The rocket ship to Venus is running low on fuel.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

The rocket ship to Venus is running low on fuel.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Last week I discussed how macro was dead and I may have accidentally nailed the top in that narrative as macro is back this week and we are seeing many movements tied to a stronger U.S. economy, the inflationary impact of the war in Iran, and political kerfuffles in Brazil and the United Kingdom.

U.S. data is running hot and American Exceptionalism is back. CPI is in the sky and PPI’s begun to fly as the double blockade of Hormuz continues and the weeks tick by. Tick tick tick. Commodity, shipping, and supply chain experts continue to warn that the shutdown of the Strait will eventually lead to various supply shocks and while those forecasts feel a bit stale as we complete week eleven of the war, it’s impossible not to wonder if there will be a day when the giant supply shock wave might reach our shores. JPM issued a much-circulated note saying that the Strait will open by June 1 because it will be too painful if it doesn’t, but many experts (including Helima Croft of RBC, who I hold in high esteem) disagreed. Here’s JPM:

“A core assumption of our framework is that the accelerating pace of oil inventory depletion will ultimately force the reopening of the Strait of Hormuz, one way or another. Our base case envisions the Strait reopens in June—anchored on June 1 for simplicity—following a clear and credible announcement ratified and confirmed by both sides, such as a statement from the UN Security Council.”

Okie dokie. It is fair to say at this point that all calls for inventory depletion and supply shock etc. should be taken with much pink Himalayan salt because we were warned that Australia was going to run out of gasoline by mid-April and agricultural prices were going to skyrocket and so on and yet the wheels of capitalism continue to turn and still appear to be fairly well greased. Maybe it’s a binary, nonlinear thing, or maybe the miracle of capitalism will find a workaround. Hard to say.

Regardless, the market is starting to price in Fed hikes as the U.S. labor market remains in equilibrium and inflation is soaring again. It’s easy to say that the inflation is transitory and it’s a one-time price level change due to a war, but central banks also need to worry about second-round effects. If the owner of a restaurant in my town watches the news and sees it’s $85 to fill up his truck instead of $70 a few months ago, he might raise the price of the salmon entrée from $31 to $35 in anticipation of higher input costs. He might also see the inflationary things going on and simply make the calculation that if he raises the price to $35 and volume drops 5%, he’s still going to make more money.

Before COVID, prices just crawled higher and businesses put little thought into pricing because inflation had been stable for 15 years. Now, this is not the case. Every company and small business in the world is willing to test the waters with price hikes at a moment’s notice because they saw that price hikes did not impact volumes that much in the 2020 to 2025 period.

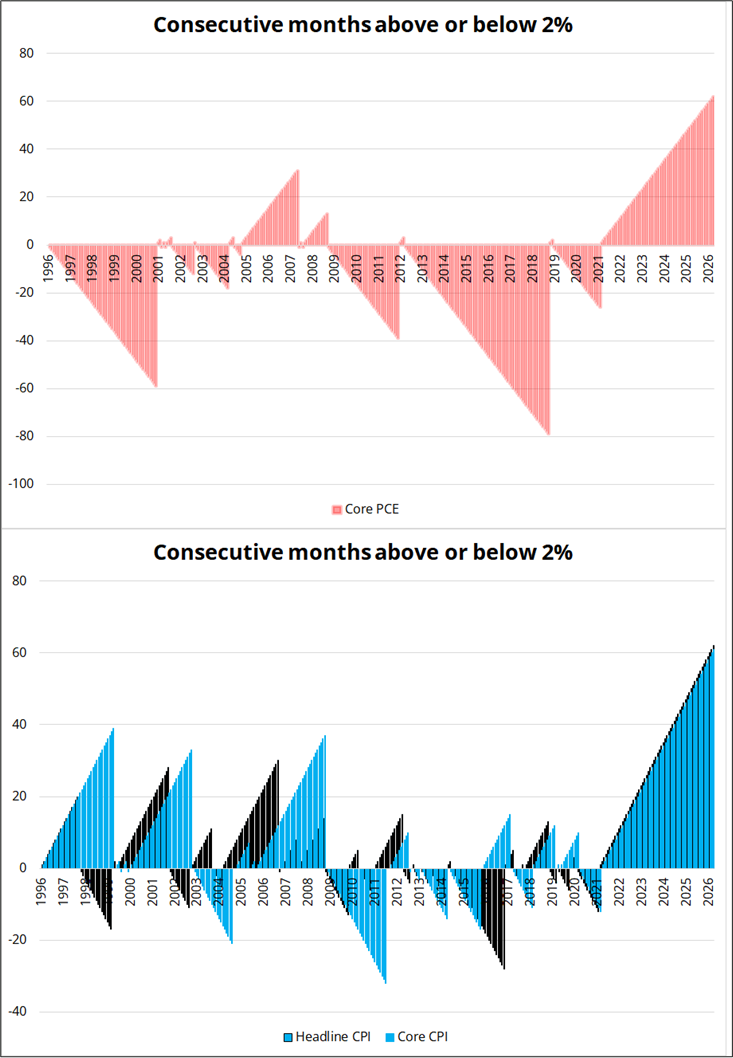

So, it’s not safe for central banks to just look through the oil price rise and shrug. That said, one can reasonably wonder if the Fed even targets inflation anymore as inflation has been way above target for more than five years. They just keep saying “Inflation will be at 2% in two years” over and over.

If you are a funny person, you might say that the Fed’s Average Inflation Targeting strategy (FAIT) worked well because they missed the target on the low side for five years then on the high side for five years. Ha.

On top of the war, you have a continuation of extreme loose fiscal policy in the U.S. as the new normal playbook is on infinite repeat: Campaign like you want smaller government, then double down on Big Government when you get in. Keynes proposed deficits as a stabilizer during times of economic weakness, but the new normal is just big deficits all the time. Keep cutting revenues (lower taxes) and increasing spending (interest costs, wars, health care, etc.). And obviously COVID was a massive shock to the balance sheet, too.

Meanwhile, the AI Capex boom is using a ton of resources and keeping some regional labor markets tight and helping stocks continue their flight to Venus. The rocket to Venus is getting low on fuel now, though. I’ll explain in the section in stocks.

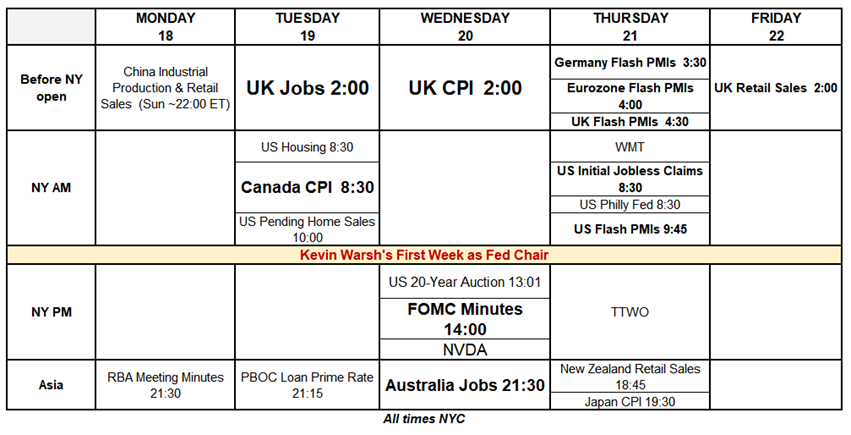

Kevin Warsh takes the helm of Starship FOMC next week, and the crazy reality is that his first move could be a hike, not a cut! If you told someone this a year ago they would have thought you were bananas. But inflation is bad. At some point the central bank will have to do its job. I would not at all be surprised if Warsh and Waller are both sounding hawkish by mid-summer and the Fed hikes in December.

Here’s next week’s calendar. NVDA Wednesday is a highlight.

Stocks continue to fly with semis and computery stuff skyrocketing Monday to Thursday along with healthcare stocks, and big box retailers. Here’s the week in review before Friday’s carnage:

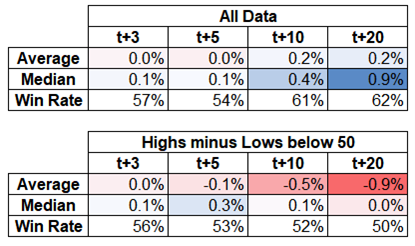

Some of this week’s rally has been fueled by gamma and microstructure type stuff (QYLD hedging, etc. etc.) that will come to an end today. It is also notable that while the S&P 500 is making new all-time highs every day, the number of NYSE 52-week lows exceeded the number of 52-week highs a couple of days this week. That is highly unusual and it’s bearish.

The average reading of 52-week highs minus 52-week lows on all-time high days is +150. We got as low as -19 this week (Wednesday).

The table here shows forward performance data of SPX after it trades an all-time high, conditional on the 52-week highs minus lows. I used a filter of <50 and the degradation of performance is somewhat linear as you lower that bar.

This is just one thing, but we have also seen a couple of days of VIX UP + SPX UP this week (that’s also a bearish condition for 20-day forward performance).

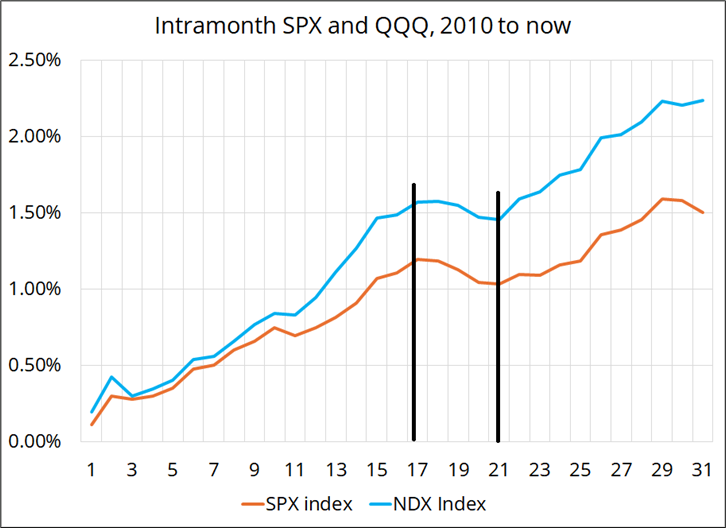

When you backtest a strategy or effect in equities, you almost always find the output is bullish because the trend of the asset (SPX or NDX) is massively bullish. Therefore, it is hard to find studies or backtests that put out bearish strategies. That said, it’s interesting that the period after expiries (17th to the 21st of each month) backtests flat to bearish. The 401k buyers and gamma hedgers and general inflows are absent in that short period.

I pointed out some of this stuff on Monday and Tuesday in am/FX, but said I was going to wait until closer to the end of the week to get short because I was concerned the gamma squeeze / forced buying would continue. In Thursday’s am/FX, I finally went tactically bearish stocks for a one-week trade. Here’s a tiny excerpt:

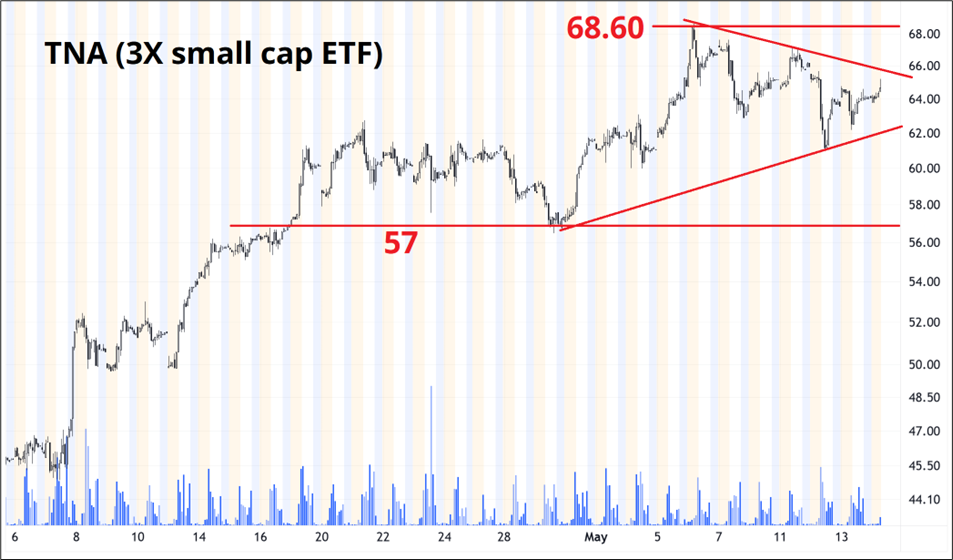

I wanted to wait until closer to the end of the week. Now, we are close to the end of the week and I want to be short stocks into the weekend. Pick your poison, I suppose, with the juiciest downside in the most-volatile stocks (SNDK, INTC, etc.), or you can always sell Russell and avoid the idiosyncratic AI capex headline risks. I like that idea best and I tend to use TNA (the 3X Small Cap ETF) as a good short vehicle when I am bearish like this. In TNA, the idea would be to sell around here (64.60) with a stop loss at 69.11, looking for 57.57. Risking 4.51 to make 7.03.

This is not investment advice! My view could change at any time! I will put it in the sidebar as my conviction is high that tactical short stocks for the next week or so is positive EV. Here is a chart of TNA.

So there you go. That’s my view.

Here is this week’s 14-word stock market summary:

The rocket ship to Venus is running out of fuel. It could momentarily stall.

https://www.spectramarkets.com/subscribe/

Bonds are becoming a concern again as the U.K. political story heats up and global inflation spikes as Iran flexes its control of the Strait of Hormuz. Bond market volatility has been low but could pick up now because central banks don’t have the bond market’s back, and inflationary psychology from COVID threatens nearly-immediate second-round effects.

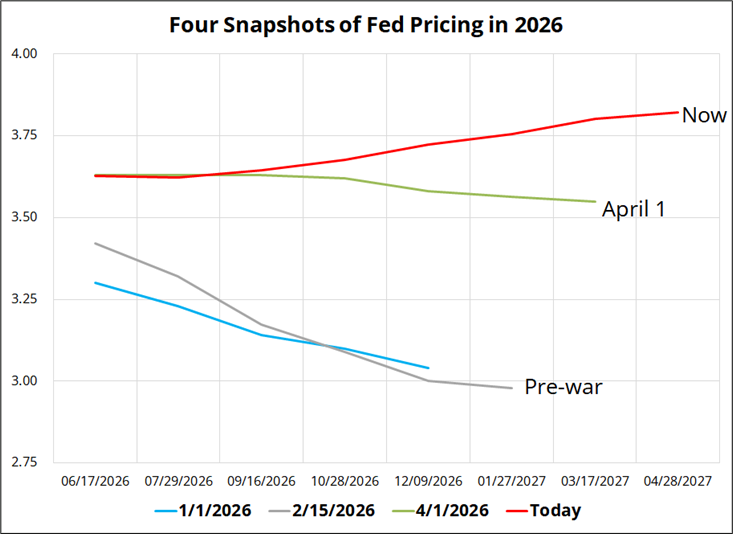

The big story is that the market is now pricing about 20bps of hikes for the Fed. This is in stark contrast to dreams of multiple cuts at the start of this year. Check out these four colored spaghetti noodles:

As I mentioned, I believe the market is not crazy to price Fed hikes here. Inflation could be a major political issue into midterms and the magical fantasy that a president can tell the Fed to cut rates to 1% and that makes any sense in the real world is closer to being dispelled. Warsh is the most orthodox, elite, $5000-suit, Morgan Stanley pedigree candidate for Fed Chair. Hassett, he is not. And there is zero shot the committee will vote for rate cuts in this sort of economic regime, regardless of what he says.

I can’t wait to see what Waller thinks about all this. Unfortunately, he’s not scheduled to speak as of right now.

The long end of the bond market is screaming in pain again.

I had been wondering why the dollar wasn’t reacting to the strong U.S. data and equity outperformance early in the week, but the USD is playing ball now and moving higher as U.S. Exceptionalism returns. American equity markets are outperforming once again as AI wins and boring stuff loses.

People thought they wanted to own foreign stocks there for a while, but have now decided that the USA is okay. America was briefly so over, but is now incredibly back.

So EURUSD finally buckled, a bit.

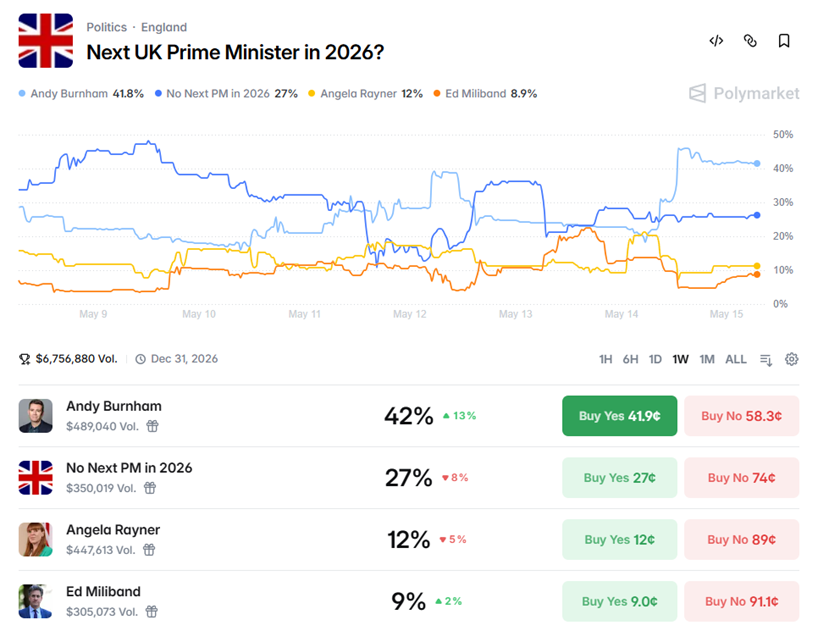

GBPUSD buckled even more as it looks like there is another change of PM coming soonish if Andy Burnham can win a by-election on or around June 18.

This has roiled gilts, a bit, and got people worried about what’s next for the UK deficit story. A chart of GBPUSD looks the same as the chart of EURUSD as GBP went from 1.3600 to 1.3350 in pretty much a straight line.

Congratulations to Phil Valori for calling this move as he went short above 1.36 into the month end madness and has ridden the view down to here. The market mostly whiffed on this GBP move because a) the market is asleep and not really paying attention to G10 FX and b) the UK politics merry-go-round is kind of boring and it’s not always clear whether there will be a market reaction to something so familiar.

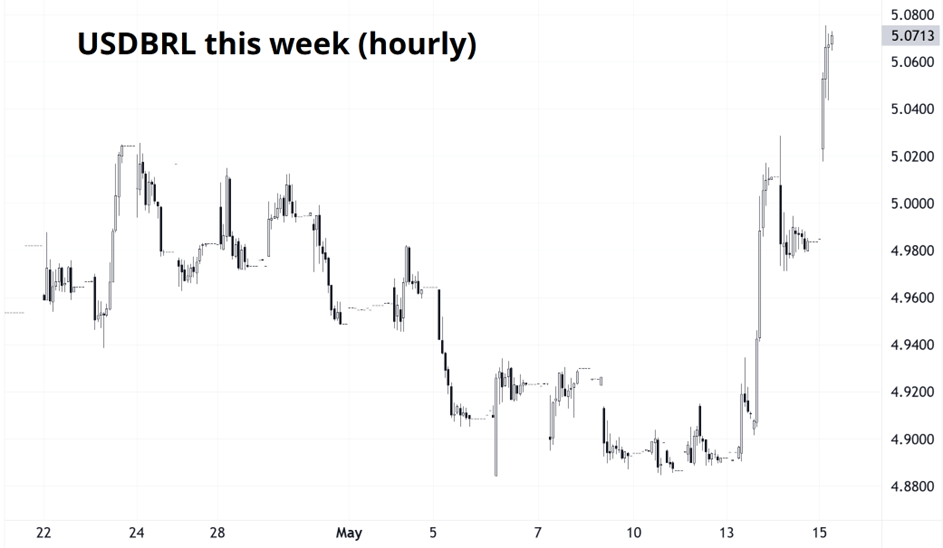

Finally, Flavio Bolsonaro has been called out in an extremely detailed Intercept article and his odds of winning the Brazilian election this October have dropped from around 44% to 33%. This is viewed as bearish for Brazil because markets don’t want to deal with another Lula term. So USDBRL, one of the more popular trades in macro because of it’s high carry/vol ratio, did this:

That’s not a massive move, but it’s enough to cause a bit of wriggling in the seat for anyone with a large position. Many FX pairs are now filling the gap that opened up after the ceasefire on April 7.

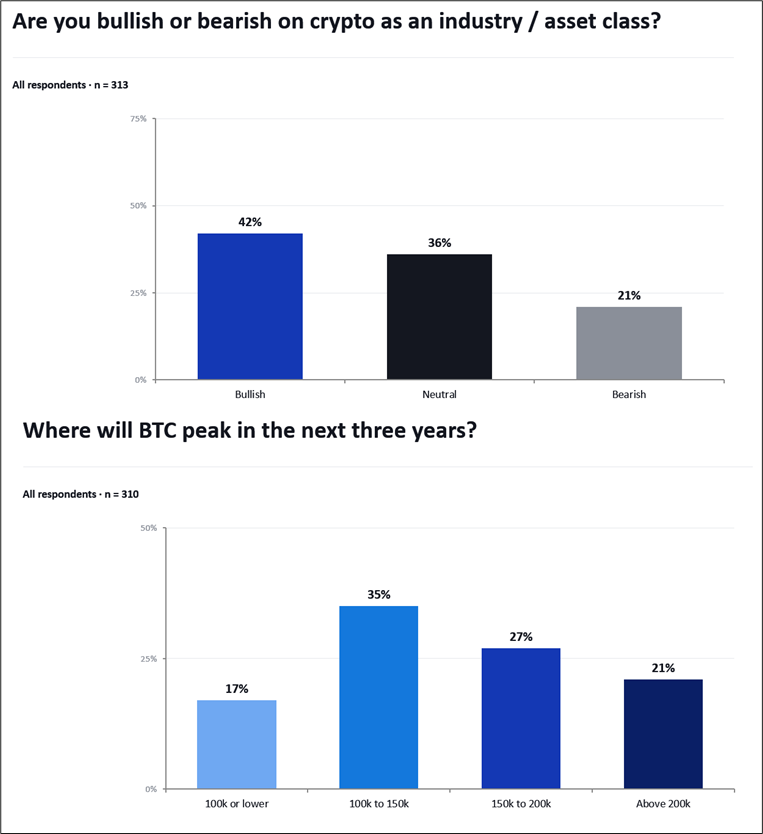

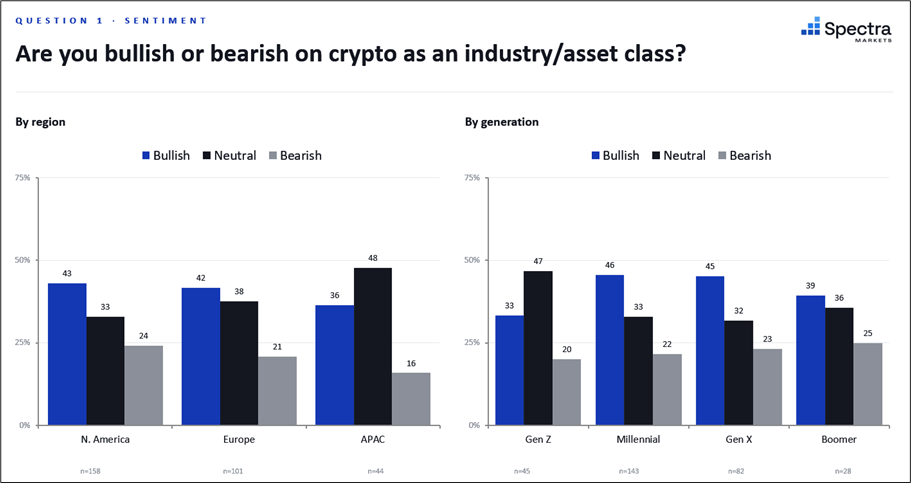

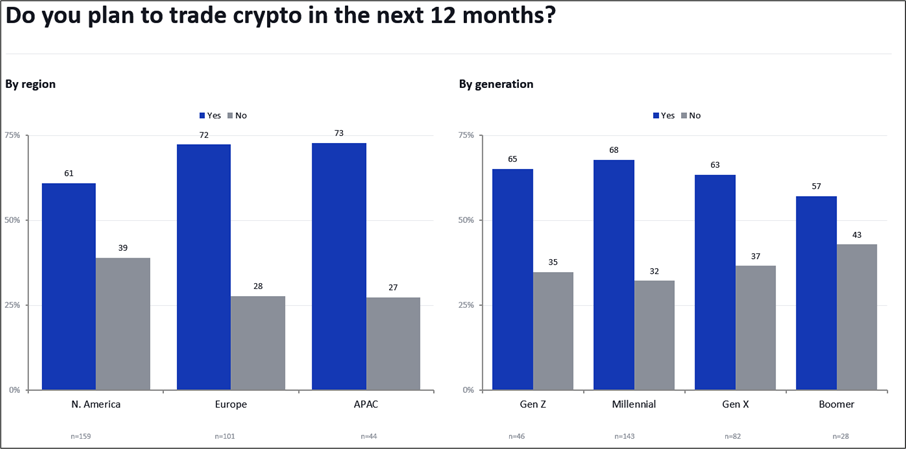

Here are the results of my crypto survey from last week:

By region and age group:

This slide confirms what I have gathered from speaking to my sons and their friends: GenZ is not as interested in or bullish crypto. I would read this entire slide as more bearish than the real consensus because my readers skew TradFi and that skews less bullish crypto overall. But the relative breakdown across ages and geography should be fine to interpret as is. In coming years, the crypto industry will need to find some new, believable bull narratives to convince younger people that crypto isn’t just altcoin scams and/or another Wall Street product backed by big government.

And finally, you can see a bit less enthusiasm in North America vs. the rest of the world. I removed Middle East data because there were only 9 respondents and I apologize to South America as I meant to put “Americas” and I put “North America”. Whoops! LATAM: YOU STILL EXIST!

Honestly: This is not the most interesting survey result I have ever published. It is what it is.

HYPE and PURR both had a nice week, and I am noticing more and more that almost every smart person I talk to in crypto seems to love those. I honestly cannot say if that is bullish or bearish. But it’s interesting and it makes me watch HYPE and PURR more closely. There seems to be some there there.

https://news.bitcoin.com/hype-jumps-17-after-hyperliquid-grants-coinbase-rights-to-usdh-assets/

Gold is trading like a risky asset as the back of the bond market blows out again. I feel like this is the zone where you try to buy the dip if you’re a longer term person playing for a move back to the all-time highs. Bullish gold and long USD is a weird combo, but it can work.

Meanwhile, crude is approaching the apex of a huge triangle. The direction of the break has important ramifications for global asset prices of all stripes.

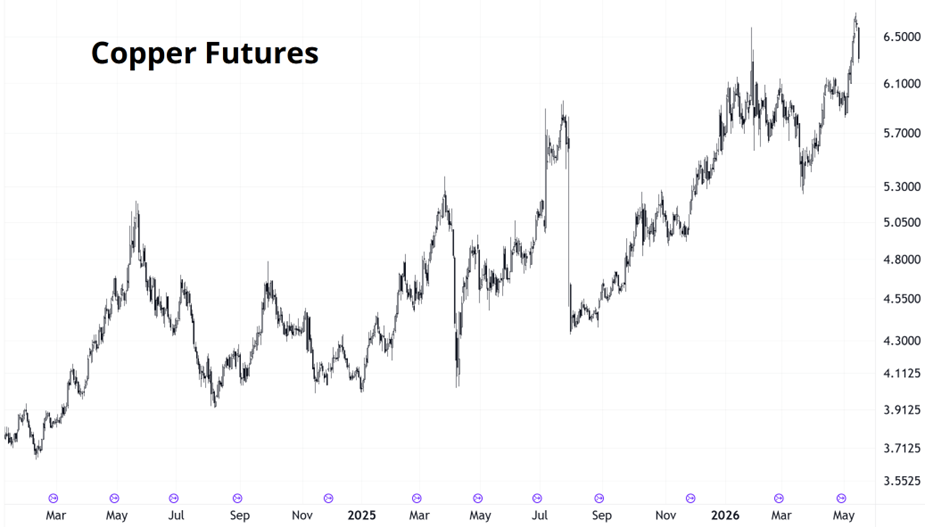

And copper continues to go up the escalator and down the elevator in a strong but scary up trend that started in 2024.

I would think if the bond market doesn’t turn around, copper will get scared soon as the tightening of global financial conditions will threaten lower global growth.

That’s it for this week.

Get rich or have fun trying.

*************

Absolutely insane directing and choreography here (Yung Lean music)

*************

Can you see where the Fed lost control?

*************

The Prodigy: Breathe ————– One of the great tracks of all time.

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.