US equities zig zag while Korea flies.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

US equities zig zag while Korea flies.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Weird vibes this week as there is fear building about a credit crisis triggered by illiquid private credit, private equity, and/or software and tech issuance and credit quality. We are seeing some huge moves in names like Apollo (down 8%), KKR (down 5%) and the regional bank ETF (KRE, down 5% today and 10% this week). The funny thing about credit is that it gets tight at the worst possible time and loose at the worst possible time.

Private credit investors are starting to vote with their feet and after years of concerns that they were marking to fantasy, not to market… The tide is going out and we’re going to find out who is swimming naked. The recent spate of moves by private equity to unload assets onto retail has raised many eyebrows as this is the standard exit strategy insiders use when things get overcooked or look overvalued. Glencore in 2011 is the textbook example, along with the flurry of IPOs in 1999 and SPACs in 2021. When suits are looking for retail bagholders, it creates suspicion.

We continue to get strange and concerning blowups, most recently MFS, the UK lender who may have pledged the same assets to multiple lenders and is now leaving those lenders underwater to the tune of nobody-knows-how-much. Apollo is said to hold about 20% of MFS senior ABF debt.

None of this is super brand new news. The stocks of private equity have been underperforming for a long time, but there is growing angst that we are going to hit some kind of liquidity moment where investors all want out at the same time and that is not possible due to poor liquidity. Blue Owl was the scary thing last week, MFS is the scary thing this week.

This wobbly credit picture is one reason US bonds have been rallying in a slow, straight line for the past few weeks.

Outside of credit, the themes this week are familiar.

Iran could be attacked at any moment. Despite some conciliatory headlines between the U.S. and Iran, the behind-the-scenes action continues to look concerning as half the U.S. military is parked in the Middle East. The U.S. Embassy in Israel is moving non-essential employees out, and China is recommending citizens evacuate Iran and avoid traveling there.

Similar to the situation going into last weekend, there is a range of military outcomes from one-off strike to full attack that would yield a wide variety of market outcomes. Presumably any attempt at regime change is a different scenario than the one and done attacks on facilities in June 2025.

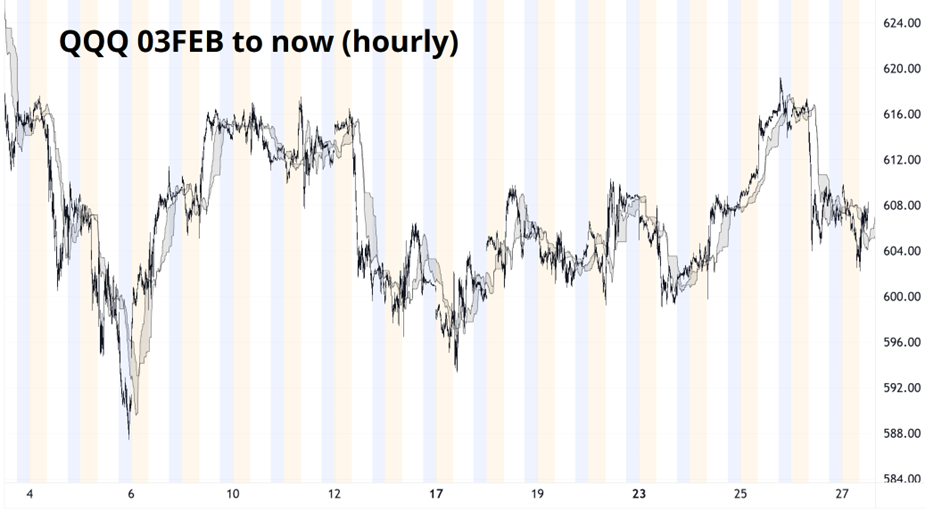

The other big theme is Buy SaaS / or sell SaaS depending on the day and buy memory and chips or sell memory and chips, depending on the day. This leaves the indices treading water at familiar levels and every time I look over at QQQ, it’s trading 607.

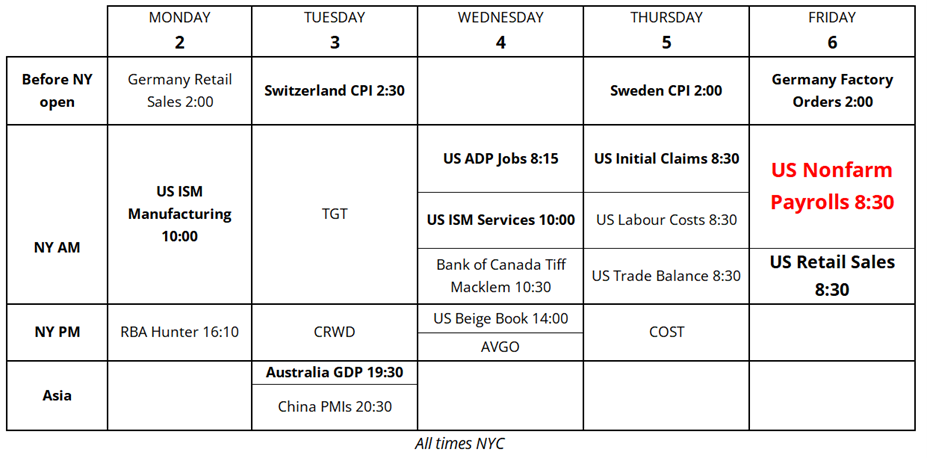

The U.S. economic data remains fine. GDP was weak but it’s noisy. Initial Claims remain low. Confidence is generally not great, but not collapsing. A few surveys (ISM, specifically) are showing greater signs of optimism but the reality is that the survey data has been completely useless for more than three years now. So there is not much reason to take a ton of heart from a few upticks in ISM. Next week we get February ISM and nonfarm payrolls. Here’s the calendar.

If you are worried that passive flows are too dominant and the market just buys the biggest stocks willy nilly with no regard to price or fundamentals, you will be greatly relieved by the massive dispersion in the stock market this year. Passive investors are completely swamped by active rotation in and out of software, megatech, oil, precious metals, foreign equities, and so on. All the stuff that people thought should have worked ever since 2017 is working now. Equal weight for the win.

NVDA hit another “good news/bad price” brick wall after earnings as they delivered everything any sane human investor might want, and the stock dumped. Blue is after-hours trading, yellow is pre-market, and white is market hours. Yuck.

The market has simply had enough of the AI Capex trade, with the exception of the memory and chip stocks like SNDK or KOSPI. But despite all the rage, Q’s are still just a rat in a cage. QQQ (the NASDAQ ETF) is unchanged this month, even as internals churn like crazy.

The real action in equities is outside the U.S. as American stocks continue to underperform on perceptions of AI overinvestment and weekly random policy uncertainty.

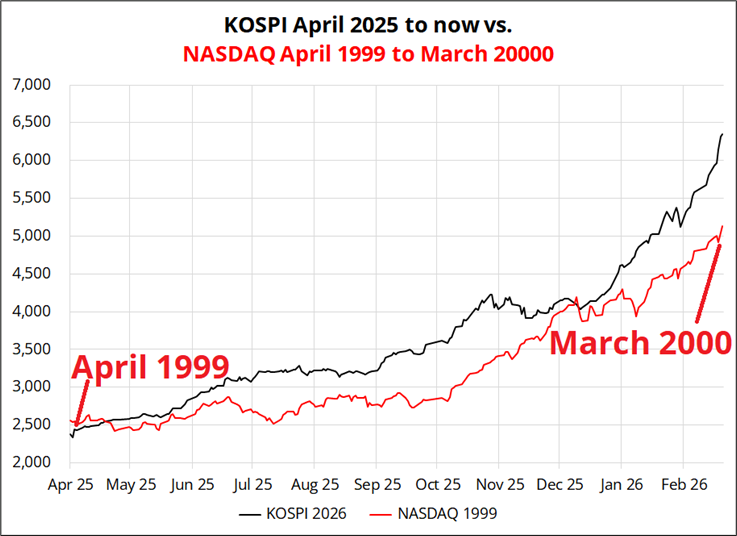

Korean stocks are in the sweetest of sweet spots as chip and memory makers there take the index to the sky like a sunbound pegacorn. Retail participation there is high, and the price action reminds me of 1999. In fact, the NASDAQ was trading around 2,500 in April 1999 before it ripped higher and peaked just above 5100 in March 2000.

This time, we have the KOSPI starting around 2,500 in April 2025 and it has now ripped above 6,000 in a similar time. I will not embarrass myself by overlaying what happened after, but here is the chart of that NASDAQ rally and the KOSPI rally. Note that they are the same y-axis because they both started at 2,500. No y-axis shenanigans here.

I believe this is an accident waiting to happen. Trade it as you will! Icarus was born in Korea, after all.

No he wasn’t.

Here is this week’s 14-word stock market summary:

Tax refunds aren’t helping so far. The market continues to rotate like a spirograph.

https://www.spectramarkets.com/subscribe/

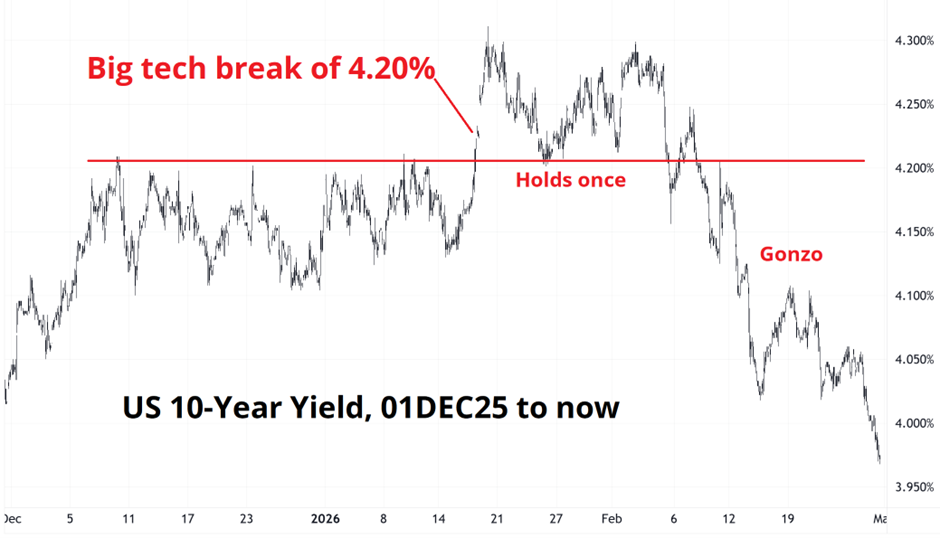

When markets don’t do what they are supposed to do, that’s a tell. When U.S. 10-year yields broke 4.20%, the market was expecting an impulsive move higher. Instead, yields flapped around for a few weeks, then headed South in a straight line.

While I generally hate when people say: “Bonds know something!” … I suppose I have to admit that you could argue that bonds sniffed out the credit and liquidity issues before the private equity stock prices did. Inflation looks to be in the rearview just as The Economist featured it as their big front cover in January 2026. Always remember that The Economist is telling you what happened in the past and what is fully priced in to markets.

My clients are not super happy this week as the most popular trades (long JPY and long CNH) have reversed. I was in the bullish JPY camp myself for a while and unfortunately Takaichi has now appointed doves to the BOJ and may or may not have had a dovish word with Ueda (depending on what media leaks you believe).

And we now know that the rate check was pretty much an unserious goofing around moment for Treasury Secretary Scott Bessent as Japan never agreed with the move and the U.S. had no intention of following up with unilateral intervention in USDJPY (obviously!). I (and most people in the market) assumed that Japan was on board if the US Treasury was doing rate checks in NY time. But they weren’t. Another example of the many strange government interventions in the economy over the past year. The U.S. drift toward State capitalism is taking me some getting used to.

AUDUSD is impressive considering how crowded it got there for a bit. It could easily have puked down to 0.6950 by now, but the buyers keep coming back. And next month is peak dividend season where you see the miners buying AUD to pay Australian holders their divvies. That is just one piece of the puzzle, but overall it’s hard to say anything bad about AUD right now. Solid.

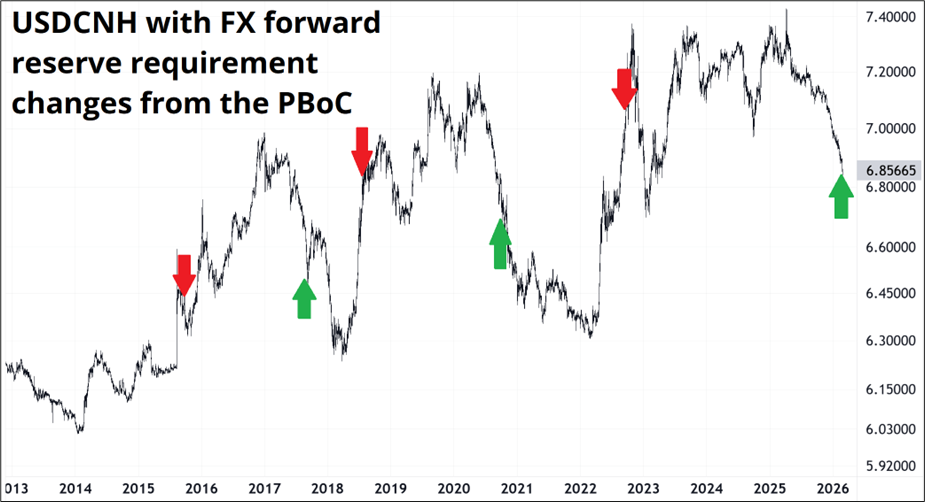

China is now officially pushing back on yuan strength as the market has become too one-sided and they don’t like giving free money to speculators. With most banks now advocating a long CNH trade and the slope of the move getting zippy, they have enacted the first pushback strategy: Tweak a rule and cut the required reserves on forward transactions from 20% to zero. These sorts of tweaks and rule changes are the standard approach of the PBoC when they want to signal dissatisfaction with either the pace of the move in the yuan, or the one-sided nature of sentiment.

These moves do not always mean that USDCNH will rip higher, but they make it much less fun to be short. You can see that in 2026, they have been allowing the slope of appreciation to increase significantly. This change of preference does not mean the slope has to turn positive; it just means it should flatten out.

Looking at past instances of these forward FX reserve requirement changes (thanks Simon Flint for the dates)… I have marked USDCNH with an arrow showing the PBOC’s intent for USDCNH.

You can see that these were not game changing adjustments. The issue, though, if you are speculating against the PBoC, is that they have a bottomless bag of other tools they can reach into. There are probably better trades out there at this point.

65k BTC. Looks like the middle of a 55k/75k range for the foreseeable future. ETF flows chasing price over the past few weeks. I have no strong view other than to play the extremes buying 58k down to 55k or selling 73k up to 75k.

I took profit on my long gold trade discussed here last week as the halt in yuan appreciation makes the trade a bit less attractive and I like fading the spike on geopolitical tension. Sure, gold could go higher on an Iran attack, but I have no edge forecasting that and it seems more and more priced in. Take the $200 and run. I am a trader, not an investor or a HODLer.

Oil is in a holding pattern, and it’s mildly interesting that it didn’t pull back at the start of this week, despite some fear that Iran might have been attacked last week. It trades well and if you want an Iran hedge, oil looks better than gold to me. It won’t go down that much on no attack, whereas gold might.

That’s it for this week.

Get rich or have fun trying.

Underworld vs. Fred Again GET PUMPED!

This one gave me goosebumps. Via Gittins. The drop….

*************

Depeche Mode when they were basically kids!

Smiles.

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.