Soft landing continues

Schrödinger’s Sign

Soft landing continues

Schrödinger’s Sign

Flat

NFP comes in pretty much on the screws and the wind comes out of the market. And things get worse next week as we have very, very little data, with CPI mid-week and not much else to get excited about. This figure should be great for carry, great for stocks, and bad for directional macro. The soft landing is intact.

Looking forward, you can argue that the deficit story could come back to the fore if the Big Beautiful Bill passes, but momentum there is not strong and the optimistic date for that is July 4. You can argue that trade deals are coming before July 9, but they are mostly going to be thin on details and big on hype and so the market will probably not react much to those. You can wonder if the US economy will slow down as the policy uncertainty starts to bite, but you won’t get any evidence of that next week. And CPI isn’t a huge focus because even if it ticks up, we won’t have a good handle on whether this is a one-time bump or a meaningful uptick in inflationary psychology for many, many months.

It’s a good time for me to get flat and wait for a new idea. I am even going to square up the platinum long as we are now approaching the 2022 highs, it’s extremely overbought, and I feel like it would be nice to come into next week with a completely clear mind and fresh, unbiased outlook. My square up is probably more about my own personal psychology, but I do also believe you will probably get better levels to rebuy.

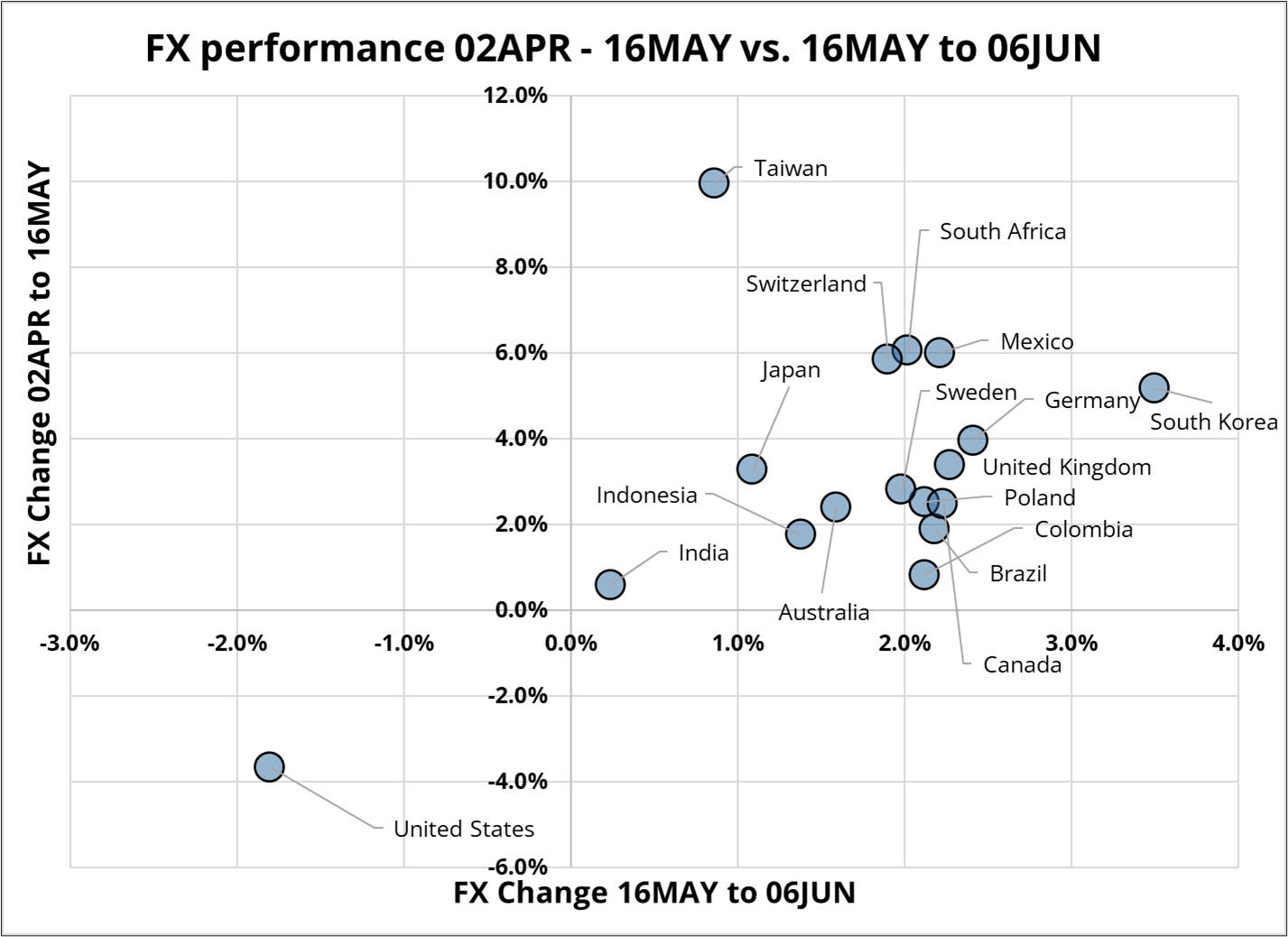

In mid-May, I wrote about how the market was trying to balance the desire for long carry with the desire to be long countries with positive NIIPs. I was curious how things played out after that piece.

Filtering for NIIP or for carry doesn’t show much evidence of a theme in FX moves since 16MAY. Returns have not been all that dispersed with pretty much every major currency up 1.5% to 3% vs. the USD in that period.

This is very mild across-the-board USD weakness with no major underlying theme or dispersion when it comes to carry or external balances. Despite the underwhelming price action, the USD continues to trend lower (in fits and starts) against most major world currencies.

That makes sense as the bond vigilantes lost their mojo once the Big Bill passed the Senate and specs realized there was going to be no new information on the bill until at least July 4, or on tariffs until near July 9.

A Nikkei article overnight highlights the lack of coordination among US officials as three negotiators push separate agendas in the same trade talks.

TOKYO — The presence of three top U.S. negotiators with differing stances on trade is adding a layer of complexity to tariff talks with Japan.

Open disagreements, competition and confusion among Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick and U.S. Trade Representative Jamieson Greer have made it hard for the Japanese side to judge the Trump administration’s intentions, according to sources close to the negotiations.

“At one point, the three cabinet officials put the talks with the Japanese side on hold and began debating right in front of them,” said one source.

“The three officials are competing for credit,” said another source close to the Japanese government who speculates that they may be trying to curry favor with President Donald Trump. Bessent and Lutnick were once rivals in the race to become treasury secretary.

In addition to the lack of unity among Bessent, Lutnick and Greer, Tokyo is also concerned about the insufficient coordination between cabinet officials and working-level staff. Tariff negotiations typically involve technical issues being hashed out at the working level, the details being set at the cabinet level, and a final agreement being reached by national leaders.

In the current talks, “the three tiers in the U.S. — the working level, cabinet officials, and the president — are disjointed, and it appears that information is not being shared,” said a senior Japanese economic official. The Japanese side frequently needed to repeat the same things at the working- and cabinet-level talks, the official added.

Trump has the final say on tariffs, but his intentions are unclear. It is difficult for Tokyo to determine what the administration wants and what concessions are necessary to reach a deal.

The US Treasury’s semi-annual currency report contained two items of note. First, some unsolicited advice on monetary policy in Japan:

BoJ policy tightening should continue to proceed in response to domestic economic fundamentals including growth and inflation, supporting a normalization of the yen’s weakness against the dollar and a much-needed structural rebalancing of bilateral trade. Treasury also stresses that government investment vehicles, such as large public pension funds, should invest abroad for risk-adjusted return and diversification purposes, and not to target the exchange rate for competitive purposes.

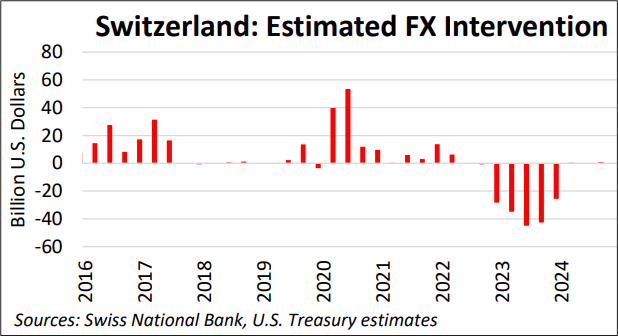

Second, they added Switzerland to the list of countries on the Monitoring List. While the SNB uses currency intervention as part of its monetary policy toolkit and not explicitly to weaken the franc to benefit exporters, this does complicate the politics of any future SNB intervention in EURCHF. Neither country is likely to care much about these US comments as the Semi-Annual Currency Report has been somewhat toothless over the years and feels more like a box-ticking process than an important geopolitical input into foreign currency intervention decisions.

If you are newish to foreign exchange, I would recommend reading the report as it contains significant useful background information on various countries’ external balances.

https://www.dwarkesh.com/p/timelines-june-2025

![]()

Have a useful weekend.

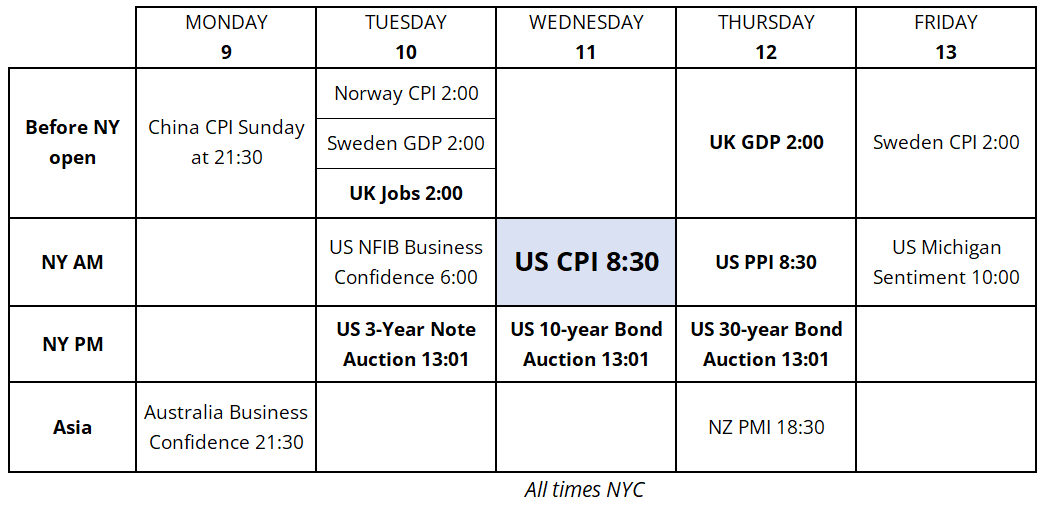

Calendar for the Week of June 9, 2025

Schrödinger’s Sign