They shot first and asked questions later.

They did WHAT for $6 million??

They shot first and asked questions later.

They did WHAT for $6 million??

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Try Spectra School for free!

If you’re looking for a good way to spend 35 minutes or so, check out Lesson 3 of our flagship course “Think Like a Market Professional” for free. https://spectramarkets.com/lessons/tlmp3/ There, you will find the entirety of Lesson 3, for free, along with a link to my Learning From Legends video with Ben Hunt.

The lesson is called “Surfing the Narrative Cycle” and delves into how you can understand the stories the market is telling itself. If you like it, you can sign up for the full course and use coupon code LESSON3 for $250 off the $1200 price (i.e., you pay $950 for 16 lessons and 10+ videos.)

What a week! The Great Repricing of AI compute and power on the DeepSeek Freak rocked the markets this week as long/short funds had either the best or worst week ever as some of the hottest favorites like NVDA, VRT, and PWR repriced dramatically to the downside while money printing machines like META and AMZN made new all-time highs. DeepSeek was the cause, of course, and you have already read enough about that story to fill your brain and therefore I will not add anything explanatory here other than a three-bullet summary for anyone who’s been trapped inside a soundproof box all week.

The final verdict, for now is as follows:

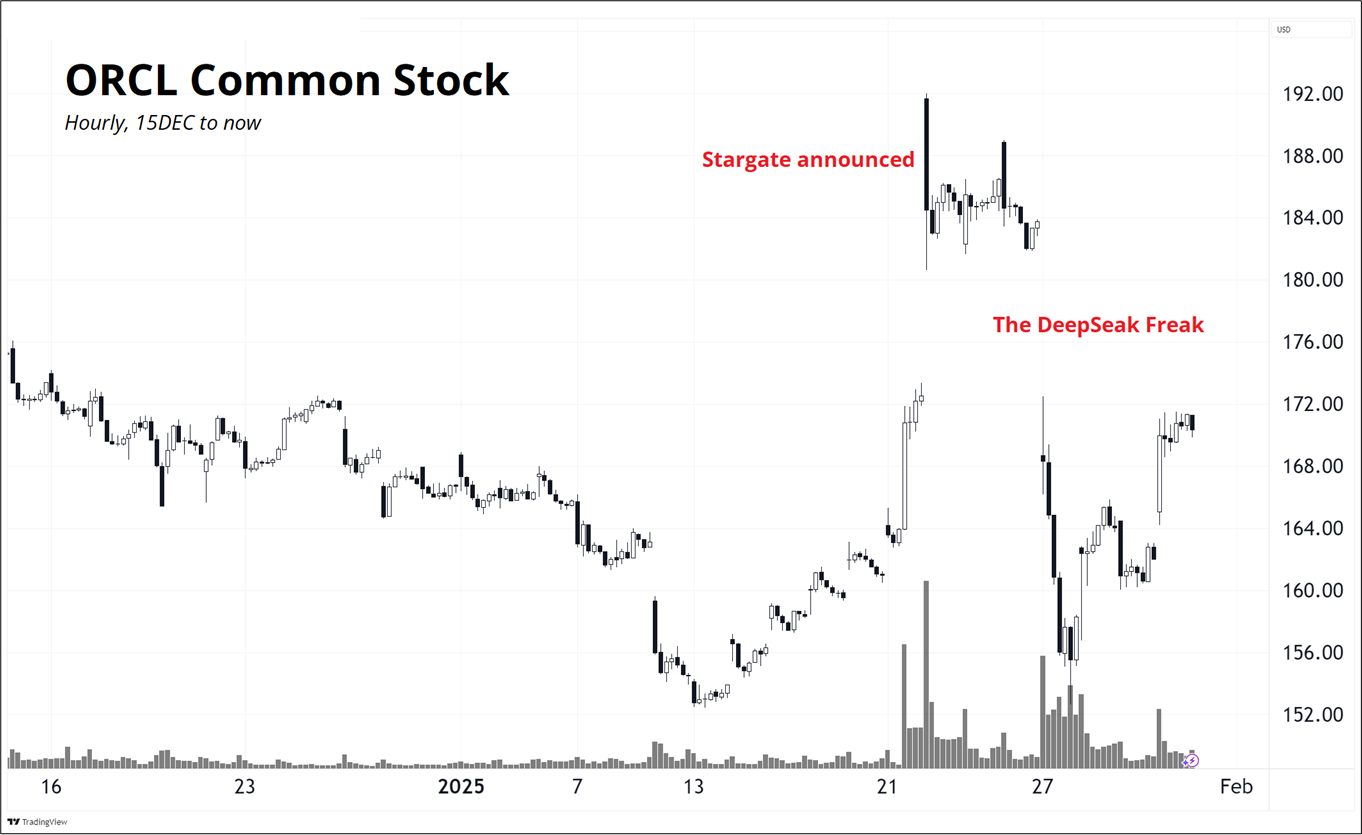

That last bullet is a reference to the US government’s announcement of Stargate, a project with a huge headline figure ($500B) that is mostly comprised of projects that were already happening anyway, but also some new money. The US government has crowned Oracle and some other companies as beneficiaries of this new project. Here’s how that went for Oracle.

Donald Trump and Larry Ellison

The simulation never disappoints as the DeepSeek Freak took hold only two trading days after the Stargate announcement. An intriguing aspect of the whole DeepSeek phenomenon is that it wasn’t actually news. Select individuals in the industry had been writing about DeepSeek’s breakthrough since Christmas week of last year, but it took VC’s losing their minds on Twitter over the weekend for the market to realize the possible importance of its arrival.

This should be a great inspiration to anyone that believes they can make money in the markets. Superior public information was widely available and anyone that could properly interpret it before the herd was able to cash in massively. Markets are very, but not perfectly efficient.

Outside of DeepSeek, the other story was the ongoing threat of tariffs on Canadian, Mexican, and maybe some other goods. The President reiterated his desire to slap Canada and Mexico with 25% levies yesterday and these are to be announced Saturday. We will get more into the tariff shenanigans in the section on fiat currencies.

In central banking, things are pretty quiet. The Fed is on hold, the Bank of Canada and ECB cut as expected and most of the cutters are getting close to neutral. The RBA is very late to the rate cutting party, but this week’s soft inflation data in Australia means the first Ozzie cut comes in February.

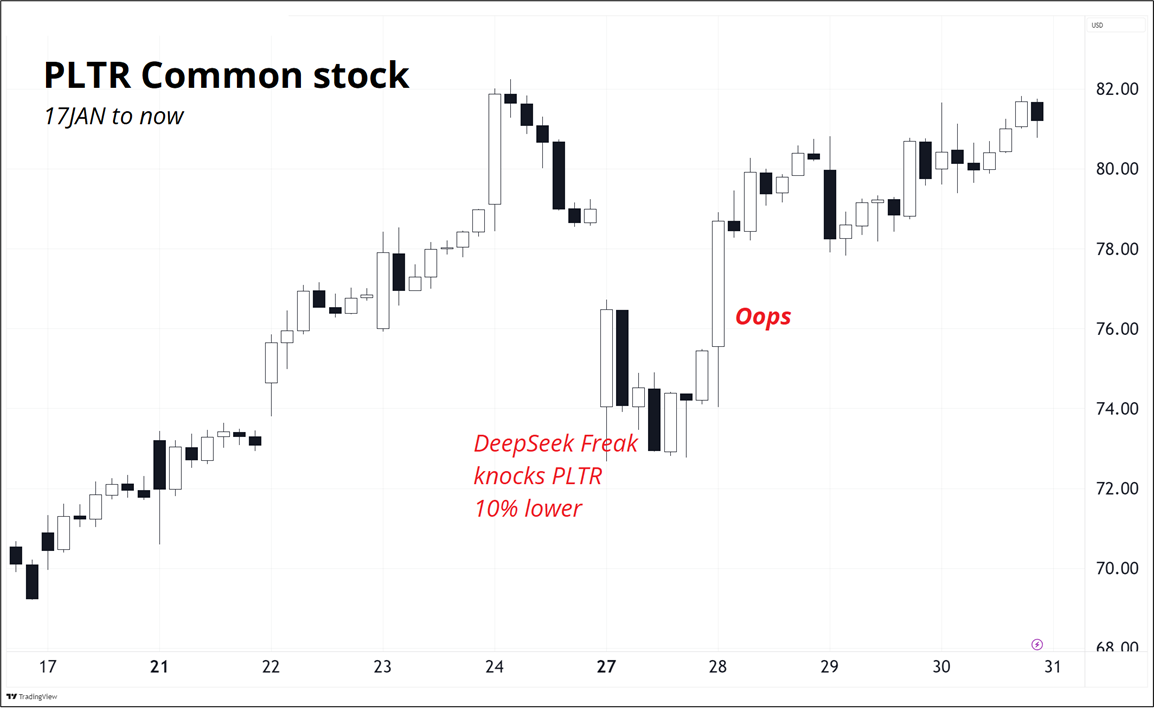

The initial reaction to the DeepSeek news was to toss all babies out with all bathwater and the cash indices all gapped a few percent lower on the Monday open. This made no sense, of course, as is often the case in markets when there is deleveraging. Companies like Palantir and META, for example, are more likely to benefit from cheaper compute, not be penalized by it. So charts of many stocks that should be unscathed or supported by the DeepSeek news did something similar to this:

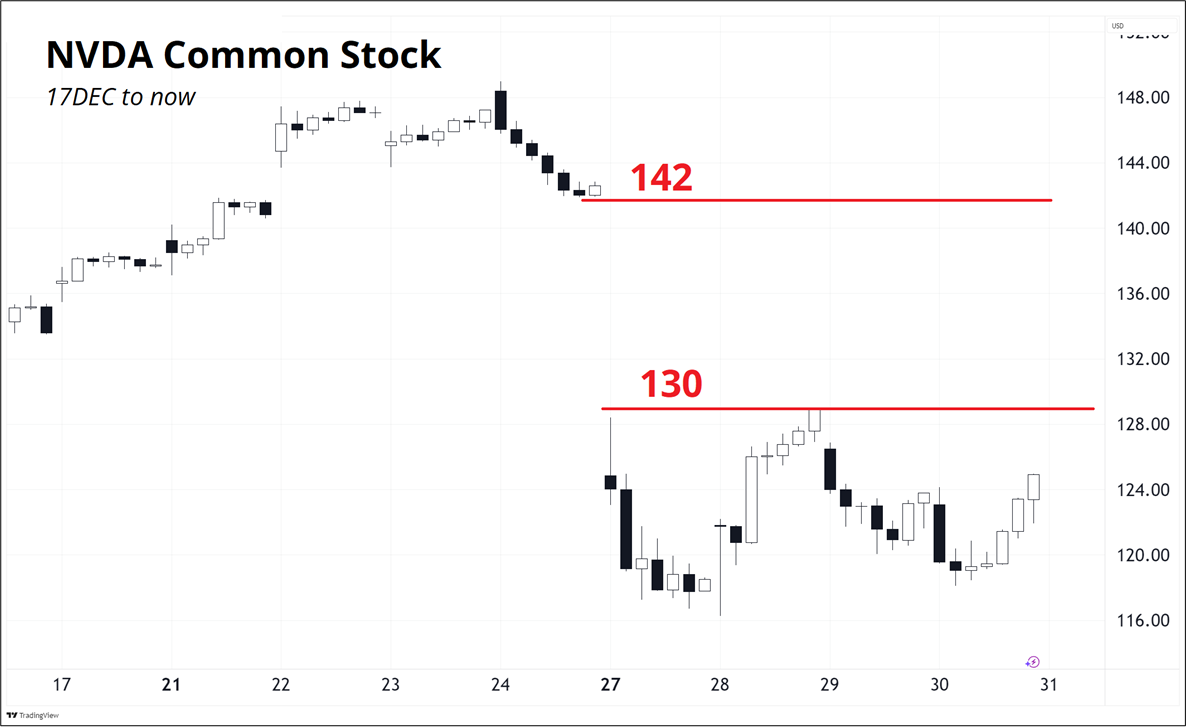

There are exactly ~~I don’t know how many~~ of these charts showing varying degrees of recovery, while the companies truly affected by this did not bounce back. Here’s NVDA:

Gaps can be extremely informative and useful when trading as they are great, obvious pivots. If you’re short NVDA, for example, your stop should either be just above 130 or just above 142. If you bought the dip, you could add on the break of 130. Etc.

The other big news this week was the IPO of Venture Global. It is the least successful IPO I can remember in all my life, and that includes the Google and Facebook IPOs, which were both duds at the time. Venture Global is a relatively new, but gigantic seller of liquid natural gas (LNG) and anything related to power generation has been in a bull market or maybe a bubble of late as the AI story includes forecasts for rapacious demand for power.

So the investment bankers thought they had a lay up. They were going to price the thing at $40-$46 for a market cap around $110B. That huge number did not fly, and they started reducing the IPO range. When the price range gets reduced, that’s usually very bad news, because it’s a clear signal that demand is weak and the thing is priced wrong.

So they dropped the range. Then they dropped it again. Finally, they ended up doing the IPO at $26. Then DeepSeek happened and the stock opened and went to $18, bottoming at a market cap of 44B. The outage for power stocks was not the only problem with the IPO as the company is also being sued for the allegedly dodgy practice of selling LNG in the spot market even though it had already contracted to sell it forward (at lower prices) to customers.

A toxic mix of bad timing, questionable business practices, and a complete whiff by the investment bankers in assessing the correct elasticity of price made for perhaps the biggest IPO turd in the last 10 years. As noted, some of the worst IPOs have been some of the best stocks to own, so who knows what happens next.

This week’s 14-word stock market summary:

Eek! The DeepSeek Freak. Much bounced, NVDA continues to trade weak. Tariffs next week?

In the last Friday Speedrun, I made the argument for why bonds should rally on a tariff announcement. It’s an easy argument to make because that’s what happened in 2018 and 2019, and after Smoot-Hawley (of course!). The confidence shock of tariffs can easily outweigh the temporary change in the price level. In the interest of full disclosure: I changed my mind. One of the worst diseases you can get in financial markets is the inability to change your mind. If you commit to the belief that a recession is coming (or already here) and then refuse to acknowledge new information as it comes in… Guess what: You will keep seeing recession around every corner. You might even torture the current data to “prove” we just went through a recession, even as stocks and yields climbed the whole time. That’s bad.

There is a tension between flexibility and flipfloppiness and honestly I would rather flip flop a bit too much than be stuck in stale views with a rigid mind possessing no Bayesian plasticity. Better flip flops than confirmation bias, every time. Keep re-aiming the bow until you think you’re on target. That’s my philosophy. When the facts change, or when you come to some new realization… Change your mind! You can always change it back.

For an explanation of why I changed my mind on the inflationary impact of tariffs, let me post an excerpt from am/FX this week.

Psychology now is not like it was in 201

Nick Timiraos had a good article in the WSJ overnight and it has changed my mind on the bond market impact of tariffs. The article is here. There are two ways you can look at the bond market impact of tariffs.

One: Look at recent history. Almost every tariff announcement in 2018 and 2019 saw bonds rally. This is a pretty good starting point for what bonds might do now. The equity-negative fear factor was larger than any inflation worries on those announcements and you could argue that’s the case today, too. I have argued that in am/FX and on the podcast with Alf in recent weeks.

Tariffs create a one-time price change that could be viewed as similar to a tax hike. It’s a step higher in the price level, but not really “inflation” per se. It also creates a negative confidence shock as foreign retaliation and risk of escalation can freeze investment in export-focused industries. Obviously, Smoot-Hawley is the textbook manifestation of a confidence shock as tariff increases (and about 20 other factors) led to a collapse in confidence and a deflationary spiral.

So that was my view. Tariffs are bullish bonds because the Fed will look through them and the economic confidence damage is greater than any one-time price level change. Until I read the Timiraos article. It changed my mind to: Two: Psychology has changed and tariffs will be inflationary. I think the key point is that inflation is a psychological phenomenon. Companies didn’t even have “raise prices more than 2%” on their list of options between 2008 and 2020. Then, the restaurants in my town realized that they could raise the price of the salmon from $17 to $22 to $31 and people would just keep on buying. An extra $9 in Uber fees and such? No problem. I’ll take two and have one for lunch tomorrow.

Even if they lost the most price sensitive 15% of their customers, the 82% menu price increase more than made up for it. This is the concept of Price over Volume or PoV that Sam Rines made famous in 2023. Companies now understand that they increase profits by sacrificing some volume to juice margins. Here’s Timiraos:

The last time Trump was president and imposed tariffs on trading partners, expectations of future inflation were low and firmly anchored—or set in dry cement. The public had little experience with inflation, and that made businesses more hesitant to pass along price increases from tariffs.

“They didn’t know how much business they would be losing” if they raised prices, said Hammack.

But several years of high inflation triggered by the pandemic and a policy response that showered the economy with ultralow interest rates and fiscal stimulus have raised questions over whether the Fed could be as relaxed about an increase in prices. If the cement is wet, expectations of higher inflation in the future could sustain higher price growth.

Because corporate management teams have been passing through higher costs, they have the experience of raising prices that they lacked five years ago. Even domestic producers that aren’t hit by tariffs could use higher import prices as an excuse for raising their own prices.

Sure, the dollar can strengthen to partially offset the inflation, but the nefarious aspect of scaled tariffs could be that they stoke inflationary expectations by putting a floor under prices, changing corporate pricing psychology, and creating a world where consumers know prices are going to stair step up, up, up as the tariff vise tightens. This could lead to front-loading, panic buying of tariffed goods, and all the usual inflationary demons that run around in central bankers’ nightmares.

End of excerpt

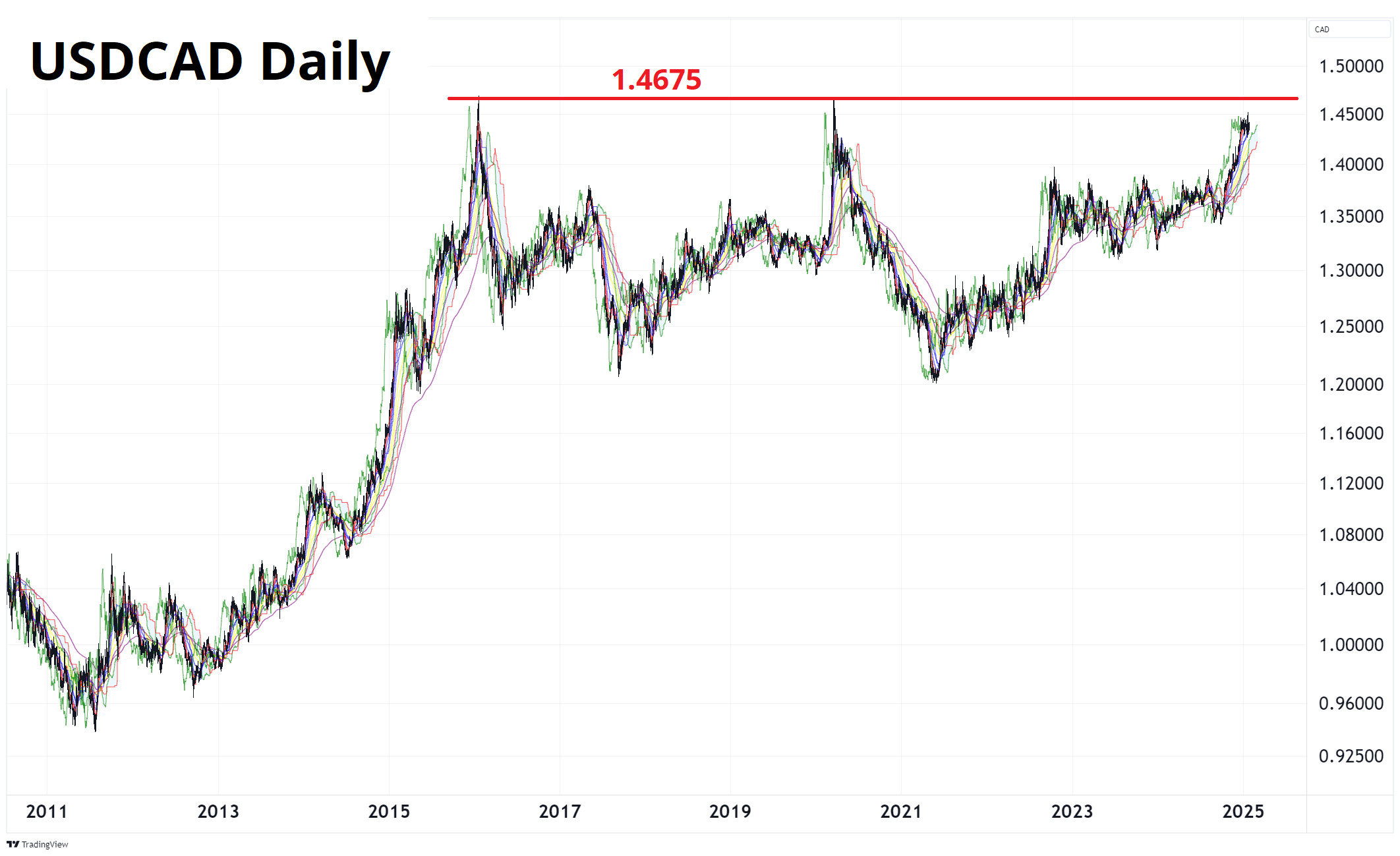

I started this section of the January 17 Friday Speedrun with: Tariffs or no tariffs? And we are no closer to the answer, sadly. The will he or won’t he continues on big tariffs for Canada and Mexico. Yesterday, Trump reiterated his plan to enact 25% tariffs on February 1 (the same thing he said two weeks ago) and his continued insistence with the date now so near triggered a sizeable pop in USDCAD and USDMXN.

The question of whether looks increasingly likely to be answer YES, but then we will quickly move to the question of “Are the tariffs real? Or just a bluff?” This question remains relevant even after the announcement of the tariffs because they won’t take force for another two weeks and therefore a heated negotiation phase will begin, and we still won’t actually know if there are going to be tariffs in real life.

I am reminded of May 2019, when this exact thing happened.

The tariff question has put USDCAD in the spotlight and it’s flying around, thinking about testing the mega double top at 1.4670.

We are also waiting for more news on a universal tariff and perhaps tariffs on China and / or Europe but the Trump Administration is using a “keep both your friends and enemies on edge” approach as he seems more interested in punishing allies than adversaries in the short term.

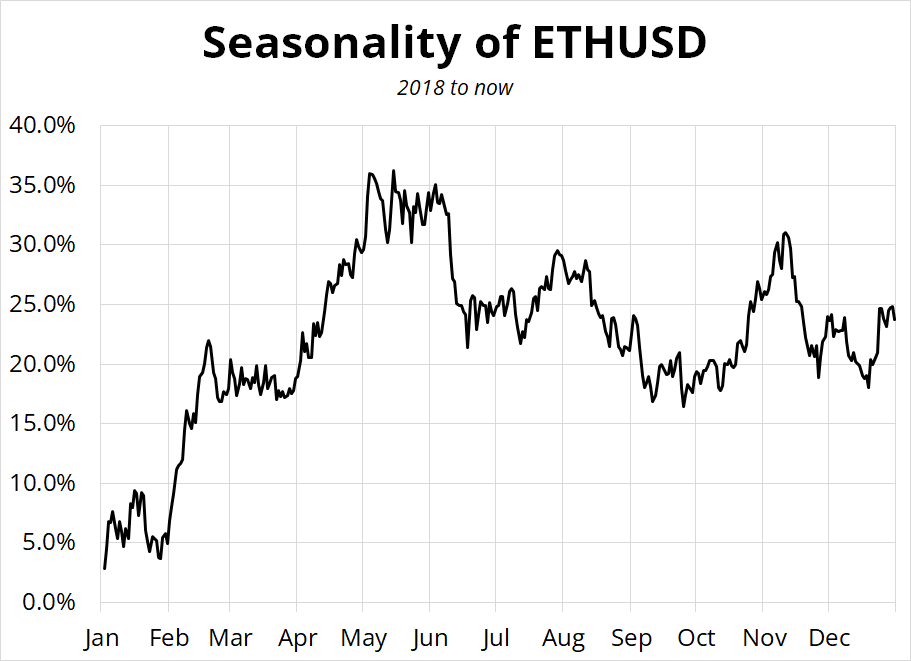

On Twitter and in am/FX this week I set out a very simple thesis on ETH. It is working pretty well so far, one day in.

You can make a decent argument for higher ETH here as it is the most hated cryptocurrency and has been mired in a horrible narrative for eons but now agents affiliated with the US government are buying it in huge quantities, it’s making a nice base around 3000, and positive seasonality starts now.

The bearish narrative (ETH has too many competitors and SOL is the better long in a memecoin cycle) has made sense for eons but maybe that story is getting a bit long in the tooth.

If this is the golden age of grift (it is), then might as well follow the grift. It’s sad, but I am not here to make moral judgments about asset prices. I am just trying to predict if they will go up or down. If a government agent is buying an asset, you might not want to be too bearish that asset.

Oil is in play with the Canadian tariff threat looming.

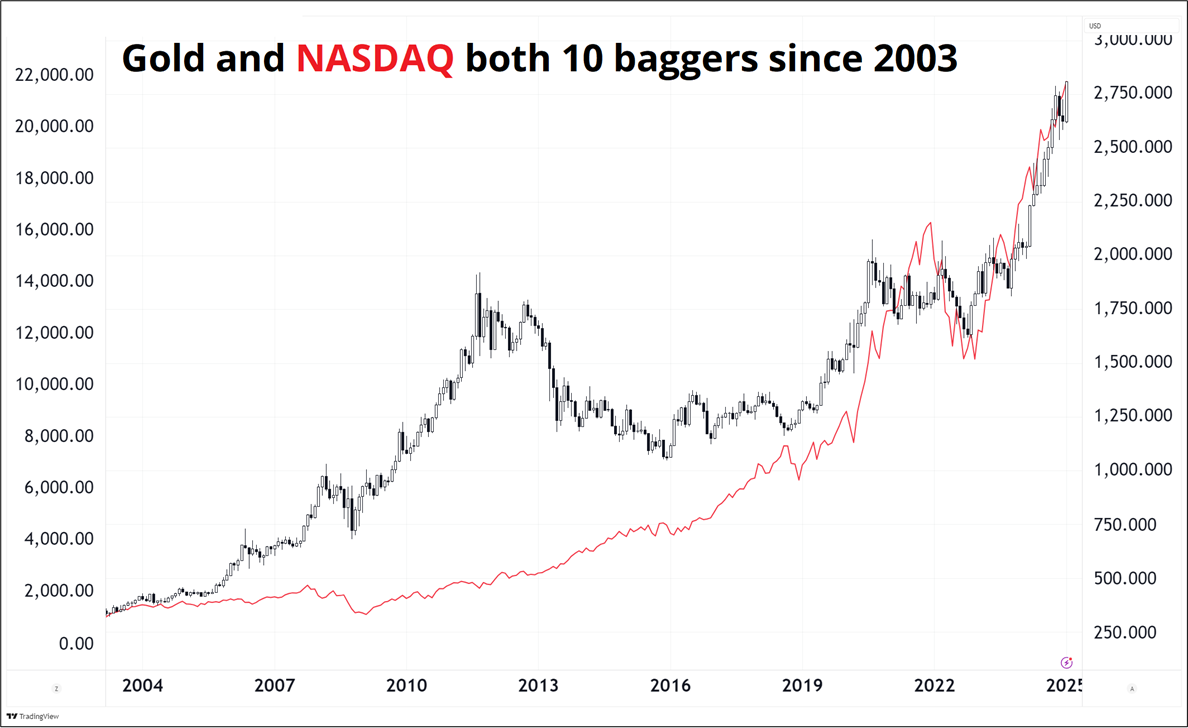

Analog bitcoin, in USD terms, (also known as “gold”) makes a new all-time high!

That’s it for this week.

Get rich or have fun trying.

An excellent article on the DeepSeek situation

If you read just one article on DeepSeek, this is a good (short) one.

*************

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.