Massive repricing of growth, fiscal, and AI spend.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Massive repricing of growth, fiscal, and AI spend.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

![]()

Listen to the The Macro Trading Floor Podcast

This week’s theme is again stagflation as prices remain sticky and growth is threatened by a combination of government cuts and extreme uncertainty around the new philosophy of Transactional Neomercantilism. While tax cuts for business and the wealthy, and the War on Drugs remain two philosophies shared by Reagan and Trump, several neocon talking points from the 1980s have been inverted, and it’s unnerving investors. Reagan advocated for:

“Our peaceful trading partners are not our enemies. They are our allies. We should beware of the demagogues who are ready to declare a trade war against our friends, weakening our economy, our national security and the entire free world. All while cynically waving the American flag. The expansion of the international economy is not a foreign invasion; it is an American triumph, one we worked hard to achieve, and something central to our vision of a peaceful and prosperous world of freedom.”

“We must not be misled by those who would make defense once again the scapegoat of the federal budget.”

Now, the new administration is offering up tariffs, lower defense spending, and a pro-Russia stance. Immigration reform and DOGE cuts are likely to create more inflation and less growth, respectively. So, it’s quite a policy mix right now, not to mention the ongoing flooding of the zone, which creates a deafening trumpet blast of information and disinformation and so investors don’t really know what is real policy and what is noise.

The optimistic argument is that at some point in the future, a new global trading order, less global trade, lower taxes, deregulation, and a better balance between the public and private sector will create a flourishing US economy. That is definitely possible, but the short-term pain is here, and we will need to wait a while for the long-term gains.

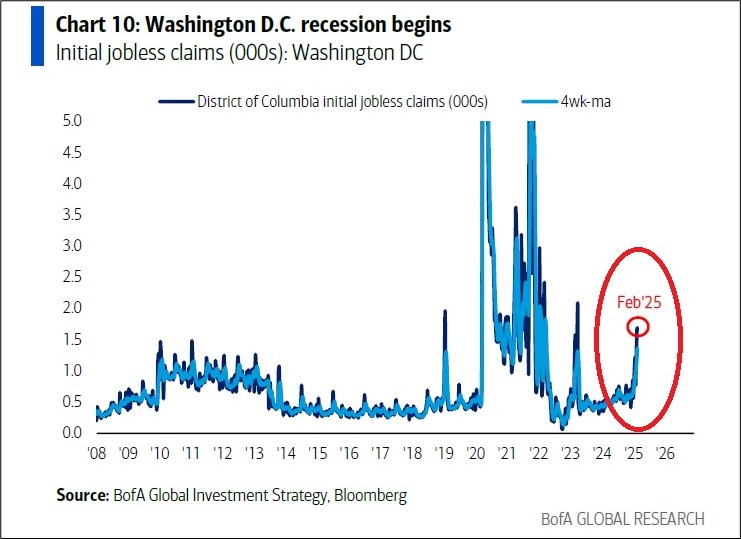

The employment impact of the DOGE cuts has started, and you can see it most clearly in Initial Jobless Claims in Washington, DC. Some are making the argument that 300,000 jobs eliminated is a drop in the bucket for the US labor force, but this fails to account for a significant multiplier as a DC spending freeze isn’t going to be pretty for consultants, lobbyists, restaurants, and any other parts of the support system that caters to the Leviathan.

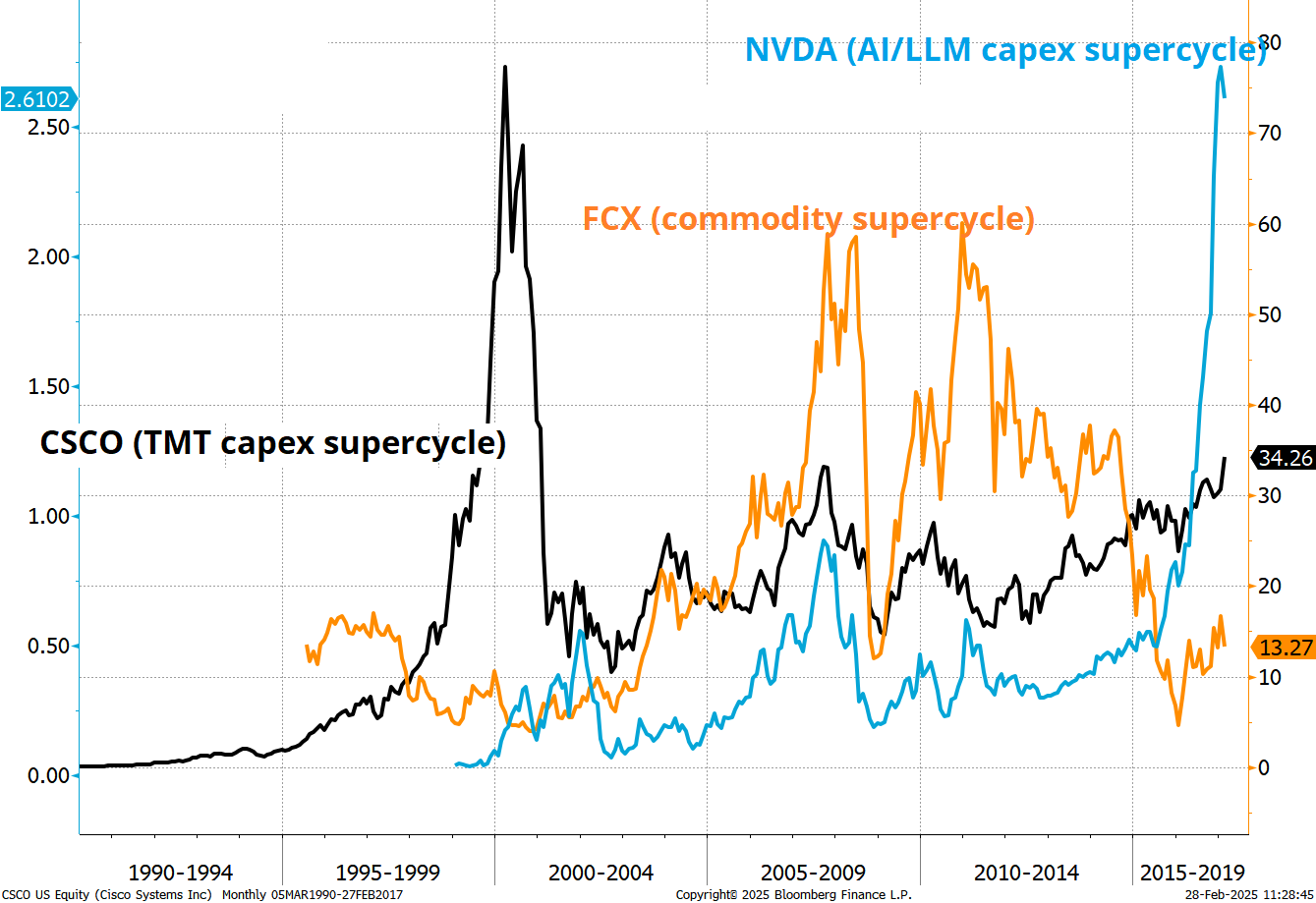

Meanwhile, the market is also worried that we have reached peak AI capital expenditure. If that’s the case, that’s also bad for growth and it’s terrible for the valuations of the many, many stocks where investors have gone all in on a once-in-a-lifetime investment theme (or, at least one of the most exciting capex themes: the dotcom optical fiber and commodity supercycle capex themes were pretty cool too).

By it’s very nature, capex is cyclical. You build all the stuff you need just once, then you don’t need to build the stuff anymore—you start to use it. Therefore, picking the top in the capex cycle is a critical decision for investors in stocks like NVDA, AVGO, VRT, and SMCI. Needless to say, those stocks all got rekt this week. The combination of Microsoft backing out of data center contracts and the DeepSeek Freak from earlier in the year have raised significant questions about the ferocity of capex-led earnings growth going forward.

When companies are bragging about how much capex they’re doing, it’s a bad sign. And that’s exactly what’s been going on in recent months as MAG7 earnings growth peaks.

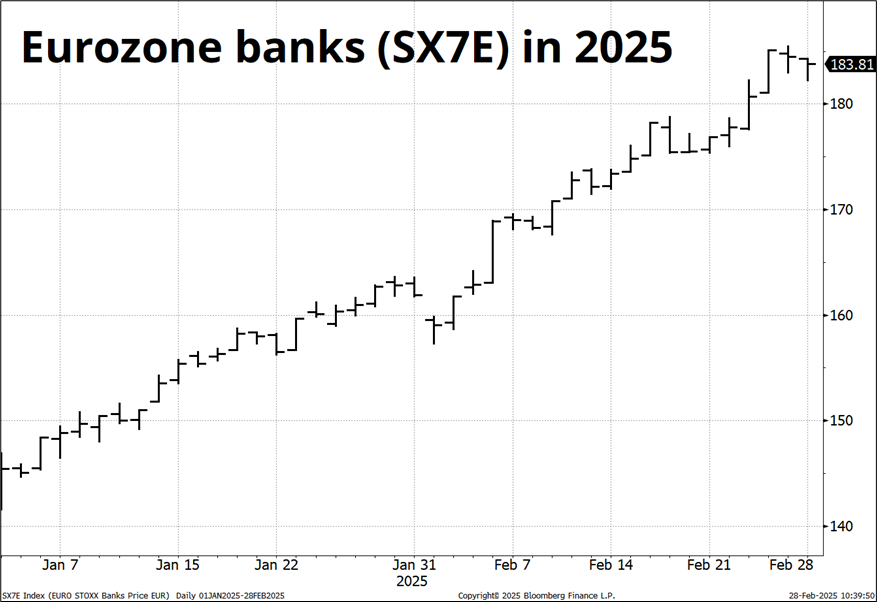

It all adds up to a horrendous week for US stocks, which we will get to next. Meanwhile, the market has found other places to invest, and Europe and China have received gobs of inbound money despite still-floundering economies. Cheap valuations and some signs of a possible loosening of fiscal strings in Europe, plus a possible resolution of the war in Ukraine have triggered a bit of a feeding frenzy in European equities. Look at EU defense stocks:

Wacky. Here’s next week’s calendar.

There was a complete meltdown in everything high-beta and high momentum this week as previous fan favorites like PLTR were destroyed. Palantir is still the most grossly-valued megacap in stock market history, even though it has fallen from 125 to 85. Trading off valuation isn’t a good strategy, but avoiding grossly overvalued stocks is a great investment strategy. At $200B and 69X sales, Palantir has no historical comps. There were stocks that got above 100X sales in dotcom, but none of them were megacaps. PLTR is a once-in-a-lifetime crazy train.

It wasn’t just PLTR that cratered this week, TSLA also completed its post-election round trip. $280 to $480 to $280 is enough to make any memecoin trader proud.

TSLA is the epitome of stocks as memecoins in the US and its deflation comes as the underlying business goes rapidly south as 50% of the world’s population will no longer own a Tesla due to the strong political statement the car now makes. Even before the start of the Tesla boycotts, the company’s vehicle sales had stopped growing. The competition caught up. The car designs are stale.

Then again, the stock has never been about automotive sales, it’s always been the sum of all technological dreams: Humanoid robots, solar panels, AI, batteries, and robotaxis, oh my!

While those other businesses are tiny, they offer investors a dream to buy into. As long as Elon Musk’s relationship with Donald Trump remains affectionate, some kind of made man premium will remain in TSLA, but two volatile personalities mixing like this could eventually lead to a breakup and that would probably be the beginning of the end of Tesla stock.

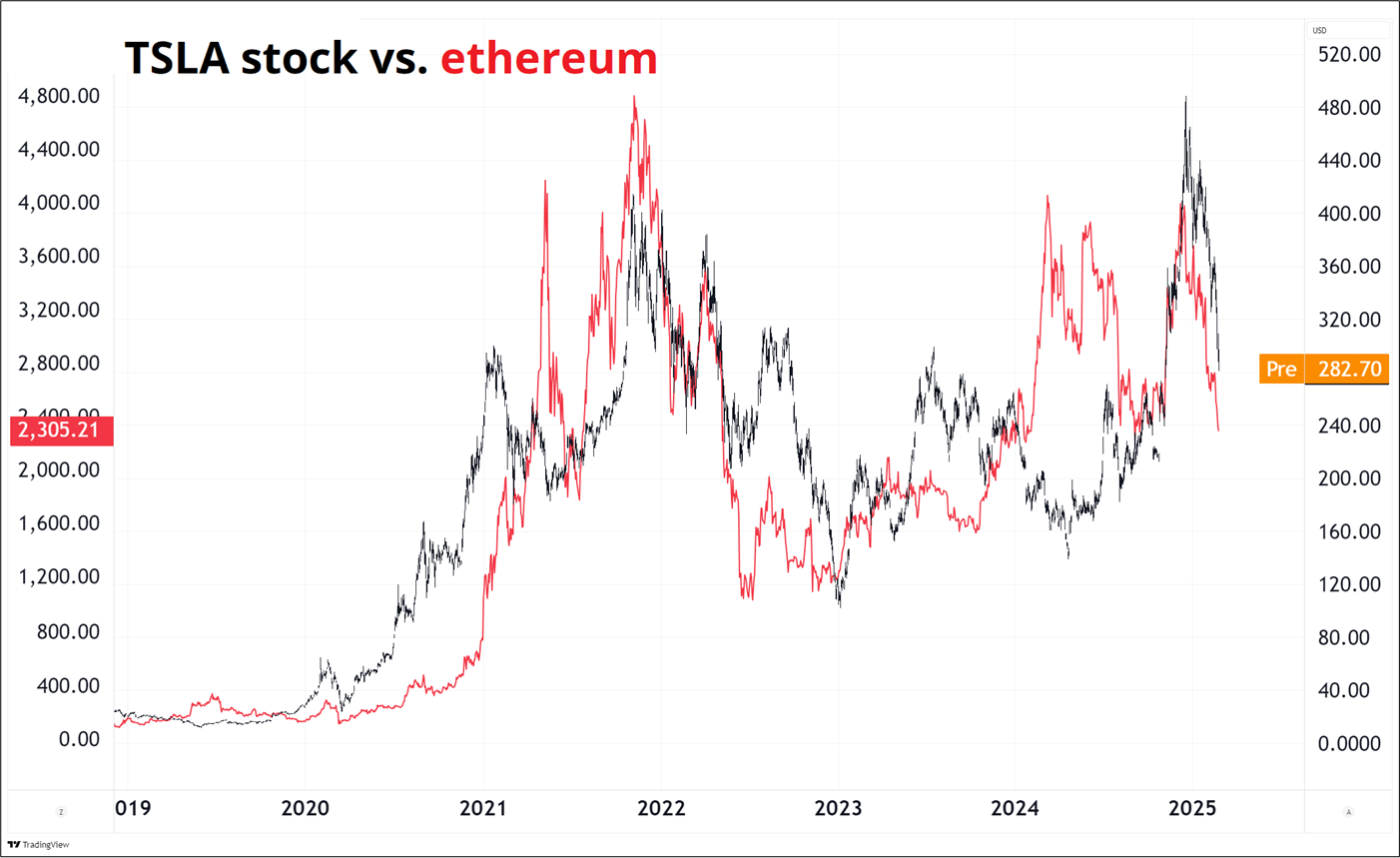

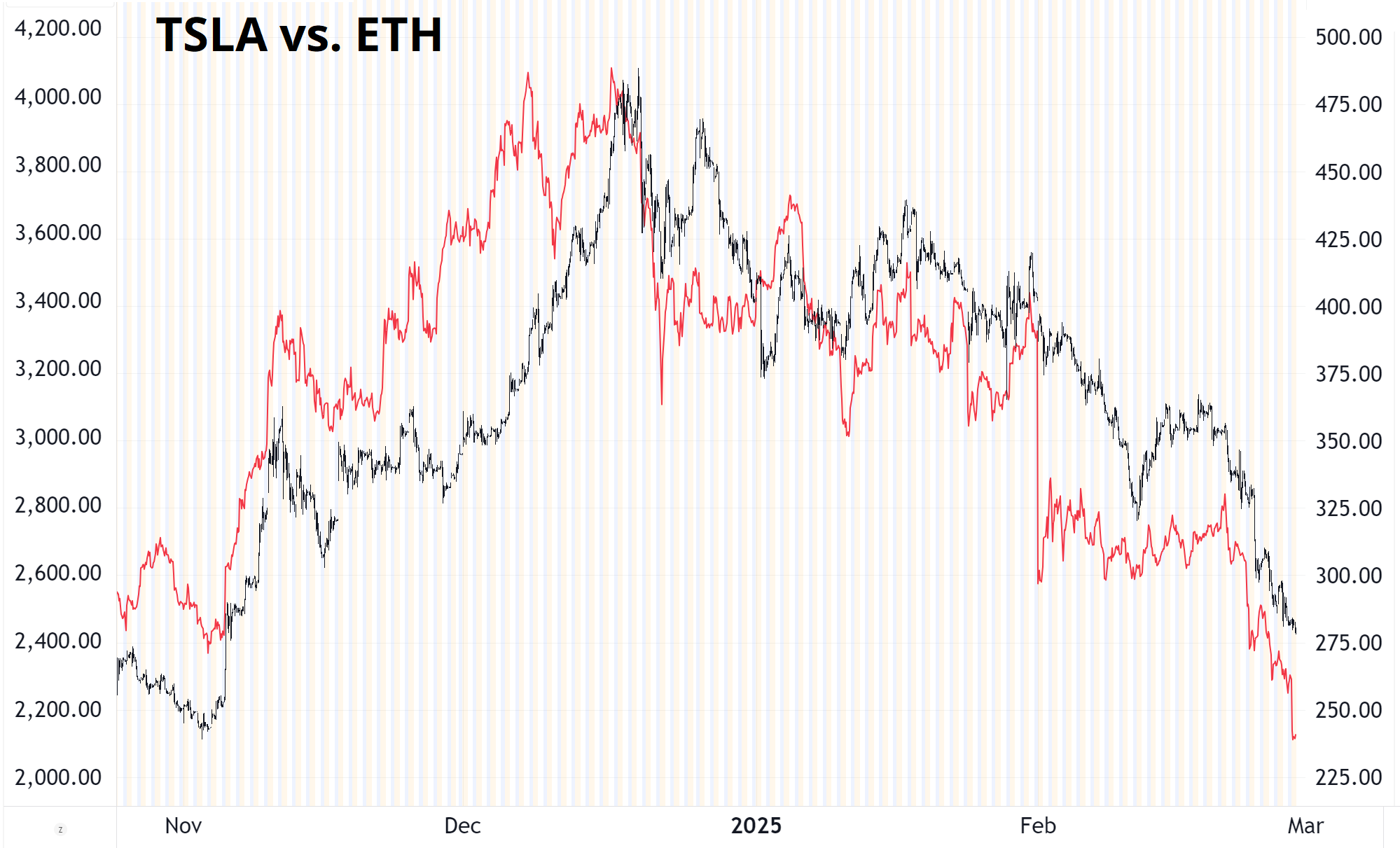

Shorting TSLA has been a fun game if you sell the rallies, but not if you sell the dips. But never forget that TSLA stock is not a car company play, it’s a play on techno-optimism. That’s why it tracks Ethereum so well.

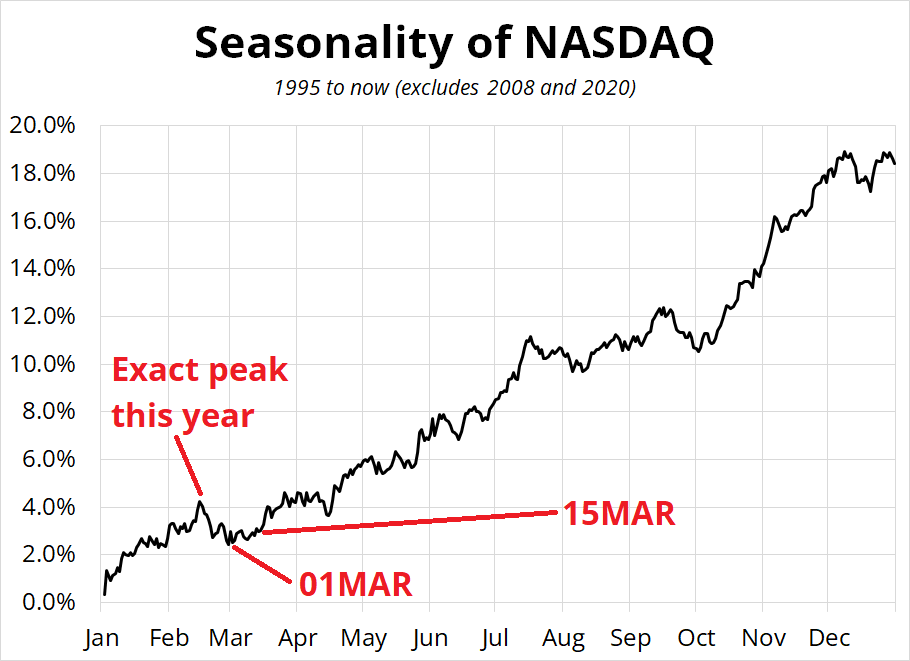

All these bad economic themes have hit right when stock market seasonality is no bueno, too. This sketchy period for global liquidity ends around March 8.

Outside of the USA, stocks are going absolutely crazy in some areas with BABA up and down 5% or 10% daily, and European banks doing this:

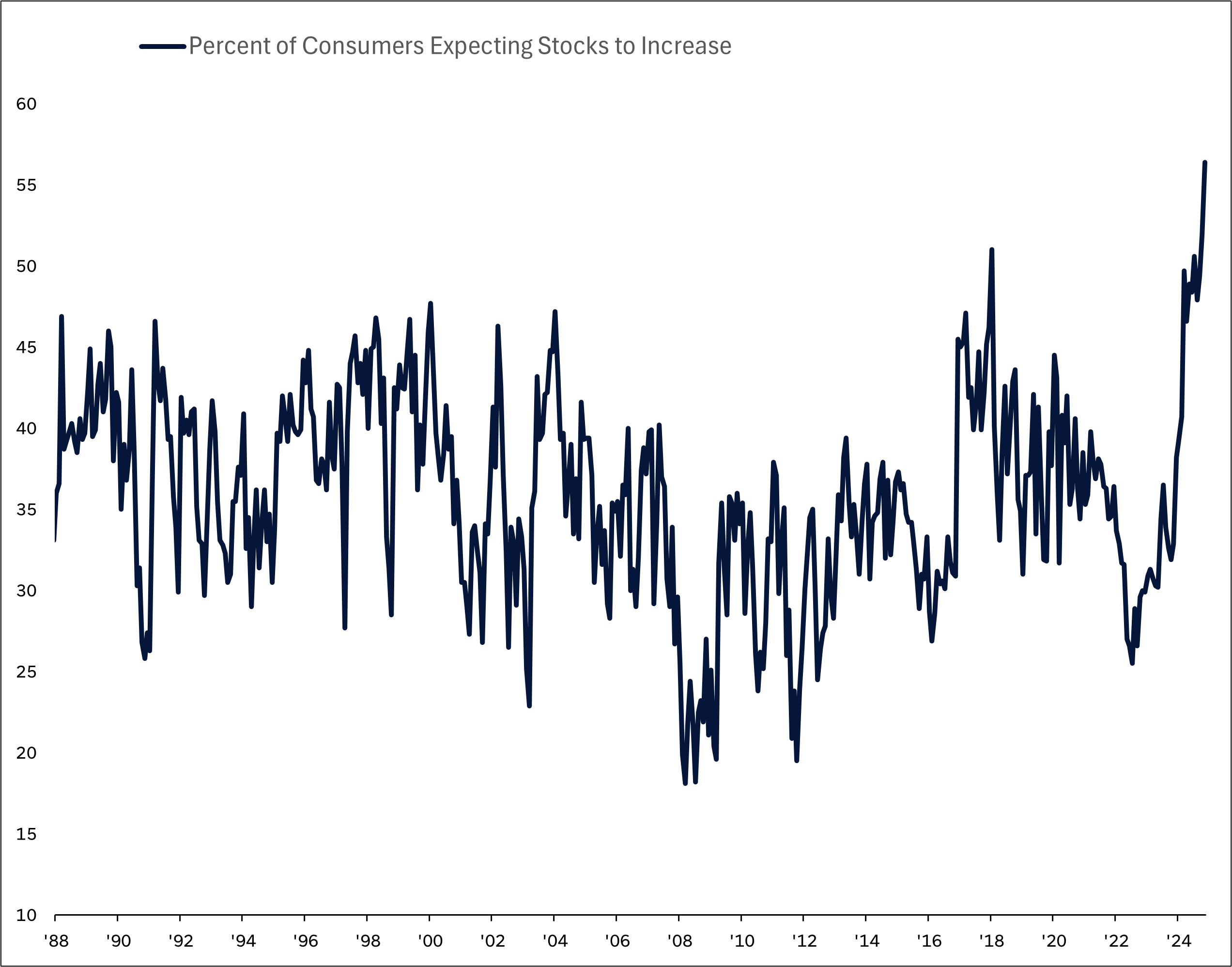

Stock market sentiment went from euphoric in December:

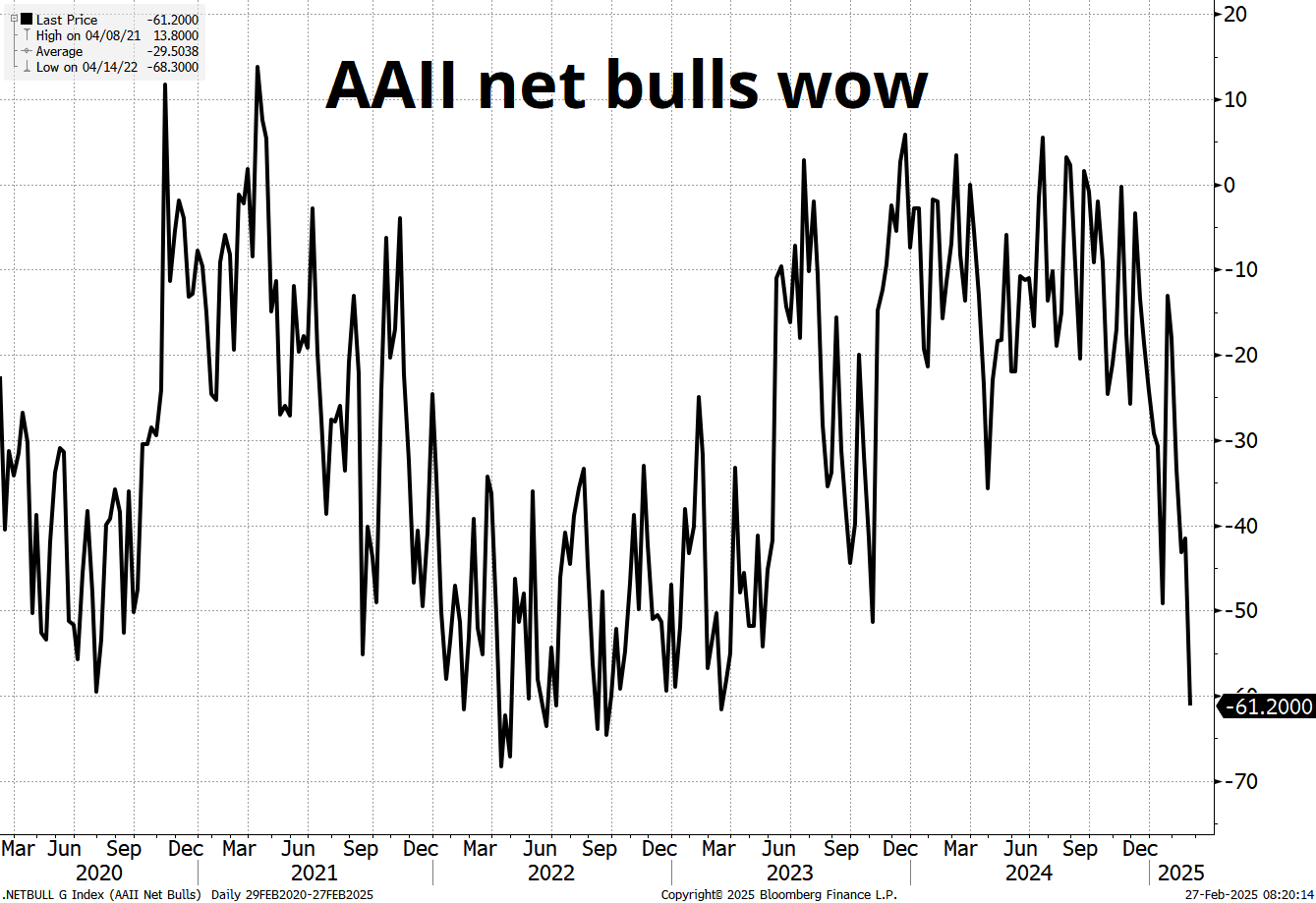

To here now:

And the bearish seasonal period for stocks is basically over.

This week’s 14-word stock market summary:

The froth has come off and now everybody is bearish. Crazy times. Crazy world.

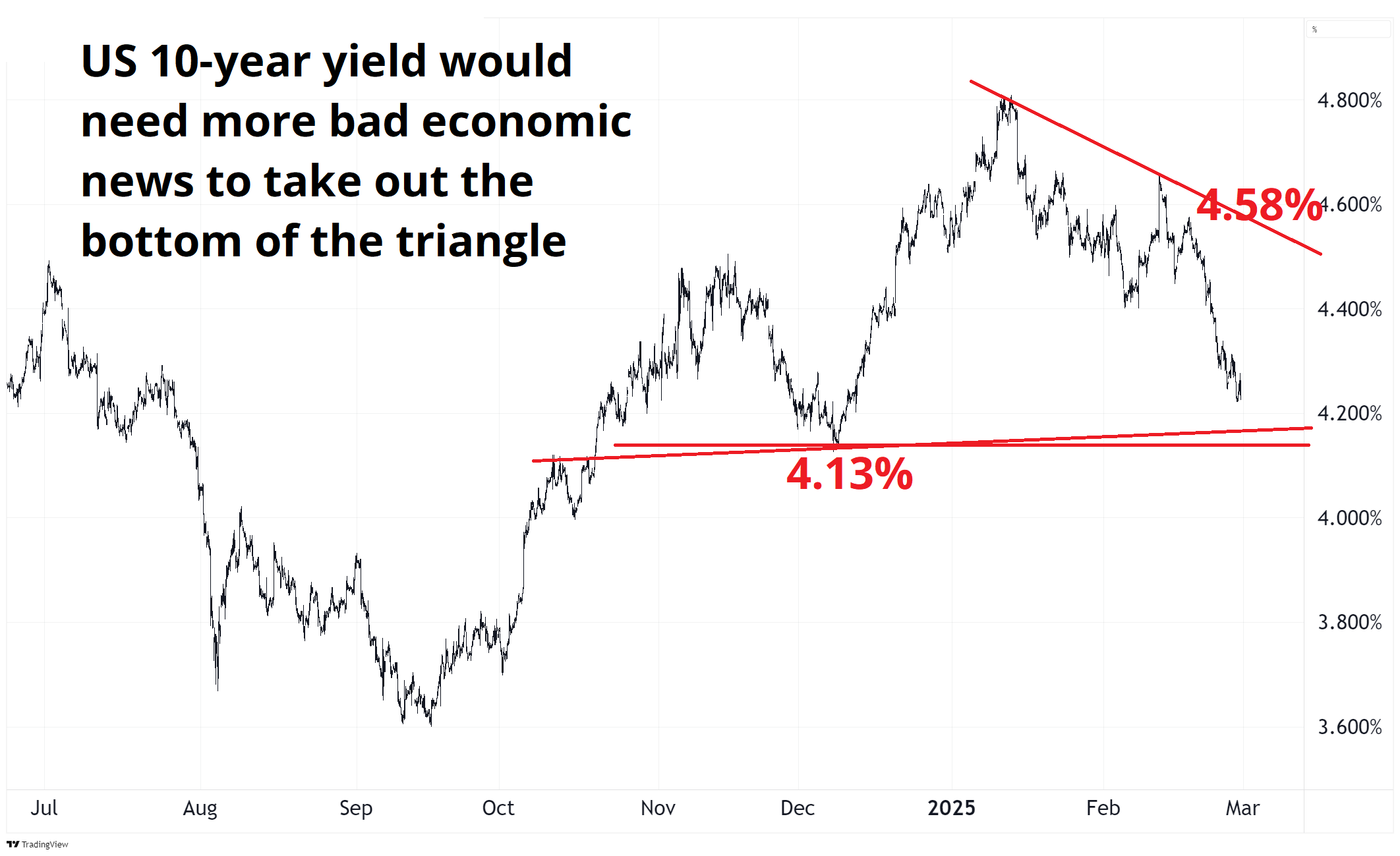

Yields are trapped between inflationary pressures and DOGEflationary drag. I don’t expect much fun in bonds as we should remain trapped 4.10%/4.50%. The front end might be tradable, but the fact that yields didn’t go lower on Thursday’s huge equity selloff probably tells you that the appetite for bonds at 4.25% is no longer voracious.

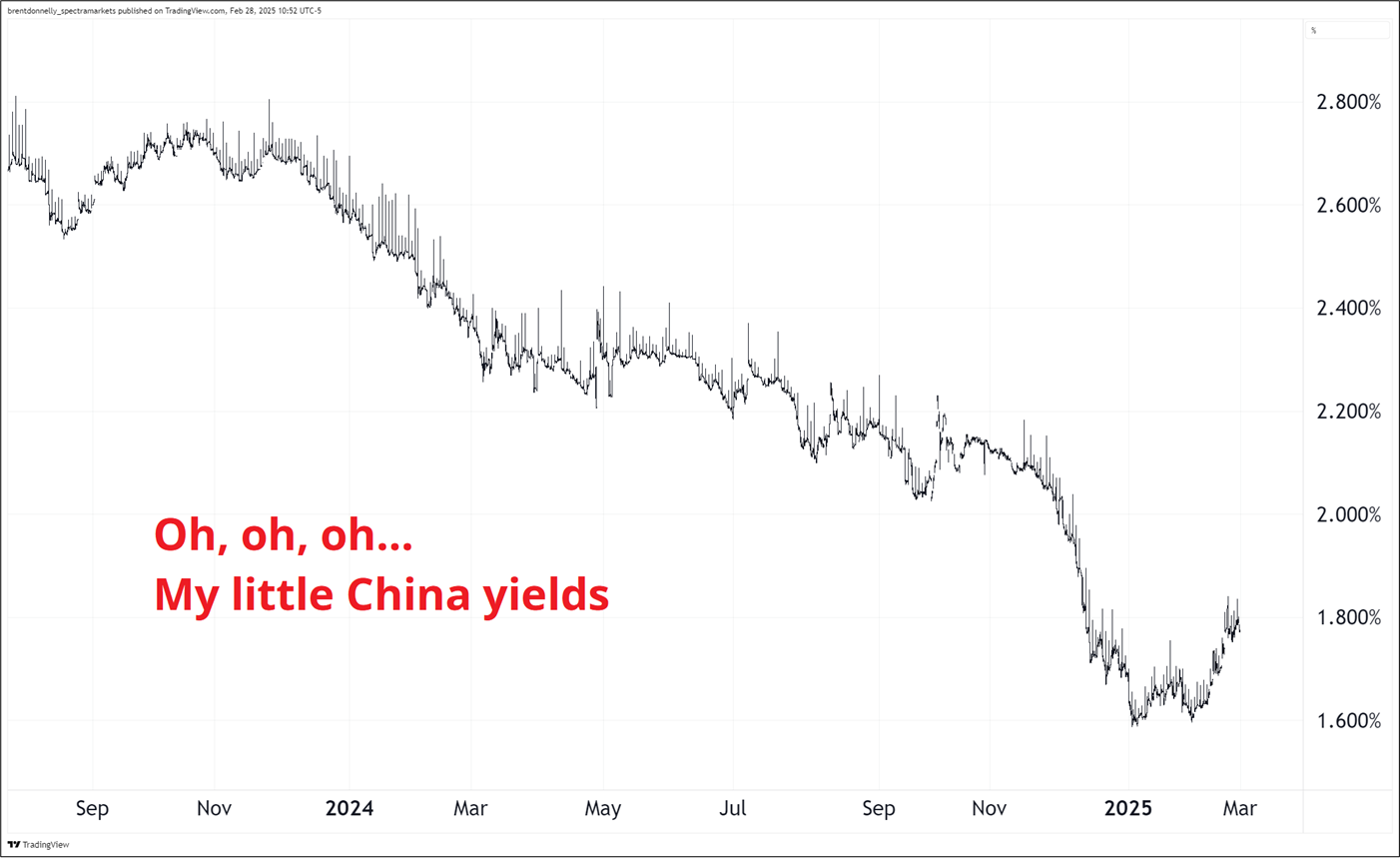

And your compulsory China 10-year yields chart, ofc:

The USD is boxed in on four sides by slower US growth, higher US inflation, US government targeting lower yields, and rising global yields. Every time the market tries a theme, it fails. USDJPY lower? Nope. EURUSD higher? Nope. AUDUSD higher? Nope. USDCAD higher? Nope. Things are moving around but not in any convincing, thematic way.

The tariffs are the Sword of Damocles over CAD still, and we will find out the dealio at one minute past midnight Monday night. If 25% tariffs are enacted on Canada, expect a complete freakout as the market is complacent and bored of the whole tariff cacophony.

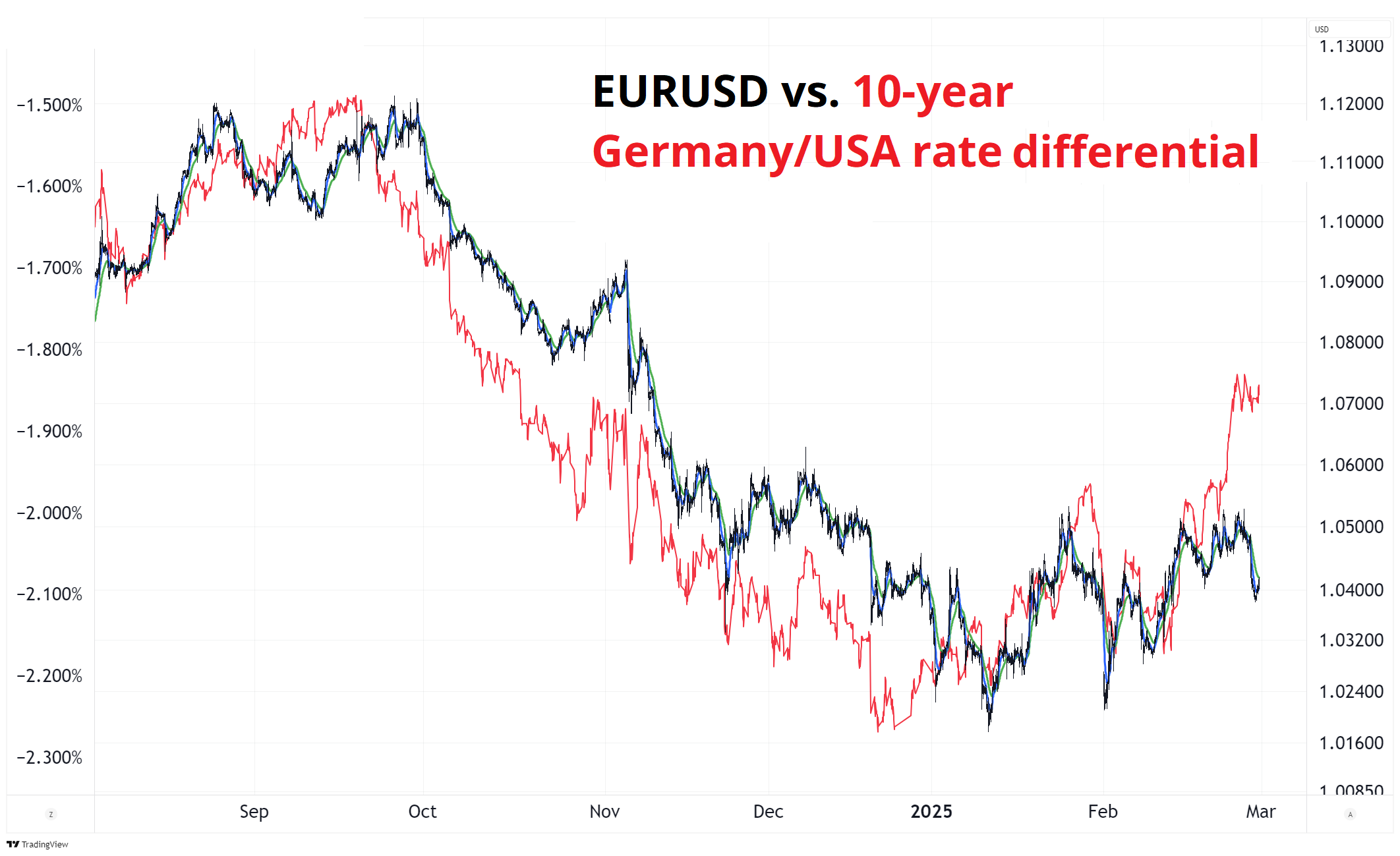

You can see in this next chart that EURUSD should be higher, in theory, as US yields are falling faster than those of Germany. But the threat of tariffs creates a reticence among euro buyers and that will not change until April 2. That’s the date reciprocal tariffs are supposedly coming.

FX markets continue to focus more on PLN than usual as it could be a big beneficiary of a peace deal in UKR.

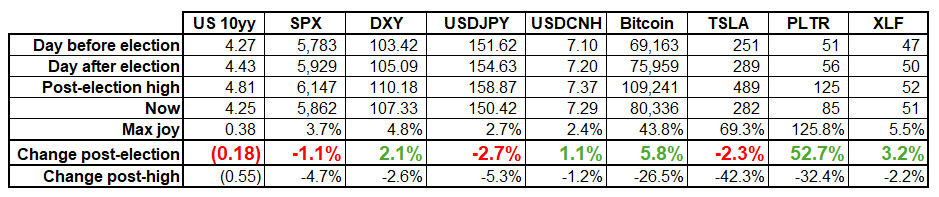

Checking in on the Red Sweep trades after just about four months, the accuracy of the common knowledge was mixed / meh.

My pre-election survey had respondents strongly agreeing that a Red Sweep would mean higher for everything in that table. While there has been much debate post-election about whether the new admin is good or bad for bonds, the unanimous pre-election consensus agreed a Red Sweep 2024 should be similar to Trump 2016. Then, USDJPY and yields skyrocketed on fiscal spending hopes, but now they are slumping on fears of fiscal drag.

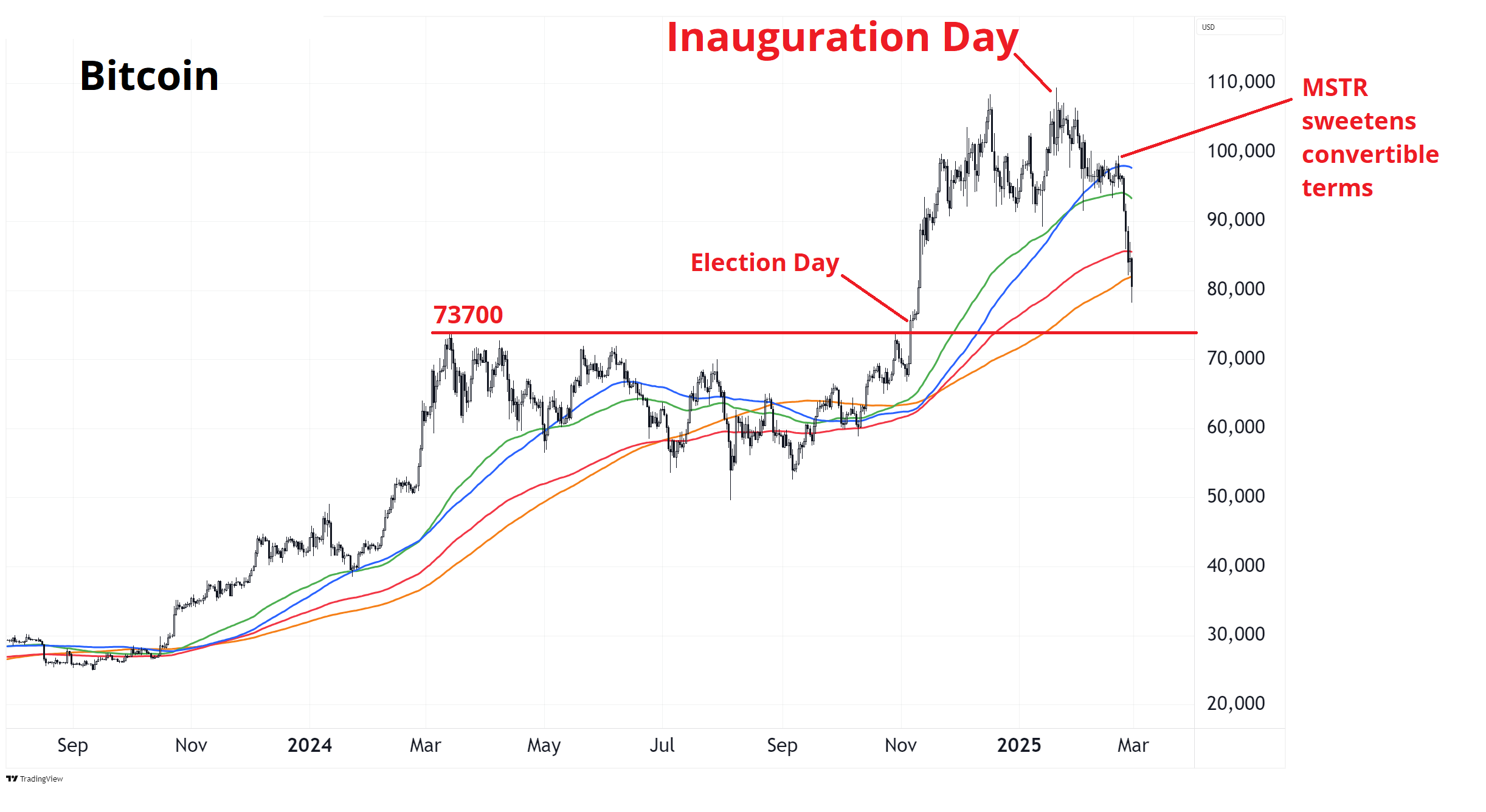

Crypto was a perfect buy the rumor, sell the fact, as it often is, as the massive post-election rally peaked exactly on inauguration day.

73700 is the old all-time high resistance (now support). Bitcoin was 69k the day before the election and 76k the day after. So those are your supports. 69100 / 73700 / 76000. That’s a pretty wide band of support, and then below that you have Michael Saylor’s average price of 66350.

Saylor’s DCA price is irrelevant to the company until the convertibles come due in a few years but could serve as a psychological point where people say “eek!”. We may soon need to come up with the correct term for negative bitcoin yield. While it’s hard to separate bitcoin-specific news from global risk appetite (because bitcoin is a tech stock proxy), it’s interesting that the day MSTR could not find buyers for their convert at the initial proposed offering price was the day bitcoin finally peaked for real (see chart).

Saylor has slowed his buying—the buyer of last resort disappeared. Obviously, though, you can also just say that all the stuff that drove the NASDAQ lower drove crypto lower and the clattering MSTR flywheel had nothing to do with anything. Or, you could say that perpetual motion machines are not real, as LUNA proved so dramatically a few years ago. The latecomers that tried to copy Saylor’s genius by trumpeting big treasury BTC buys at 100k look bad.

In that table above, you can see that PLTR and XLF worked, and basically nothing else did unless you took profit on 01JAN or on inauguration day. TSLA has had a crazy round trip as it trades more akin to a memecoin than a publicly-traded car company.

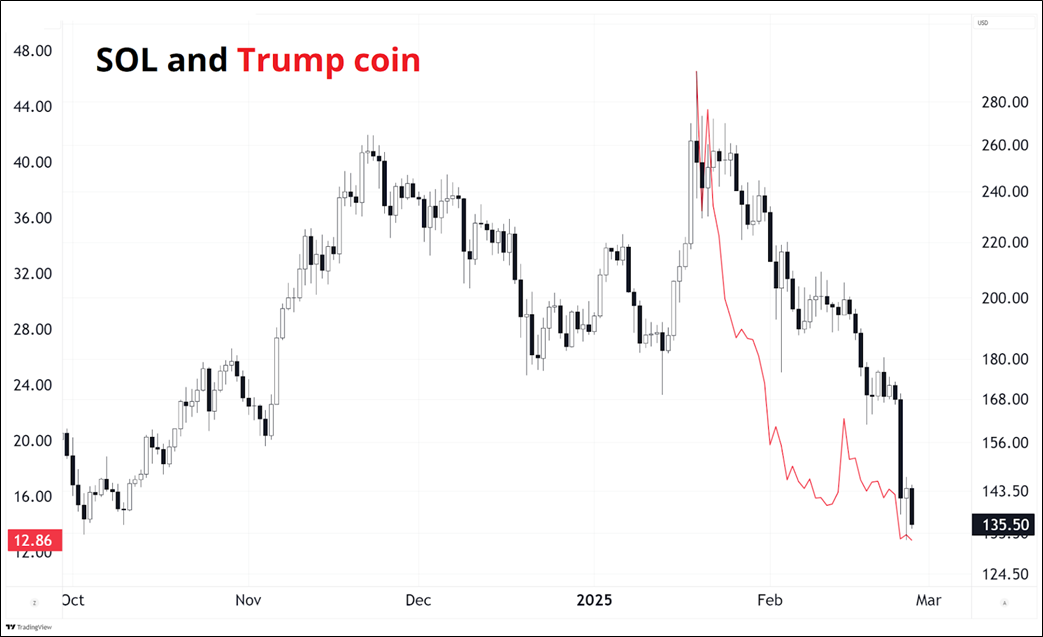

TSLA follows ETH and SOL, not F, GM, or MBG.

Bonus chart. Correlation causation yadda yadda.

My gold short (from am/FX) is performing well and the 2805 target is near. Meanwhile, the BCOM thing I talked about last week worked out gloriously as commodities absolutely tanked in a straight line along with global risk appetite. Here’s OJ futures.

That’s it for this week.

Get rich or have fun trying.

Great essay on the intellectual foundations of the broligarchy.

Silicon Valley’s Reading List Reveals Its Political Ambitions

*************

Useful risk management thread from Alexander Good

*************

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.