Zooming out a bit to look at AI, labor supply, and bubbliciousness

highlights

Three Big Themes

Current Views

Long NZDCHF @ 0.4770

Stop loss 0.4689

Long EURGBP @ 0.8674

Stop loss 0.8589

Long 26AUG 1.8050 EURAUD call

Cost ~36bps Spot ref. 1.7790

Hedge 1.8140/90

Long 26AUG 0.8760 EURGBP call

Cost ~33bps Spot ref. 0.8680

Un, Deux, Trois

There are three big themes right now:

- AI Capex dominance.

- Labor supply vs. labor demand.

- Froth in AI stocks and crypto DAT.

Let’s go through them one by one. First, the AI Capex dominance theme has been widely discussed as tech capital spending is the largest force in the economy right now and there appears to be a bit of a procyclical flywheel where the more big tech spends on AI, the more big tech earns from AI spending. August 27 features NVDA’s earning release, and that should give further insight into what exactly is going on under the hood.

Recent earnings releases from lesser AI companies have seen lower stock prices in CRWV (down 33% since earnings last week), AI (down 20% since last week), BBAI (down 30% since last week) as the bubbliest speculative plays have come back towards Earth.

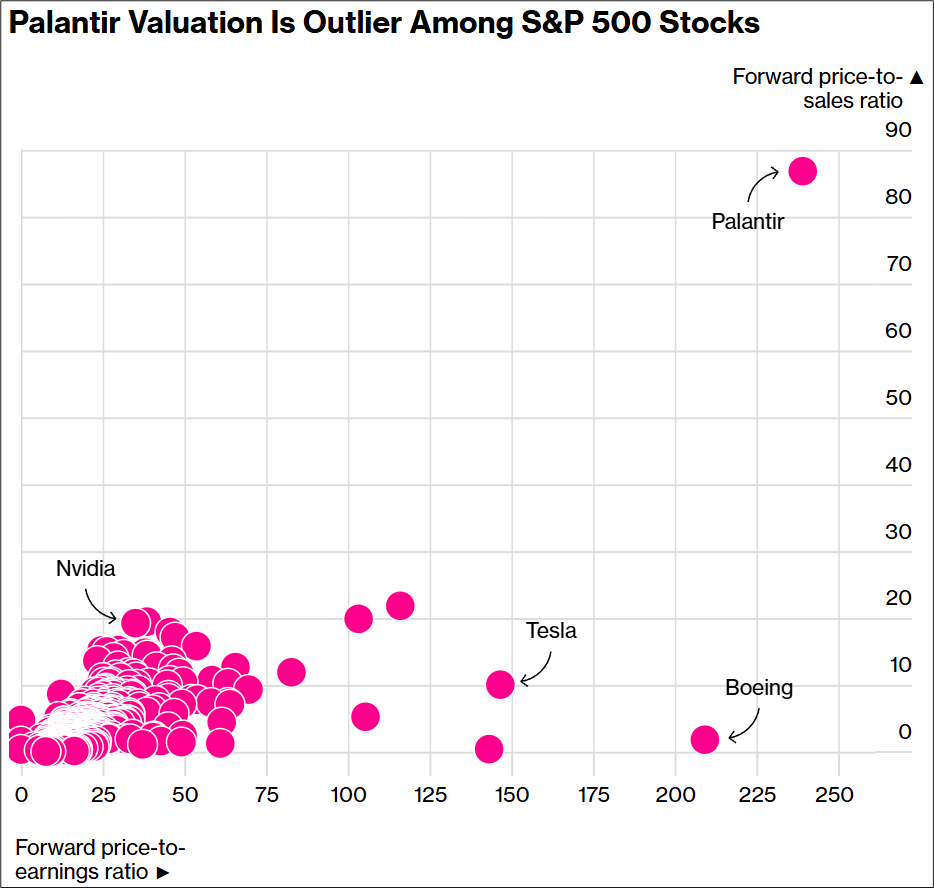

The big boys have seen big round trips as MSFT is back to flat after a 510/550/510 round tripper post-earnings, PLTR went 150/190/150, and META went 700/800/750. AI is as much a momentum play as a fundamental earnings play, and so the price action after NVDA will probably mean more than the numbers themselves. Tim Power is pitching FX vol around that data because NVDA has the power to move the entire market and there is little to no premium in FX options for their earnings.

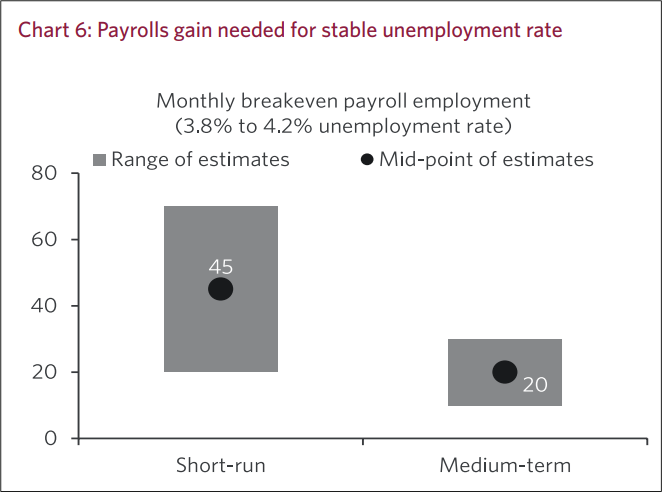

Second, I think the labor supply vs. labor demand story is probably the most interesting thing happening in macro right now, even though it’s pretty wonky. It is particularly relevant right now given the chosen topic for this year’s Jackson Hole conclave is: Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy. There is a litany of factors pushing labor force participation lower, and this is pushing the breakeven for NFP down and down some more, with economists now estimating that the economy need only produce 50k jobs or so per month to keep the unemployment rate steady.

Economists and macro peeps tend to be uniquely obsessed with the demand side in US labor markets, because the supply of labor was fairly steady and reliable pre-COVID. This focus on demand caught economists wrong-footed in 2021/2022 when we saw some low headline NFP figures, but low unemployment as the supply of labor dried up during the Great Resignation.

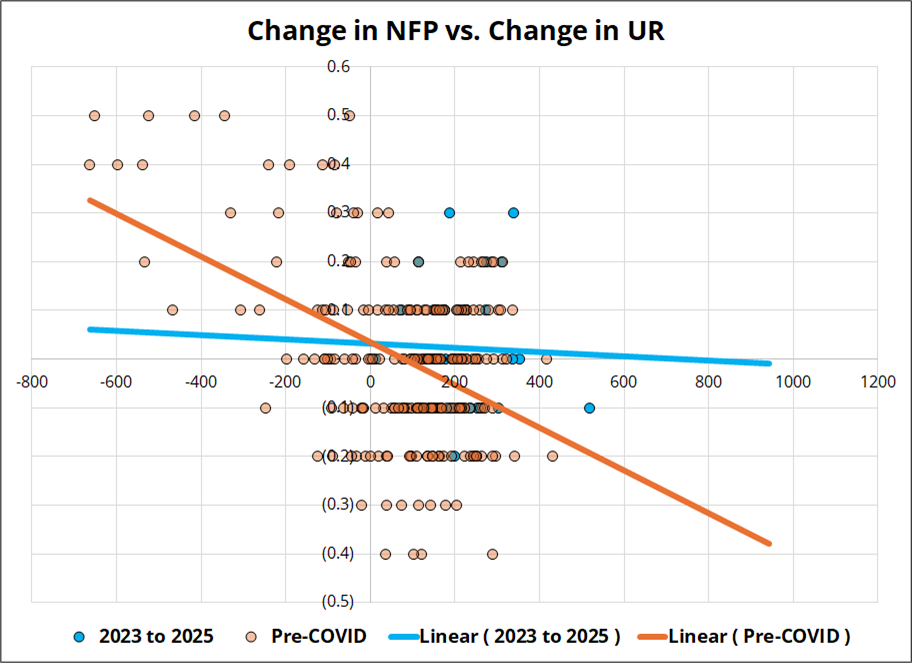

In a world of steady labor supply, strong NFP should reduce the UR, and vice versa, but this is not what has happened as labor force participation has plummeted since mid-2023 and immigration has stalled.

The chart is a bit weird-looking because the UR data is not continuous (it’s rounded to the nearest 0.1 on Bloomberg) and the sample for 2023 to now (the blue dots) is small (31 dots). Still, you can see that the normal relationship that held 2000 to 2019 is not holding. This will get more extreme as the US immigration crackdown eliminates more labor supply as it reduces the number of working age people in the labor force.

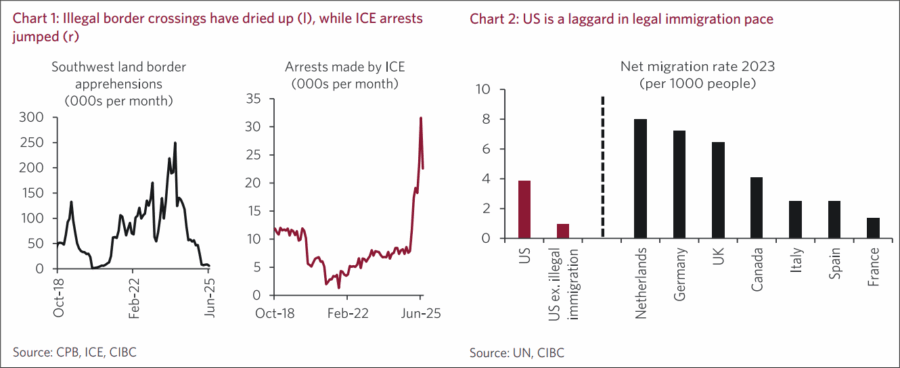

Avery Shenfeld, the excellent economist from CIBC, wrote a nice piece on this dynamic yesterday. Here are a few of his nicer charts.

And this one is a beauty:

Here’s how Mr. Shenfeld explains it:

It’s not just that population growth will slow to a crawl, but also an unfavorable shift in the mix of those living in the US. Our estimates include a projection that the labor force participation rate will grind lower to a shade above 62% over the medium term, as the economy loses immigrants with a high attachment to the labor force, and population ageing puts downward pressure on the labor force attachment of those left behind (Chart 7). That will mean prime-age worker participation, a gauge the Fed puts significant weight on, should move down another 0.5%-points from where it sits today, while older workers will see healthy 401Ks and increasingly decide to call it quits, falling to multi-decade lows.

This lack of supply also explains why Initial Claims are not rising. If you lose your job, you can find another one. Here’s Austan Goolsbee, President of the Chicago Fed:

“I want us to not over-index on monthly payroll employment when we’re in an environment where we don’t know what the breakeven is because we don’t know what the immigration flows are.”

And this piece from the SF Fed covers the Claims story in detail and shows there is no big problem in the labor market right now.

The third theme is the froth in particular sectors like AI and crypto. The absolute torrential flood of supply of Crypto Treasury stocks (aka Digital Asset Treasury or DAT) is a sign of a top for the entire space as the strong hands are desperately trying to dump as much supply onto retail as they possibly can before the music stops. As long as retail will pay professionals $2 for their $1 worth of ETH and BTC, the madness will continue, but the entire trade is procyclical. DAT issuance drives up ETH and that drives up the stock price and allows for more issuance and that allows for more ETH buying. Until it doesn’t.

Here’s a page I added to my bubbles scrapbook yesterday, so I can show my grandkids. We have had a memestock bubble, an NFT bubble, a SPAC bubble, and a DAT bubble (and maybe an AI bubble) all in the space of four years. Pretty amazing!

“There was a new bubble every single year after the Great Pandy, Grandpa??”

“Yes, you had to live it to believe it, X9acious.”

Update on sidebar trades

My call on RBNZ was wildly off the mark. I am surprised at how 3% is becoming the new 2% inflation target for central banks as the RBNZ joins the Fed in dovish leanings into rising inflation. Their confidence in the transitory nature of the current stickiness in inflation is kind of amazing. The stop loss has not been hit yet on the NZDCHF, but it’s close. It’s worth wondering whether I would be better off just hitting a bid here, but generally with trades like this, I stick to the pre-planned parameters as that’s the path of least overthinking (and least regret).

The EURGBP survived another attack on 0.8600. Despite strong inflation data in the UK, the pound isn’t rallying as the market looks at a stagflationary setup with a more hawkish central bank and does not like what it sees. The EURAUD call is now ITM. I plan to start hedging from 1.8140 to 1.8190. As always, all trade updates and tactics are in the page 1 sidebar.

Final Thoughts

- I still think Powell will sound hawkish, but I find it very hard to figure out whether it matters. The pricing is the pricing and the market doesn’t seem to care about Powell’s break-even rates for NFP vs. UR. I think paying the October Fed meeting looks attractive. 35bps are priced in and as long as the Fed doesn’t go 50 in September (which I think is a zero delta), you have a pretty good chance of making money at maturity while you might get a zippy winner if Powell holds the line and the US data cooperates in September.

- *TRUMP CALLS FOR FED’S COOK TO RESIGN. We have sanewashed what is going on in the US because the zone is so completely flooded nobody can keep up. But this is not normal. We are going to make Canada the 51st state and take over Greenland and Panama… Wait… Forget that! We are going to eviscerate the Fed and the statistical agencies and install hand-chosen puppets…

- A friend of mine had a great idea. Powell should come out for his Jackson Hole speech and give a 90-minute talk about central bank independence including the history of Arthur Burns, Turkey, Argentina, and Zimbabwe. He can then go on to explain why the Fed has decided not to hike rates despite four years of above-target inflation, cycle lows in unemployment, and generationally loose financial conditions. And then drop the mic.

- Two cats are racing across a river. One is named one two three and the other is named un deux trois. Which one wins?

One two three wins because un deux trois cat sank[1].

Have a Bubblicious day.

—

[1] I know I included this joke in am/FX once about 9 years ago but there are a few new subscribers since then—and it’s my favorite. If you recognize the joke from that long ago, thank you for your long-time patronage.