We eagerly await Trump’s actual policies while feverishly speculating on what they might be.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

We eagerly await Trump’s actual policies while feverishly speculating on what they might be.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Try Spectra School for free!

If you’re looking for a good way to spend 35 minutes or so, check out Lesson 3 of our flagship course “Think Like a Market Professional” for free. https://spectramarkets.com/lessons/tlmp3/ There, you will find the entirety of Lesson 3, for free, along with a link to my Learning From Legends video with Ben Hunt.

The lesson is called “Surfing the Narrative Cycle” and delves into how you can understand the stories the market is telling itself. If you like it, you can sign up for the full course and use coupon code LESSON3 for $250 off the $1200 price (i.e., you pay $950 for 16 lessons and 10+ videos.)

A bit of a funny week as Waller laid out his conditions for a Fed cut, some other Fed members hinted a cut might not be necessary, the labor market data came in pretty solid, and… The cut got just about fully priced in anyway. With so much policy uncertainty in 2025, one might think that the path of least regret would be to wait, but the market doesn’t think that!

It is basically unheard of for the Fed to pass on a cut that is fully priced in, but I would say the disconnect between the guidance and the pricing is about as big as it ever gets. I am not saying they are guiding to no cut, but their guidance has not been suggesting of an 88.8% chance of a cut! But the market decides when the Fed will cut, generally, not the other way around. Oh, and here’s the Atlanta Fed’s excellent real-time measure of US GDP:

The neutral rate is rising and we have no idea where it is and the economy is better than fine. Let’s cut rates!

There was a good deal of cacophony in France this week, as the political situation looks a bit wobbly and the market can’t decide whether to buy or sell French assets. Ultimately, the news was bad (no confidence vote goes through) and the price action was good (EUR higher) because everyone was ready and positioned for the bad news when it happened.

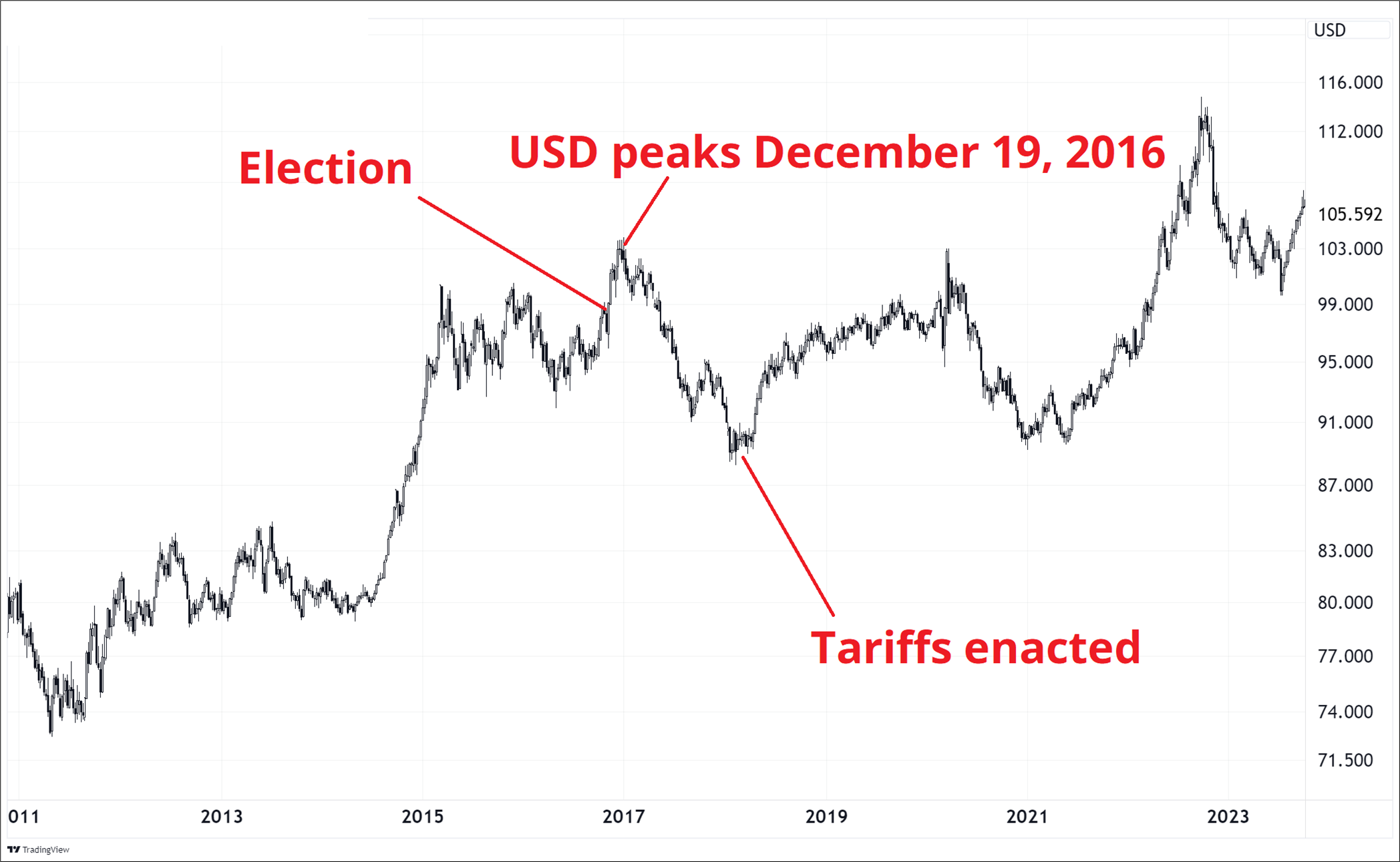

Markets seem to have found an unstable equilibrium point here as Trump 2025 policies seem to point to radical action on tariffs, taxes, and government restructuring while the realities of execution remain unknown. Will Trump slow play the tariffs via some sort of phase-in period in an attempt to extract concessions from trading partners and enemy states? Or will he just go whole hog on Day One and stay true to the aggressive rhetoric? Hard to say!

In 2017, we had a bit of a similar setup and then Trump super slow-played everything as he errantly focused on his unsuccessful attempts to repeal Obamacare and build a wall on the Mexican border. He wasted almost a year with these distractions while negotiating unsuccessfully with China and then finally slapping on the tariffs in 2018.

Because everyone was ready for bigly action in 2017 and it didn’t happen, the USD got absolutely smoked as the bullish dollar positioning for tariffs was forced to unwind.

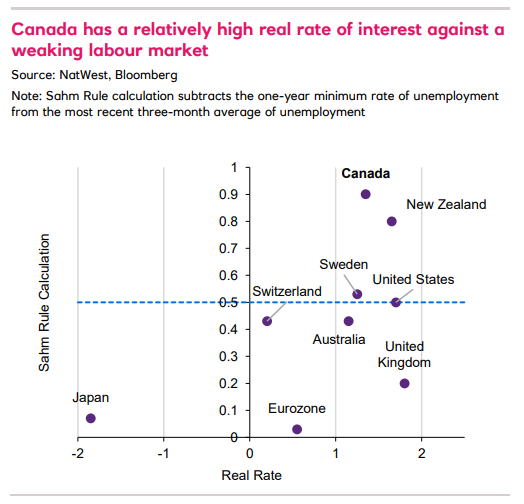

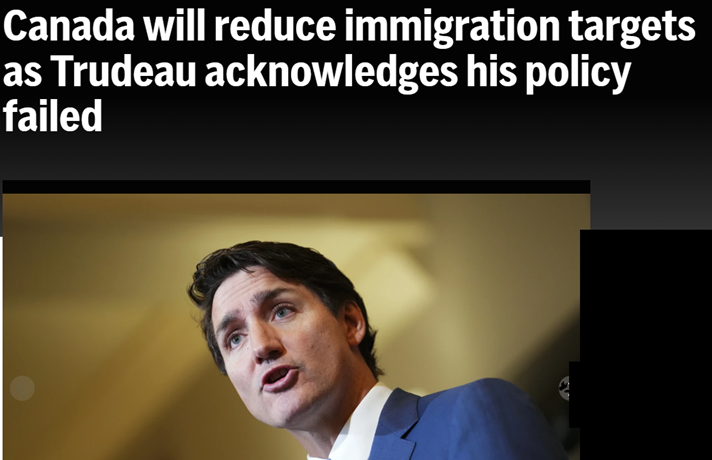

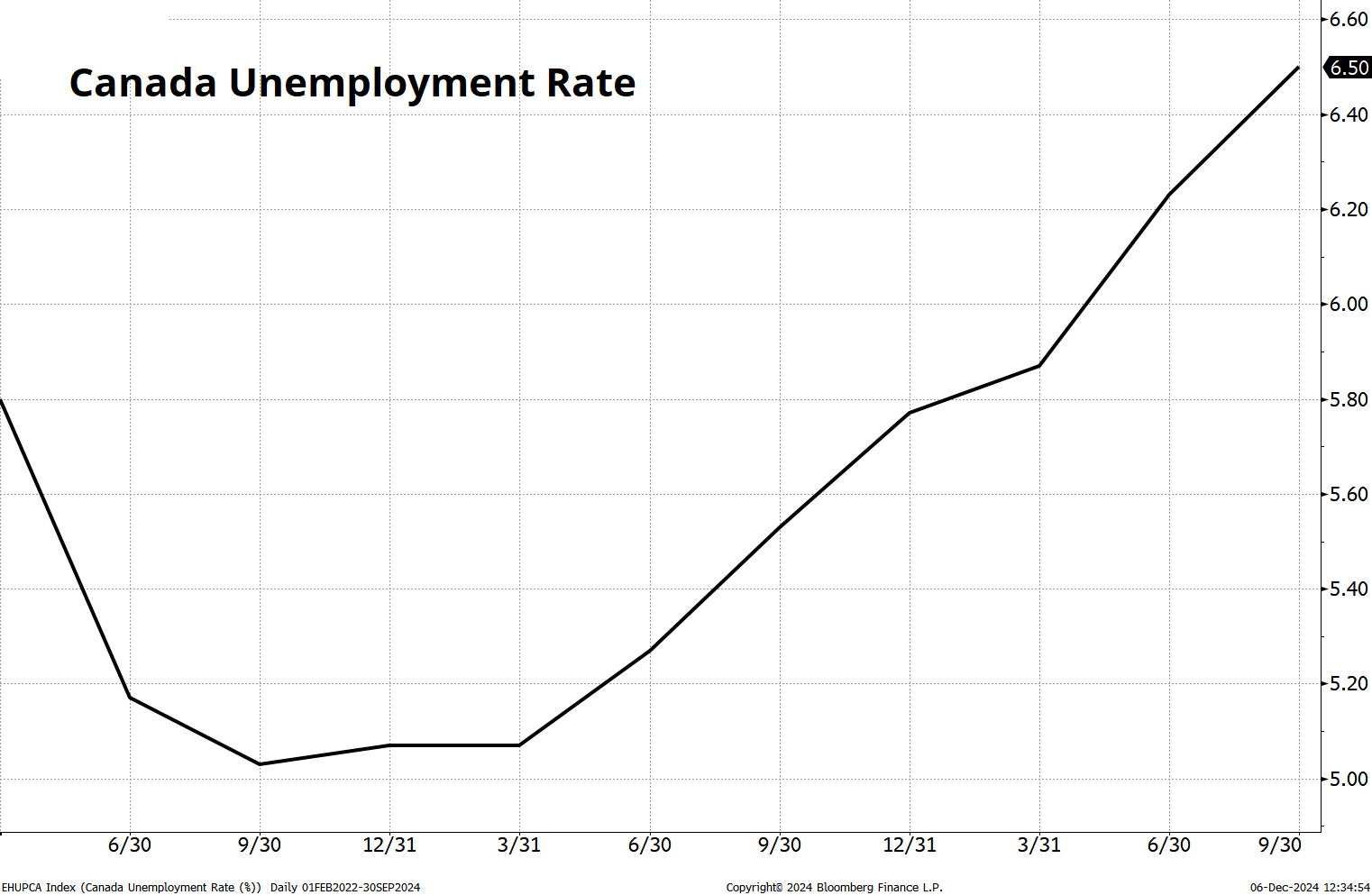

Elsewhere, Canada is heading for a possible economic accident in 2025 on the back of:

Let me give you a series of graphics related to that list:

Extracting meaning from Donald Trump’s Truth Social posts feels a bit like decoding a Q drop. He says: “Oh Canada!” while looking past a Canadian flag and out over the Swiss Alps. What does it mean?! What is the meaning of this?

What is the meaning of life on Earth!??!?

Trump appears to be schoolyard bullying Canada with particular vim right now for some reason, and it makes me wonder if he has something more nefarious up his sleeve… Like, maybe tariffs on Canadian crude oil? He can attach some sort of random reasoning based on fentanyl or whatever and achieve two goals at once: Target a large trade deficit “offender” and benefit US oil producers by making Canadian producers dramatically less competitive overnight.

Just a theory. With its reliance on US exports, its creaking housing market, and an enormous consumer debt pile, the vulnerabilities for my homeland are starting to stack up. I have been pushing 3-month 1.45s in USDCAD for the last week or so and I think that anyone who is naturally long CAD should be hedging.

You have four central bank meetings next week, and with today’s jobs number locking in a 50bp cut from the Bank of Canada, the greatest mystery now surrounds Switzerland’s SNB. I’ll cover that in the section on Interest Rates.

Here’s the beautiful trading calendar you will find each week in am/FX if you subscribe:

I didn’t mention CPI, but yeah. There it is.

Don’t forget to buy the 2025 Spectra Markets Trader Handbook and Almanac here.

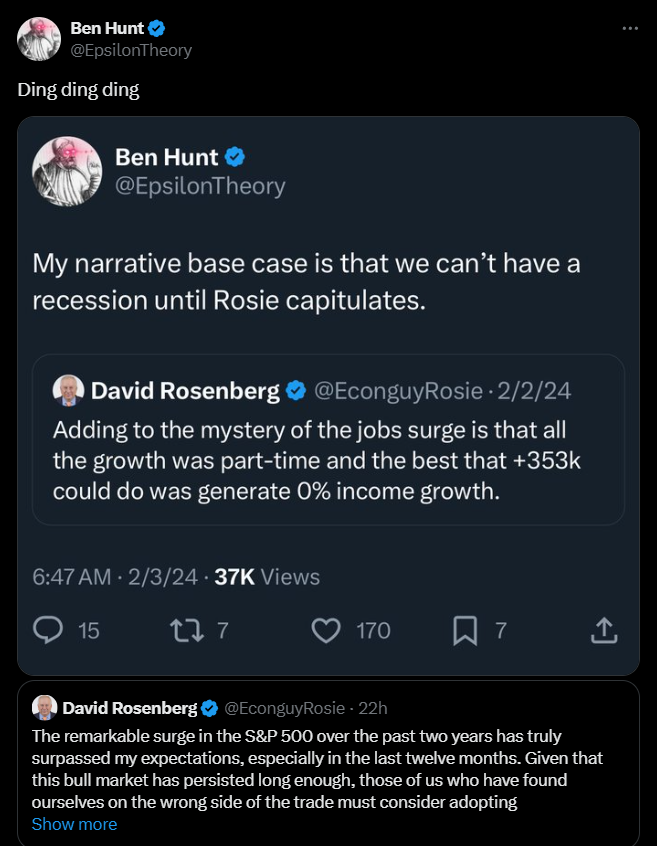

Oh, hey, stocks went up again. Quel surprise. JK, of course, as I am surprised how persistent and steeply sloped this has been. Couple more warning signs as a noted bear on the economy and the stock market capitulated after years of being on the wrong side of the stonks:

https://x.com/EpsilonTheory/status/1864795250872496490

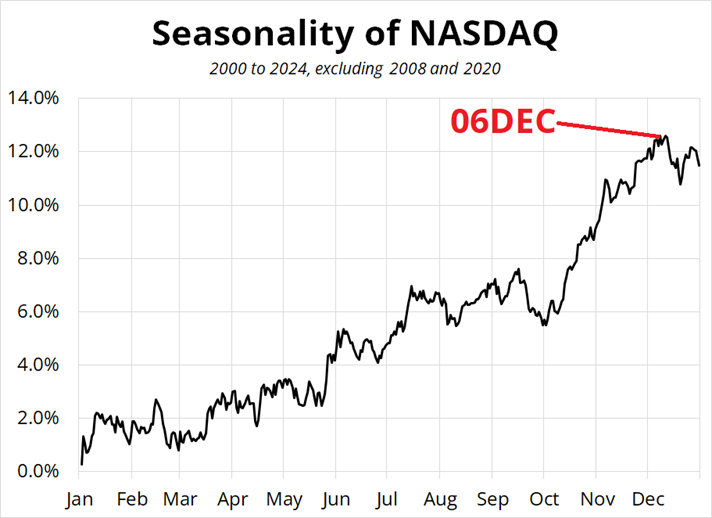

Dave Rosenberg is a fantastic human being but due to his fame and persistent bearishness, you can’t ignore the fact that he’s semi-capitulating here. And this coincides with the average seasonal high of the year for the NASDAQ.

I have been wary and wrong for about 100 SPX points, and I have been reducing my personal exposure to stocks as we go up but have not yet had sufficient onions / foolishness to go short. I think Q1 will be negative for stocks and right now I plan to go short around the turn of the year or just after. This is a fairly bold call since these are the quarterly performance stats for the S&P 500 since 1974:

Win% funny yea yea I noticed

This week’s 14-word stock market summary:

Bull market in late innings can be a tough but rewarding short in 2025.

US yields didn’t do all that much and we covered the Fed already at the top of the show… So… As promised, here’s my view on Swiss rates.

The SNB is the most interesting meeting of the four this week because it’s priced exactly 50/50 for 50. As an outsider, inflation looks alarmingly low in Switzerland, but for Switzerland, YoY inflation of 0.7% is actually not that odd. The current SNB target rate is 1.0% and the implied rate for September 2025 is one bp below zero (i.e., -0.01%). Schlegel has consistently been saying that negative rates could come back, and they don’t seem particularly panicked about that fact, but that’s an obvious statement as they will never remove that optionality.

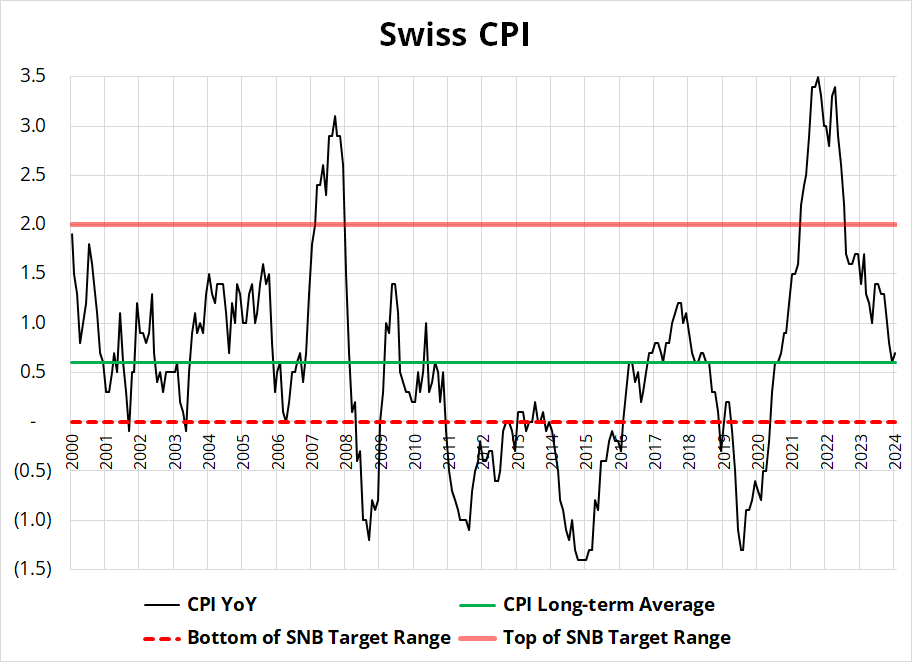

Board member Petra Tschudin sounded pretty chill in a November 21 interview, saying: “Inflation is now comfortably in the range of 0% to 2% where we want to see it.” Here is the inflation situation in the Swiss Confederation:

It’s very important to note when dealing with Swiss Inflation data that it is not seasonally adjusted. Therefore, we can be almost certain that inflation is about to bounce as we approach the seasonal nadir for Swiss prices.

Swiss inflation is at its 25-year average and it’s likely to bounce in the new year. I don’t think the SNB will go 50bps in December. I think the SNB cuts 25, not 50.

To all the 14 people that subscribe to FSR and also care about Swiss rates: thanks for reading.

As briefly mentioned earlier, the market is long USD, waiting for tariffs. If there are huge tariffs, the USD will still go up. If there are phased-in tariffs, the market won’t know what to do. If there are negotiations and slow playing of tariffs, the USD will drop about 10% on a frozen rope like it did in 2017 after Trump failed to deliver anything bigly in the early innings of his first term.

Now we’re in a bit of a holding pattern as people are going to be reducing risk soon for Christmas once we get all these central bank meetings out of the way. The combination of bullish USD macro, bearish USD seasonality, and meaningful long USD positioning makes for an extremely difficult forecasting assignment over the next few weeks.

I tried a long USDCHF trade this week and it was not very fun. I underestimated how big the USD long position was and how much people would want to reduce it into NFP. I ignored seasonality and positioning and got caught up in the euro bearish hype.

In macro trading, you first need the right list of inputs and variables to help you think about where markets are going. But then you need to correctly weight the variables in real time. I thought that macro would outweigh positioning and seasonality, and I was wrong.

If you want to learn the concepts and frameworks that will help you succeed in markets, check out: “Think Like a Market Professional”.

Bitcoin omfg. The price contains six digits!

Wen lambo!?

Now lambo!

*LAMBORGHINI DEALERS DECLARE FORCE MAJEURE DUE TO SUPPLY SHORTAGE AS BTC CROSSES $100K

If you reside on planet Earth, you probably know what’s going on in the orange coin as the orange man appointed another man who is also crypto friendly.

Deregulation or more like: no regulation is great for crypto in general as Hawk Tuah girl well knows after her $50 million rug pull this week. The fewer the rules, the better it is for commercial banks, crypto prices, and memecoin grifters.

Rules are a pain! Regulation bad!

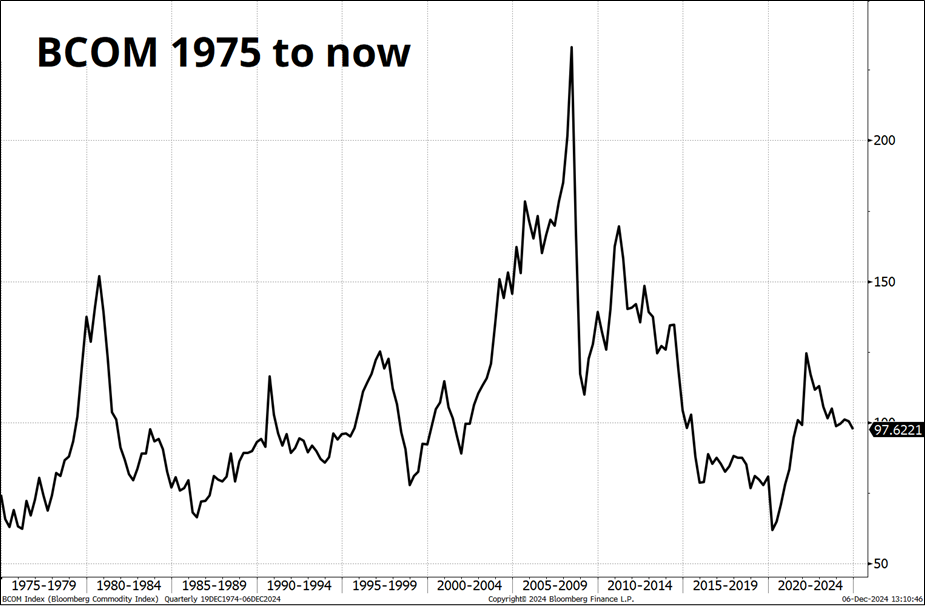

While there is a positive drift in stocks due to earnings, dividends, innovation, and debasement, commodities only tick one of those four boxes. And one of those factors that’s bullish stocks (innovation) is bearish commodities. We continually extract more productivity from each kernel of corn or barrel of oil or cotton plant each year. So you get a chart that looks like this:

Due to substitution effects and relentless technological advancement, commodities shortages are always temporary. Higher commodity prices are the cure for high commodity prices as supply and demand adjust almost instantly. In stocks, higher prices do not increase supply and they often increase demand.

Anyway, just some random thoughts on commodities because they are going nowhere this week and I remain skeptical of the idea that the Great Rebound in Commodities is imminent. China isn’t doing great, and neither is Europe. I don’t see Japan and the USA picking up the slack.

Whew! OK! That was 8.554 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

Links of the week

Stadium DJ Fred Again goes tiny desk style. Artistic!

Message in a Bottle sample nice!

A funny tweet.

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.