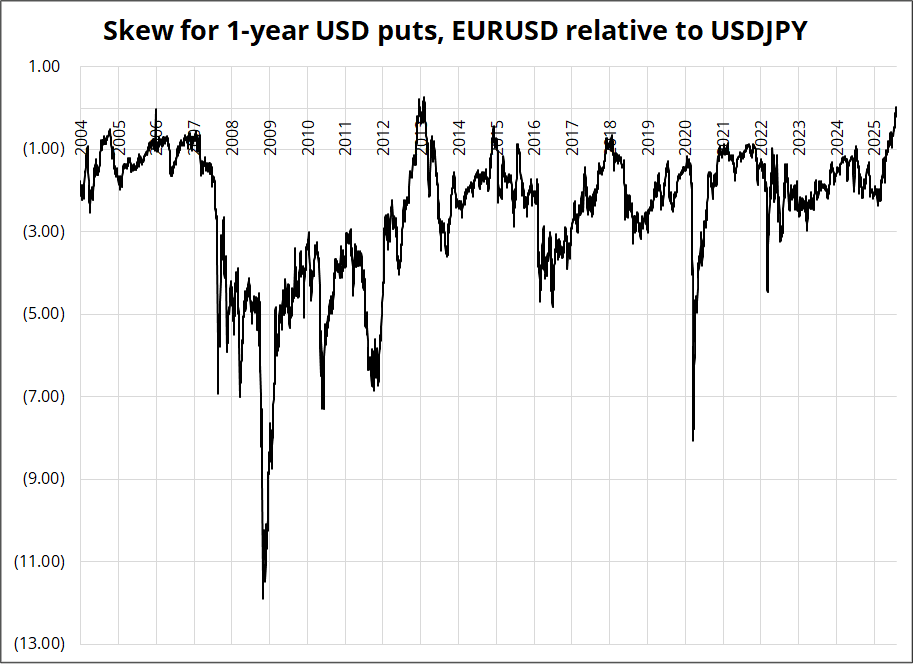

The euro is gaining safe haven status relative to the JPY.

Distribution of global population by latitude

The euro is gaining safe haven status relative to the JPY.

Distribution of global population by latitude

Long 26AUG 1.8050 EURAUD call

Cost ~36bps Spot ref. 1.7790

Long 26AUG 0.8760 EURGBP call

Cost ~33bps Spot ref. 0.8680

Tim Power pointed out that something unusual is happening in the vol market as the market appears to be viewing the EUR as relatively more of a safe haven than JPY vs. history. Here’s the chart:

This probably reflects:

The rip in 2013 was the result of Draghi’s “Whatever It Takes” speech and was probably more about unwinding “THE END OF THE EURO” trades than it was about strong EU credibility. This time, the change could be more structural. This has implications for portfolio hedging (EUR/XXX better hedge for SPX weakness than XXX/JPY, etc.) and it’s also relevant to correlation traders. If you think the VIX is going higher, you might be better off long EURAUD than short AUDJPY, for example.

Some of this will depend on why VIX rises (if it does). If it’s because of stagflation or higher bond yields, EUR will almost certainly be best. If it’s because of a US recession, JPY could still outperform and the options market will mean revert aggressively back towards more historical norms.

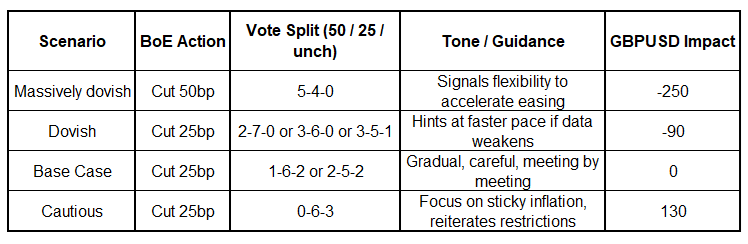

The BoE meet tomorrow and while there’s a pretty good chance it’s a 2-5-2 nothingburger, it’s worth being ready in case it’s not. The UK faces a more extreme version of the same problem faced by the Fed: Falling demand for labor and sticky inflation. At some point a central bank facing stagflation has to choose which is the lesser evil.

The vote split will be the key to determining which way the BoE committee is leaning. Here is the distribution of 26 economist forecasts.

And here’s my assessment of the outcomes and their potential impact on cable.

I have the late August EURGBP call and feel like it’s probably not a bad thing to own as EUR continues to trade well and the Bank of England has looked through high inflation before. In 2008 and 2011, inflation was sky high in the UK and the Bank of England never budged. The Bank of England just kept sending letters until inflation got back down below target again. To quote one from 2011:

“The key consideration for monetary policy is the outlook for inflation in the medium term, and the balance of risks around it, rather than the current rate of inflation.”

The BoE has OK logic and some history on their side if they decide to take the medium-term view that employment is the real problem to be dealt with, and inflation will subside over time.

A fun thing I learned while preparing the chart above is that Bloomberg houses data for the Bank of England Base Rate all the way back to 1910. Neat.

The DSI for corn is below 10, which puts it in the 97th percentile for lowest readings. I know nothing about corn, but if you’re working on a bullish thesis, this is something you can add to the mix.

HT CnD :]

Have a corny day.