Tokens and chips, not oil

Crazy unfiltered photograph of HK from @bauhiniacapital on X

Tokens and chips, not oil

Crazy unfiltered photograph of HK from @bauhiniacapital on X

Short USDCHF vol expiring 30APR

Sell put spread: 0.7800/0.7780

Sell call spread: 0.7860/0.7880

Risk 1 to make 1.1

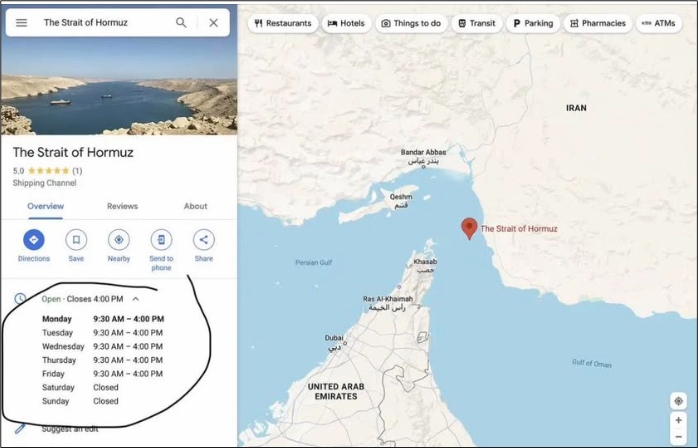

Strait of Hormuz update:

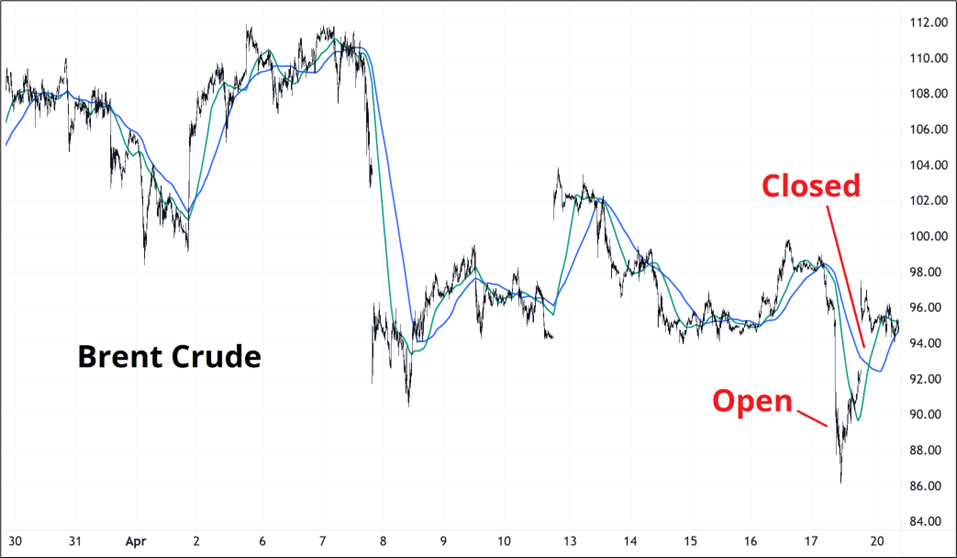

Oil up but still near the lows, so not a huge fear trade going on.

We remain well below the scary levels in crude and tech earnings are coming. This week we get some upper tier B-listers like TSLA, INTC, NOW, and IBM while next week the stars come out (AMZN, MSFT, META, GOOG all Wednesday and AAPL Thursday).

It is hard to be overly bearish stocks, and this little blip lower is probably another opportunity to buy as megatech has cheapened up and the market simply does not find the Hormuz story compelling anymore. We are in Week 8 of the conflict now and while the ceasefire looks set to expire in less than 36 hours (8 p.m. NY time on Tuesday), it’s hard to make a strong bear case for stocks, even if and when it does. As discussed in Friday Speedrun, the shortage of chips and tokens is more important to the market than any shortage of oil or fertilizer.

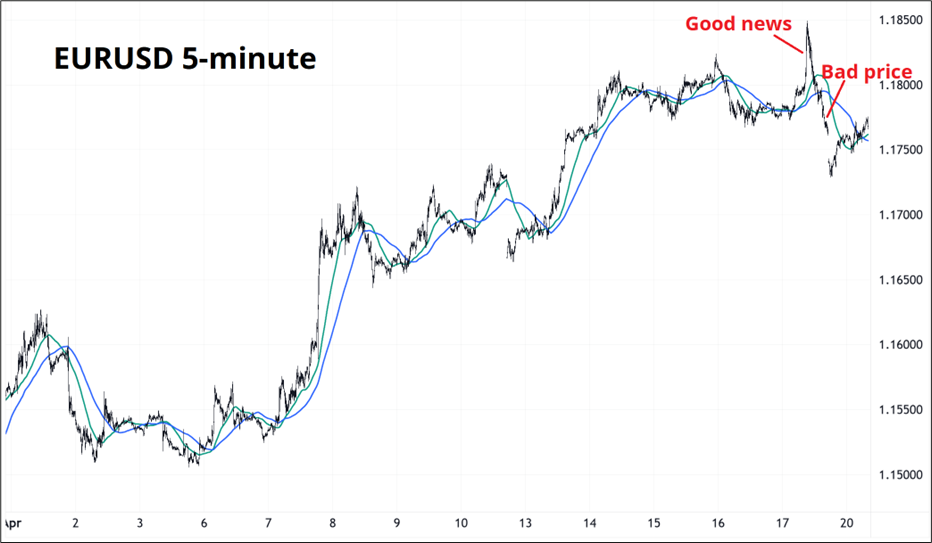

The same can be said for long USD—it’s a tough case to make. One argument in favor of long dollars is the pathetic price action in EURUSD on Friday after Iran seemed to announce the supposed reopening of the Strait. EURUSD rallied up to 1.1848, but the move looked forced and was swiftly rejected. We were back below 1.1780 by the close. This supports my theory of low-vol mean reversion for a week or two as there is no reason to engage heavily in the USD trade from either the long or short side.

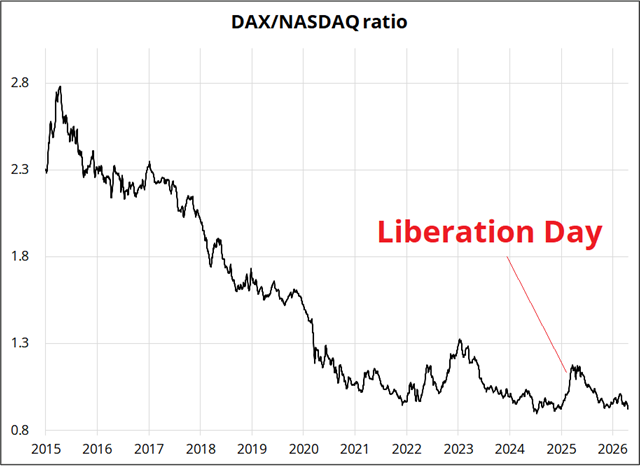

I suppose you could argue that the return to bullish sentiment for AI also introduces the possibility of a return of the US exceptionalism trade as the DAX/NASDAQ ratio is getting back down towards the all-time lows, but that’s not really true yet. Better to wait for a cleaner setup. Right now, we have no visibility on the war, no visibility on the U.S. economy post gas price spike, and nothing interesting on the techs or positioning side.

The DXY is right in the middle of the range. The good news/bad price setup in EURUSD has been resolved by a zippy little move to 1.1730 and now we are in a sort of boring equilibrium state.

On March 3, a client who doesn’t trade much USDJPY sent me an email:

Not really sure the obsession with usdjpy is?

It’s the same price basically everyday

And in the weeks that have followed, he keeps sending me emails that say (essentially): Still 159 LOL.

He has a point! It’s good to ignore things that are not moving. When I blasted a suggestion that the crap out in oil is bearish USDJPY, a different client responded: You mean the thing that never works?

I am not a believer in not doing a trade because it didn’t work in the past because that is blind extrapolation. If you thought that way, you would have been short USDJPY from 75 to 150 and long JGBs from 0% to 3% because long USDJPY and short JGBs never worked for years, either. Until they worked. That said, the point is valid: The bar for a USDJPY short (or CHFJPY short!) should be high right now because the base case has to be that they are going up or nowhere.

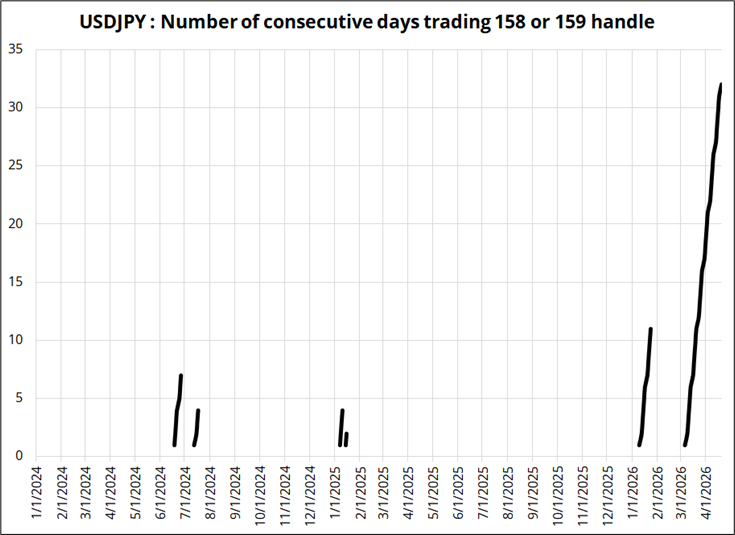

This chart kind of says it all:

Which has resulted in quite the ugly little flag formation:

We are hemmed in by oil importers buying USDJPY and fear of intervention and large JPY shorts capping the topside. The first day we pass without trading on a 158 or 159 handle, I will take that as a regime shift. Otherwise, the base case is more nothing.

This story from Kyodo claims to know the outcome of next week’s BOJ meeting:

The Bank of Japan is likely to postpone raising interest rates and will raise its inflation forecast.

It was learned on the 20th that the Bank of Japan is likely to refrain from raising interest rates at its monetary policy meeting to be held on the 27th and 28th. The policy interest rate will be maintained at around 0.75%. Although domestic prices are expected to rise due to persistently high crude oil prices, the Bank of Japan intends to assess the impact on the economy first. The inflation forecast for fiscal year 2026, which will be announced after the meeting, is likely to be raised.

Given the current financial environment, where real interest rates, even considering price fluctuations, are low and at an accommodative level, the Bank of Japan was exploring the possibility of raising interest rates. The ceasefire talks between the U.S. and Iran are also fluid, and the final decision will be made after confirming the situation until the last minute.

Bank of Japan Governor Kazuo Ueda stated at a press conference held in Washington, D.C. on the 16th (17th Japan time) that “it is very difficult to determine how to respond to the worsening situation in the Middle East through monetary policy.” He emphasized that “policy decisions will be made while reviewing the risks.”

The Bank of Japan is expected to maintain its stance of continuing to raise interest rates, given the high wage increases seen in this spring’s wage negotiations. This is likely due to concerns that the US-Israeli attack on Iran could cause oil prices to soar, leading to “stagflation,” a situation where inflation and economic deterioration occur simultaneously.

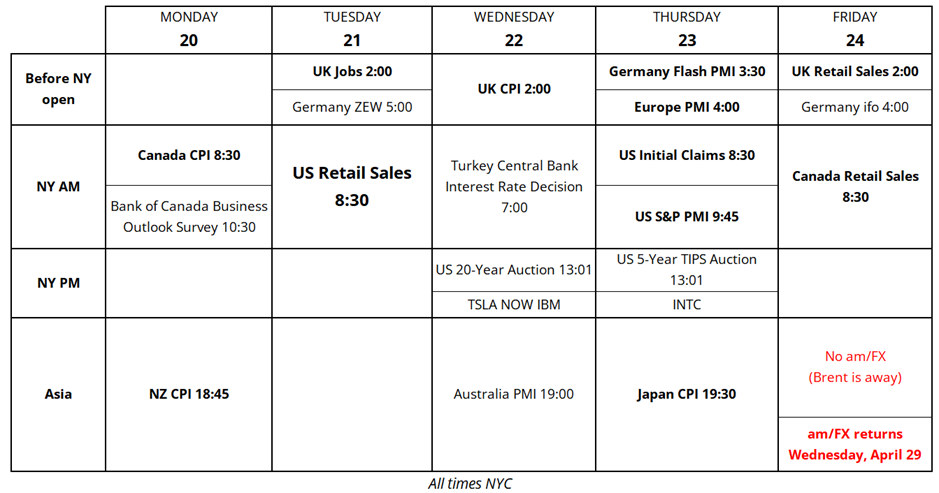

Here is this week’s economic calendar; but does economic data really matter for markets? (No).

I suppose Retail Sales could matter a bit, or maybe we get a flicker of interest on the CPI releases. But earnings next week and oil prices up or down are the main drivers now, not economic data.

Positioning report follows.

Have a gorgeous week.

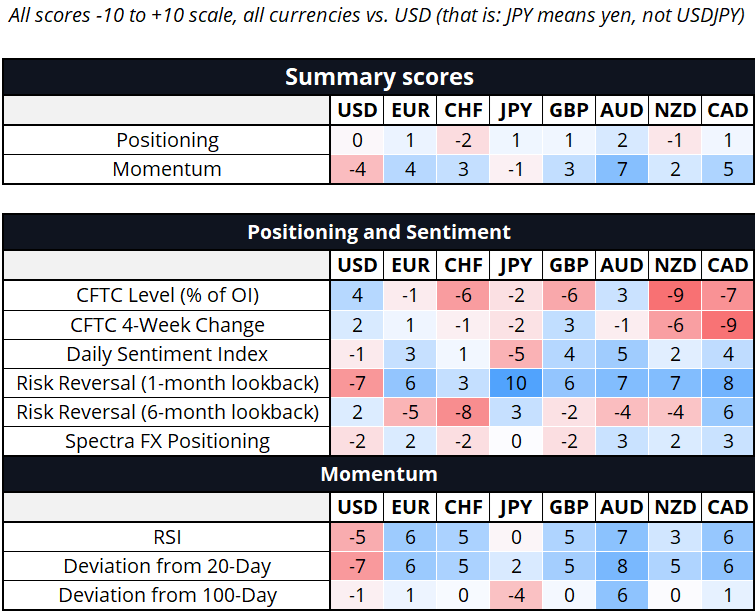

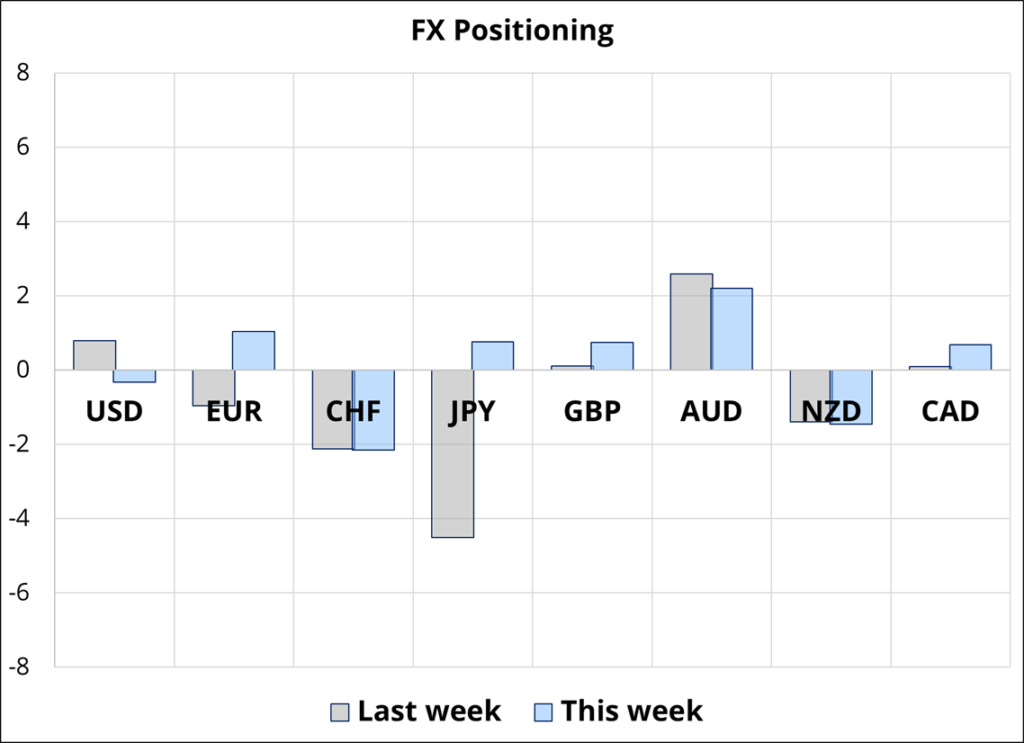

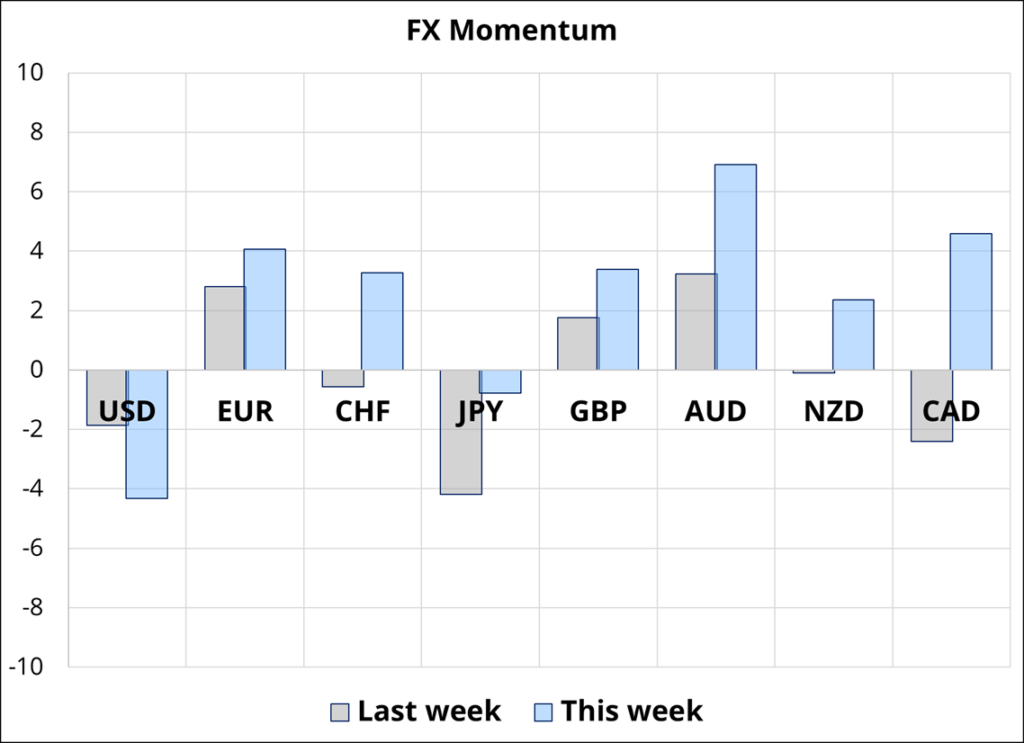

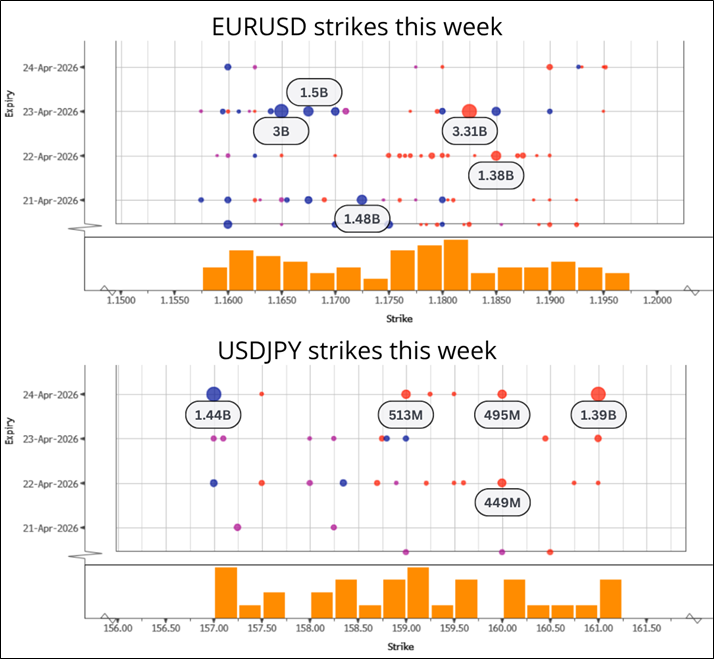

Hi. Welcome to this week’s report. (To read about how I use and trade this report, see here.) Positioning is close to home this week as our USD score is right on zero and most pairs are showing low conviction. The risk reversals in JPY have moved enough to put JPY in bullish territory for the first time in a while. Large EURUSD strikes above 1.18 might explain the big rejection up there last week.

Crazy unfiltered photographs from @bauhiniacapital on X

The sun is low enough that its light is traveling through a longer path of air. Hong Kong often has humid, hazy air with aerosols in it: pollution, sea salt, moisture, and sometimes dust or smoke.

Those particles scatter the shorter wavelengths first, especially blue and green, so what gets through most strongly is the red/orange end.

The haze also dims the sun enough that a phone can capture it as a defined red disk instead of a blown-out white blob.