Regime shift or markets gone hog wild?

The AI imagines itself calling itself

(in the style of Tamara de Lempicka)

Regime shift or markets gone hog wild?

The AI imagines itself calling itself

(in the style of Tamara de Lempicka)

Flat

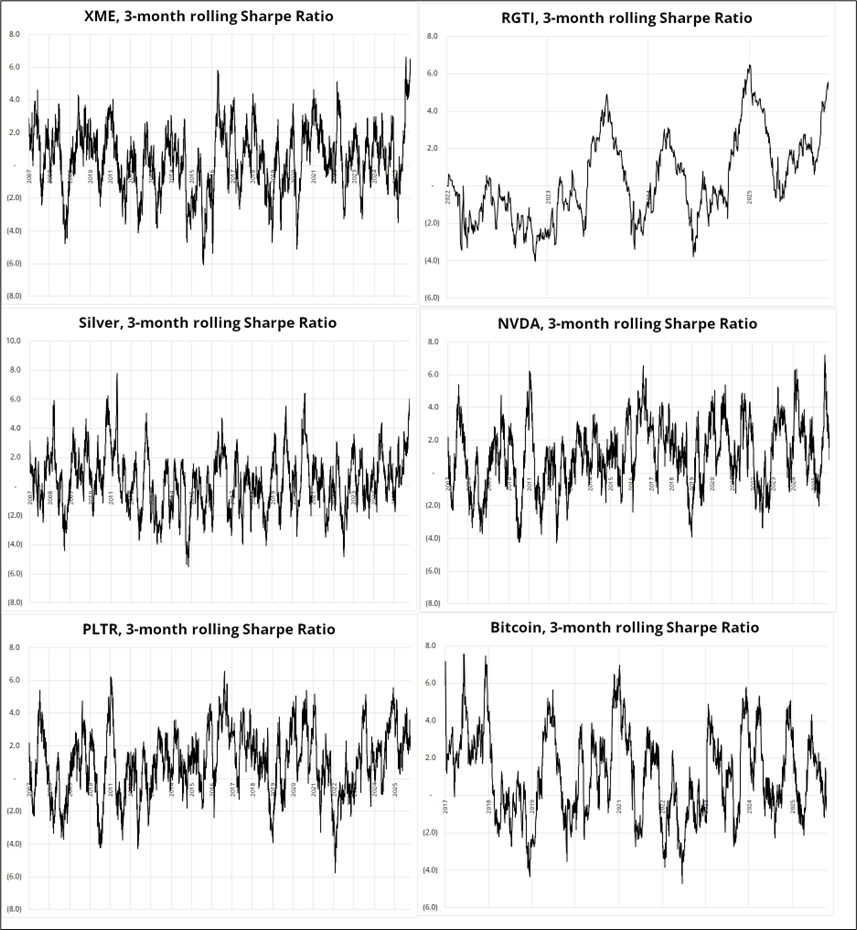

Check out some of the Sharpes of various products of late.

Bananas.

I remember sitting there one day at Lehman Brothers in 2007 and getting given 100 million NZDUSD by a good name and thinking: “Kiwi is already down 300 pips today and 800 pips this week, these have to be OK to hold.”

They were not OK to hold!

I quickly learned that overbought and oversold mean absolutely nothing in a crisis market because forced liquidation boosts vol and sends the mean reversion monkeys (like me) back to the zoo. I was able to transition away from focusing on deviations from the 100-hour and various similar overbought/oversold metrics in time to survive and thrive in 2008, but there was a painful and costly 6-month period in there before I adapted.

I bring this up because gold and silver and XME and RGTI (and other stuff, but not crypto, NVDA, or PLTR) are trading like we are in some kind of fiat currency crisis or massive positive liquidity shock akin to 2008/2009 or 2020—but without the vol. I feel like I am missing something. Silver and XME are realizing less than 30 vols over the last 90 days, and gold is realizing sub-15% as all three fly to Ganymede.

There is a point where you say “the regime has changed” and overbought and oversold are meaningless—and you adapt to the new market structure. But I suppose I am having trouble seeing how this rally in silver (for example) is different from the one in 2011 as it’s based on a similar narrative. And: If this is a pure liquidity bacchanalia, why are crypto and NVDA and PLTR flatlining?

I understand that I am supposed to be the one answering these questions, but right now I am perplexed so I’m just throwing it out there. Sky-high Sharpes can be a good overbought/oversold signal, but only if that’s the kind of regime you’re in. If you’re in a panic regime or crisis, those signals are not useful. Are we, though?

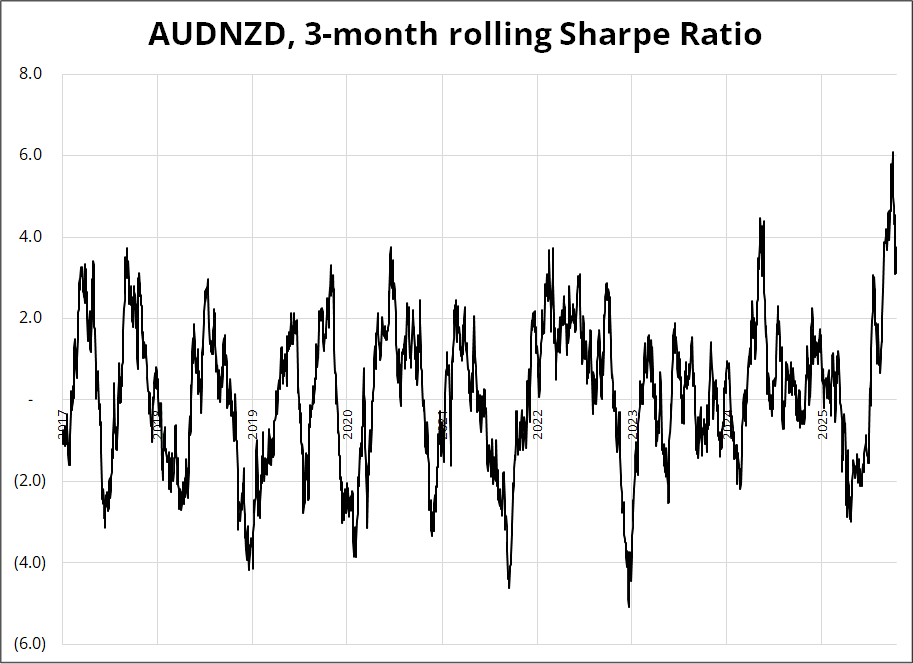

If you’re wondering about FX, USDCAD’s Sharpe has been above 2.0 over the past three months, and AUDNZD got as high as 6.0 before two violent corrections. First, on the 100% China tariff “news” and second on last night’s Aussie jobs data. The Australian data was modestly on the weak side, with the UR ticking up two tenths, and the market is getting a bit tired / bored of a profitable position that has been working well since the dovish RBNZ on August 19.

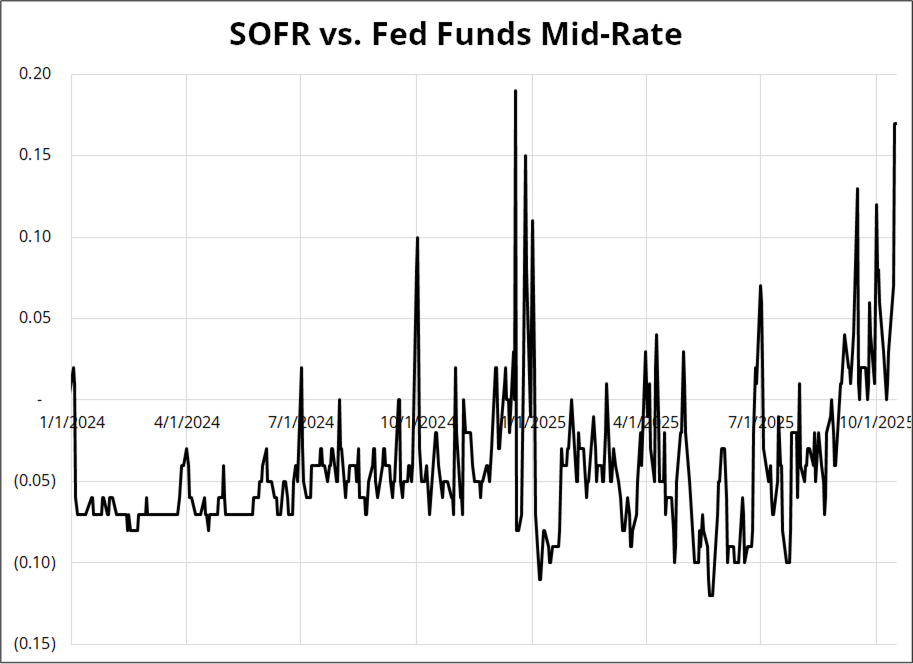

A few mentions of funding pressure here and there over the past 24 hours as the deadline for California tax payments was yesterday. Because of the wildfires (starting January 7, 2025) and a federal disaster declaration, the IRS granted relief to affected taxpayers in parts of California (notably Los Angeles County). Deadlines for federal tax filings and payments that would otherwise fall between January 7 and October 15, 2025, were postponed until October 15, 2025.

You can see in the chart here that today’s rise in SOFR is comparable to year-end funding stress at the turn of 2024/2025. Probably nothing to be concerned about, but worth watching over the next few days, especially after the wipeout of crypto leverage over the weekend. Perhaps the altcoin flashcrashes are symptomatic of leverage in other trending asset classes. Again, probably a nothingburger, but worth monitoring.

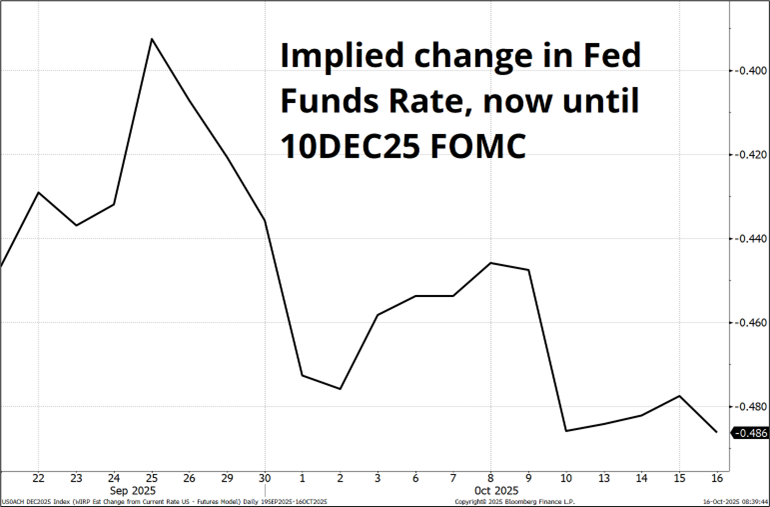

With two full cuts now priced for the Fed (48bps implied, see chart) and questions remaining about whether or not inflation is picking up, my guess is that the USD will run higher into the October 24 CPI print as there is very little room for Fed pricing to go more dovish for 2025 and there is some possibility December gets partially priced out on a strong release.

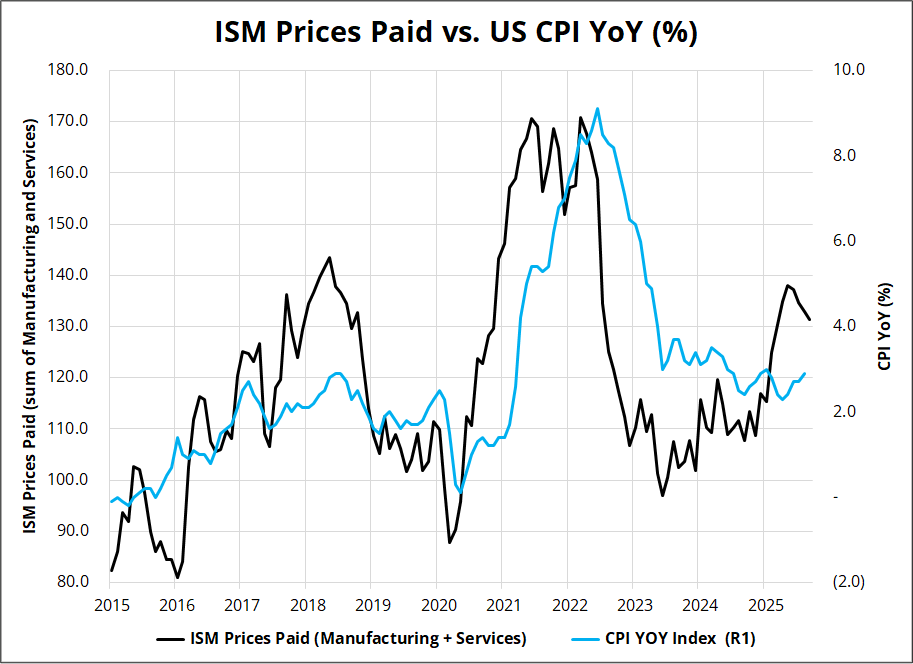

ISM Prices Paid jumped earlier this year, and that tends to foreshadow rises in CPI (see next chart). That said, Prices Paid has come off a bit, so the signal is a tad ambiguous.

I will consider going long USD at some point ahead of CPI, but prefer to wait until early next week. Candidates would be USDCAD or USDCHF. With EURCHF back on a 0.92 handle (where the SNB is again more likely to dabble), USDCHF could be a useful USD long as USDJPY is getting way too confusing with Takaichi priced in, rate diffs forever pointing lower, and US 10-year yields unlikely to break down from the current 4.0%. An option (USD call) that captures both CPI and corporate month end will probably make sense and I will likely do that early next week. The last time EURCHF was on a 0.92 handle, SNB Sight Deposits made a noticeable move higher. While they are not a perfect proxy for intervention, they’re not bad.

Have a dialed-in day.

The AI imagines itself calling itself (in the style of Tamara de Lempicka)

I can’t imagine using these, but did you know ChatGPT and Uber can both be accessed by telephone?

1-800-Chat-GPT and you just talk to it. Not too shabby.

1-833-USE-UBER

Weird.