong. You can always find some devils in the details if you look hard enough!

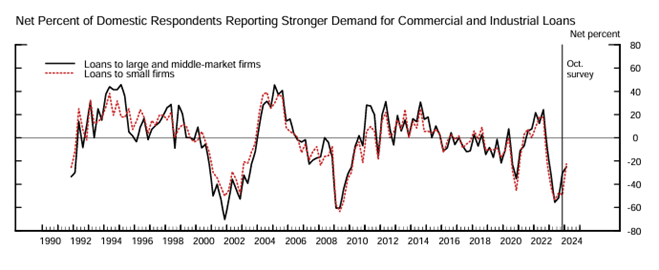

Instead, there’s still a huge cohort of analysts finding fault with every number, including yesterday’s release of the SLOOS. The SLOOS has turned more optimistic so now people are saying “yeah but the levels are still bad.” Yes, but they’re getting better, just like you would see as a mid-cycle slowdown bottoms out.

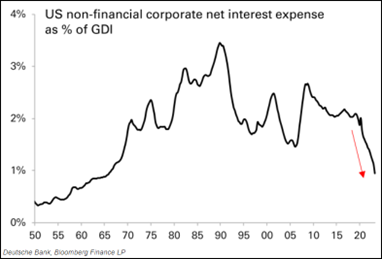

US corporates are incredibly well-positioned and have rolled their debt so successfully that rate hikes from 0% to 5.5% have led to lower interest payments in aggregate. Here’s a chart from George Saravelos via John Authers.

If the current economic expansion was on cruise control even when SLOOS was at 2008 levels, imagine if credit demand picks up again! Even a bit!

Final Thoughts

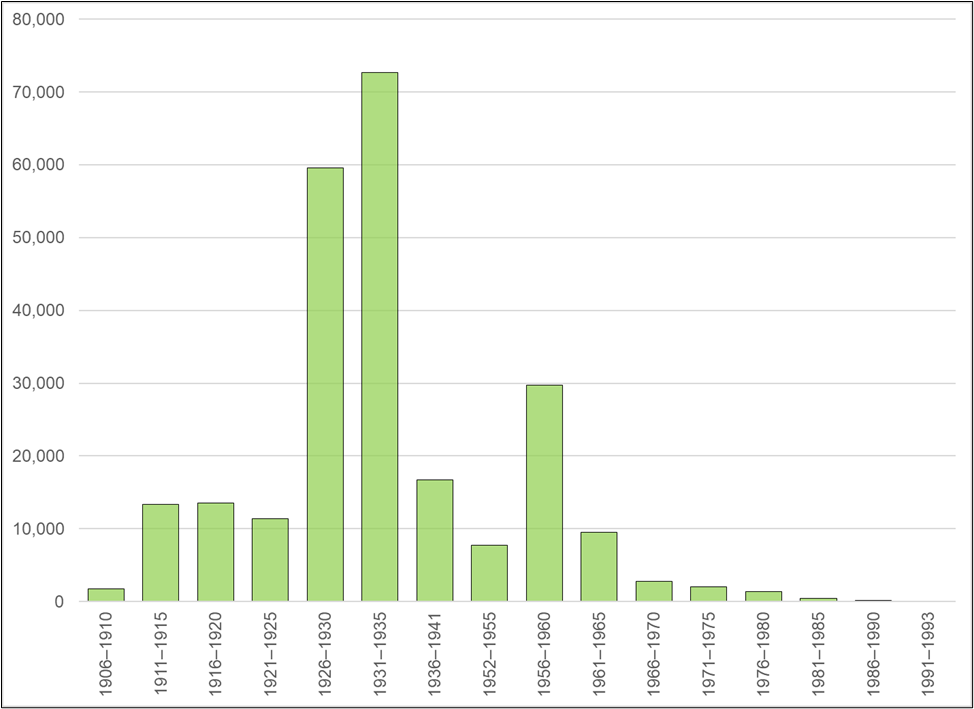

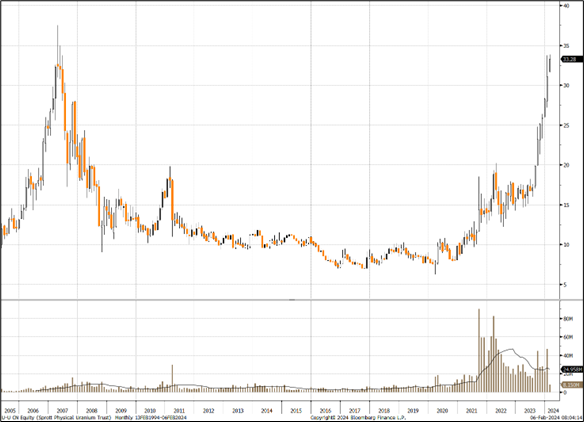

Even in Brazil, the consensus long uranium view came up a few times. I know nothing about it, but this retail fervor for uranium reminds me of 3-D printing in 2012. Or umm.. Uranium in 2007. Note declining volumes on this leg of the rally too.

Sprott Uranium Trust, 2005 to now

Good sushi in São Paulo: https://guide.michelin.com/us/en/sao-paulo-region/sao-paulo/restaurant/huto

good luck ⇅ be nimble