Most of the pillars of the big USD down trade have crumbled

There are 293 ways to make change for $1 USD.

Take a guess how many ways there are to make change for $100 USD.

Answer at bottom of page.

Most of the pillars of the big USD down trade have crumbled

There are 293 ways to make change for $1 USD.

Take a guess how many ways there are to make change for $100 USD.

Answer at bottom of page.

Long 1-month 1.8050 EURAUD call

Cost ~36bps expires 26AUG

Spot ref. 1.7790

Long 1-month 0.8760 EURGBP call

Cost ~33bps expires 26AUG

Spot ref. 0.8680

It is getting harder and harder to find a coherent USD bear thesis beyond the super-structural stuff like NIIP and deficits. There is no evidence of any capital flight anymore, Section 899 is off the table, there is no Mar-A-Lago accord, US GDP growth is steady around 2.5%, US unemployment is low, Initial Claims are falling, US inflation is sticky, Fed cut odds are shrinking, and the AI Capex story has accelerated post-DeepSeek.

I wonder if the market is about to have a change of heart moment as the policy uncertainty abates, the US soft landing continues, and US 2-year rates are third highest of the 20 countries listed on Bloomberg’s WB page (behind only Mexico and Brazil). It will take some chutzpah for the market to make another huge pivot as everyone was all in long USD in February, then all-in short USD in May. For so many humans to change their minds so aggressively all at once again will be difficult, especially as the structural story continues to lurk as a bearish force in the background.

Maybe it’s more realistic to expect a chopfest with selective attempts to go long USD against JPY, GBP, or AUD while the market buys EUR crosses and leaves CAD, CHF, and other more confusing currencies alone. Gold looks vulnerable as the USD debasement trade loses steam and policy uncertainty drifts meaningfully lower now that most of the big nations have agreed to some kind of trade deal with the US.

While some of the trade deals appear to include commitments by foreign countries to invest huge sums in the United States, most market observers are taking these commitments with blocks of salt given the US government’s tendency to tout huge and transparently fake headline numbers that often include previously-agreed commitments plus future commitments that are almost certainly never going to happen. Much as China never fulfilled most of its commitments in the Phase One trade deal of 2018, Japan and the EU are unlikely to send trillions of USD of new investment dollars to the USA this time around. One investment bank described the deals as “cloaked in vagueness” lol. This article from Nikkei captures the confusion and inconsistencies.

“Details released by the White House on its tariff agreement with Japan include many points that are unclear or out of sync with how Tokyo has explained it, including the date it goes into effect and the framework for Japanese investment in the U.S.“

The US administration deserves enormous credit, however, for managing expectations so well that now these deals on a napkin are enough to elicit a reaction that is something like “this is not as bad as feared!” or “this is the least bad outcome!” We can now pivot away from trade war angst to the flurry of economic data coming this week as the world tries to figure out whether any of this policy has an impact on the real economy, or the US continues to enjoy the multi-year soft landing that started in 2023.

The big events will be ADP, GDP, FOMC, and NFP this week, but you can also potentially get some movement on Core PCE, and the Quarterly Refunding Announcement. Of all the market movements that the government was hoping for, lower 10-year yields have been a notable miss so far, so it’s not impossible to imagine Bessent attempting to engineer something with his QRA announcement. I continue to like EURGBP and EURAUD higher via options, as explained in Thursday’s piece, though the overnight price action is sad.

On the Fed, people think that dissents are baked in the cake. Bowman and Waller both put up hawkish dissents in the past (Bowman on rates in 2024, Waller on QT in 2025) and are likely to post dovish dissents this time, arguing for an immediate insurance cut. I think you could just as easily argue for an insurance hike at this point, given inflation has been above target for 52 months (!), we have no idea where the neutral rate is, financial conditions are loose, inflation is about to rise, unemployment is low, wage pressure and labor supply issues will increase on immigration crackdowns, the wealth effect is in play with equities at all-time highs, and the deficit train is accelerating… But hey. I don’t get a vote!

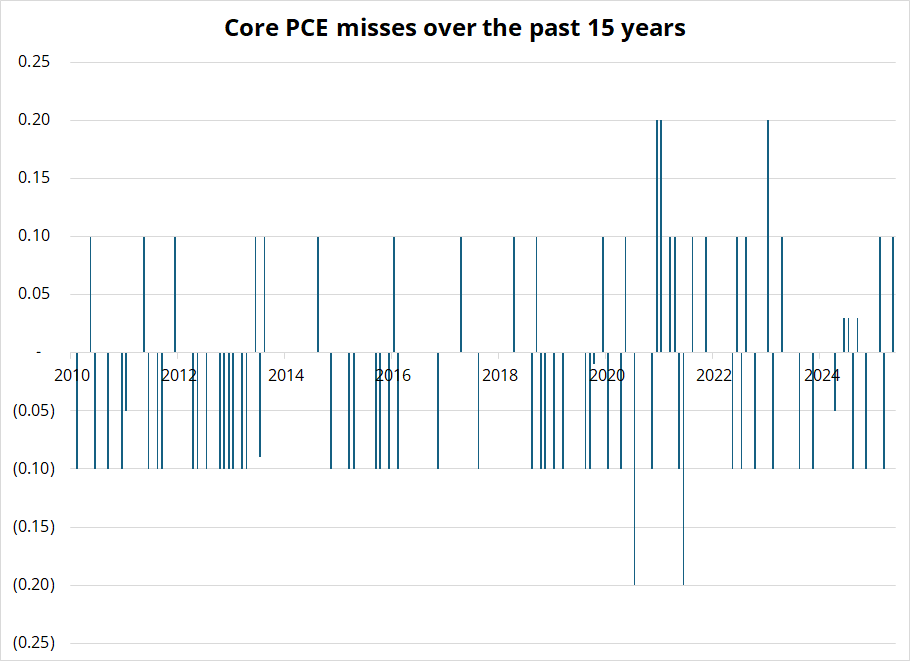

A quick point on Core PCE. It comes out after CPI and many of the components of Core CPI can be used to predict Core PCE. Therefore, misses on Core PCE (Actual economic release vs. Bloomberg median) tend to be small. They rarely exceed 0.1, as you can see here.

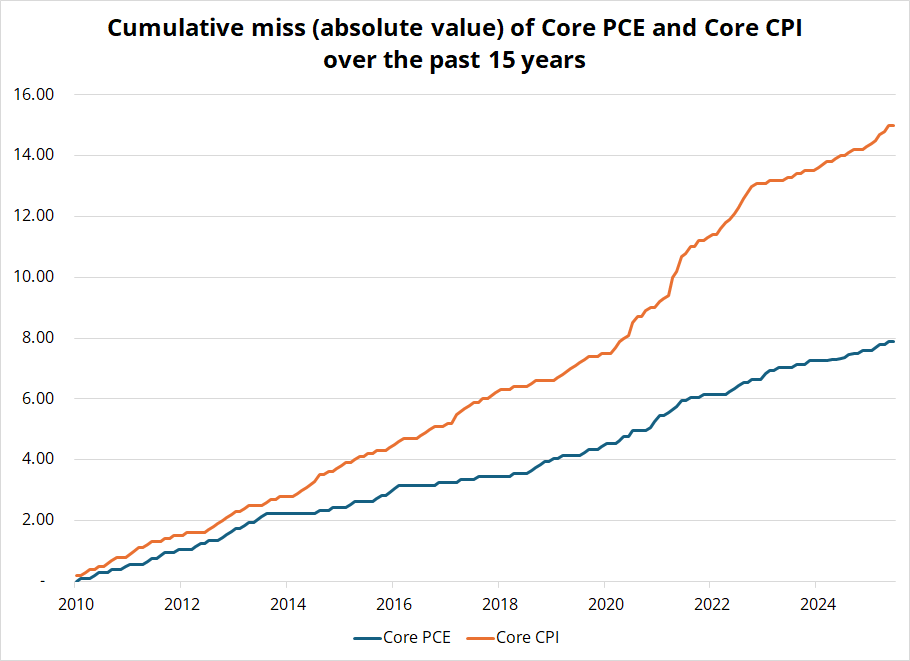

If you take the absolute value of all the misses in Core PCE and Core CPI and add them up over time, you can see the difference in how easy PCE is to predict relative to CPI. That’s why Core PCE isn’t often a market mover.

Number of ways you can make change for various US currency denominations

| 1 cent | 0 |

| 5 cents | 1 |

| 10 cents | 3 |

| 25 cents | 12 |

| 50 cents | 49 |

| $1 | 293 |

| $2 | 2,728 |

| $5 | 111,022 |

| $10 | 3,237,134 |

| $20 | 155,848,897 |

| $50 | 58,853,234,018 |

| $100 | 9,823,546,661,905 |

https://sites.williams.edu/Morgan/math-chat-archives/293-ways-to-make-change-for-a-dollar/