~17 days until we know what is what.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

~17 days until we know what is what.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

Try Spectra School for free!

If you’re looking for a good way to spend 35 minutes or so, check out Lesson 3 of our flagship course “Think Like a Market Professional” for free. https://spectramarkets.com/lessons/tlmp3/ There, you will find the entirety of Lesson 3, for free, along with a link to my Learning From Legends video with Ben Hunt.

The lesson is called “Surfing the Narrative Cycle” and delves into how you can understand the stories the market is telling itself. If you like it, you can sign up for the full course and use coupon code LESSON3 for $250 off the $1200 price (i.e., you pay $950 for 16 lessons and 10+ videos.)

Hello Friday Speedrun readers! It’s been a few weeks, and we are edging closer to the launch of Trump 47. The leadup has been full of drama as Biden vs. Trump became Harris vs. Trump after the failed debate in June and now we are about to find out how much shock and awe DJT is willing to unleash in his second and possibly final term.

The consensus expectation is that this presidency will involve new tariffs. After that, you have a great deal of skepticism and confusion around the other policy pillars. Government spending reductions suggested by DOGE don’t seem particularly serious and the mass deportation promises will be nearly impossible to fulfill.

Tariffs are bullish USD, and the market is heavily positioned in FX because the policy impact on stocks and bonds is not clear. As such, dollar longs are the most excited and coherent cohort in financial markets right now. In other asset classes, some are playing higher stocks and lower bonds on deregulation, faster growth, tariff inflation, and more fiscal spending… While others are short stocks and long bonds on fiscal drag, economic shocks from tariffs, and high valuations and concentration in tech.

The Fed, which has been a key driver of markets over the past three years, has moved to the sidelines as inflation remains stubborn, but restrictive rates are no longer necessary. This has elevated the importance of the neutral rate because you can’t set Fed Funds at neutral unless you have some idea of what neutral actually is. And nobody has a clue.

Meanwhile, economic data in the USA is coming off the boil (a bit) and the situation in China, Europe, Canada, and the UK looks precarious at best and horrifying at worst.

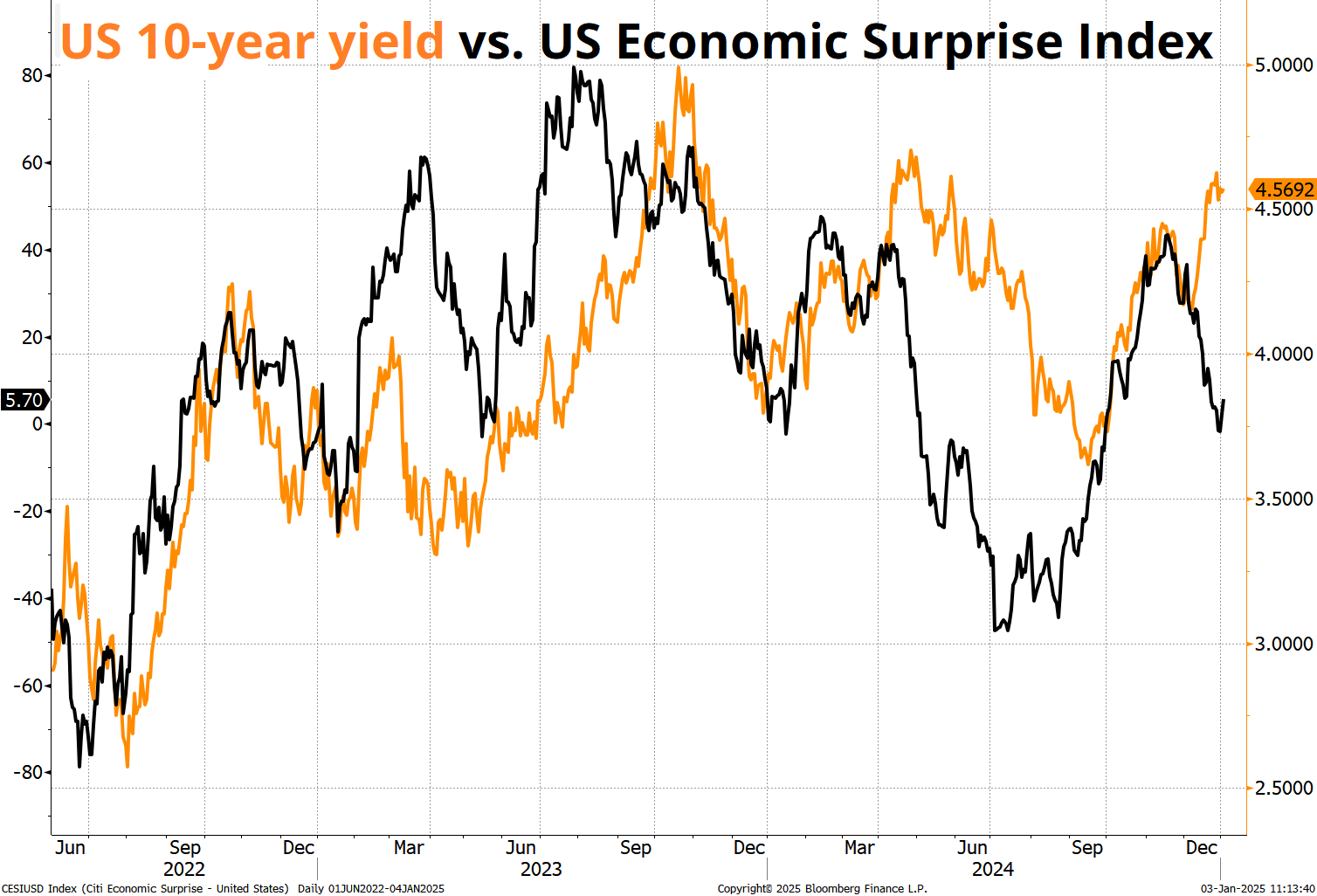

The disconnect between US yields and US economic data surprises is worth a look.

This suggests to me that there is risk premium in bonds for the Trump uncertainty, and I guess we can talk more about this in the Interest Rates section, but there are some scenarios now where 10-year yields are completely mispriced and trade quickly back to 3.70% in the next few months.

Don’t forget to buy the 2025 Spectra Markets Trader Handbook and Almanac here.

When I wrote the last Friday Speedrun, I included this chart of the NASDAQ:

Since then, the index broke down as the Fed came in hawkish in mid-December. Losses have been limited so far, with some eye-watering short squeezes offsetting some zippy selloffs to give you a chart that now looks like this:

You can see strong trends extend far away from the blue line (100-day moving average) and then correct to touch the green line (200-day). The current tiny correction has barely made a dent in the index as we are still well above both moving averages. A real correction would take us to 19550 in the NASDAQ and 5550 in the SPX, so this is not even a flesh wound yet.

The first 10 days of the year tend to be bullish for stocks as new inflows into passive funds (401k retirement plans) dominate, but then you enter a choppy sideways zone on the calendar.

Interestingly, the 12JAN top before the chop lands just one week before the 20JAN Presidential inauguration date. This is a key date for the year in macro as we see what Trump will declare in the opening days and weeks of his new term. Will he go scorched earth on close allies like Canada? Or is he bluffing the 51st state as a misdirection tactic before tariffing the heck out of China? Or neither? Or both? 17 days to go!

In single stock news, next week’s bank earnings will be of critical importance because the only sector getting more love than AI these days is the banking sector (XLF, FTW) as dreams of financial deregulation percolate once again. Glass-Steagall worked so well that everyone is naturally clamoring for more.

TSLA dropped a turd of a deliveries number this week after already trading weak after Elon Musk trolled the MAGA crew, but even as the company’s ageing designs are slowly becoming reminiscent of the Ford Taurus wagon, the stock has held in OK as it remains more of an option on future robotics and/or a memecoin celebrating Elon Musk’s made man oligarch status than an actual stock that represents a car company.

2014 Tesla Model S, gently used

People love to bandy about crazy visuals like this one…

But valuing TSLA as a car company completely misses the point.

TSLA is a car company the way MSTR is a software company. I.e., it’s not. TSLA is a kaleidoscopic collection of technofuturistic hopes and dreams. It’s a memecoin that trades partly off an oligarch’s ability to write future legislation. Maybe Exxon Mobil trades off discounted cashflows or book value or whatever. Tesla doesn’t. You can believe the story being sold, or you can not believe it. You can get on board, or stay on the sidelines. But don’t use DCF or cross-industry market cap comps to benchmark Tesla’s valuation. That’s not the right framework.

We talk a lot about what it means to use the right and wrong frameworks in Spectra School, btw.

This week’s 14-word stock market summary:

The trees have, in fact, grown to the sky. Anything can happen now. Anything.

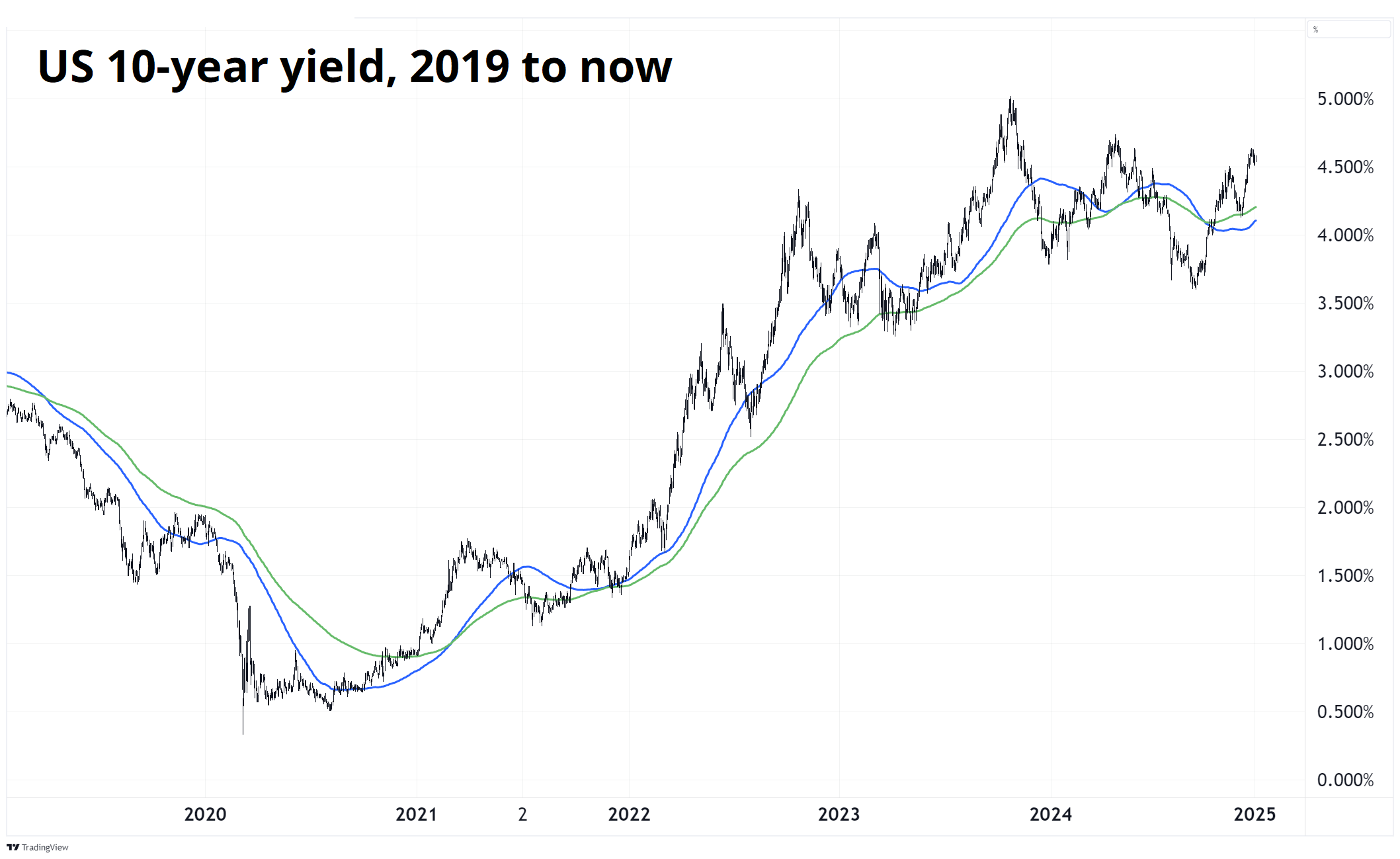

US yields have not made much progress post-FOMC, but they hold steady at high levels. You can see we are drifting back up towards the hallowed 5% level, where Bill Ackman and Janet Yellen announced the top in 2023.

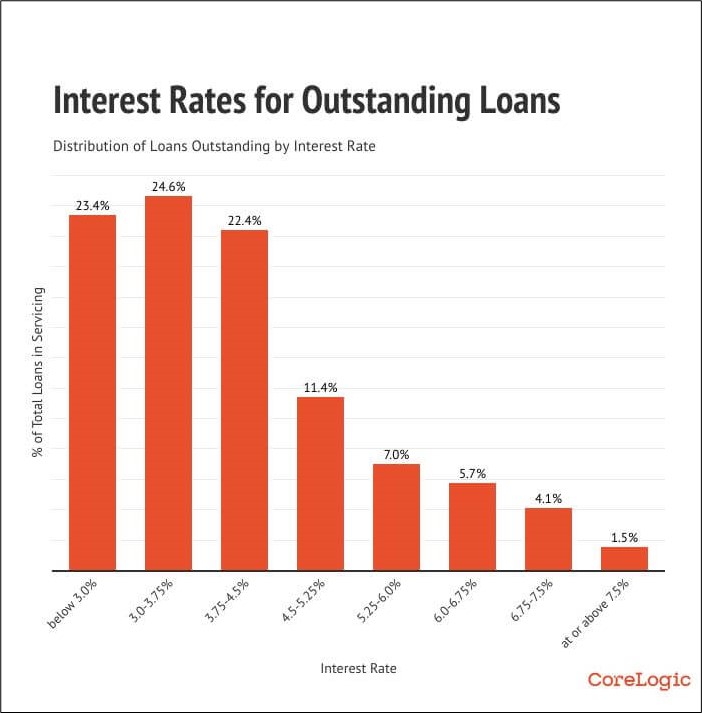

This move higher in yields and mortgage rates is jangling nerves around housing as it will slowly be time for more and more borrowers who were previously locked in sub 3% to renew at much higher levels.

As those sub 4.0% mortgages come up for renewal, an already moribund housing market will face new challenges. Most of the market (and the Economist!) have been wrong on housing for the past two years.

Residential construction employment and home building stocks have been incredibly resilient, but a weak housing market is one potential source of weakness for 2025. Maybe the homebuilder stocks have already sniffed this out. Here’s XHB, the homebuilder ETF, without The Economist articles on it. If you’re into technical analysis, note that we are now below both the 100-day and 200-day moving averages, and that’s one heck of a bear flag right there. The technicals imply $80 before $120. Nothing in Friday Speedrun is investment advice. I might be short today and long tomorrow. Trade your own view!

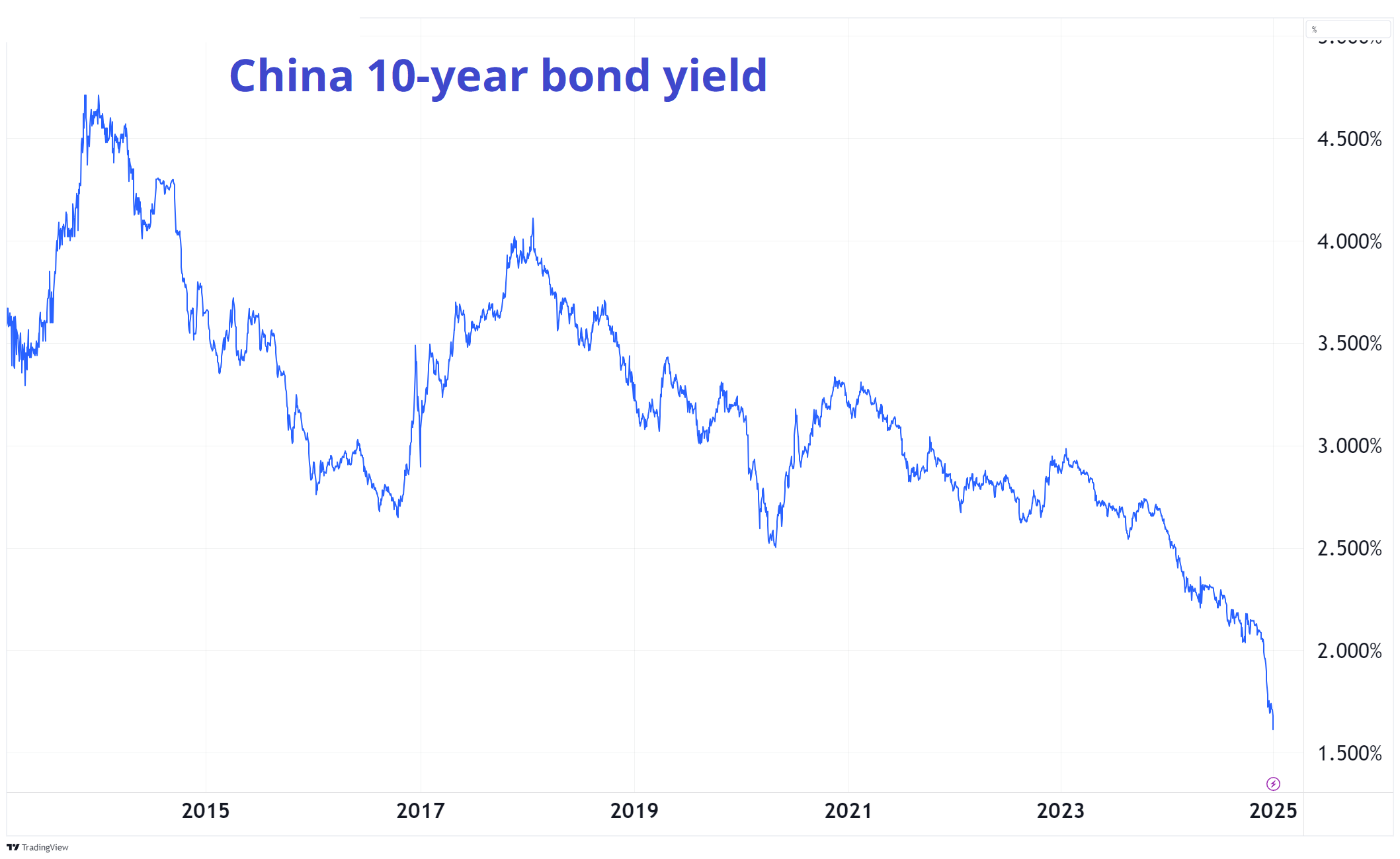

And I cannot write a section on interest rates without sharing the most epic yield chart in the world right now. WOWOWOWOWOWOWOwwwwwwwww…

This is what a deflationary balance sheet recession and “pushing on a string” looks like.

The market is long a lot of USD. Positioning is not a single variable to be used for making trading decisions, but at the extremes it is an important input. Right now, USD longs need a lot to go right in order to make money. They need big tariffs on Day One, or strong US economic data, or some kind of fiscal spigot release signal from the new administration. There is an asymmetry, in other words. If tariffs are slow played or scaled, or there is a negotiation phase like there was in 2017, the USD is going to get smoked.

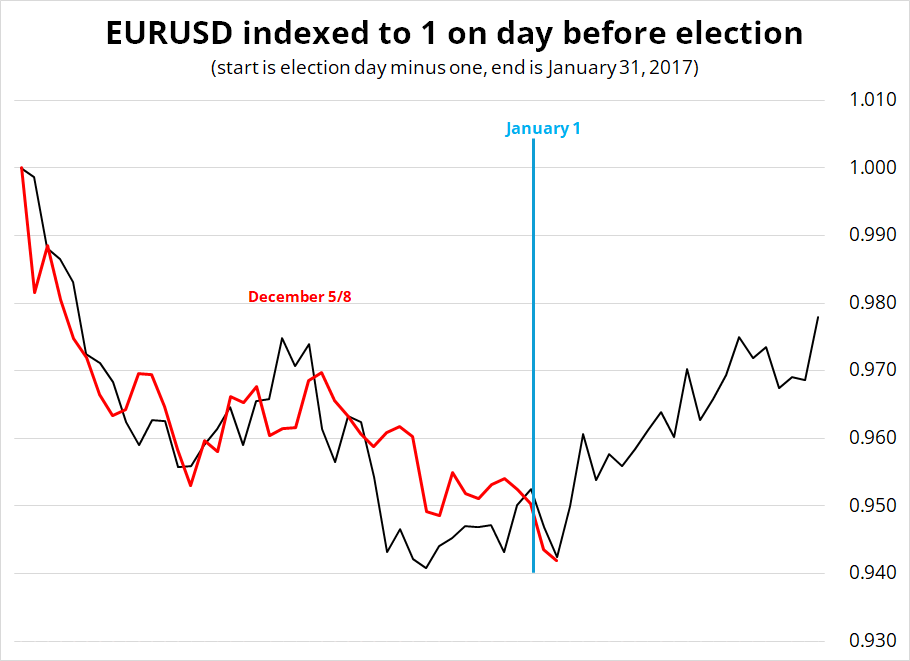

If you were not around in 2016, Trump got elected and everyone bought dollars because fiscal and because tariffs. Then, nothing really happened policy wise in 2017 as he focused on repealing Obamacare and other losing efforts and so the USD cratered throughout most of 2017. The parallels between the 2016/2017 period and the price action so far are stunning. EURUSD continues its freakishly accurate replication of the price action after President Trump was elected in 2016.

This analog will make sense until it doesn’t, of course, because if Trump enacts a 10% global tariff or a 25% tariff on Canada and Mexico on January 20th, the USD is going up, not down. That said, it remains an eerily-similar setup with the market max long USD at the highs and the clock slowly ticking as we await the policy principles.

There were many different features to the market in 2017, including a dovish BOJ that was holding rates negative, but there were also many similar features. The most strikingly similar aspect is that EURUSD rallied in August 2016, peaked just above 1.1200, consolidated in September, dropped to 1.08 in October, rallied a bit, then sold off down to 1.03 in November/December.

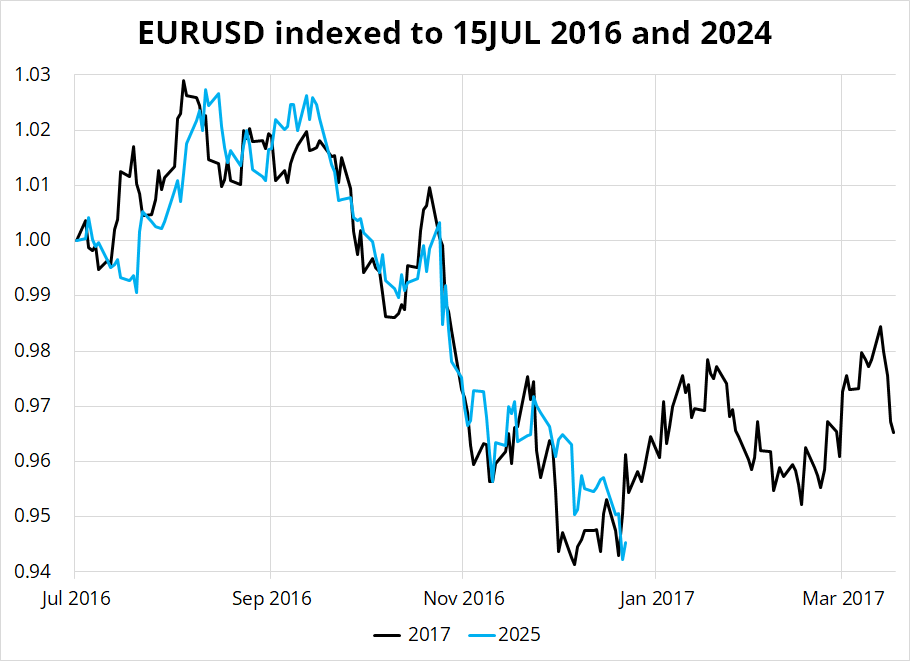

You can see in the chart that the fit is kind of incredible.

The two series are indexed to 15JUL of their respective years but given EURUSD was mostly trading on the exact same handles, the chart looks similar if you just use a normal y-axis. This year’s action is all just about exactly 150 pips lower than the 2016/2017 action. The summer high in 2016 was 1.1350 and this summer’s high was 1.1206 and the low in 2016 was 1.0388 and this low was 1.0226.

I don’t want to overstate the importance of this thing, but it’s hard to completely ignore the parallels. The onus on the newsflow is now to deliver some shock and awe, or bonds will rally, and the dollar will sell off.

It all comes down to the tariffs. Or the no tariffs.

Bee tee dubs: On December 13, in the last Friday Speedrun, I said USDCAD to 1.45 by January/February seems reasonable. We are basically there. The thesis played out well as both spot and USDCAD vol ripped higher. I think it’s a bit overcooked now, but if Trump does indeed place a large tariff on Canada, USDCAD will explode. It’s pretty much binary at this point for USDCAD. Big tariff = 1.50. No tariffs = 1.40. The only middle ground would be something like a tiny tariff on Day One with the promise to ratchet it up monthly unless Canada builds a border wall or stops all the terrorists or something something.

The MSTR story continues to capture everyone’s imagination as Saylor buys more and more bitcoin and the premium of MSTR vs. NAV has shrunk substantially. There are so many ways to look at MSTR, and most of them involve getting really excited or super angry.

The believers say it’s an option on further bitcoin appreciation. The non-believers say people are extrapolating from the past and in fact MSTR is an overpriced and pointless exercise in financial engineering.

When GBTC traded at a premium, it was a horrible investment, but at least people could justify it by saying “it’s the only listed way to play bitcoin!” Now, we have a litany of spot ETFs, so what optionality are you attempting to capture with MSTR? You’re paying a premium for leverage but leverage works both ways and there is no guarantee that the premium remains elevated. In fact, the natural path of the premium should be to head towards zero as MSTR sells more converts.

With a stock like GME, there is optionality. They might add a bitcoin treasury strategy, or they might start a new metaverse or dominate the NFT market or something. With MSTR, what you see is what you get. An increasingly large pile of bitcoin and more and more dilution until the premium disappears or stabilizes at lower levels. If the premium reappears, Saylor will slap it again. Again, with TSLA, there is optionality on hopes and dreams and future business lines. I don’t see any optionality with MSTR. It’s just a bitcoin ETF that trades at a premium.

So just like I hated to see people buying GBTC at $40 when bitcoin was at $10k, I hate to see people buying MSTR at $330 when bitcoin is at $98k. If you have an edge on predicting the growth and shrinkage of the premium and you are a professional basis trader in crypto—go for it! But buying MSTR as a leveraged bitcoin play feels really really bad to me.

If you want leveraged bitcoin, just use leverage and buy bitcoin.

It’s that time of year when everyone tells you that commodities and foreign equities are cheap relative to X, where X usually represents S&P or NASDAQ. They probably are, but they also were in 2017. So, I dunno. Maybe?

Oh! Here’s an article.

https://www.mining.com/chart-commodity-prices-slump-50-year-low-us-stocks/

Savvy readers will note the URL is “mining.com” so probably biased! But unbiased people always spend the turn of the year talking about the big discount on global equities and the high cost of US stocks. It’s true now but it’s been true for a really really long time. It’s not necessarily any more actionable now than it was in 2018, 2019, 2020, 2021, 2022, 2023, or 2024. Well, I guess it worked in 2022, but you get the idea. If someone is pitching this to you, they need to offer a specific explanation of why it didn’t work in the past but will now work going forward.

“Thing is low” is not a good reason to buy thing.

Even NYU Marketing Professor Scott Galloway is in on the act this year! And I have nothing but respect for him. I’m just saying this is a yearly meme.

https://www.profgalloway.com/2025-predictions/

That was 11.3545544 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

Better Letter makes fun of forecasters.

Forecasting out beyond 10 or 15 days in highly complex systems is basically impossible. Some hilarious examples in this article.

What happens to USDCAD if Trudeau resigns?

A wily veteran Canadian FX trader opines. Also, survey results asking traders what they expect in 2025.

An excellent commodity trading Substack from JJ, a pit trader who I can just about guarantee has been trading longer than you.

Sad, inspiring, and compelling. Avicii follows the tragic tortured genius path travelled by Van Gogh, DFW, Kurt Cobain, Robin Williams, and so many others.

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.