Big 360 on the Fed.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Big 360 on the Fed.

Hello. It’s Friday. Thanks for signing up. I’m Brent Donnelly.

The About Page for Friday Speedrun is here.

Here’s what you need to know about markets and macro this week

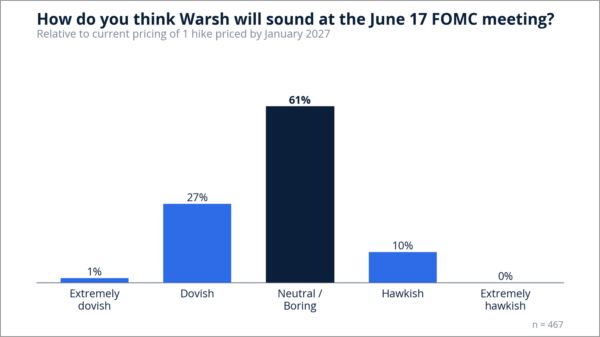

Quite a lot has happened since I published the last Friday Speedrun on June 5. I went to Ireland, for example. But that’s not what I mean. The most interesting and surprising thing that happened was Kevin Warsh came out directly against the doves and proclaimed that the Federal Reserve is finally serious about inflation. It’s worth noting that Powell said this too. Every central banker says this. But the market was caught wrong-footed as going into the first FOMC Chaired by K-Warsh, I did a survey and the respondents said this:

Oops. The market is not always right. Whoever invented that saying probably doesn’t outperform the index. Plenty of pixels have been spilled about Warsh, and at this point my view is that the market has taken things too far, going from one extreme (2 cuts priced right before the war) to the other (1.5 hikes priced after the war).

I see a macro backdrop that looks similar to pre-war. At that time, we were pricing in two cuts and now we’re pricing in 1.5 hikes. That seems wrong to me.

The two biggest counterpoints to my dovish argument are:

Headline NFP growth has been super strong since the start of the war. This is true and it’s the best pushback against a dovish view. And yes, inflation is about more than just oil—memory and AI capex are inflationary. But oil still dominates.

Warsh really wants to get inflation back to 2%. If that’s true, I will be wrong and I will lose money. The Fed has essentially allowed 2.8% to be the new 2.0% for years and if Warsh wants to crush the last mile of the inflationary pressures that started after COVID, he’s going to need to hike aggressively.

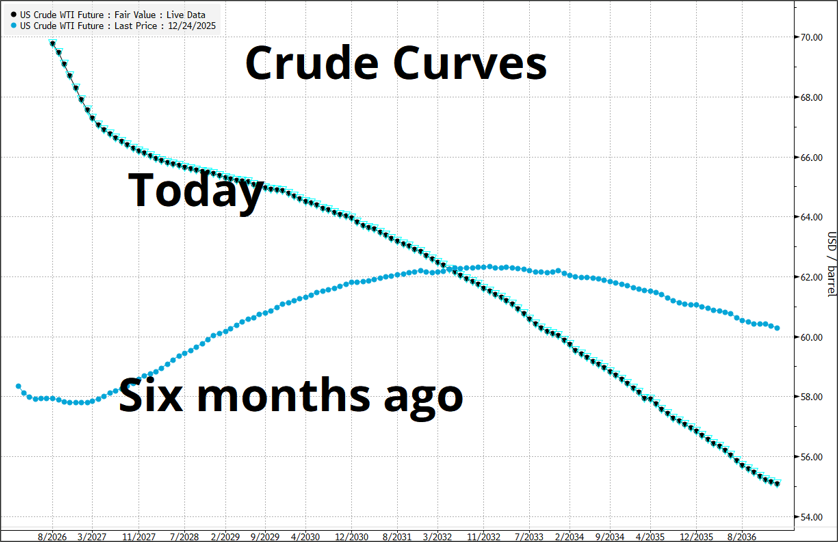

Take a look at the crude oil curve compared to where it was six months ago. Wow. The back end is significantly lower despite four months of closure in Hormuz.

Going forward, the trajectory of prices looks like this:

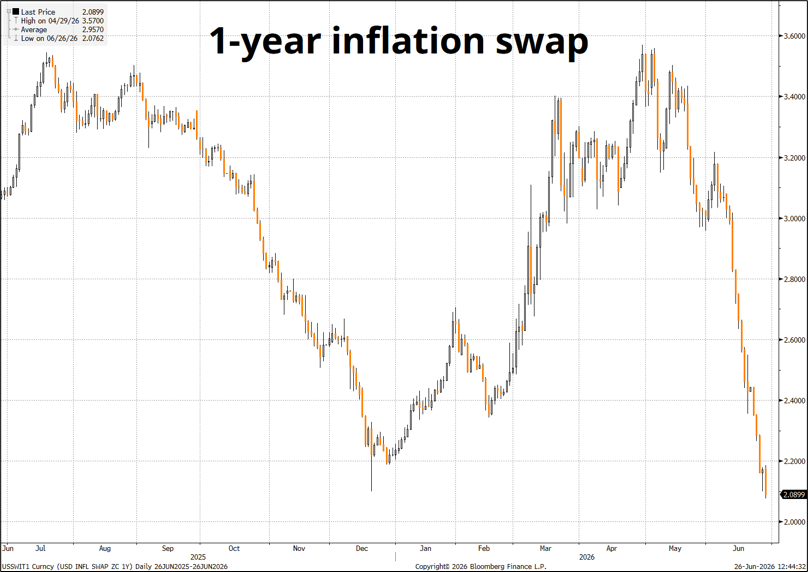

And 1-year inflation swaps are doing this:

After debating the current setup with a bunch of clients this week, I think you can basically boil it all down to one question: Do you believe Kevin Warsh? Personally, I do not believe him nearly to the extent that the market does. I believe as soon as inflation starts to fall, which it will, he will back off the hawkish talk and move towards something that sounds more like: “We’re winning on inflation and there is no need to panic.” The fear of second round effects should be completely gone here as there are now no first round effects. You can’t have second round effects without first round effects!

That would seem like a quick flip, but remember a month or two ago he was dovishly-focused on Trimmed Mean inflation because it’s still bobbing around near 2.0%. Central bankers have unlimited data sets, sliced and diced a zillion ways, and they can always come up with data to match their current policy preference. I would not be surprised if we are soon back to the old: “Inflation will be back at 2% within 2 years” FOMC permaforecast.

New Fed chairs like to sound hawkish. October 3, 2018, a new Fed Chair (Powell) got too hawkish, saying “we are a long way from neutral” and everything blew up. Real rates went to 2% and stocks cratered.

Now, a new Fed Chair (Warsh) got super hawkish, and real rates are up around 2% again. Stocks are not loving it. But the real takeaway (for me) is that 2-year yields peaked November 9, 2018, as tightening financial conditions turned everything around in a month. Here is a chart of 2s at that time.

I think Warsh’s opening hawkish gambit is partly performative and the bar for him to flip less hawkish is snake-belly low. We are probably close to a peak in 2-year yields as the market is max short 2’s and Warsh went berserk in a bid for credibility on day one. Inflation is going to come down as oil and other commodities fall and financial conditions tighten.

The great fertilizer panic of 2026 is over. The nearly impossible to believe reality is that the Strait of Hormuz closed for almost four months—an absolute worst-case scenario according to most analysts—and yet nothing happened. Oil was $70 in January and now it’s $70. Corn prices are lower. Fertilizer is unchanged. Crazy.

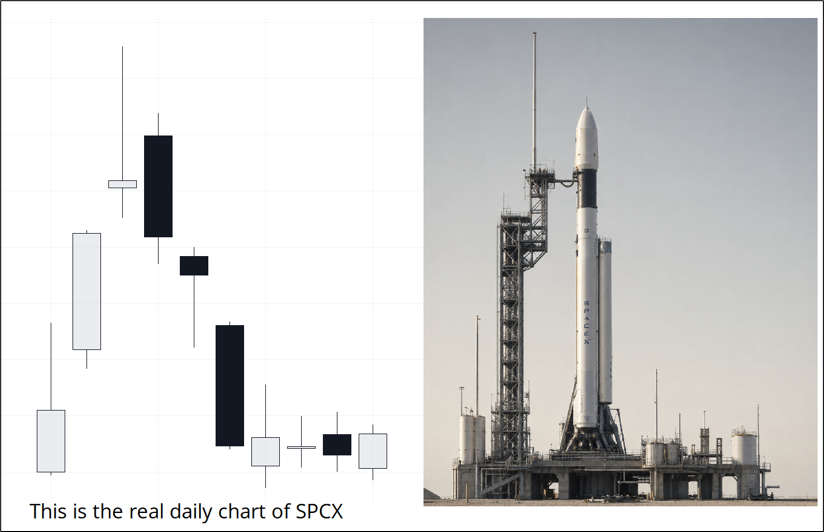

The SPCX IPO is out of the way, and it went pretty much exactly as most people predicted. Up until you could go short and buy puts, then down.

The daily chart of SpaceX looks like a rocket sitting on a launch pad.

Of course it does.

The broad market is struggling a bit under the weight of a stronger USD, tighter financial conditions, higher real rates, a hawkish Fed, and nerves around the ongoing collapse in gold, bitcoin, and oil. If you recall what happened after Powell errantly turned temporarily hawkish in October 2018, the stock market collapsed on Christmas Eve of that same year. Then, the calvary came in, the Fed cut, and we were off to the races again.

Semis remain the only game in town after Micron’s decidedly insane earnings numbers. Have a look at the progression of company earnings.

This is what Gwen Stefani would call bananas. B-A-N-A-N-A-S.

Fun fact if you watched that video: Stefani was 35 years old when she made it. Wild.

Going into Micron’s earnings release, I expected the market to sell the stock on just about any outcome, but that was completely wrong and it rallied from 1030 to 1250. Now, it’s struggling to make headway and has carved out a triple top up there. Let’s see what happens next week!

Here is this week’s 14-word stock market summary:

Choppy / unchanged since May. Earnings are still good, but the Fed is hawkish. So????

https://www.spectramarkets.com/subscribe/

I am bullish 2s because I don’t think Warsh will deliver on his hawkish message, nor will he need to. I think inflation has peaked and it probably peaked a month before Warsh burst onto the scene squawking hawkishly. The timing could be ironic, as it was in October 2018.

You can play 2-year notes through futures, cash, or call spreads. I think the ideal timing for bullish derivative bets is something expiring in September because the July meeting is overpriced at 20% and the September meeting is overpriced at 75%.

I will, however, state here that there is an alternative hypothesis where I am completely wrong and Warsh actually DOES want to push inflation lower. If that is what happens, they could feasibly hike rates in July to send a message of like: We’re serious. The jobs market is strong and current measures of inflation are high. If you decide you’re going to base policy off current data, not forecasts, it would make a ton of sense to hike right now and lay down the law for all the doubters out there (like Brent Donnelly, for example). Hiking rates into a collapsing oil price doesn’t feel like a winner to me, but it could happen.

The rate cut fever that preceded the nomination of a new Fed Chair, and continued after Warsh’s appointment, is now a rate hike fever. Fevers don’t usually last.

I will definitely not say that I’m 100% confident here. I think NFP and July FOMC will provide substantial clarity.

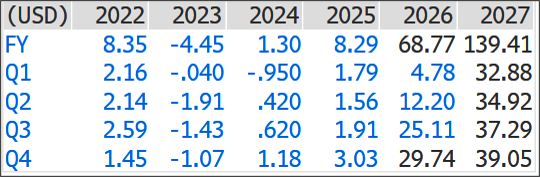

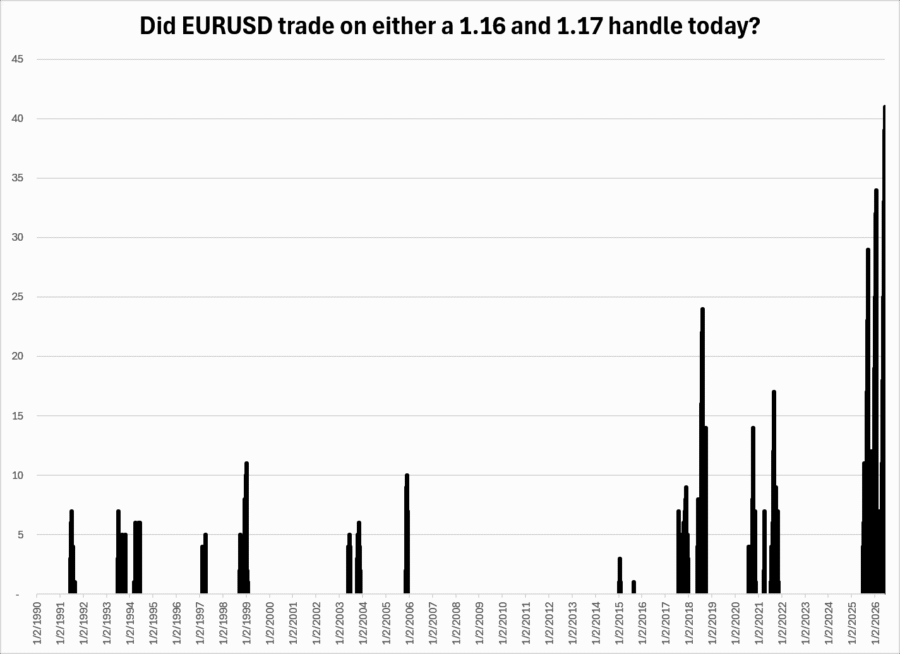

I published this humorous chart on June 5:

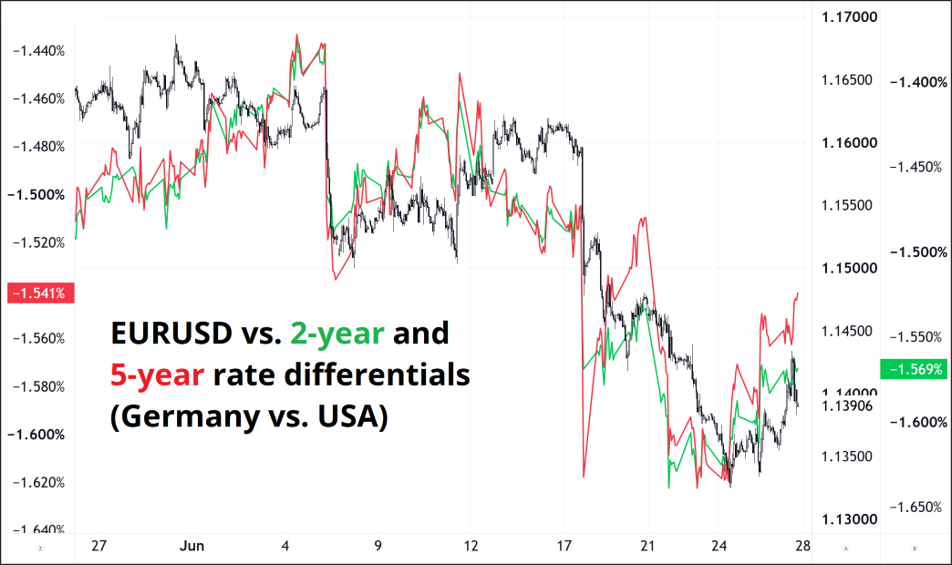

EURUSD finally broke out of the boring low-vol regime that day, and has been slipping and sliding to a low of 1.1330. Warsh did most of the damage with the hawkish FOMC meeting on 17JUN and EURUSD has been obediently following rate differentials before and after that day.

If I am right about lower U.S. rates, it’s likely I will be right about a lower USD too as I am bearish USDJPY and USDMXN specifically and will probably add USDKRW next week. There is a certain feverish element to the USD bullishness out there and the data suggests the trade is crowded. As corporate USD buying peters out into the end of the month, I think USD bears will have a pleasant July. This is a new view, and I have been putting on the trades for clients in the last two days.

These are just my views; definitely not investment advice!

The crypto DAT stupidity and new worries about whether or not Saylor has any plan to pay back MSTR’s monster debt load are pushing the digital coins lower. I wrote on June 5 that the death spiral narrative was taking hold and it’s in full command right now.

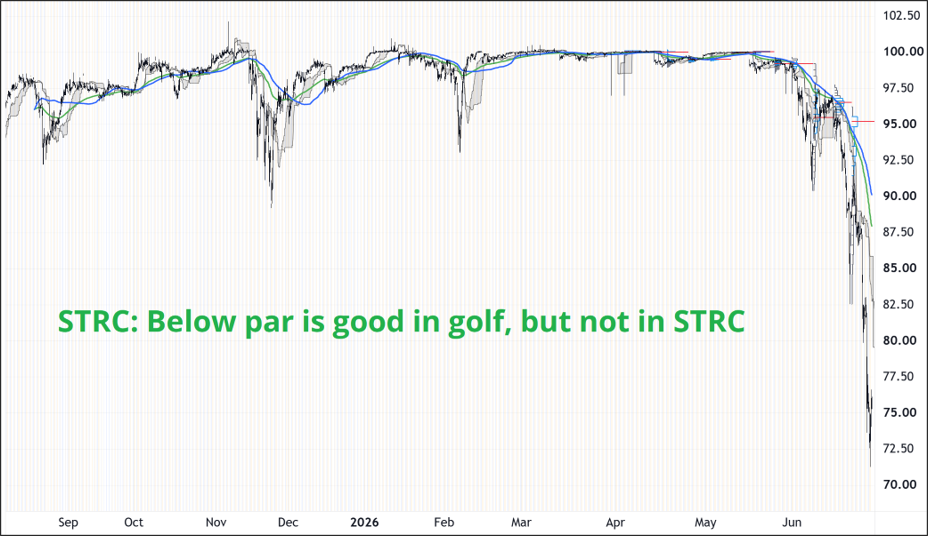

As the death spiral / contagion theory is in full force, we may start to see some true craziness in STRD, STRF, STRK, and STRC as the market prices in the fact that the mechanics behind the MSTR Rube Goldberg machine look a little bit too much like the mechanics behind LUNA. Saylor needs to come up with billions, and the collateral is getting trounced. That has led to a bloodbath in STRC (for example)—a product that was loosely advertised as a fixed-income like instrument but trades more like a non-linear doom loop bet / value trap.

Here are some headlines from the 2025 scrapbook.

In the end, as many predicted, the crypto DAT thing is purely a stupid procyclical Rube Goldberg machine that leaks cash and there is (surprise!) no such thing as an infinite money glitch. Sadly, Saylor’s antics sucked in a lot of people who are new to markets and may have believed the PT Barnum madness.

Now STRC is $74, Bitcoin is 60k and here we are. In 2022, Saylor survived because there was no reason for him to sell bitcoin. He had nothing to pay back. Now, a wall of converts and dividend payments lay not too far ahead, and he will have to keep issuing stock or selling bitcoin if he doesn’t get a kick save from a giant bitcoin rally before 2027.

That par joke is bad, but there is a much funnier one later.

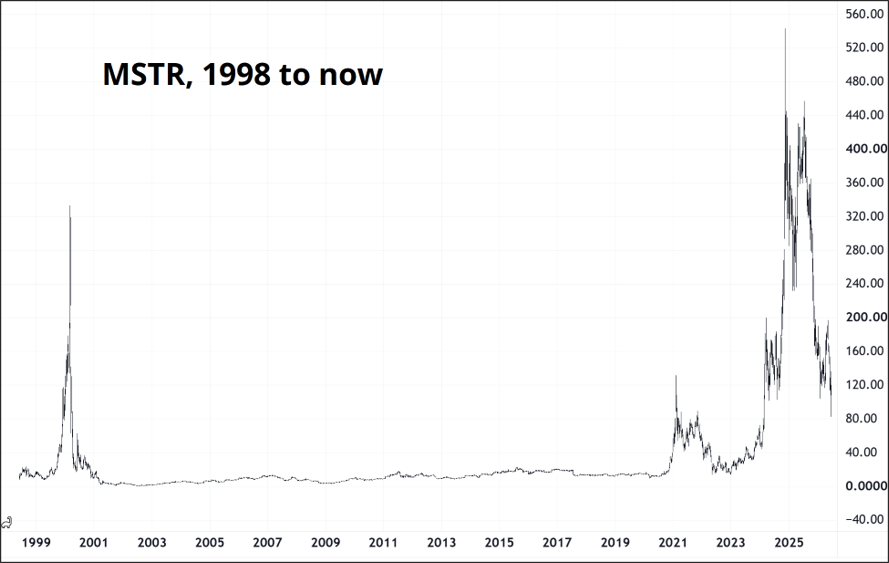

The smart and talented Felix Jauvin likens MSTR to the final boss as BMNR, UPXI, NAKA, etc. etc. have all been taken to the woodshed and now it’s time to see if the market can finish off MSTR too. Here’s the long-term stock chart, which explains why anyone who was around in 1999 stayed a million miles away from MSTR over this cycle.

This story is not yet fully written, but I find it incredibly hard to imagine the market will ever come back to crypto the way it did in 2018, 2021 or 2025. And the MSTR debt clock is ticking.

Tick.

Tick.

Tick.

Imagine I told you in February: Hey, I have some cool secret info. The Strait of Hormuz is going to close early March and still be effectively closed in late June. Oil is trading at $67. What odds will you give me that oil is below $70 at the end of June?

Umm. Dude. Like… 20:1? I’ll pay you 20:1.

Ok. Done.

Forecasting is hard! Even if you have all the information, things don’t always make sense. Next time you see a bunch of hysterical stuff about product X or stock Y or commodity Z… Remember. Extrapolation and forecasting are not the same thing.

The good news is: The Economist nailed it again. Uncanny.

https://www.spectramarkets.com/amfx/the-magazine-cover-indicator/

That’s it for this week.

Get rich or have fun trying.

Absolute banger of an article from Adam Butler

https://www.panoptica.com/the-neuro-metaphysics-of-ruin/

Do yourself a favor and allocate fifteen quiet minutes to this. It’s so good.

*************

I do feel “expired at par” would have been funnier, Ed.

*************

Music 1: New Phoebe Bridgers Song!!!!!

First new album since COVID (June 2020). She is the bestest.

The last 15 seconds of the video are the best part.

Music 2: 1970s African Disco yeah baby yeah

Music 3: Cool vibes from Quantic

*************

*************

Thanks for reading the Friday Speedrun! Sign up for free to receive our global macro wrap-up every week.