It’s not so much the “WHY?” as the “WHAT?” that matters most in markets. Keep your eyes peeled for good news / bad price setups.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

It’s not so much the “WHY?” as the “WHAT?” that matters most in markets. Keep your eyes peeled for good news / bad price setups.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

Here’s what you need to know about markets and macro this week

Before we get started, check out the video about Spectra School right here. It describes our flagship course…

This self-paced course will equip you with a set of robust and practical frameworks that combine logic, stories, data and more to help you see markets more clearly, make better forecasts, and make more money.

The course includes:

What you’ll learn about:

Course fee: $1,200.

Let’s go!

A feature of markets that drives new traders crazy is good news / bad price. “But Yahoo’s earnings were great!” he shouted as he pounded the Level II screen in March 2000, “Why is the stock going down?!??!”

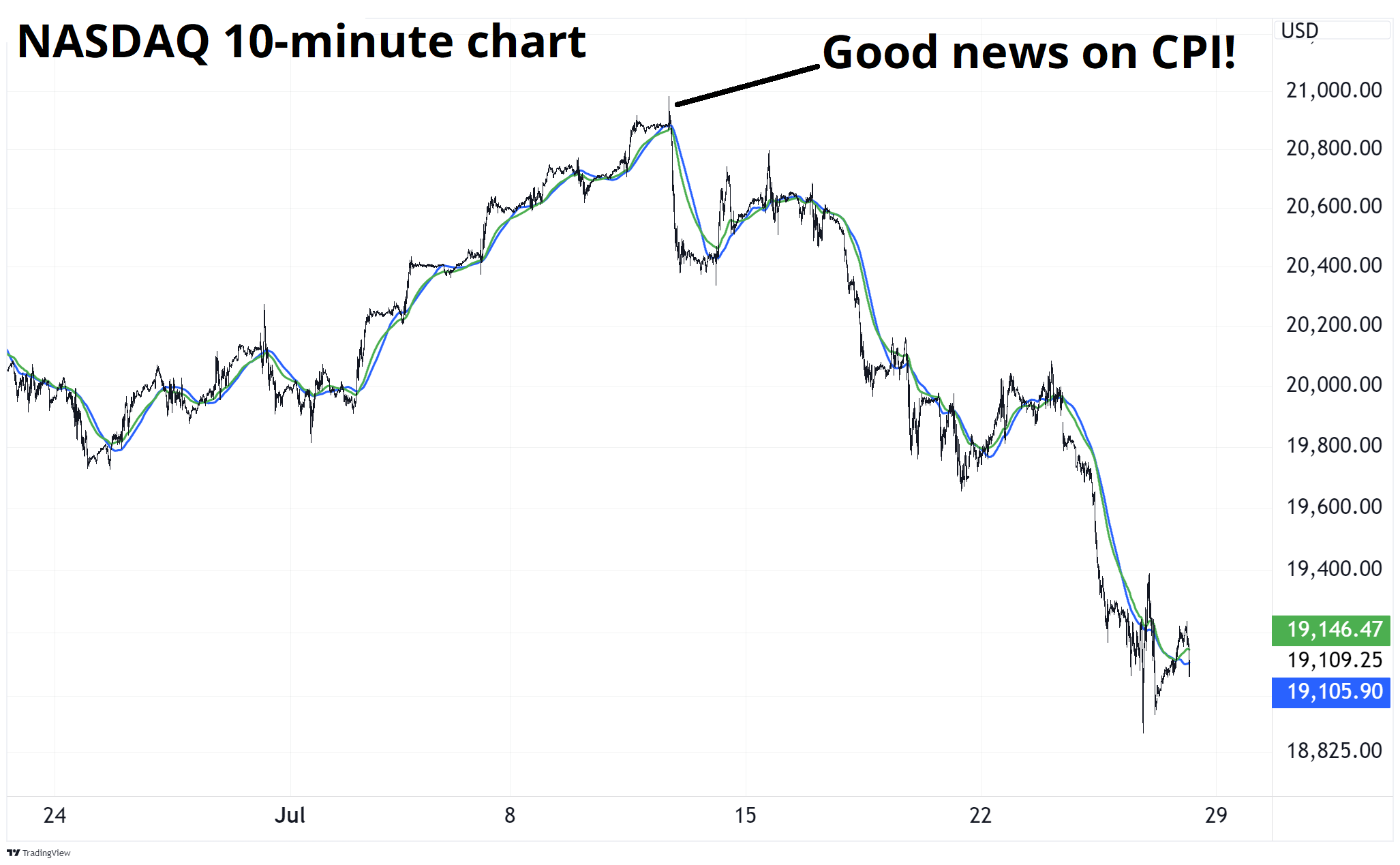

We saw a classic good news / bad price after the US CPI report earlier this month:

CPI came in softer than expected and then the NASDAQ dropped 10%. Wut? But that’s often how markets work. In fact, we saw the mirror image at the ding dong lows in October 2022. After that worse than expected CPI report, stocks went down for about 10 minutes and the proceeded to rally almost exactly 100% over the next year and a half. Craziness.

This also happened in 2011 when Bin Laden was killed.

There are two main reasons this happens:

In contrast, the exact opposite setup was in play this month. The soft landing and immaculate disinflation stories had been in force for more than a year. Slightly lower inflation was in theory bullish for asset prices, but everyone everywhere was psychologically prepared for disinflationary news and everyone everywhere was already max long every asset in the world.

While the killing of Bin Laden was a geopolitically bullish thing in theory, in reality medium-term sellers decided that the pop induced by the news was something you want to sell, not buy. You can see the wick on the S&P candle that day—big wicks like that show strong but failed attempts to penetrate a level. They indicate rejection.

So yeah. Somewhat counterintuitively, bad CPI put in the low in 2022 and good CPI put in the high in 2024 (so far).

It’s not so much the “WHY?” as the “WHAT?” that matters most in markets. Keep your eyes peeled for good news / bad price setups like this as they can often be indicative of narrative exhaustion.

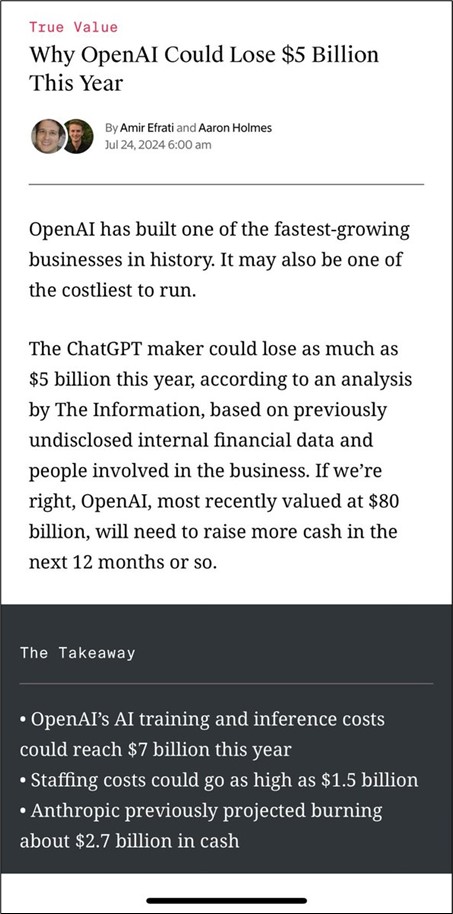

The turn in the AI narrative that started with the GS piece in late June continued this week as this story made the rounds:

While losing money can be a badge of honor sometimes (like WeWork in 2017 or every SPAC and turdco. in 2021) … It’s not necessarily great. More and more people I talk to and read are coming to the conclusion that:

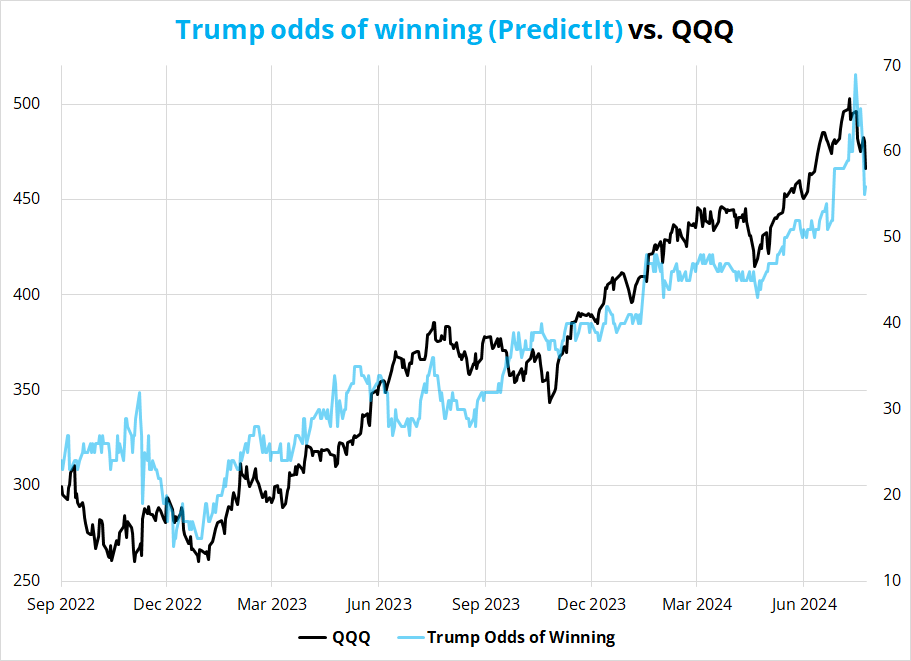

That narrative shift was lurking in the background and then Biden dropped out of the presidential race and all hell broke loose. It is controversial to say that Trump’s odds are influencing asset prices, but that’s what I believe.

Two main possibilities here:

During her 2020 presidential campaign, Harris called for a repeal of the TCJA’s corporate tax rate, which dropped the top levy from 35% to 21%. Her repeal would have reverted the top rate back to 35%. By comparison, Biden has called for raising the corporate rate to 28% in 2024.

I would go with number 2 more than number 1. I think Trump’s odds matter for macro.

While the Harris comment from 2020 is stale, it’s still probably not too far off base (see here, for example). The MMT regime launched by Trump in 2017 and aggressively pushed by Biden through COVID is likely to remain in place if Trump wins. It is more likely to be watered down by a Harris administration. As such, debasement trades are less amazing under Harris because fiscal policy is very likely to be less generous. This would be consistent with history: Republican governments ring up larger deficits than Democrats, mostly because tax cuts do not pay for themselves.

To me, this also means that rising Harris odds should be good for bonds. Slower growth + smaller deficits = less growth and less risk premium = lower yields.

I think you can track Trump’s odds and they should correlate somewhat with all the debasement trades. Trump is MOAR MMT. Harris probably is not.

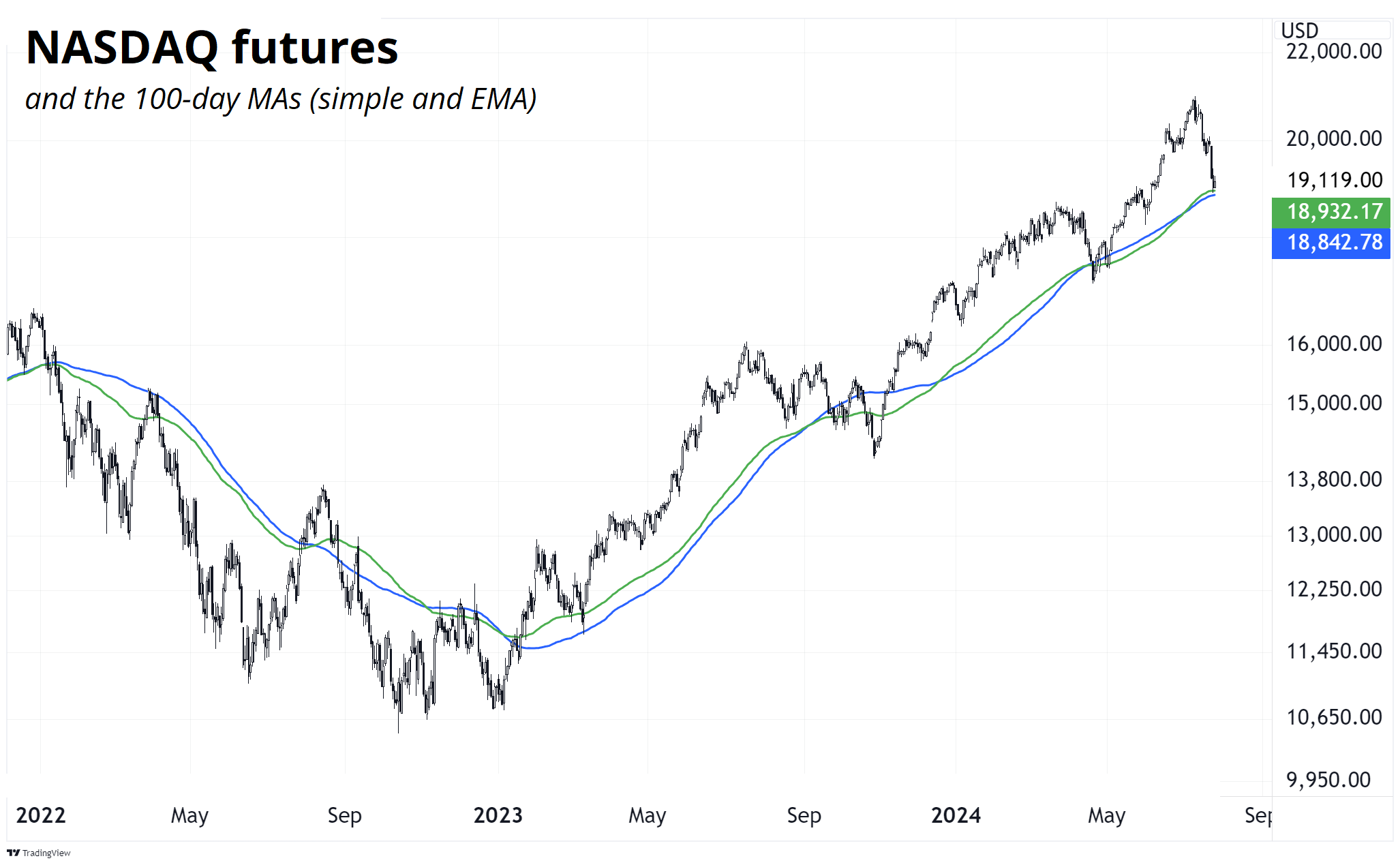

Chart-wise, we are in a massive support zone for the NASDAQ as the 100-day moving averages (simple and EMA) come in right around here. You can see the MA’s have been pretty good, but nowhere close to perfect, when it comes to defining the epic up trend that has dominated since early 2023.

Here is this week’s 14-word stock market summary:

Momentum and narrative cut both ways. Everyone to the other side of the boat.

Interest rate markets are boring right now as the looming economic slowdown fails to materialize quickly but also hasn’t really gone away. US GDP came in stronger than expected (Atlanta Fed GDPNow wins again!) and the US economy is totally fine. The soft landing and immaculate disinflation continue, and the Fed is absolutely locked into a rate cut in September at this point. It would take a geopolitical event or market collapse to justify 50bps in September and almost no imagineable string of US data could prevent the cut now, I think.

The only action is in the curve, where steepening continues.

The inversion of the yield curve lit up the recessionistas two years ago and the disinversion is likely to light them up again. At some point, if you call for a recession for long enough, you will be right ofc.

The current setup in bond markets is super interesting to me because you have basically perfect certainty for the next three months (not quite, but close) and then much, much more uncertainty than normal after that. With no visibility on fiscal policy in 2025/2026, the Fed can’t really predict or forwardly guide what they’re gonna do. They have to play it one month at a time and see who wins the election and how committed that winner is to continuing the MMT policies made mainstream by Stephanie Kelton Donald Trump and continued by Biden.

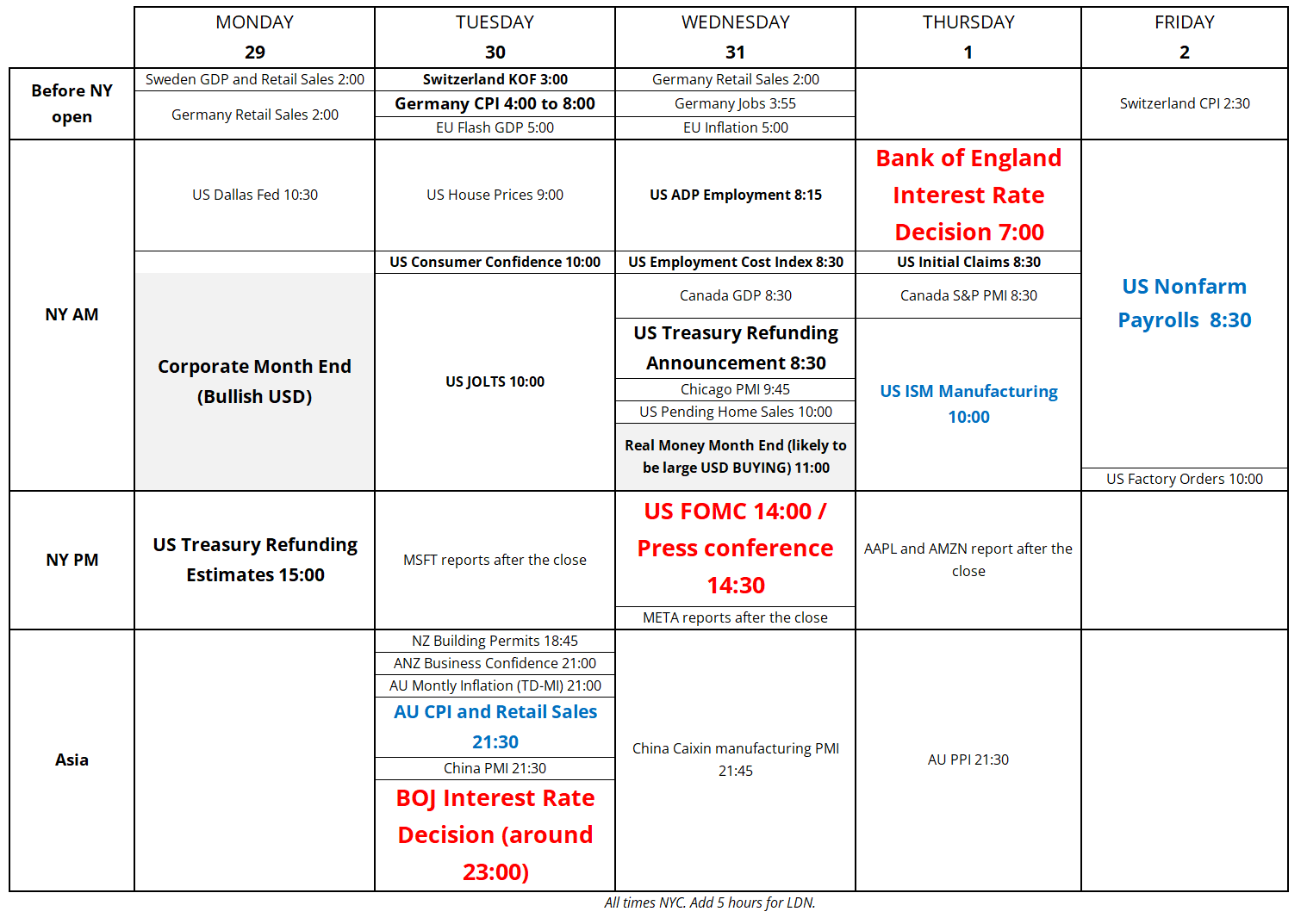

Next week, the calendar is absolutely nuts, with multiple central bank meetings and tons of other stuff. The BOJ meeting and Bank of England meeting are both priced as something close to a coin toss, so those will be market movers pretty much by definition.

I am particularly interested in what the BOJ will do because there are many good arguments for a hike and the angst over the weak JPY seems to have gone beyond the MOF and is shared by most government officials. Still, that last sentence was true in 2022, too, and the BOJ didn’t play ball. Let’s see if they do next week.

Here’s the calendar, in all its glory:

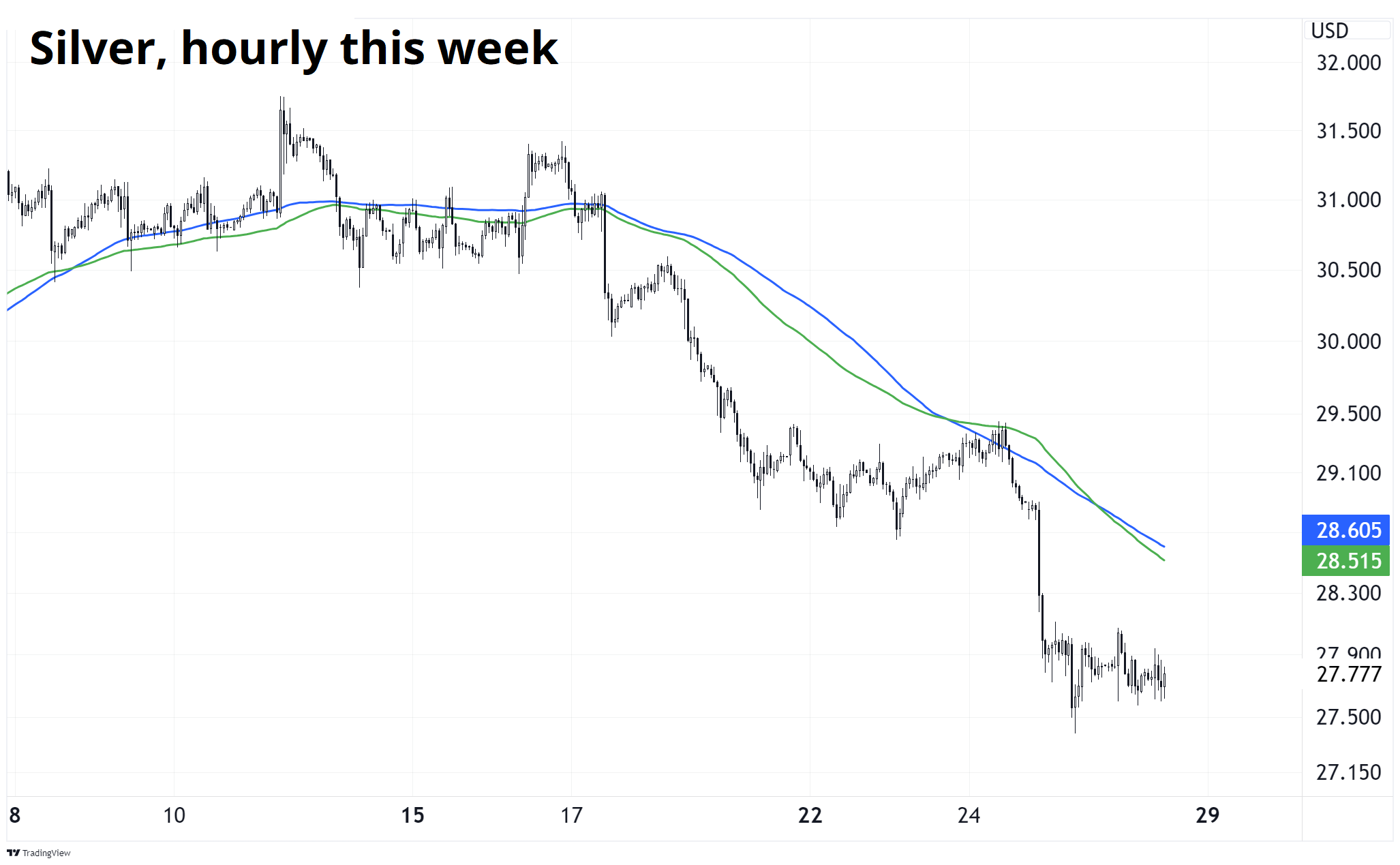

You want vol? We got vol! USDJPY is flying all over the place and liquidity has gone from nearly infinite to sketchy almost overnight. That tends to be how it works. One day USDJPY is trading 1 pip wide in 30 bucks and the next you try to sell 14 USDJPY and it moves 9 pips. Vol of liquidity and vol of liquidity vol can be high. Crazy stuff.

The move in the JPY was part of a broad-based unwind of all the most popular carry trades including USDJPY, EURCHF, USDMXN, USDBRL, AUDJPY, and so on. Anything with carry got Old Yellered. Anything that relies on MMT and US fiscal stimulus got completely crushed. USDJPY ticks both boxes.

While the pair got smoked and continued the steep selloff triggered by the visible fist of the Ministry of Finance, it did manage to hold the critical 152 level despite mega selling down there.

That’s the hourly chart; you can see that the 100-hour MAs capped the rally this morning. The daily chart shows the importance of the 152 level more clearly:

Levels don’t get much more epic than that. Massive resistance becomes massive support, holds on a retest in May and holds again this week. That level is the absolute megapivot for USDJPY. Note that I am not pointing out this level in hindsight; I used it as part of my reasoning for a sexytime tactical long trade in am/FX yesterday.

The ETH ETFs started trading this week and we got another buy the rumor / sell the fact trade. These are getting pretty obvious and thus are not leading to massive declines anymore, but still.

The selloff in ETH was probably more a function of tech stock weakness than any flow imbalance post-ETH ETF but it’s still fun to see how the launch of these things always leads to profit-taking in the related coin.

Overall, crypto has traded incredibly well through this tech correction, and the lack of cryptocurrency selling in the face of a QQQ melt is bullish. MSTR not too shabby, either, as it’s trading near the all-time highs in anticipation of the August 1 split (10-for-1). Wanna hear something crazy?

The all-time high in MSTR is $1999.99. Round number bias, FTW.

Also, this happened!

https://watcher.guru/news/michigan-state-pension-fund-adds-6-6m-in-bitcoin-etfs

Go Blue!

Gold and silver are debasement trades, and they logically did not do very well this week as popular stuff got unwound and forward 2025/2026 debasement probability dropped when Biden finally stopped out of this losing bid for reelection. That said, gold came almost all the way back—silver did not. It’s hard work being long silver!

With China done buying gold for now, CFTC positioning showing a rapid buildup of longs and open interest in XAU, and Trump no longer a lock for president (despite remaining a huge favorite)… I really dislike precious metals right now. This is sacrilege in most quarters of FinTwit, but hey. There are better things to own, methinks.

Ags, copper, iron ore, and anything that relies on Chinese growth continue to trade horrendously as the Third Plenum came and went and all we got was a couple of lousy rate cuts.

I saved this image as “stupid unfunny t-shirt meme.png” on the Spectra Markets shared drive

And… Finally… This week’s Macro Trading Floor podcast is ready to go.

Whew! OK! That was 9.44644 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

Smart, interesting, or funny

A long read that I found quite interesting.

Don’t let those wonky academics intimidate you! You’re smart.

In this short Substack essay, Justin Ross introduces me to a new concept: Levels of Analysis. The framework helps explain why debating and making decisions is so freaking hard.

Music

Bad mood banisher

I like you: A happier song by Post Malone and Doja Cat

Impossible to be in a bad mood while listening to this song. Doja Cat is pretty dope.

One of the great poetic verses to start to a song (especially if you’re a Canuck)

Fireworks by The Tragically Hip

If there’s a goal that everyone remembers

It was back in ol’ 72

We all squeezed the stick and we all pulled the trigger

And all I remember is sitting beside you

You said you didn’t give a fuck about hockey

And I never saw someone say that before

You held my hand and we walked home the long way

You were loosening my grip on Bobby Orr.

I don’t even like this rendition, but it’s amazing how it’s a perfect combo of the 1980s and 1990s in one song.

Sweet Child of Mine performed by Sheryl Crow

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.