US policy shenanigans inflict scars

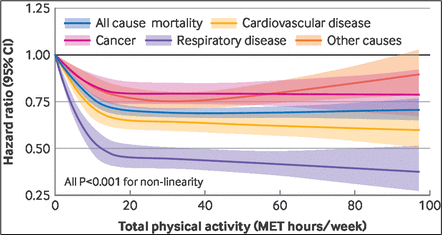

Benefits of different types of exercise (lower line means longer life)

Larger graphic at bottom of page

US policy shenanigans inflict scars

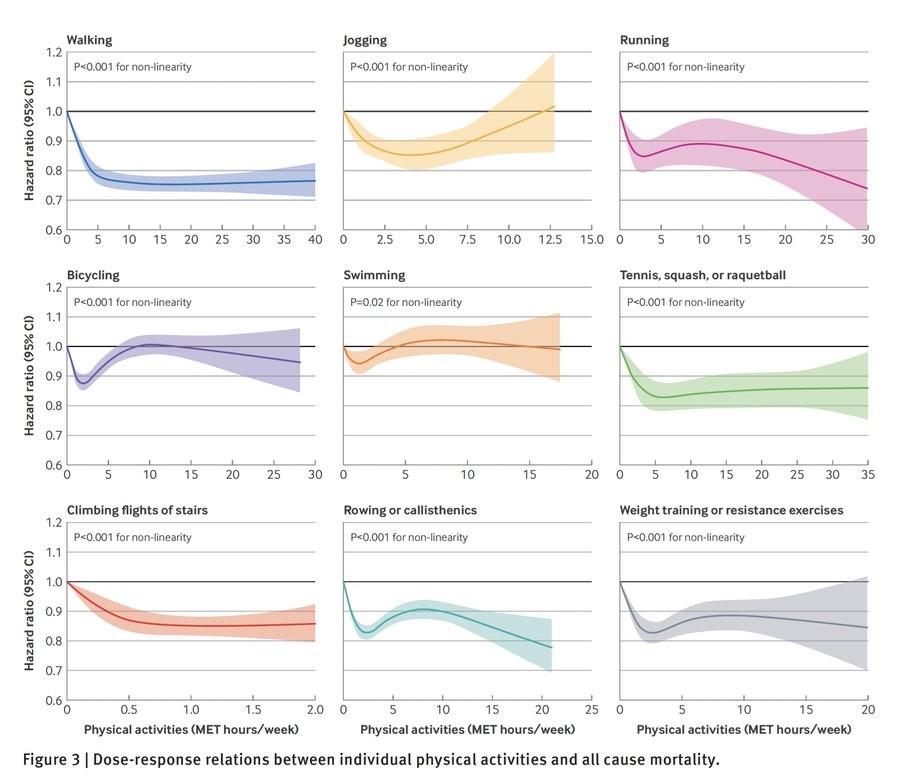

Benefits of different types of exercise (lower line means longer life)

Larger graphic at bottom of page

Flat

When people start talking about diversification away from U.S. asset markets, the biggest pushback is that it’s impossible because the other markets around the world are all too small. And as 2025 turns to 2026 and global markets outperform the U.S., you can see the demand shock idea implied there is real. Smaller markets cannot absorb the inflows in a world where people are trying to reduce exposure to the USA.

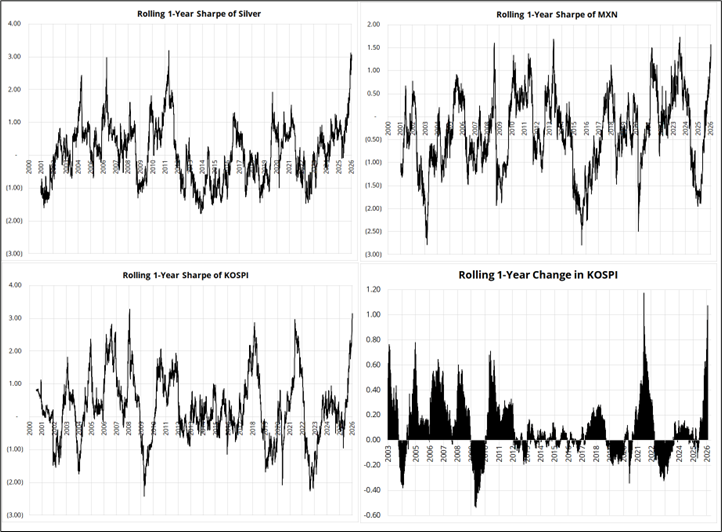

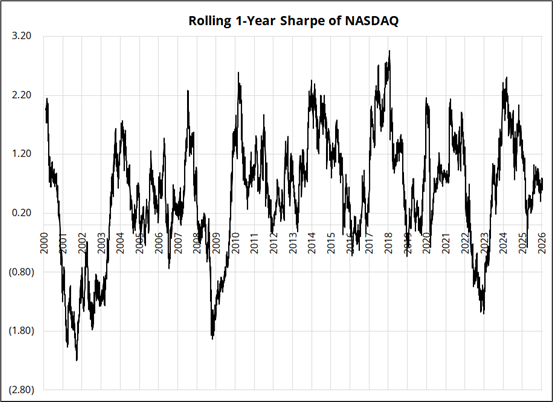

Whether it’s silver, KOSPI, Peruvian stocks, or whatever… We have seen some epic straight line moves in many assets. The charts above show three Sharpe ratios (XAG, MXN, KOSPI) and the 1-year rolling returns of the KOSPI. There are many, many assets throwing off Sharpes of 3+. Meanwhile, the NASDAQ, which was the epicenter of the TINA trade for years, is annualizing at a Sharpe of 0.61.

The huge bounce off the April 2025 lows and the still-stable capital flow data for U.S. securities obscure the fact that there has been a substantial underperformance by U.S. assets, especially for unhedged foreign investors. This week’s Greenland shenanigans will add to the overall feeling that U.S. assets, while still obviously very investable, are perhaps a bit less investable than they were. There is irreversible scarring from the policy uncertainty and that leaves two primary tracks for the USD: Go nowhere, or, go down.

There is a strong behavioral element to investment in the USA. The feeling of “there is no alternative” has pervaded for years because the U.S. has outperformed so consistently. Anyone that tried to take the other side got fired. Now, the question is how many months or years of U.S. underperformance are required before it’s “safe” to diversify? The “all-in USA” people will start to feel the fear of getting fired and looking stupid and diversification will slowly feel a bit more like the safe play if you want to stay in the middle of the herd.

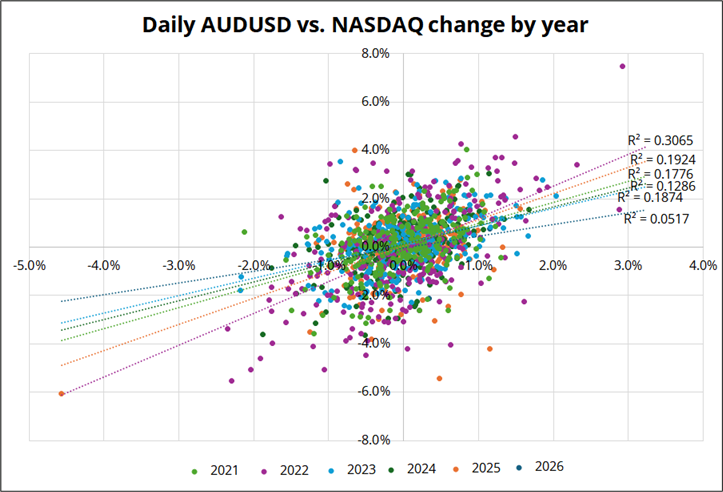

The second element that needs to be considered, especially for the USD, is the evolution of perceptions about the correlation between currencies and equities. If we get to a point where Australians believe, for example, that lower NASDAQ = higher AUDUSD, that will force a behavioral change because the negative AUD vs. NASDAQ correlation is the strongest argument for remaining unhedged. If and as correlations change and U.S. assets continue to underperform, the career risk calculus changes.

Below is a scatter of AUDUSD daily changes vs. NASDAQ, colored by year. Don’t worry too much about going blind staring at it. Just look at the flattest trendline, the one with R2=0.0517. That is 2026 (small sample size!) which shows you that so far this year, AUDUSD and NASDAQ have not scattered the way they used to. Again, the sample size is very small but slowly we could see this creep into hedging psychology if it continues. If you’re worried the U.S. is going to underperform, and you see your hedges will cost you when it does—there’s only one thing to do!

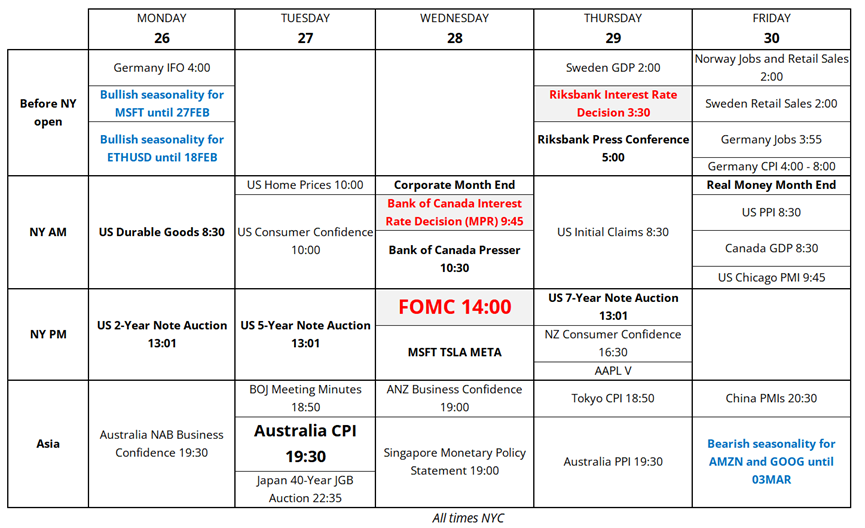

Owners of gamma should have plenty of opportunities to play Pong back and forth as we get some major earnings reports, big central bank meetings, three US bond auctions, corporate and real month end, and a bunch of other random stuff. Aussie CPI Tuesday should be strong and should take RBA hike pricing to 99%.

Below is an excellent slideshow from Steen Jakobsen at the CFA Society of Lichtenstein. Steen is a great combination:

Link to his slides: New Macro Regime: State Capitalism.

If you are in North America: May you survive the media hysteria over the coming snowstorm. And the storm itself! I am foolishly skiing tomorrow in 2F/-15C weather because a father’s love for his son knows no bounds. Pray for my fingers. And toes.

Benefits of different types of exercise (lower line means longer life)

From this paper. The paper is interesting.