Low volatility is the big story, despite wacky and wonky pockets of vol here and there. Wake me up after the election (when September ends).

Becoming who we are…

Low volatility is the big story, despite wacky and wonky pockets of vol here and there. Wake me up after the election (when September ends).

Becoming who we are…

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

Here’s what you need to know about markets and macro this week

![]()

Before we get started…

Get the tools and practical frameworks you need to understand markets in the real world. Course info, syllabus, and FAQ on the website.

Check out the video for a quick run-through. The course is perfect for traders, sell-side analysts, wealth managers, RIAs, finance students, econ grads, central bankers, and anyone outside finance who want to learn how markets operate in the real world. www.spectramarkets.com/school

Hello! I was off for a few weeks and now I’m back and older than ever. June next year will mark my 30th anniversary in FX markets, which is impossible to believe, but also true.

The macro landscape has looked fairly similar for the past few months. Softening inflation, weaker but still solid jobs market, 2% GDP growth, assets super buoyant (driven by megatech), housing prices solid, homebuilders ripping, China soft, etc. These things have all been mostly true all year.

September FOMC is fully priced for a cut and that makes sense to me. The Fed is getting exactly what they wanted, and the soft landing has been delivered successfully.

While the current pricing is of note, perhaps more notable is the lack of volatility. See how we were jumping around in one-cut increments there in January/February as 2024 started with hopes fears of a US recession. Since April, economic and interest rate volatility have been low to very low. This is consistent with FX and equity vol trading at near-subterranean levels.

Low volatility is the big story, despite wacky and wonky pockets of vol here and there. This tale of low volatility could be the story until we get much closer to the US election in November. Wake me up when September ends.

Macro outside the USA has been mixed with some mildly interesting stuff going on, for example:

These mild policy divergences have seen a few zippy moves in FX, and we will discuss those in the fiat currencies section later on.

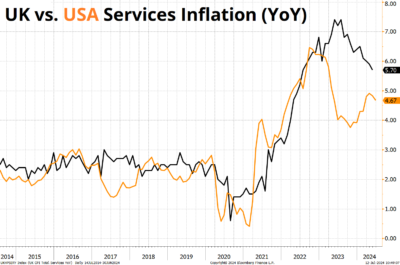

The Bank of England’s decision to focus on Services Inflation is a good example of how tricky monetary policy can be when you are allowed to choose from 15 or 20 different inflation metrics. In the US, Services inflation is lower, and the last two month-over-month readings have been negative. Still, US Services inflation is not exactly: Problem solved.

The theory that we are gradually normalizing back to pre-COVID levels in output and employment while prices remain a bit sticky due to structural changes in the labor market makes sense to me.

The big political story while I was off was Joe Biden doing an imitation of when you let go of the neck of a balloon and the air comes out and it makes a farting sound as it spins around the room randomly, then deflates and lands listless and limp to the floor.

Here is a 39-second highlight reel of Joe Biden’s performance over the past three weeks.

What does it mean for markets? Not a ton so far. He does seem to be good for steepeners because he will pressure the Fed while enacting inflationary fiscal and tariff policies. And a Trump win should be good for crypto as he will embrace it with open arms and put an end to the regulatory idiocy plaguing US crypto for more than ten years. But there are too many questions for now as we don’t even know if he’ll be running against Biden, Harris, or “other”.

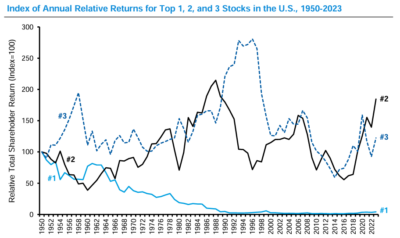

There have been volumes written about the concentration in the US stock market and the story comes down to two main views:

a) Concentration is a sign of danger reminiscent of 1999.

b) Margins and revenue growth justify a massive premium for megatech.

Unless you are a long-only tech fund manager, I don’t think you necessarily have to take a strong view on this. You can instead say:

I don’t want to short megatech because there is so much momentum and there is significant truth to the idea that operating margins at these companies mean they look like quasi-monopolies. Surveillance capitalism is winner-take-all due to network effects and while AI might be overhyped, not many people make money shorting bubbles.

While also saying:

I don’t want to own a 4.3 trillion-dollar company trading at 40X earnings. Basic history and valuation and “trees don’t grow to the sky” analysis suggests these could be bad investments on a multi-year time horizon. Michael Mauboussin has shown that owning the biggest market cap stock in the US is historically a super bad idea. Behavioral signs abound (i.e., the Signing of the Boob). The current structure of the major equity indexes does not provide diversification: It’s an all-in bet on tech.

Source link below

There is no rule that says you have to be long or short megatech. You can step aside and say: This is too hard. I will give up the potential gains without risking a short position. I will shift into equal weight SPX or something similar or buy RTY or something diversified.

You can play to win, or you can play to avoid losing. At these valuations, and this stage of the cycle, playing not to lose is a solid strategy. Especially when you can get 4.20% risk free with CPI at 3%.

If you are a person that likes to read smart stuff and learn about financial markets, Michael Mauboussin is one of the best writers out there. His piece about stock market concentration is the most balanced writeup I have seen on the topic. You can read it here.

I would be remiss in talking about the stock market without mentioning the blockbuster one-day rotation trade that happened after CPI. It’s not often you see a group of sectors up 3%+ while other large sectors drop more than 3%. That’s what we saw on Thursday.

In normal times, equity indexes tend to represent diversified portfolios of large companies. Now, they represent a tiny, concentrated portfolio of megatech. Invest appropriately.

Here is this week’s 14-word stock market summary:

Rotation shenanigans create substantial noise, but we are still near the ATH.

As discussed, the September rate cut is locked and loaded. Imagine a world of trend growth, trend inflation, and slightly restrictive policy and that’s what you’ve got right here. Market pricing is not always irrational or violently volatile. There are times when the market is right or close enough to being right and there isn’t a lot of money to be made taking the other side. That’s this market since April or so.

Despite clear slowing in growth, jobs, and inflation, there is very little evidence of recessionary headwinds and so US 10-year yields remain within the large triangle that has defined the price action for many months.

Depending on how you draw your triangles, and the thickness of your Crayola®, the support is somewhere around 4.05%/4.10%. So let’s say that if US 10-year yields close below 4.0% one day, something more significant has changed. For now, we’re still bobbing along near the center of the equilbirium zone that has dominated trade since this time last year.

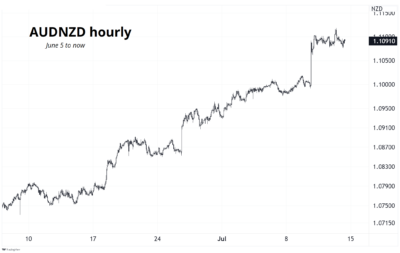

As mentioned earlier, the RBA is one of the few central banks where cuts are not on the table.

No big USD move still as the DXY remains moribund and rangebound. The moves have been in the crosses. For example, RBA on hold or maybe hiking vs. dovish RBNZ = AUDNZD up.

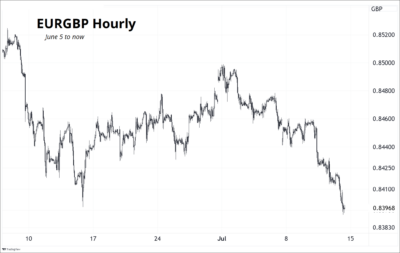

Hawkish Bank of England (Chief Economist Pill this week, especially) and a steady-as-she-goes fiscal policy.

Is trump bullish or bearish USD? Nobody knows. Loose fiscal, tariffs, political pressure on the Fed, stated weak dollar policy vs. actual strong dollar policies… It’s confusing. One or two cuts from the Fed and a 4.2% 10-year yield doesn’t scream LOWER USD! Nor does it suggest the USD should rip. Nothing to see here.

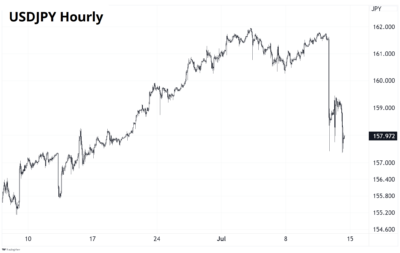

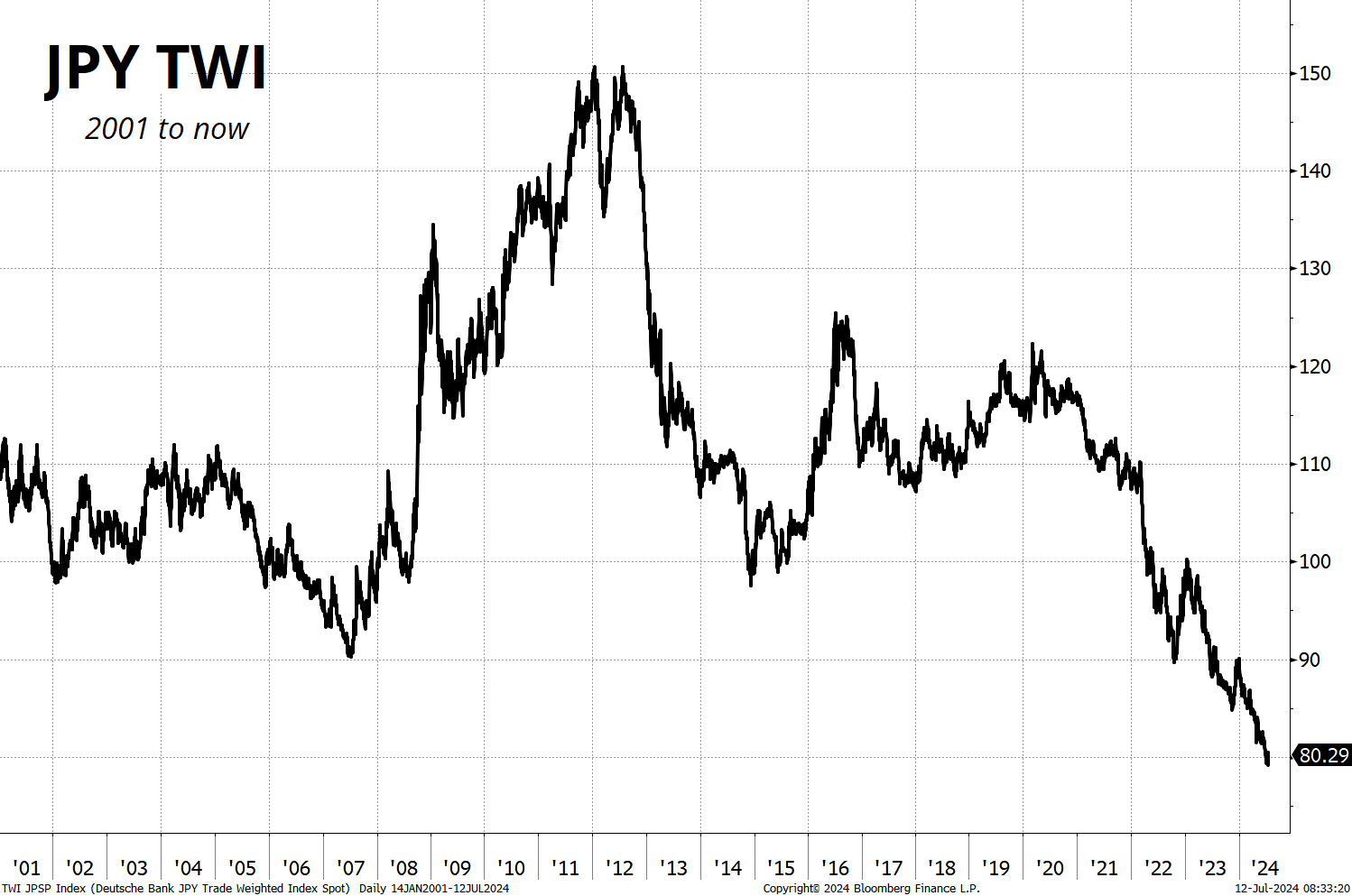

Elsewhere in fiat world, the Japanese Ministry of Finance put its boot on the neck of USDJPY again, in another attempt to stem JPY weakness. That leads to this fugly chart:

The nature, strategy, timing, and tactics around JPY intervention have changed.

Still, all they can do is put temporary floors under the JPY. They can’t push it higher without some cooperation from the Fed, BOJ, and global asset market volatility. As long as vol is low, the level of carry in USDJPY will attract speculative money. Momentum and levels of interest rate differentials suggest that USDJPY is high, but that has been the case for a few weeks as USDJPY started rallying up and away from rate diffs in early June.

It seems likely that USDJPY’s path of least resistance is sideways to small down from here. As long as volatility is low, there’s no panic.

There is a sizeable wedge between bitcoin and QQQ right now as tech stocks are close to the all-time highs and up 11% in six weeks while bitcoin is 20% off the highs and down almost 20% in those same six weeks. The reason is simple: The bitcoin ETF buy flows petered out just as Mt. Gox and German sell flows appeared.

These sell flows are not infinite, but they are not even close to being done as Mt. Gox still holds 141,000 BTC and Germany holds 23,000. You can read an excellent thread (via Sol) right here.

My view is:

The crashy and volatile nature of BTC makes it a perfect security for those who have patience and a willingness to leave limit orders. I would scale buy orders between 50,000 and 53,000 and pray for sloppy selling.

Recall that 49,250 was the post-ETF launch mini-top and buy rumor / sell fact level and then we consolidated before a clean break of 50,000 and Space-X style launch to 73k. As such, I think 50k is the megasupport and even with those giant sell flows yet to come, you can’t hope for much more of a discount than that as NASDAQ trades above 20k.

If your spine is made of titanium and you have giant globes, you could make try short NVDA / long BTC as a pair trade. Good luck with it.

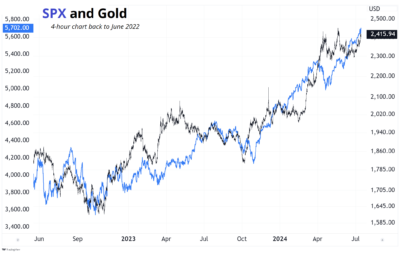

Gold is the risk-averse man’s SPX these days as they move together but gold is up 40% from the lows while the S&P 500 is up 60%. Both are hedges for global fiat debasement and both are serving the same purpose right now. Silver is trying to join the party but can’t seem to get legs for some reason as it’s still trading $30 vs. ATH of $50 while gold is tickling the ATH as I type.

The rest of the commodity complex is mixed as the BCOM drifts in a 95/110 range, unchanged vs. mid-2021. Lumber, corn, and wheat are trading like absolute dawgmeat.

OK! That was 8 minutes. Thanks for reading Friday Speedrun.

Get rich or have fun trying.

Smart, interesting, or funny

This week we talk about the Fed, Trump, the USD, and managing the psychology of low vol markets when your primary strategy is directional macro, and your performance is positively correlated to volatility. Note that the link also always includes a transcript for your reading pleasure in the show notes.

Less boring than it sounds!

Mesmerizing.

Music

Three excellent early 1990s songs about alcoholism.

1993 Moxy Fruvous: Drinking Song

This is one of the most beautiful and sad story songs I know. Listen to the lyrics all the way through, alone, in a quiet place. That final verse hits so hard.

1993 TOOL: Sober

One of my favorite songs, ever. Uses the same chord progression as Led Zeppelin’s Kashmir.

One of the most recognizable opening chords in rock music. Still a haunting song, 34 years after its release.

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.