Payrolls Thursday!?

Today’s data is dated, but I suppose a negative print might get people excited. That outcome would be bearish for a few minutes, then bullish as the market reprices December FOMC back to 80% (from sub-50% right now). The obsession over December FOMC is misguided as 2026 pricing is the more relevant metric for asset prices.

USDJPY

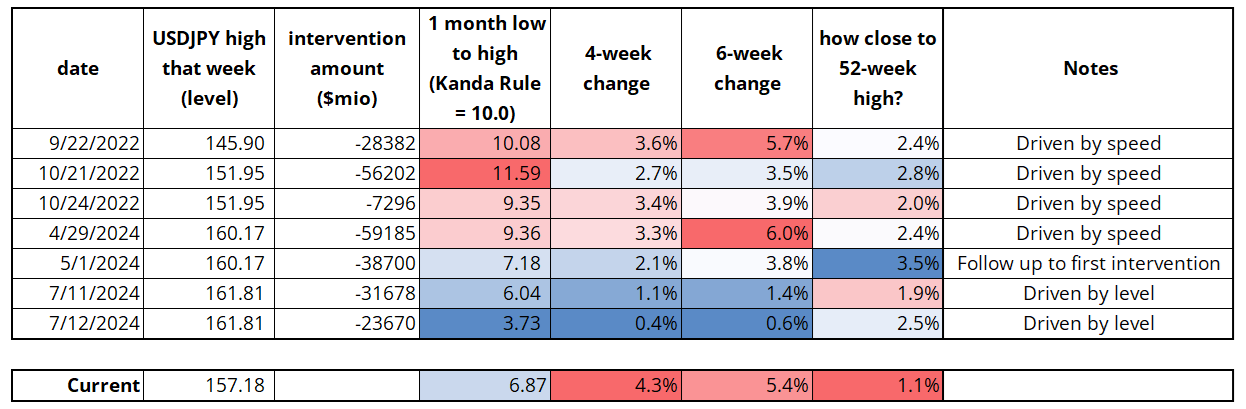

We have a different finance minister now (Katayama vs. Kanda) but here are the measures of level and speed around the last USDJPY interventions. We are in the red zone on everything except the Kanda Rule. This probably means the risk reversal is wrong here (USDJPY puts should be bid soon as the market positions for, or hedges against, intervention).

Note that the MOF intervened after CPI on July 11, 2024, so if NFP is weakish it’s best to be on the ready in case they do the same and slam USDJPY after jobs.

USDJPY intervention data from: https://fred.stlouisfed.org/series/JPINTDUSDJPY

Any impact from USDJPY intervention is likely to be temporary as dovish fiscal and negative 2% real rates cannot be fought for very long with 10B of USD selling here and 10B there. Buyers will emerge 152/153.

Notice on the table above that each intervention came after a new high in USDJPY, so you could argue that 162.25 (new cycle high) is the absolute highest the MOF would allow USDJPY to get without intervening. First, we probably get a rate check around 158.50/00, then things escalate as 160.00 approaches. The closer we are to 160, the more the risk reversal should go bid for USD puts.

NVDA

AUDJPY was a good play through NVDA as the stock rallied and AUDJPY went up a fair bit. Friday 101.80s were trading for 20bps with spot at 101.30 yesterday morning and now AUDJPY is above 102.00. Let’s see what NFP brings. My presumption is that an in-line number will lead to another leg higher for stocks and cross/JPY as the market has spent a full week going to full raging bear mode in stocks and has little to show for it. 24300/24400 held perfectly in NASDAQ futures and it’s going to be hard for the bears to hold on into the weekend. NVDA was the last bear catalyst unless September NFP somehow ends up important (which I don’t think it will be).

Options markets were pricing a 7% move in NVDA so that would target 199.50 as a stretch point for the stock this morning (186.50 close X 1.07). $205.68 is the $5 trillion market cap level that was temporarily breached before Sorkin rang the bell at the top. The all-time high is $212.

For your 2026 radar

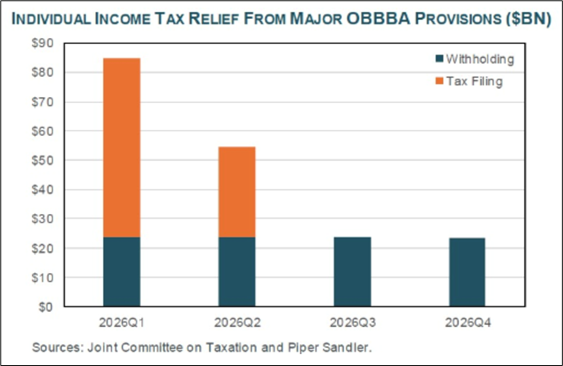

On August 7, the IRS announced that it would not be adjusting W2 or 1099 tax forms for the 2025 calendar year. This, despite the fact that many of the provisions in the OBBBA are retroactive to January 1, 2025. That means that Americans will get larger than normal tax refunds in Q1 2026. Piper Sandler estimates $91 billion of tax relief could arrive between February and April 2026, with $59 billion paid via refunds and $32 billion from lower taxes owed, while JPM sees a huge surge in refunds coming too.

https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/notes-on-the-week-ahead/the-investment-implications-of-the-refund-surge/

Here’s a graphic from Piper Sandler:

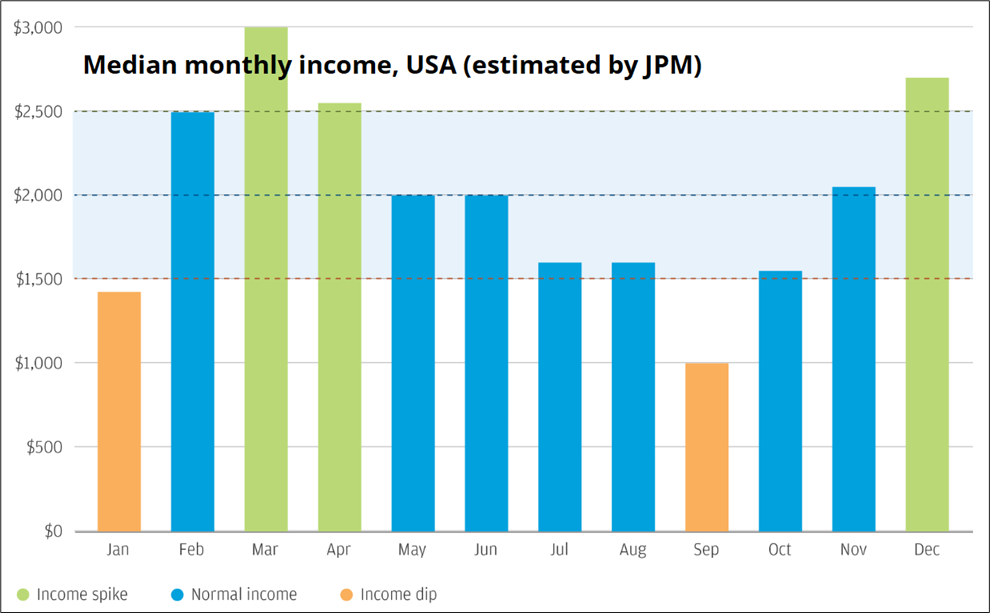

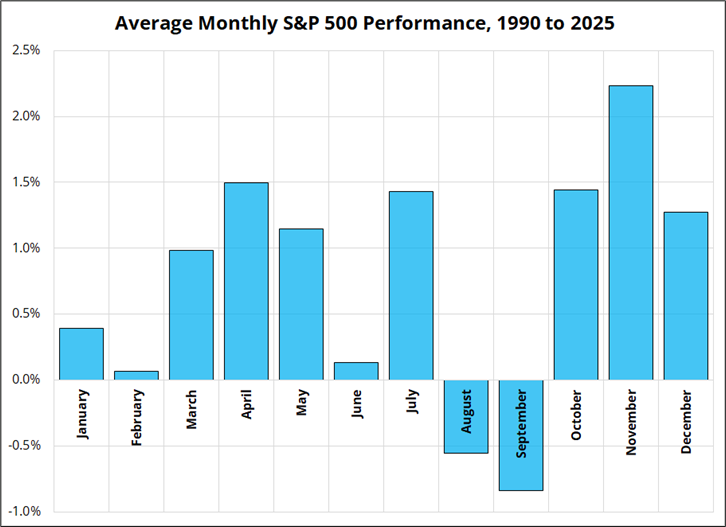

One of the reasons for equity seasonality is the flow of income to households. Here, from JPM, is an approximation of US median income, by month. On the right is the seasonality of equities. A fixed percentage of many US incomes goes directly into 401ks and directly into the stock market, so income surges should lead to inflow surges and higher stock prices, all other things being equal. Flow does not completely dominate, of course, as we saw in April 2025 when tariff fears overwhelmed any positive flow story.

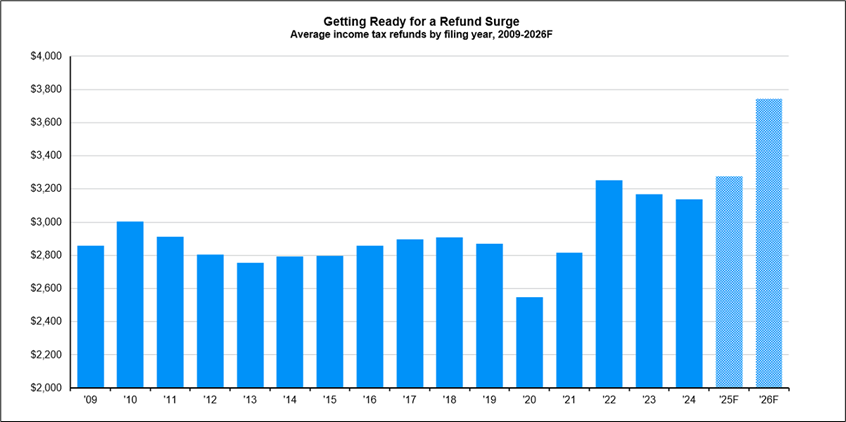

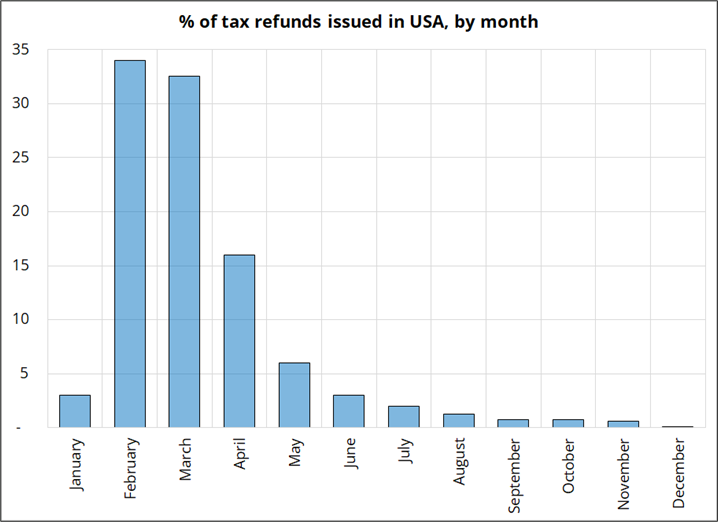

Today, more than ever, free money dropped in US bank accounts flows into stocks and crypto, and February, March, and April 2026 will probably see some of that. More than usual. Tax refunds are mostly sent out between February and April as the early filers receive the largest refunds and those begin flowing 15FEB. See chart here.

No call to action here, I just thought this was interesting as it’s part of the bullish fiscal/liquidity story for Q1 2026. I think the equity selling is burnt out now and the market will soon want to start getting long for 2026. Bullish. Good luck with NFP!