Another V.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Another V.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

So… It looks like the world is more worried about the shortage of generative AI tokens than it is worried about the shortage of crude oil.

Markets can only sustain maximum energy for so long before they burn out. The exception to this was 2008, when every single day was crazier than Liberation Day for about 250 days in a row. We knew that was insane at the time, but man… That was insane.

Anyway, the point here is that the market reached a point of maximum energy in March, started to get a bit bored of the war in Iran in early April and fully capitulated on all the war trades this week.

Macro punters studying supply shock megatweets have been badly hurt by all this because oil remains higher for longer but the stock market just does not care. This was visible on Monday morning of this week, when I published the following in am/FX around 8 a.m.

There are two less-famous behavioral concepts that I believe strongly in. The first is the cheer hedge. The second is the WTF indicator. This indicator (which stands for: What the Fudge?) triggers when every person I am talking to is asking “What the fudge?” about a move. This is happening this morning in stocks. People are beside themselves with some mix of confusion and rage because stocks are barely down.

That’s bullish.

By Wednesday, the WTF situation was resolved.

That thing is now 26750.

This type of indicator is a short-term thing very similar to bad news/good price and so it has now run its course. I find that setups like this (buy rumor/sell fact, good news/bad price, the Cheer Hedge, Sunday gap reversals, and more) quite consistently have a shelf life of 36-48 hours. There is no behavioral reason to expect further upside in stocks at this point, so I’m back to neutral. That does not mean I am bearish.

The macro story got less bad, but perhaps more importantly, the market came to the same realization it comes to at some point during every geopolitical flare up: This will not impact corporate earnings. You can debate whether or not that is true, but that is what the market has decided by repricing like this.

BUT OIL IS $100!

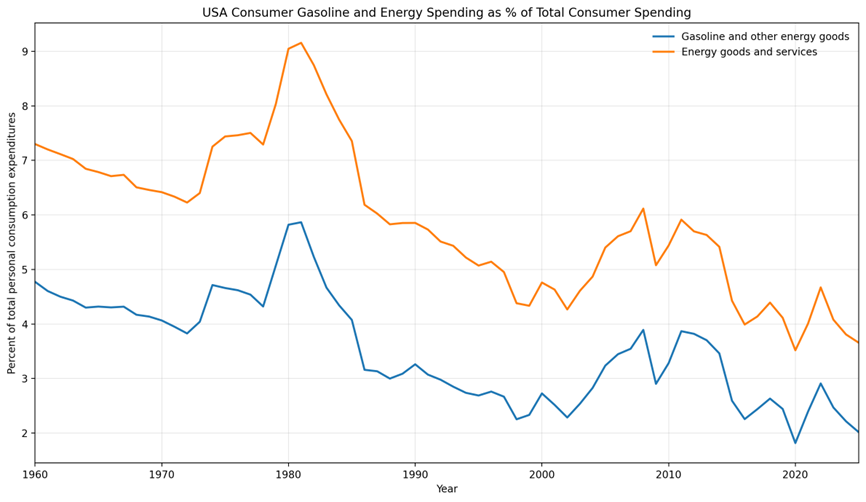

Energy as a proportion of consumer spending has been falling for years, so it’s not 100% certain that an energy shock today is anything like an energy shock 25 or 50 years ago.

And… Oil is $82.

You can find any number of ex-post explanations for the equity rally, but the important thing is that the “Hormuz is shut, calamity ensues” framework is wrong. Sure, it might be right eventually, but it’s wrong enough at this point to be completely useless for anyone trading any realistic time horizon. As an investor, if you sold the lows because of a coming global supply shock, you might thank yourself in three months when the gas stations are closed and we’re reenacting scenes from Mad Max. But if you’re a trader, that framework whiffed.

Markets are wrong all the time, and in this case, the market bought in to the idea that there was going to be a supply shock that would have a meaningful impact on economic growth and earnings. But in the background, the AI trade was refueling, the market was already max short software and other tech, and so the slightest sign of second derivative change in the Iran situation and……. Blastoff.

Ok, cool. So massive positioning, a wrong framework, and a cessation of kinetic activity in the Middle East got us here. But now what?

The annoying thing about these rolling macro shocks is that they blow up the economic data for ages and now we have to sit and wait at least three, if not six months to see the dust settle. Similar to Liberation Day, when the economics were not clear for a long time, we won’t know how much higher inflation and lower growth will result from the attack on Iran.

And by the time we know, people might not care. For example, tariffs did lead to higher inflation. The immigration crackdown did lead to slower headline job growth. And yet here we are.

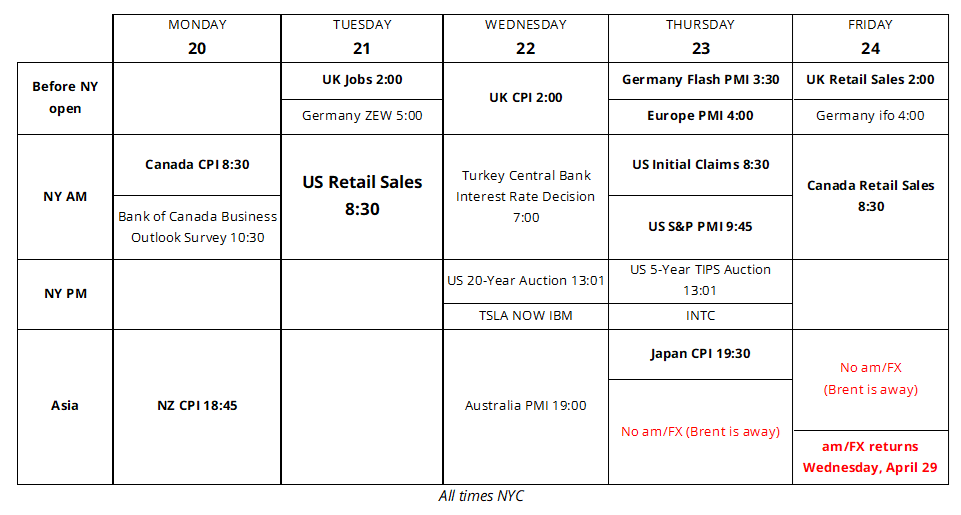

It’s funny these days when I create the economic calendar of the week ahead, I feel like I’m wasting my time because there is no economic data point anywhere in the world that can meaningfully move markets right now. Due to lags, the data we are looking at right now barely incorporates the war.

So, umm. Here’s next week’s calendar!

I wrote last week that the baseline assumption has to be that we have just witnessed another bullish v-shaped bottom and recovery of the 200-day. And I guess that’s what we’ve got. Stocks are making new all-time highs as I type this, and everything is awesome. MSFT and all the most-hated software names rebounded mightily this week after reaching a level of bearish sentiment rarely seen.

MSFT has been a textbook example of extreme sentiment in both directions. Everyone loved it at $525 and hated it at $360 and here we are. Given the mega rally we have already seen off the lows, the stock market is already starting to put some warning signs. But I’m not flipping short here. From a trading point of view, I have squared up longs and just decided to watch from the sidelines a bit.

Early signs of froth (ALREADY!)

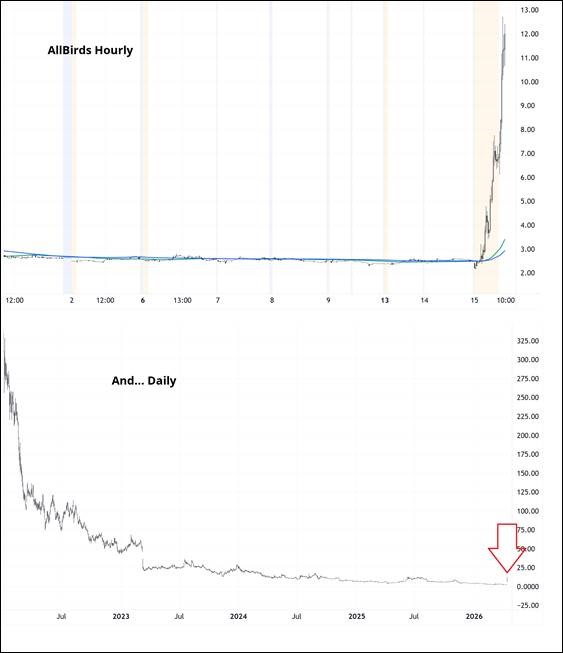

AllBirds converts from shoe company to AI company in a move reminiscent of the blockchain bullsh*t in 2018 and the crypto DAT nonsense in 2021. If you have a husk of a company teetering on bankruptcy why not stuff it full of the latest fad and pretend it’s a real company again!

To her credit, my wife always hated AllBirds for whatever reason.

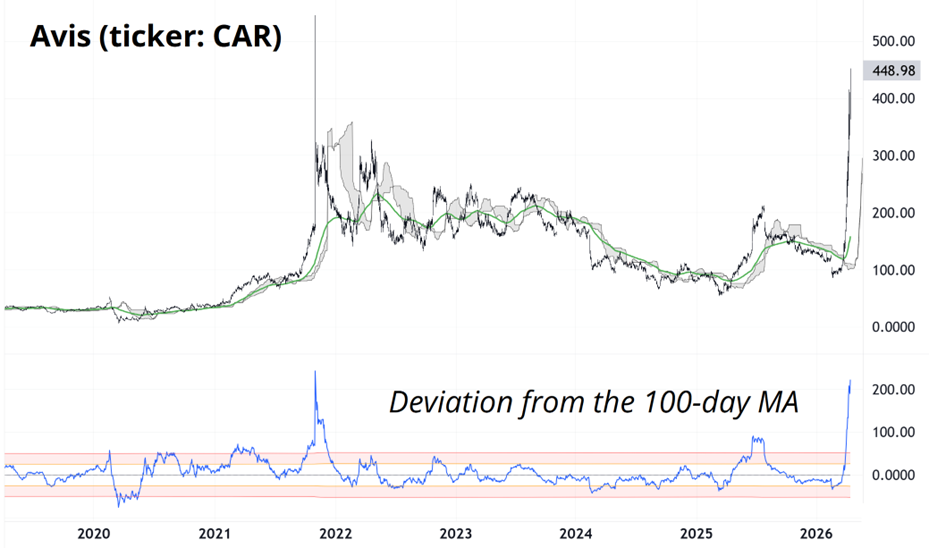

And you have another short squeeze in Avis. Just like we saw in 2021. There is no fundamental good news here, in fact the newsflow is getting worse. It’s just one of those stupid things that happens in markets when floats are thin.

The stock is hard, but not impossible to borrow. Note that we are approaching the same level as the peak of the 2021 squeeze. Gnarly. The only safe way to fade this is by selling call spreads. Puts are too expensive. Shorts are impossible to manage and expensive to hold.

New all-time closing high for Qs.

This thing is 648 pre-market as I write this at 9:16 a.m.

Looking forward, I am max nimble as I don’t want to chase things up here but don’t think a core bearish view will work, either. In stocks, there is no such thing as overbought. I am now just looking for fun stuff to play in either direction. Agnostic and flexible, like Charles Darwin if he did yoga.

I am particularly watching quantum stuff like INFQ and crypto stuff like PURR because it seems like the market wants to rerun the degen bull playbook now.

Here is this week’s 14-word stock market summary:

Max fear to pockets of silliness in five short days. Time for tactical trading.

https://www.spectramarkets.com/subscribe/

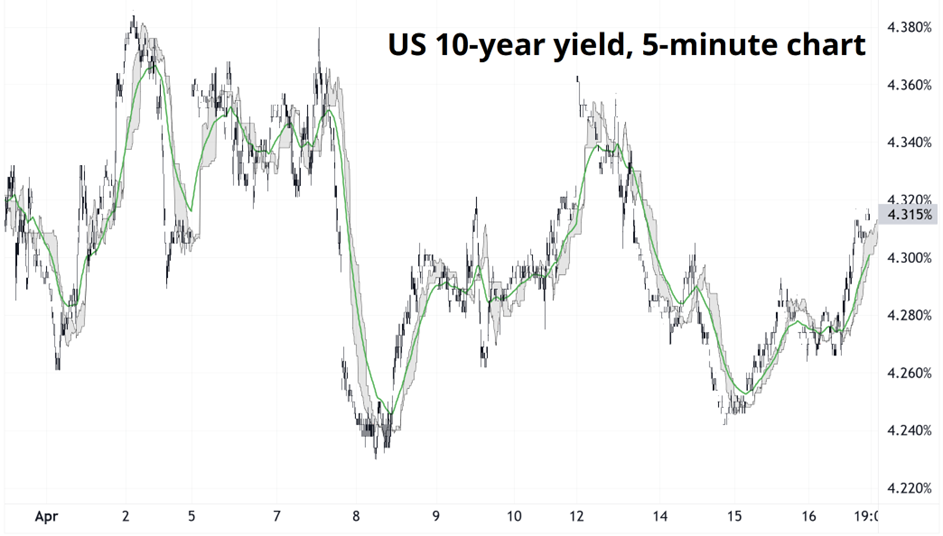

I am not exaggerating when I say that I cannot remember a single person asking about or talking about bonds this week. The pricing in the front end has gone to a fair level given oil prices look set to stay higher for longer and we are now going to have to wait and see what the economy does. The war in Iran has driven gasoline prices and mortgage rates higher, but it’s hard to know whether that inflationary impulse will be fully offset by reductions in spending elsewhere.

The U.S. 10-year yield has been steady this month. Here’s the chart:

If you made money trading bonds in April, you probably have a good franchise seat. But tell your boss it was all alpha.

Last week’s Friday Speedrun covered my main view in FX which is that the USD is done rallying. That said, I am not confident it needs to sell off aggressively. My base case for the next week or two is that FX is in a range and we go nowhere. So anything that’s in the money from the short USD side (especially if it’s long vol) is probably going to be less fun for the second half of April than it was for the first half.

I did some vol-selling stuff in USDCHF today, and I don’t expect much to happen given the lack of newsflow on Iran and the irrelevance of the economic data. How is one supposed to have a strong short-term view when there is nothing going on?

That means: Short vol, long carry, and modestly short dollars if you must. The DXY failed exactly at the top of the range, right as month-end USD buying petered out, and we are now in no person’s land, chartwise. I know the use of person there will really bother some people—that’s why I did it.

PSA: If you receive an email that contains the word “petrodollar” … Hit delete without reading.

The market seems to have mostly given up on trading or talking about crypto these days. I mean, it still exists, but the degens are all trading quantum computing stocks and oil. It’s kind of amazing.

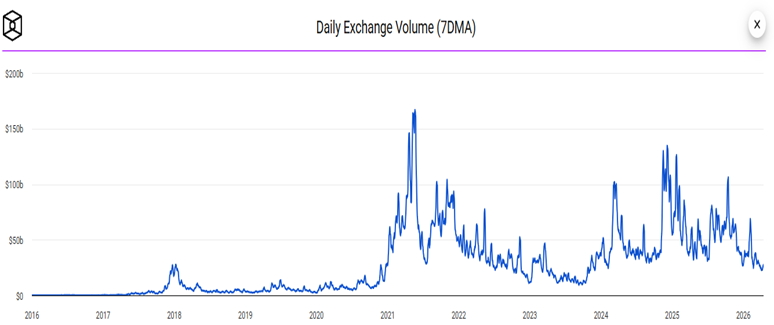

Here’s total exchange volume for crypto. Not pretty. This fits with my thesis that bitcoin has run out of narratives. This does not mean it will never have a narrative again, it’s just that nobody cares about it today. The bears are bored, the bulls are bored. It feels like there are entire days it doesn’t move.

You can see the peak in volumes right when Trump was elected. The Crypto President narrative has not worked out very well. In fact, it has reinforced the simplistic normie view that crypto is a massive kiddie pool for fraud.

https://www.theblock.co/post/397675/world-liberty-financial-new-proposal-criticism-justin-sun

Go HYPE! I did not go long, but I’m cheering for you.

I still can’t believe they named an oil after me.

The unlikely combination of higher crude and higher stocks was the winner this week as we saw a full abandonment of the negative correlation that dominated throughout March. As we enter Week 8 of this 4- to 5-week war next week, the market is bored.

Narrative flip! I would not be shocked if we start hearing about a massive glut of trapped oil coming back to market in months to come and oil prices go back to $70. Stupider things have happened. In fact, that’s basically what happened in 2022/2023. The market just accepted the absence of Russian crude or the fact that it was all being redirected. Economies are flexible and they adapt quickly.

Alternative scenario: The market is on crazy pills, oil DOES go to $200 and all heck breaks loose.

I’m ready for both.

Note the triangle break in Crude.

That’s it for this week.

Get rich or have fun trying.

Familiarize yourself with the concept of Cognitive Surrender. It’s a real thing and you need to fight it.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6097646

*************

*************

*************

*************

*************

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.