It was a week of crosscurrents and contradiction

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

It was a week of crosscurrents and contradiction

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

It was a week of contrasts and contradictions this week as geopolitical fear oscillated with hopes for peace, the Fed released dovish dots and a hawkish statement followed by super-dovish commentary from Waller and stocks did their best imitation of a sin wave.

And the count of countries that have signed a trade deal with the United States as the July 9th deadline nears is exactly one. The EU looks resigned to a 10% tariff and no deal, while Japan, Canada, and Mexico all inch closer to some kind of memorandum of understanding in lieu of a deal because trade deals take months to write up, not weeks or days.

The AI and stablecoin bubblettes continue to froth their way to the moon as Coinbase announced a deal with Shopify to get Circle’s USDC rolling. COIN and CRCL have joined forces and they’re making a move to become the stablecoin standard for e-commerce. If you imagine the world two years from now, as Stanley Druckenmiller urges investors to do, it’s pretty easy to see a world where Mastercard and Visa no longer dominate online payments and I’m using Apple Pay to pay for stuff online with USDC on the Coinbase platform. Whatever stablecoin can achieve e-commerce interoperability first and capture the network effects of a global payments system begging for disruption will collect some serious rent from consumers in the 2030s.

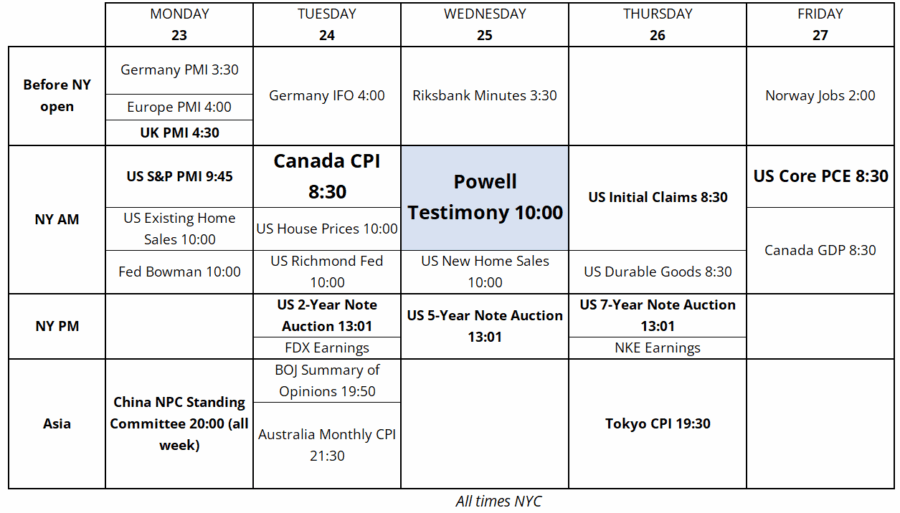

The economic data was boring this week, as were the central bank meetings as the Riksbank was dovish (EURSEK much higher), the SNB was as expected, the BoE was snoozy, and the FOMC delivered a mixed bag. I will be off for the next two weeks travelling, so here’s next week’s calendar for your planning pleasure.

The American stock market cannot breach the no-fly zone in the NASDAQ = 22300/22400 area and we continue to chop around. Missiles lighting up the night sky in the Middle East keep investors on edge, but everyone knows that everyone knows that geopolitics don’t matter for MAG7 earnings and so it’s just as scary to be short as it is to be long. Here’s the NQ this week:

This thing closed at 21660 last week, so that’s a lot of noise into June expiration. Those little red lines show the point of control for each day and you can see that 21900/22000 has been equilibrium all week with various dips and rips on headlines and random supply / demand imbalances.

Stocks remain antifragile as bombs drop nightly in Iran and July 9th is creeping closer. I guess people have completely forgotten about tariffs as we continue to wait to see any impact on any data other than erratic survey responses that simply follow the S&P 500 up and down. I was of the view that the bad sentiment data would flow into bad hard data at some point, but the process is so paleolithically slow that it’s hard to hold onto much conviction. Inflation may go up due to tariffs, but there is also a non-zero chance that price hikes will be small enough that they don’t show up as they’re offset by services disinflation.

Claudia Sahm’s writeups are always excellent and in her latest, she opens the door for the possibility that tariffs will be offset by disinflation while still acknowledging the base case is probably that we just haven’t waited long enough yet.

https://stayathomemacro.substack.com/p/what-are-inflation-surprises-telling

On April 25, I made a graphic, and it remains relevant. The problem is market time is slower than economic data time. Each day, markets go up and down and news comes out and algorithms interact with fearful and greedy humans, and each month feels like a year, and each year feels like a decade. We can’t wait around for confirmation of a thesis—tariff uncertainty will freeze hiring and boost inflation—that might not ever come true. We need evidence of recession or stocks drift higher.

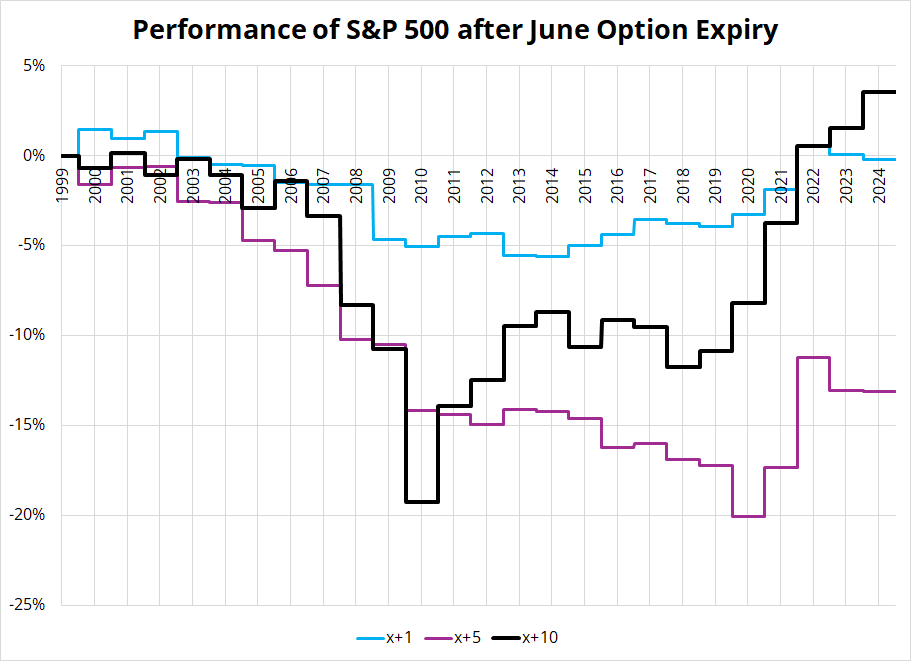

There used to be this theory that stocks sell off after the major option expiry dates because portfolio managers and such need to reload their puts as part of a properly hedged book and/or speculators love to be bearish and so they need to rebuy the (usually worthless) puts they bought last quarter. There has been a massive change in market dynamics post-COVID, though, as calls are the drug of choice for speculators, and “Stocks only go up” has become an unironic investing strategy.

If you look at the performance of the S&P 500 after June expiry, you can see that pre-COVID, the price action was generally bearish and post-COVID, it flipped bullish. This chart shows running P&L of long S&P 500 at the close on June options expiry, closing it out 1, 5, or 10 days later.

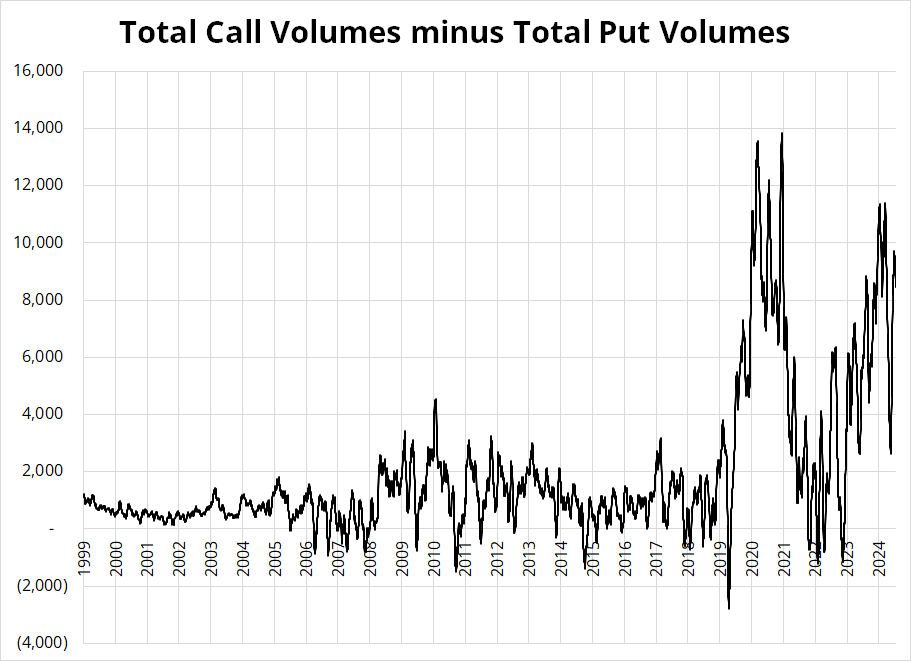

Confirming evidence of a switch in the supply/demand dynamic for puts and calls can be seen if you look at total call volumes relative to total put volumes on all US exchanges. Everyone has seen the chart of call volumes exploding from lower left to upper right, but this is a bad metric. You need to look at the relationship between call and put volumes because put volumes have also exploded.

The more short-dated options people trade, the larger the overall volumes are going to be because short-dated options have lower nominal price tags (despite higher IV) and so even if the world was spending the same amount of money on options (they’re not!) … You would see higher volumes if speculators moved to shorter and shorter dates. What’s actually happening is that interest in options has exploded and most of that interest is in the very front end.

Also note that the demand for calls is highly procyclical and contributed to the bubbles in 2021 and the maybe-bubbles right now in stuff like CRWV, PLTR, and CRCL.

Hard to get super excited about long stocks at the all-time highs with the July 9th tariff deadline approaching and missiles crisscrossing the night sky in the Middle East. But that’s why it will probably work.

This week’s 14-word stock market summary:

Up down sideways and diagonal. Geopolitics are scary. Tariffs are forgotten but not gone.

Chris Waller has decided to head a strongly dovish charge at the Fed, even as the rest of the committee seems more interested in a wait-and-see approach.

*FED’S WALLER: COULD CUT RATES AS EARLY AS JULY MEETING

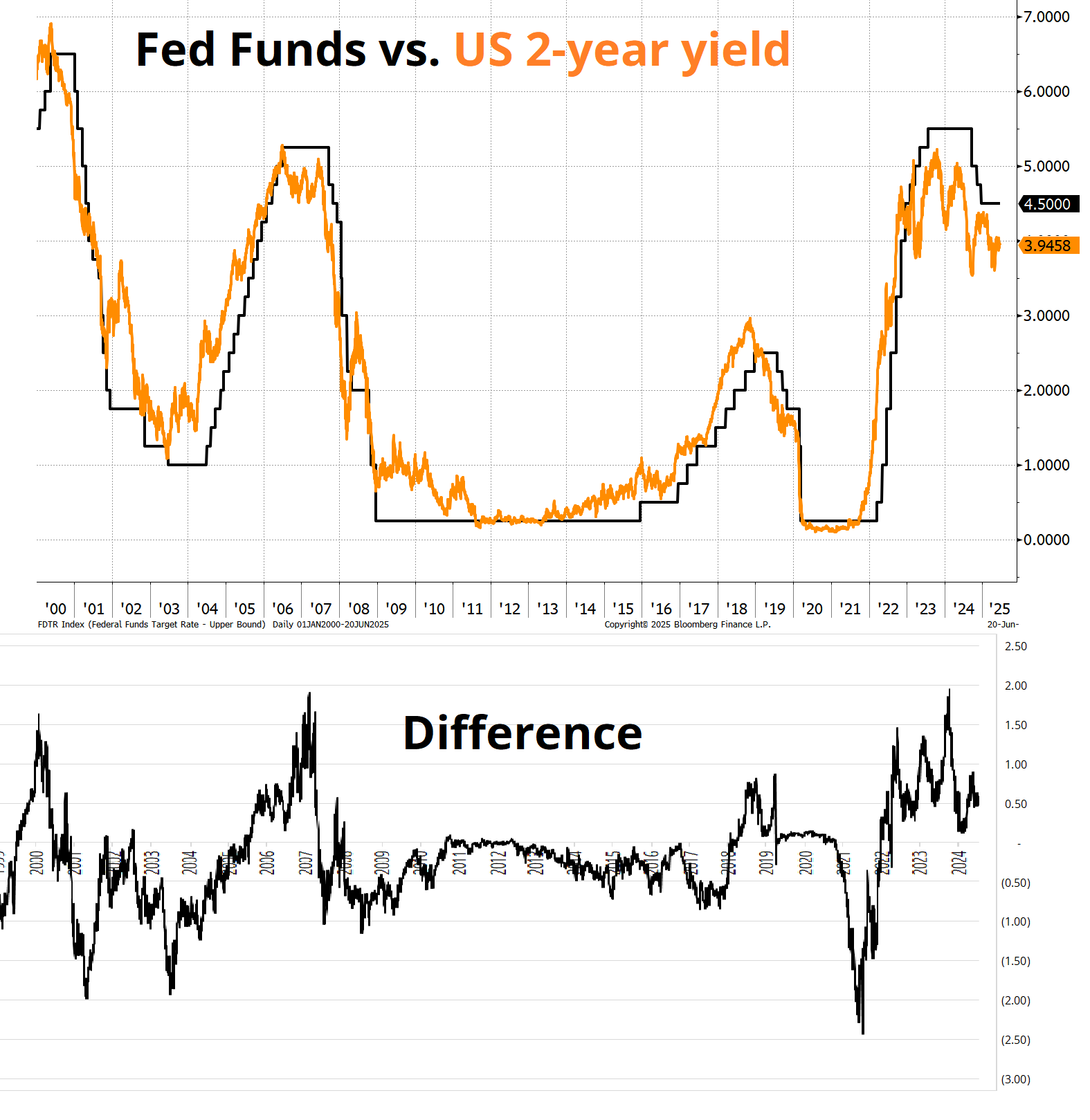

His thinking might be that if there is a bit of flex in July FOMC pricing, that creates a feedback loop where the psychology of the Fed is amenable to at least thinking about thinking about a cut. If July FOMC is priced at 14% chance of a cut, the Fed won’t cut. It’s circular as they can guide the market or the market can guide them, depending on the circumstances. You can see 2-year yields lead on the way up (orange line) because the Fed hates hiking and only does it when it’s absolutely forced to do so. Fed Funds and the 2-year yield go down in synch because the Fed leads the way ‘cuz they love to cut.

Anyway, Waller continues to lead the dovish camp, but I am not too sure how many others are with him at this point. He’s like Jerry Maguire standing up in the middle of the office yelling: “Who’s coming with me?”

I guess in this analogy Austan Goolsbee is Renée Zellweger?

Nobody has a clue on 10-year yields as the Big Beautiful Bill is not at the forefront of the narrative right now, CPI is soft but could unsoften in coming months, Atlanta Fed GDPNow is booming on a snapback, and the US jobs market is deteriorating veryyyyyyyyyyyyyyyyy slowly. Too slowly to matter much for bonds so far.

The market has completely given up on the short USD trade, even though EURUSD is not at all far from the highs. This is probably a good setup if you are bearish USD because the market is asleep at the wheel here and USD rallies remain fleeting.

The BIS published a good piece on the April FX story. You can read it here:

https://www.bis.org/publ/bisbull105.pdf

AUDUSD can’t get out of its own way, but does look keen to try the topside again sometimes soon while the JPY has no friends and the JPY-bullish narrative has decayed to the point where I couldn’t even tell you why you would want to be long JPY at this point. The BOJ continues its radical, unorthodox policy despite a doubling in rice prices and rip roaring inflation in Japan.

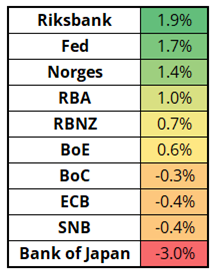

A super basic way to calculate real policy rates is to take the current central bank rate and subtract current Core CPI. That’s not very sophisticated, but it’s easy to understand. Here’s how that measure looks across some of the majors.

Japan. What you doing?

So the killer use case for crypto ended up being that the government and Blackrock will buy it, unprofitable businesses will hoard it in a cynical attempt to find exit liquidity, and centralized big fintech will use stablecoins as a payment method to usurp V and MC. Interesting turn of events that reinforces crypto’s chameleon quality. It can be whatever people want it to be. Remember OpenSea?

I don’t really get why bitcoin trades so poorly of late, but I suppose it’s just consolidating near the all-time highs, same as NASDAQ.

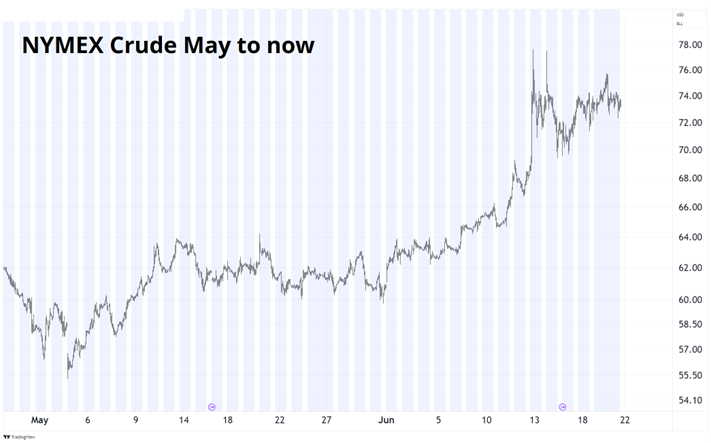

Here’s what oil has been doing throughout this war between Iran and Israel.

It has held in much better than I would have expected. I suppose until the missiles stop flying, there will be a $7 premium embedded in the price and that premium will either go back to zero, or it will go to $25 if Iran’s oil production is compromised or the Strait of Hormuz sees a stoppage.

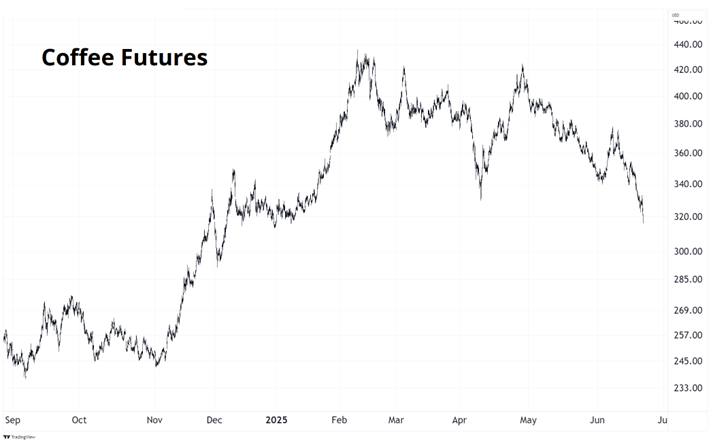

Elsewhere, silver made a new 13-year high but lost momentum above $37 and gold is chilling. Coffee has completed its 2025 round trip. 320 to 420 to 320.

That’s it for this week. I am off ‘til July 7. Be nice.

Get rich or have fun trying.

*************

This excerpt from the Quran should resonate with all the traders out there:

My Lord, cause me to enter a goodly entrance and to exit a goodly exit and grant me from Yourself a supporting authority.

(Surat al-Isra’ 17, Āyat 80)

https://academyofislam.com/quranic-reflection-no-530-ayat-1780-a-good-entry-and-exit/

*************

*************

Gambler to himself: I like those odds!

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.