When oil gets to $100, expect Trump to declare victory.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

When oil gets to $100, expect Trump to declare victory.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Quite a lot has transpired since last week’s Speedrun as the U.S. and Israel attacked Iran and Korean equities collapsed 20%. The sunbound unicorn was, indeed, like Icarus.

Oil prices are mooning like crypto in 2021 and the “No More Foreign Wars” administration has declared unconditional surrender as the objective in Iran. Risky assets have sold off, but not THAT much, and formerly high Sharpe trades like EMFX have been clobbered. People got so used to buying EM on every dip, but they have now finally faced up to the realization that the idea of emerging markets and high carry assets as safe havens makes no sense.

The moves in energy prices are a negative terms of trade shock for Europe, and the market went into this whole thing short dollars, so the USD has rallied on the war news. The most glaring aspect of the market mosaic right now is that there is, once again, nowhere to hide.

Bonds are down. Gold is down. Crypto is down. Private equity and software are down. Foreign equities are down. The yen is down. And nobody really trusts the dollar as a safe haven anymore, this is more like forced buying of dollars, not confident hedging of risks.

Nonfarm payrolls showed weakness, but given the distortions from weather and strikes, and the strong NFP release last month… It’s mostly noise. The U.S. economic data paints a continued picture of soft landing with ISM and Initial Claims still showing everything is fine. Here’s what I said in am/FX this morning:

—

excerpt

It’s an interesting moment in markets now as fast money is out of EM longs after two rounds of blowups in MXN, HUF, COP, KOSPI, and so on. Real money is still mega long EM as it has been churning out a 2 or 3 Sharpe for ages, and they are much slower to pivot. Rising vol will continue to force degrossing. That said, we are in the rare moment where convexity goes both ways.

Given the opaque strategic goals of the US/Israel attacks on Iran, the administrations can declare victory at any time and say they did what they were hoping to do. Given the nuclear facilities were already destroyed in June 2025, then now not destroyed… They can easily be declared destroyed again, for example. If and when Truth Social lights up with a “WE DID IT! WE WON THE WAR!” message, EM, AUD, and many other assets will absolutely rip.

On the other hand, as refineries fill up, export bans hit, the Strait of Hormuz remains troubled, and so on… Crude will keep creeping higher and will probably trigger another round of convex liquidation as we see 95/100 in CL and/or Brent crude. Normally markets are convex in the direction of risk aversion, but right now markets are convex in both directions.

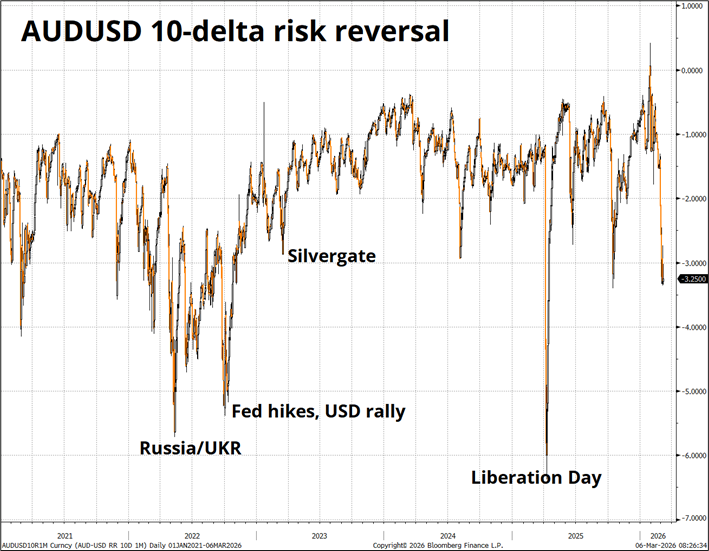

The degree of forced selling and hedging can be seen in options market skew.

I think that chart shows perfectly that:

To me, the path of least resistance remains higher oil, and weaker EM, but there is always going to be a risk of a declaration of victory and end of the war. You cannot really trade in front of this because the war could be over next week, or in 2027. You just have to be ready.

One major catalyst that could trigger the end of the war is a rise in oil prices to $95-$100. The administration has shown in the past that the markets are the ultimate arbiter of U.S. policy (that’s where the TACO acronym came from) and if oil gets near $100, I believe the intestinal fortitude will break down and you will see a recalibration or end of the war. So, if we get there (Brent is 88, CL is 86), I will get busy buying topside AUDUSD, TLT, and KOSPI and downside in USDBRL and EURHUF.

To summarize my view:

There is currently convexity in both directions for EM. This is rare. Normally it goes up the escalator and down the elevator. Now there is elevator service in both directions. This has important implications for trade structuring because options markets are heavily skewed in the direction of risk aversion and more guano hitting the global fan.

Here’s a good point of view from Kevin Muir.

end of excerpt

Despite eye-watering sector rotations, and a run up in the VIX from 16 to 26… The NASDAQ is just in a huge range and has been stuck here for six months(!)

Note the three-touch trendlines on both the highs and the lows as we converge towards the apex of a gigantic triangle. We are coiling like crazy. Before the war started in the Middle East, markets were already grappling with private credit write-downs and fears of AI Capex overspending, and now crude oil has nearly doubled. Given that backdrop, my bet is that it’s the bottom of the triangle breaks, but my conviction is low given the prospect of a declaration of “Mission Accomplished” in Iran at any arbitrary moment.

Here is this week’s 14-word stock market summary:

Stocks are resilient and panic is minimal. $100 crude should bring panic and TACO.

https://www.spectramarkets.com/subscribe/

Central banks are worried about higher oil.

Ripping oil prices are inflationary, and yields are responding. Front end traders have gone as far as pricing in an ECB hike for 2026. That’s almost surely not happening, but just because it’s not happening doesn’t mean the market can’t price in three hikes first!

Oil shocks are one of those economic events you can model as deflationary or inflationary, depending on your time horizon and worldview/bias. Everyone remembers the shocks of 2007/2008 and 2011, and what happened after the ECB hiked into those shocks, but you still have to respect that crude oil is a huge driver of consumer prices. And if central banks do nothing, they risk feeding inflationary psychology.

This chart of US 2-year yields is a looker, as Sal would say.

The PBoC had excellent timing as they put the bottom in USDCNH, pretty much to the day. Same thing with the USD-bearish cover from The Economist. Funny.

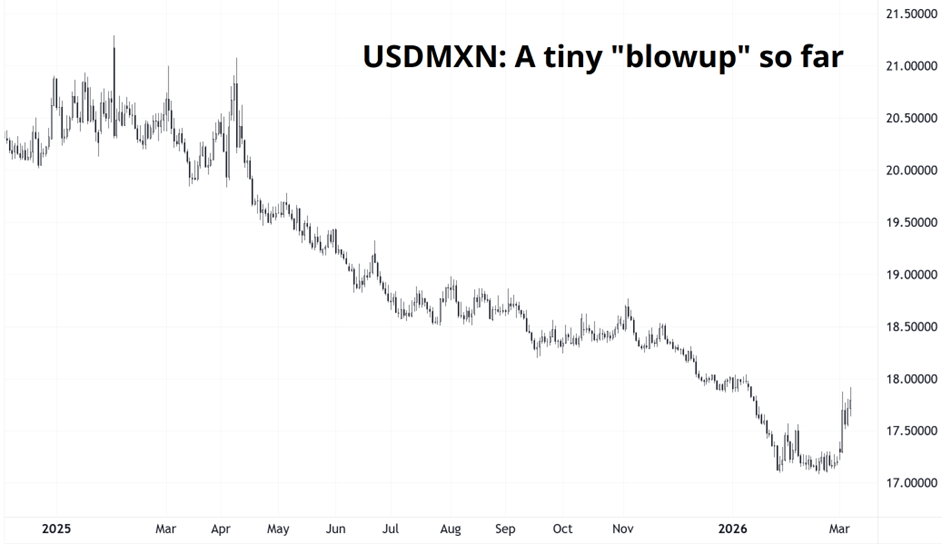

Now, the most favored EMFX trades (USDMXN, EURHUF, etc.) are kind of blowing up as the market thought there was a free lunch in EM, but there isn’t. There never is.

Then again, “blowup” is strong. It went from 20.5 to 17.00 in a year and now it’s 17.84.

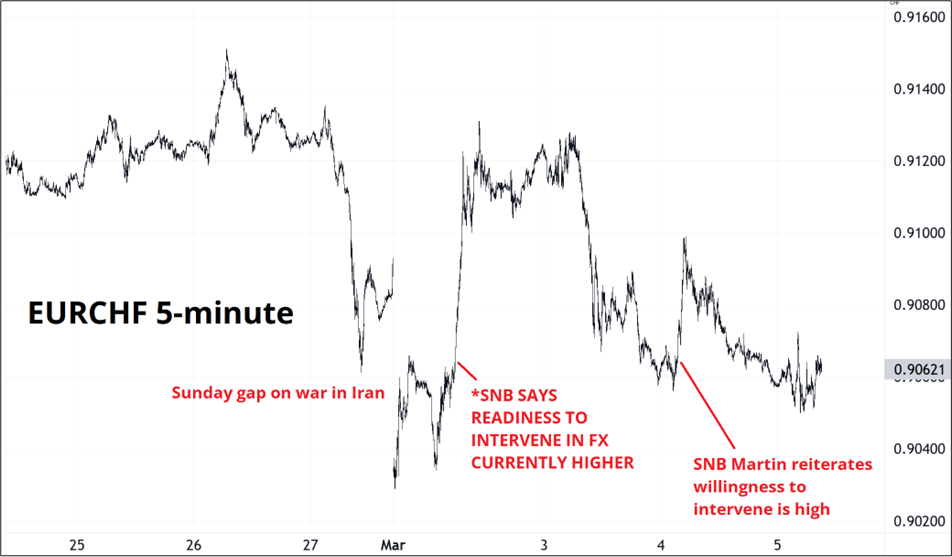

Meanwhile, the SNB is getting annoyed with CHF strength again as EURCHF plumbs the all-time lows (ex flash crash). This chart is from yesterday and now EURCHF is 0.9024.

The SNB squawked twice at 0.9060. While they have very low credibility on intervention, they can turn the market for a week or two. Humans place larger-than-normal importance on round numbers and we are getting close to 0.9000. And the SNB is run by humans.

Our Chartered Market Technician at Spectra Markets sent me his update for USDJPY. Here is the latest technical analysis:

Subscribers to am/FX got a technical treat this week as I posted this Wednesday:

Looking at a bitcoin chart, you can see that there was a prolonged period of equilibrium 53000/74000 until the U.S. election triggered a breakout. The new zone was 74000/125000 and now we might be back in the old zone and therefore I would watch 74,000 as major resistance from here.

Lo and behold!

$35 dollars is 0.00047297297 of $74000. How’s that for precision?

Gold is about the most egregious good news/bad price setup I have ever seen. War in the Middle East and gold is lower. Not good for short-term punters who are long. You can imagine that a declaration of victory by the US and Israel will now deliver a quick $500 drop in gold.

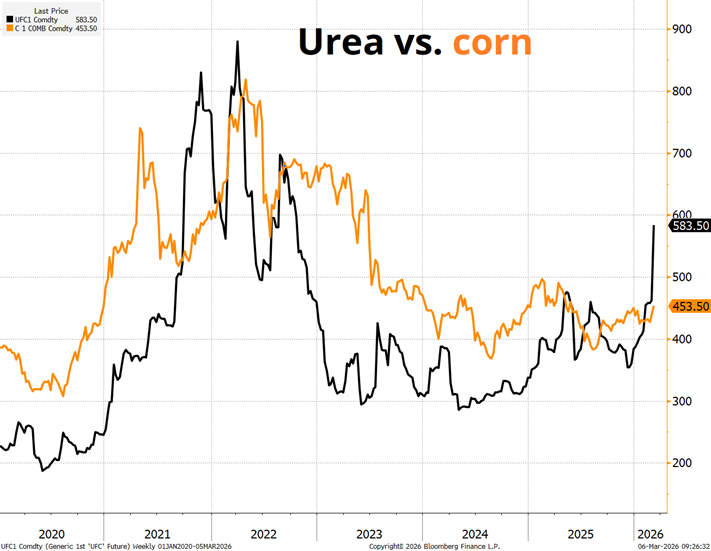

Meanwhile, everyone is staring at crude futures, but fertilizer is a big issue now, too. The supply and price shock there could bleed through to higher agricultural prices if the conflict isn’t settled soon. Here’s Urea futures (urea is fertilizer) vs. corn futures.

Very hard for plebes like me to trade ags, but this is a developing story and is part of the inflationary impulse caused by war. Then again, the best ag trader I know tells me cost of production is only one thing to consider in ags and unlike oil, ag production is not getting shut off.

That’s it for this week.

Get rich or have fun trying.

*************

*************

*************

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.